Article contents

If you’ve owned a property before, you won’t qualify for Stamp Duty relief or most government schemes like shared ownership – even if your partner’s a first-time buyer.

In the market for a new home? Buying with someone who’s a first-time buyer? Here’s all you need to know if you’ve owned a property before but your partner hasn’t.

First things first, let’s get one thing straight: what exactly counts as a first-time buyer?

According to GOV.UK, ‘A first time buyer is defined as an individual or individuals who have never owned an interest in a residential property in the United Kingdom or anywhere else in the world and who intends to occupy the property as their main residence.’

Don’t worry, it’s not as complicated as it sounds!

Basically, to be classed as a first-time buyer, you need to have never owned a home before. In the government’s eyes, you also need to be buying a home to live in rather than a property to rent out. Simple!

So, why is it so good to be a first-time buyer?

Well, as a first-time buyer in the UK, you’ll get lots of benefits as the government is trying to make it easier for people to get on the property ladder. But a lot of them can’t be accessed if you’re buying a home with someone who’s not a first-time buyer. Urgh.

Tembo will find your best deal, fast, all with award-winning service.

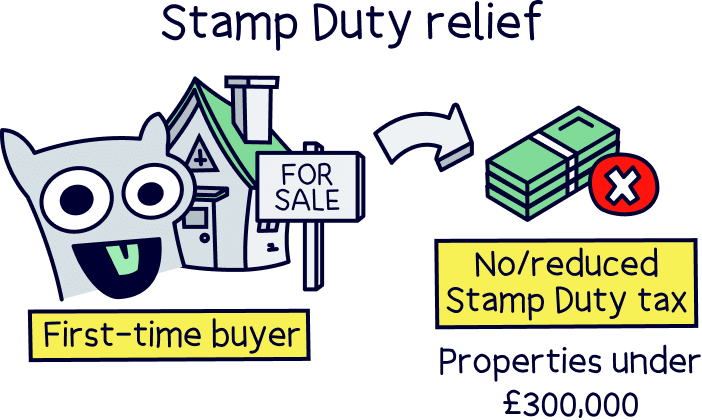

Yes. We hate to break it to you but unless everyone buying the property is a first-time buyer, you’ll have to pay Stamp Duty. Sorry! The only exception is if the property you’re buying is under £125,000 (£300,000 for first-time buyers) in which case, you won’t have to pay any Stamp Duty no matter if you’re a first-time buyer or not.

Nuts About Money tip: find out how much stamp duty you will have to pay to buy a home with our Stamp Duty calculator.

Stamp Duty Land Tax is a tax that’s charged when you buy a property. However, first-time buyers don’t have to pay it as long as they’re buying a property that costs less than £300,000, thanks to a scheme called Stamp Duty relief.

It's worth mentioning our Stamp Duty calculator again, you can find out how much you'll have to pay based on your own circumstances.

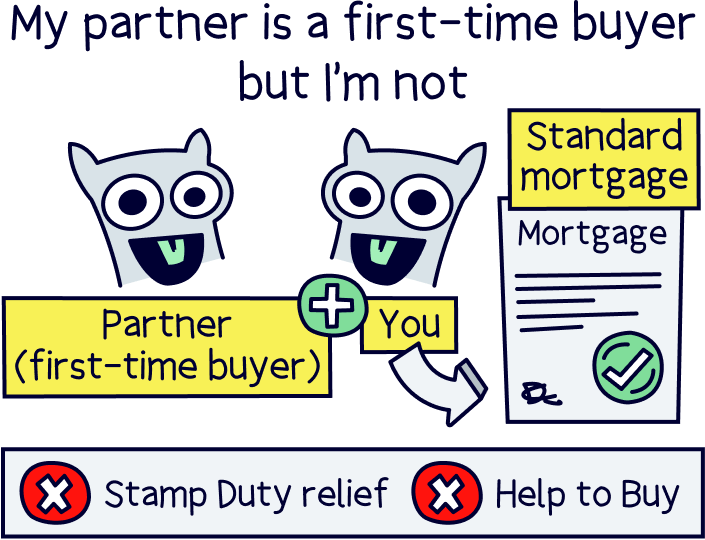

Sadly, if you’re in a couple and your partner is a first-time buyer but you’re not, between you, you’ll still need to pay the full Stamp Duty tax.

The only way that you could get away without paying it is to make your partner the sole owner of the property. However, there are a couple of problems with this.

First, it will only work if you’re not married or in a civil partnership. If you are, we hate to break it to you, but you’ll legally count as one buyer. So, even if your partner has never bought a property before, the law will act as if they have.

Second, buying the property in just your partner’s name probably isn’t the best idea. You wouldn’t have any legal ownership of the property which could be problematic if there are any disputes later down the line. Plus, only your partner’s salary would be taken into account when you came to apply for the mortgage. So, you wouldn’t be able to borrow as much money as you would if you were both applying together.

Ultimately, it’s probably going to be easiest to just bite the bullet and pay the tax.

Nuts About Money tip: find out how much you could borrow on your own or in a couple with our mortgage borrowing calculator. Also, calculate the total moving costs and the mortgage needed with our moving cost calculator.

Most of the time, no. There’s not much help available for a first-time buyer who’s buying with someone who’s owned a property before. That said, there are a few different schemes out there and they all have different eligibility criteria. Below are the main ones and who qualifies for them.

Note: If you want any help with these schemes, speak to Tembo¹. They specialise in them, plus, you'll get 50% off their standard fee with Nuts About Money.

The Help to Buy Equity Loan is a government scheme that helps you buy a new-build property by loaning you a maximum of 20% of your property’s purchase price (or up to 40% in London).

Sounds great right?! But bad news: it’s only available if both you and your partner are first-time buyers. So, sadly, you can’t access the help if one of you has owned a property before.

Not only that, but if you’re married or in a civil partnership, you have to make a joint application. So, unless you’re unmarried, even if your partner wanted to buy a property using the scheme on their own, they wouldn’t be able to.

Shared Ownership is a scheme that lets you buy a share of a home if you can’t afford to buy the whole thing. You basically pay rent on the part you don’t own until you can afford to buy the rest.

Sound appealing? Good! Because this scheme is open to first-time buyers and people who have owned homes before. Hooray!

However, to qualify you’ll need to show that you can’t afford to buy a home without help. Between you, you’ll also have to earn less than £80,000 per year (or less than £90,000 per year in London).

But be very careful with this scheme. In fact, we’d advise to stay well away. You’ll never own the property outright and you’ll be liable for a vast range of hidden fees through a regular service charge you can’t escape from. As far as we’re concerned, it’s just not worth the stress!

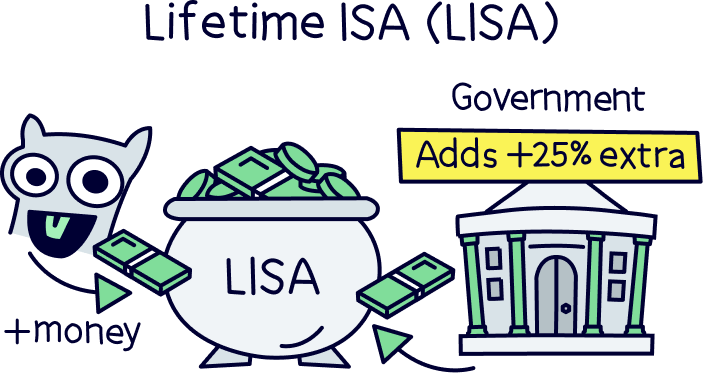

A Lifetime ISA is our favourite kind of bank account that can be accessed by new applicants.

So, what exactly is it?

Well, it’s a savings account that helps you save to either buy your first home, or to tide you over later in life. You can pay up to £4,000 into it each year and the government will give you a 25% bonus on the money you put in there.

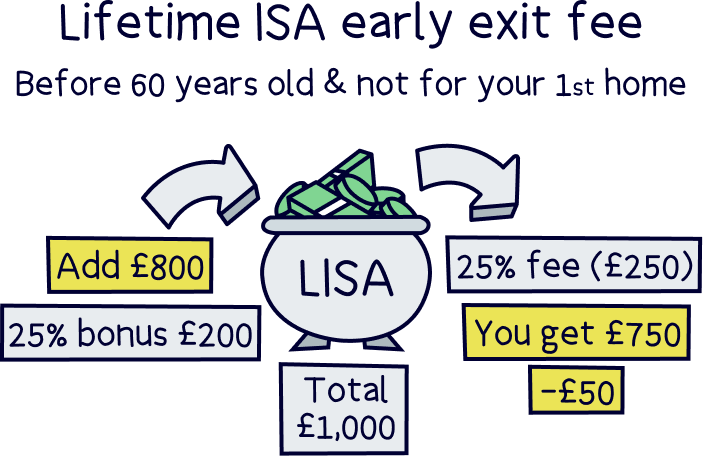

Just bear in mind that you need to make your first payment into the account before you’re 40. Plus, you can’t add into it anymore after you’ve turned 50. You can also only use it to buy your first home if the property costs less than £450,000.

The great thing about a Lifetime ISA is that as a first-time buyer, your partner will be able to use it even though you’ve owned a property before. In fact, if you have a Lifetime ISA of your own, you can use yours towards the home too. However, you’ll have to pay a hefty 25% withdrawal charge to do so, which means you’ll technically lose more than the bonus you get – so it’s not really worth it.

Nuts About Money tip: see how much you could save with our Lifetime ISA calculator and compare the top Lifetime ISAs.

No, you can’t lie about being a first-time buyer. At least, we wouldn’t.

Most government schemes will need you to sign a declaration to confirm you’re a first-time buyer. If you lie on this and it later turns out you weren’t telling the truth, you could lose your property. Worse still, you could be committing a criminal offence, which is pretty serious!

There are lots of ways that someone could check whether you’ve owned a property before, such as searching the Land Registry for your name, checking to see whether there’s a previous mortgage on your credit history or looking at your HMRC records to see whether you’ve paid Stamp Duty previously. Ultimately, even if you are inclined to break the law, we’d say it’s just not worth the risk!

Ready to team up with your partner to buy the property of your dreams?

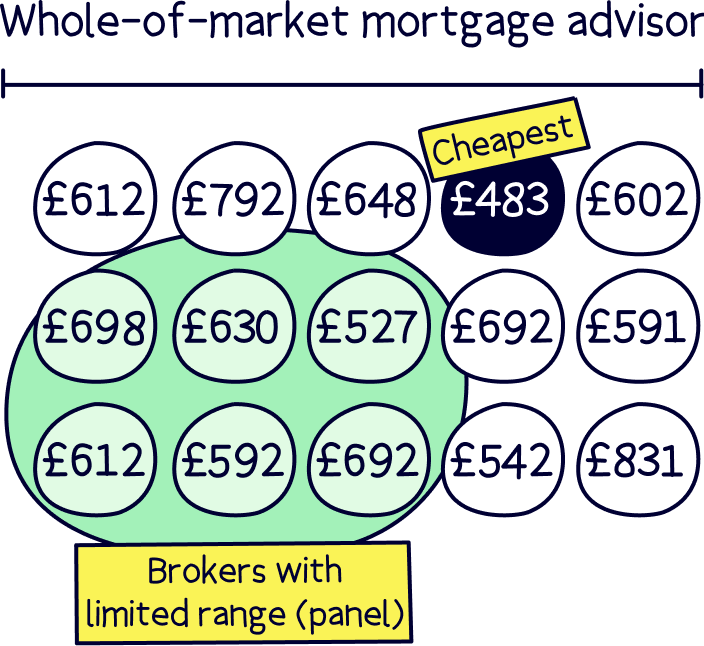

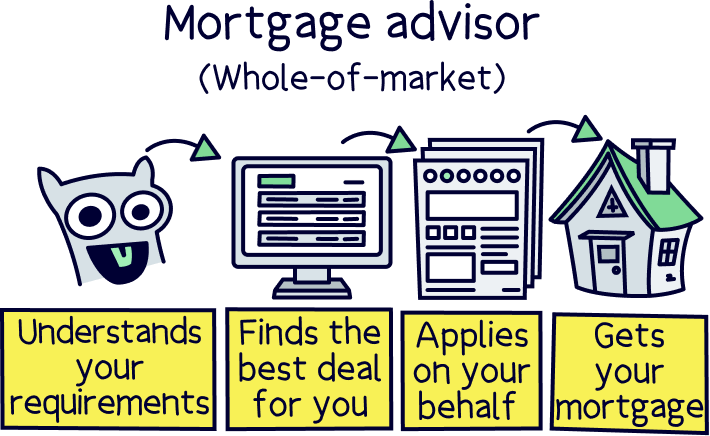

Whether you qualify for government help or not, just get in touch with a ‘whole of market’ mortgage advisor who can compare all the different deals from lots of different lenders.

Want to know more about mortgage advisors (also called mortgage brokers)? Read our useful article Do I need a mortgage broker?

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money too. How great is that?

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Want more options? Here's our top mortgage brokers.

Not only can a mortgage advisor help you with the most cost-effective way to buy a property together, but they’ll even sort your whole application out for you (there’s a reason we call them lifesavers!).

You’ll be sipping champagne in your brand new pad before you know it.

For more information about mortgages visit our mortgage home page.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.