Article contents

Yes! You should definitely use a mortgage broker. They’ll get you the best mortgage deal from all the different mortgages out there. You could save £100s per month on your repayments. Some of them are even free, and they’ll even apply and handle everything for you too!

Looking to buy a new home, or just switching mortgage deals? A mortgage broker is essential. The difference between a good mortgage deal and a bad deal can be £1,000s per year and £100s per month. Think of all that money you could save!

Using a mortgage broker guarantees you will be on the best mortgage deal. And as some mortgage brokers are actually free to use, it’s a no-brainer.

Having said that, don’t just use any broker – make sure you use a good one. We’ll run through what the difference is, how to find one, and cover everything in a bit more detail. Let’s go!

By the way, if you’re already convinced by using a broker, our top recommendation is Tembo¹ – they’re online, whole-of-market and although it's not free, their customer service definitely makes up for it. Plus you can get 50% off their standard fee with Nuts About Money. If you want a free online mortgage broker, check out Habito¹, they're great too!

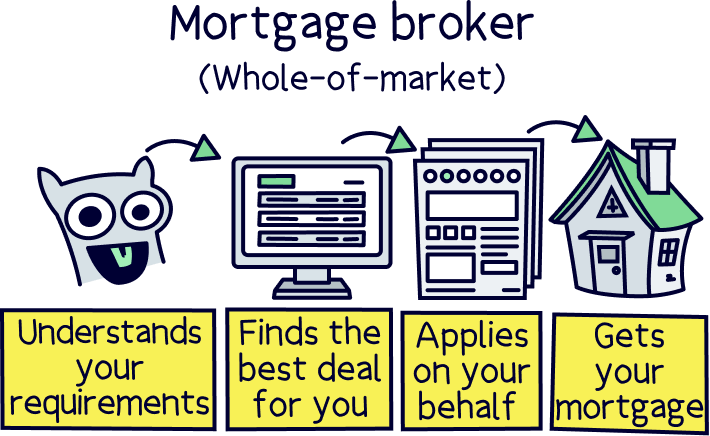

A mortgage broker (also called a mortgage advisor), is someone who compares mortgage deals and finds the right mortgage for you. There’s over 20,000 mortgages out there from over 100 lenders – so it’s quite a feat!

They do this by first getting to know a bit about you, things like whether you’re a first time buyer, moving home or switching to a new deal (remortgaging). They’ll also get to know a bit about the property you’d like to buy or remortgage. Then, they’ll go off and consider all the factors and your personal circumstances, and then come back with a recommendation for the best mortgage for you.

It's important to know that they don’t just look for the cheapest mortgage (although they will try and get the best deal). They will also consider your personal circumstances and what lenders (the people who give out mortgages) are likely to lend to you. Different lenders will lend to different people based on their circumstances (more on this below).

A mortgage broker will also handle all the paperwork too. You don’t need to do a thing. They’ll handle the whole mortgage application process (which can be quite stressful), and chase lenders for updates. You can see why we love them so much.

Just make sure you use the right mortgage broker. The difference between a good one and a bad one could be £100s of pounds per month!

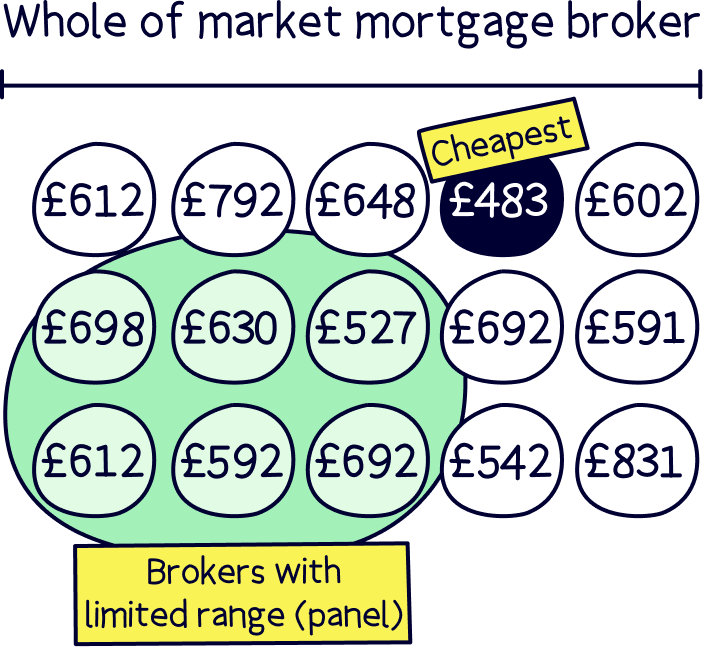

We’re going to bang on about this a lot, as it makes a big difference! We recommend you only use an independent mortgage broker who can search every mortgage deal out there. This is called ‘whole-of-market’.

It simply means to search the whole ‘mortgage market’, which is all the mortgages from all the different mortgage providers. And there are quite a few!

If you use a mortgage broker who can’t compare deals from the whole market, you can’t be sure you’ll get the best and most suitable deal for you, and as a result, could end up paying a lot more than you need to.

Some mortgage brokers have access to the whole market, some only have access to a few lenders and some can only recommend a very limited number of mortgages, such as a mortgage advisor at a bank, who can only recommend their own bank’s mortgages.

Nuts About Money tip: never walk into your bank and ask for a mortgage – you’ll likely pay a lot more than you need to.

And by the way, independent brokers also have access to ‘broker only deals’, which are exclusive rates you wouldn’t be able to find yourself.

If you just want a quick look at the best deals check out our mortgage comparison table.

When a mortgage broker is comparing deals to find the right mortgage for you. They’ll look at things like:

Mortgages have become pretty complicated over the years, every mortgage is different, let's give you a quick overview and what to look out for.

If you’re looking for lower monthly payments, you’ll get a different mortgage to someone who’s looking to pay off their mortgage as quickly as possible.

Lower monthly payments would most likely be a longer mortgage term (the duration of the mortgage, like 35 years), to keep the payments low, but you’ll pay more interest in the long run (as you will be paying interest for more years). However, a mortgage with higher monthly payments but a shorter mortgage term will usually mean less interest overall.

Everything depends on your circumstances and what type of mortgage you’re looking for. You can see why a mortgage broker is quite handy now right?

Tembo will find your best deal, fast, all with award-winning service.

What’s super important is to look at the overall cost of the mortgage, rather than the interest rate or any one specific thing.

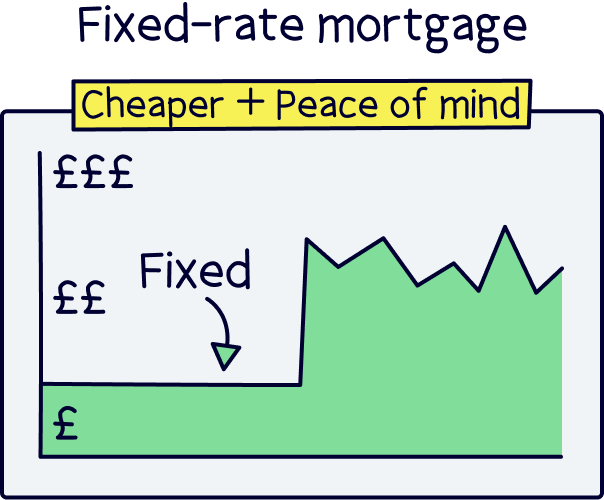

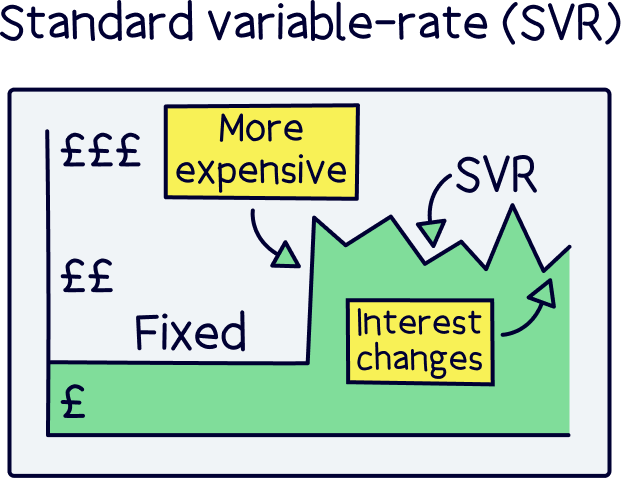

The overall cost is what you’ll pay in total over the fixed term period – that’s the period of time at the start of your mortgage where the interest rate is fixed. This is normally 2 or 5 years, but can be any length of time.

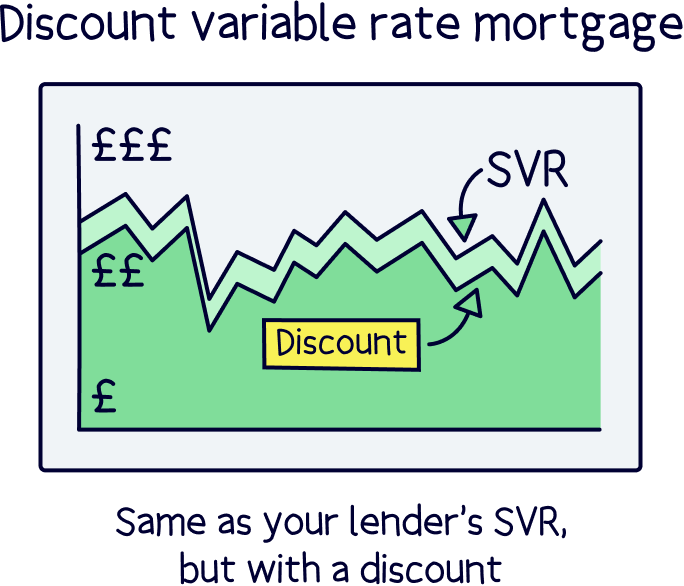

After your fixed rate period ends, the interest rate will go up to the mortgage lender’s standard variable rate (SVR) which is often very expensive.

The good news is you can remortgage (switch deals) at this point, to another lower interest rate mortgage with either the same lender or another lender (always use a broker to compare deals again).

Anyway, what this means is that because you’re going to remortgage after the fixed rate period ends, then only the overall cost during that period is what you should take into consideration and compare. This cost includes the monthly repayments, but also any additional fees, such as arrangement fees – which is a fee to get the mortgage from the lender.

Lenders often try to get their mortgages top of the mortgage comparison tables by reducing the interest rate but increasing the fees to get the mortgage. It’s a bit sneaky. Using the overall cost, you’ll be able to compare everything to make sure you really are getting the best deal.

The benefit of using a mortgage broker is they’ll do all the complicated maths for you. You can be sure you’ll be getting the cheapest mortgage, that’s also suited to you. Which brings us onto…

If you didn’t already know, there’s quite a big range of mortgages! All suited to different types of borrowers. Here’s the main ones:

There’s over 100 mortgage lenders in the UK. Some compete with each other, and some are fairly unique and offer their own special mortgages. However, they all have different criteria for accepting customers – that’s their own rules to determine if you’re a good fit for them or not (and some are pretty strict!).

For example, some lenders aren’t too keen if you’re self-employed, or run your own business, but other lenders will love you. And, it’s the same for a range of different types of jobs. Some lenders also don’t like those on a low income, or if you’ve got a small deposit. The list goes on!

Basically, a mortgage broker knows the criteria of all the different lenders and knows which lender will be perfect for you and your circumstances. It gives you the highest chance of getting accepted for a mortgage when you go on to apply. You’re in safe hands when you use a broker.

Watch out: if you apply for a mortgage with the wrong lender and you get rejected, it can have a negative impact on your credit score, and could stop you from getting a mortgage afterwards.

Mortgage brokers are fully qualified professionals – you can't just rock up and be a mortgage broker. They also need to be authorised by the Financial Conduct Authority (FCA) in order to give mortgage advice.

This means you also get protection from the Financial Services Compensation Scheme (FSCS). So, if you do end up on the wrong mortgage deal thanks to your advisor (very unlikely), you can get compensation.

Note: you wouldn’t get any protection, or compensation, if you applied for a mortgage directly yourself, without the help of a broker.

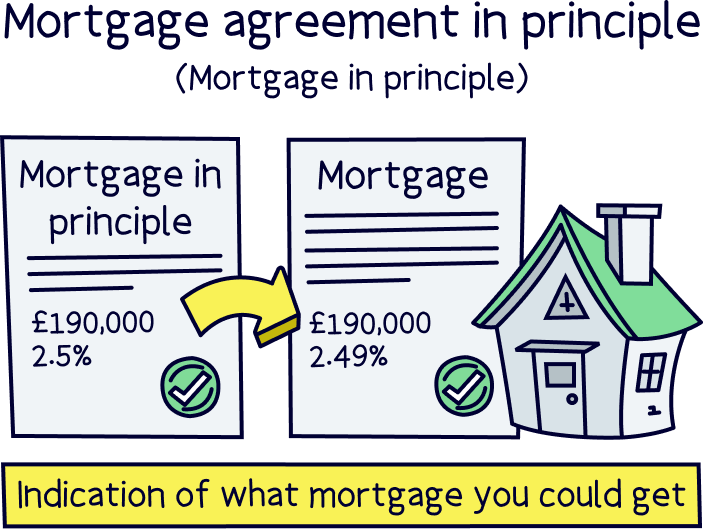

A mortgage broker can also help you get a mortgage agreement in principle. This is an official document normally from a mortgage lender that they’re happy to lend you money!

It proves you can actually get a mortgage in the first place, and that you can get a mortgage for as much cash as you’d like to. Plus, it won’t affect your credit score either. The only time a mortgage lender will do a hard credit check (one that stays on your credit report) is when you make a ‘full mortgage application’ when you’re ready to go ahead and get the mortgage.

Often when you’re house hunting, estate agents will ask for a mortgage-in-principle before you even get started. It’s not a legal requirement, but they want to know you are a serious buyer before they start showing you round properties.

The mortgage-in-principle will show how much you can borrow, and can sometimes also show the monthly repayments, interest rate and a few other things such as the type of mortgage.

Although, it’s not actually a guarantee you’ll get the mortgage, provided your circumstances don’t change, such as getting a new job, and as long as you pass the credit checks when you make a ‘full mortgage application’, you’ll more than likely get the mortgage.

Nuts About Money Tip: you can get a mortgage-in-principle online within minutes with Tembo¹ . It’s not an agreement from a lender, but it will give you a good indication of how much you can borrow, and should be good enough for an estate agent.

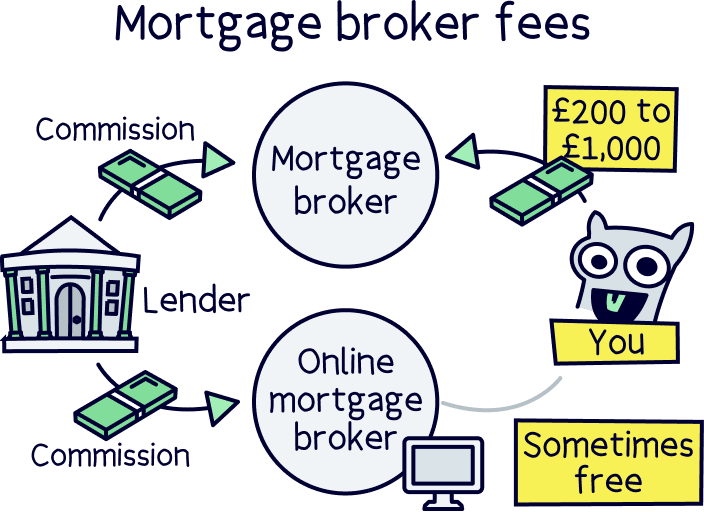

All of this mortgage advice, and all this work, must be expensive right? Well actually, no! Some mortgage brokers are actually completely free. How good is that?

Mortgage brokers get paid a commission from the mortgage lender when they find a mortgage for you, and so don’t have to charge you too. However, most do, and the average fee mortgage advisors charge is around £500. If you’re paying more than that, and you’re not getting a specialist mortgage, such as a guarantor mortgage, (so specialist mortgage advice), you’re probably overpaying.

The good news is that with online mortgage brokers, some of them are completely free, they don’t charge you anything because they make enough money from the mortgage lenders. And, between you and us, we think they’re much better too. Everything is online, works to your schedule, rather than the mortgage advisors (you don't have to make appointments based on when they are free). You can even sort everything out while sitting on the sofa watching TV.

We’ve reviewed the best online mortgage brokers. Here’s the spoiler – the best is Tembo¹ - they've got award-winning service and will guarantee to find the best deal for you. Learn more with our Tembo review.

There’s some mortgage lenders who only offer direct deals. This means that a customer has to go directly to them to get a mortgage. The largest in the UK are First Direct and Yorkshire Bank.

Often these are not the cheapest mortgages, but if you want to be 100% sure, you can check the rates with these lenders directly, without having to apply for anything. We recommend doing this in addition to using a mortgage broker.

Convinced a mortgage broker is the right choice for you? Excellent! It’s the only way you can be sure you’ll get the best deal, and as some of them are free, so why not use them. Especially as they’ll handle the whole mortgage application process for you too.

There’s only one major rule, which is to use a whole-of-market mortgage broker. This means they can search every mortgage deal out there. Otherwise, you might end up paying £100s more per month more than you need to.

Finding the best mortgage brokers is pretty easy too. We’ve already done the research for you.

Your options are either an online mortgage broker, where everything happens online, and so works around your schedule – you can even do it all on your phone (or at work – we won’t tell your boss), and you can even chat to your advisor over live-chat (on their website). The good ones are completely free, and of course whole-of-market.

Our recommended online brokers are:

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Want more options? Here's our top online mortgage brokers.

You could also use a local mortgage broker, who’s a bit more traditional, and you can either meet them face-to-face, chat over the phone and over email. Most mortgage brokers will charge a fee, and some are particularly expensive, plus not many are whole-of-market, so make sure you ask (here’s all the questions to ask a mortgage advisor). But some of them are great!

As a reminder, check out Tembo¹, they've got an award-winning service and you could be chatting to an expert in just 10 minutes. Plus get 50% off their standard fee with Nuts About Money. Or visit Habito¹, a free online mortgage broker.

And there we have it. Happy house hunting, or remortgaging! You’ll be on the best deal in no time with a mortgage broker.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.