Article contents

Mortgage advisors aren’t all the same! You need to find one who can find the best deal for you, at a price you’re comfortable with (some are free!). You also need to ask some important questions to figure out your actual budget and what a real mortgage could look like.

Ready to buy your new home? Exciting times ahead! Now comes getting a mortgage, which can be a complicated and stressful time but it doesn't have to be!

You’ve already made the best decision you can, which is choosing to go with a mortgage advisor (also called a mortgage broker), rather than finding a mortgage yourself, as this will save a lot of admin time and importantly making sure you’ll find the right deal for you. We call them the superheroes of mortgages!

However, not all advisors are all the same – in fact they vary quite wildly, and not using the right one could cost you £100s per month extra on the wrong mortgage.

Here’s the 8 key questions to ask a mortgage advisor before you get started. And if you don’t like what you hear, move on!

Not sure where to find a good mortgage advisor? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. You'll also get 50% off with Nuts About Money.

Not just anyone can give mortgage advice (legally), they need to have been given permission (authorised) by the Financial Conduct Authority (FCA). The FCA are the people who assess and review the advisor to make sure they’re suitable, with no previous bad history, and qualified to advise on mortgages.

They’ll also be assessed regularly, and have to follow set guidelines and procedures to ensure they are treating you fairly, finding the right deal for you, and not recommending the best deal for them (the highest commission).

It also means that if they do recommend you the wrong deal, you’ll be entitled to compensation.

It’s best to check the FCA register yourself – it’s easy, just search their name or the name of the firm.

You may find a mortgage advisor isn’t authorised directly, but an ‘appointed representative’ of another firm who is authorised. That’s completely fine! It’s often how individual or small companies can get started and save on extra costs.

If your mortgage advisor isn’t authorised to do so by the FCA, run for the hills!

The most important question to ask every mortgage advisor (once you know they’re actually allowed to be giving mortgage advice!).

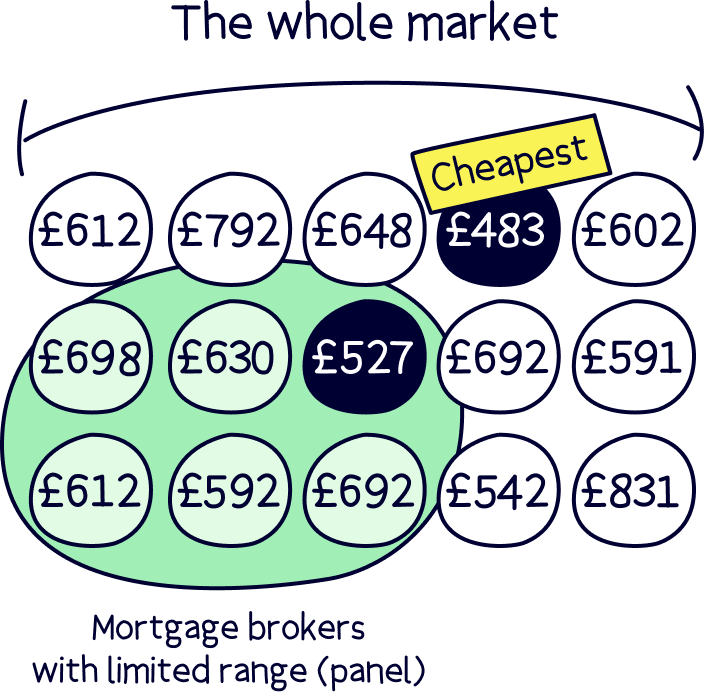

In order for you to get the best mortgage deal, the mortgage advisor needs to be able to search every mortgage deal out there, to then find the best one for you. Being able to search every mortgage deal is called ‘whole-of-market’, i.e. you are searching the whole mortgage ‘market’.

If you don’t get the best deal, and there are over 20,000 mortgages at any one time, it could mean you are paying a lot more than you need to be every month in interest. This can range from £100s to sometimes £1,000s per year. Now imagine that over the lifetime of your mortgage!

Most mortgage advisors don't search the whole market, so you'll need to ask. Why ask? If they don't, they’re more likely to hide it and not tell you!

Lot’s of brokers can only recommend a few mortgage lenders (the people who give out mortgages), and there’s even some who can only recommend their own mortgages, such as if you went into a bank on the high street (never do this, loyalty to your bank doesn’t pay!).

There’s over 90 mortgage lenders out there, so don’t settle for a broker searching just a few lenders. Use one that searches them all! You could save yourself a small fortune!

Now it’s time to talk money – once you know they’re allowed to give advice, and that the advice you’ll get means you get the best mortgage deal for you.

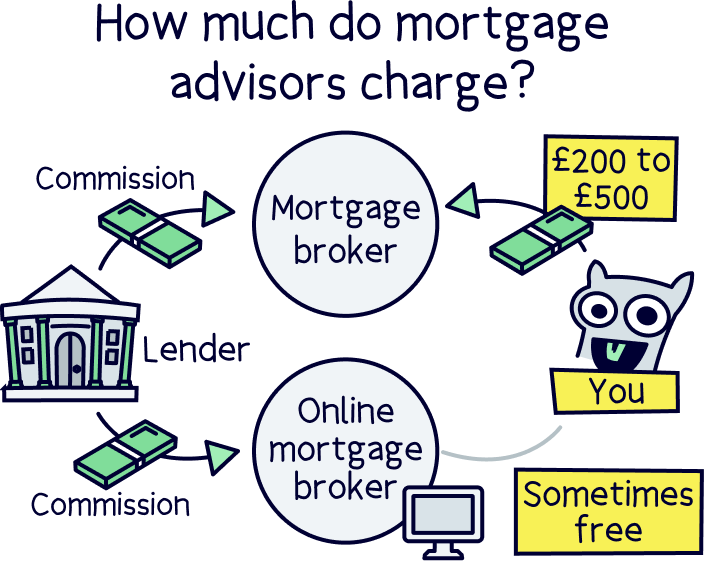

So, a typical mortgage advisor, who you’ll speak to in person, over the phone or over emails will often charge a fee, and this can range from around £200 to £500. It really depends on their service and what type of mortgage you’re after.

If you’re not moving home and remortgaging instead (switching mortgage deals), it’s often a pretty simple process for the broker, and they’ll charge a lower fee. Whereas moving home and first time buyers are a bit more work, so normally a bit higher.

If a broker is charging more than £500, that’s a bit too much. They might be trying their luck!

Note: the broker also gets paid from the mortgage lender when they get you a mortgage – because they are finding them business and they’re effectively doing lots of the paperwork. So trying to charge you lots of money too is a bit cheeky.

There are free mortgage brokers out there, but remember to only use one that can search the whole market.

Online mortgage brokers can sometimes be free, search the whole market, and work to your schedule (as you’re doing it online!), so it’s worth checking out if you’re comfortable with handling your mortgage online – there’s no reason not to, and they’re super popular these days.

The best one is Tembo¹, they'll guarantee to find you the best deal and have award-winning service. (You'll get 50% off with Nuts About Money too.)

Tembo will find your best deal, fast, all with award-winning service.

Now we’re into the good stuff! How much can you actually borrow? Can you actually afford the home you like?

A good mortgage advisor will go through your finances in detail to work out how much you can actually afford to borrow and if you are likely to be accepted for a mortgage at that amount.

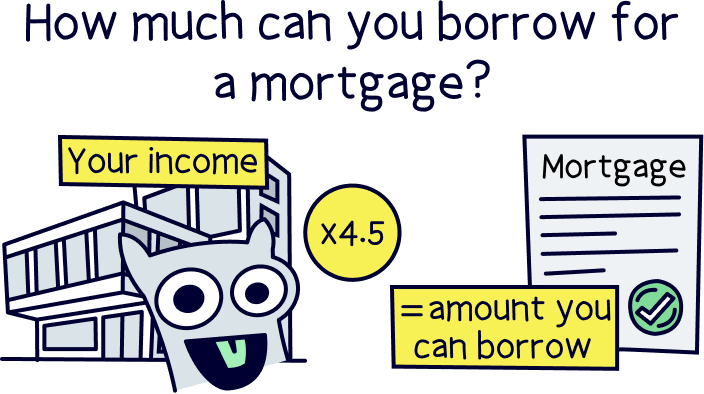

Typically you can multiply your income (such as your salary) by 4.5x, to get a good indication of how much you can borrow, for instance if you earn £30,000 per year, then you can borrow £135,000.

However, if you have lots of bills each month, other debts and not much spare cash left from when you get paid, you may find you can’t borrow as much as 4.5x as the lender will think you can’t afford the monthly mortgage repayments. They’ll also look at your credit history – you can learn more about that with our guide: what credit score do you need for a mortgage?

A good advisor will get you a mortgage-agreement-in-principle, which is a very strong indication of how much you can actually borrow, and often this is from an actual mortgage lender, so you know you’ll be able to borrow that much and they won’t be guessing!

If you’ve got a house in mind, you’ll know from getting your mortgage-in-principle how much you borrow.

So, to get a good indication of how much deposit you’ll need, you can take the price of the home you have in mind, let’s say £160,000, and take away how much you can borrow, let’s say £135,000, which gives £25,000. So, you’ll need £25,000 as a deposit to buy your home. And a bit extra for fees.

However, it gets a bit complicated, and this is where a mortgage advisor comes in, as they’ll do a lot of the maths for you.

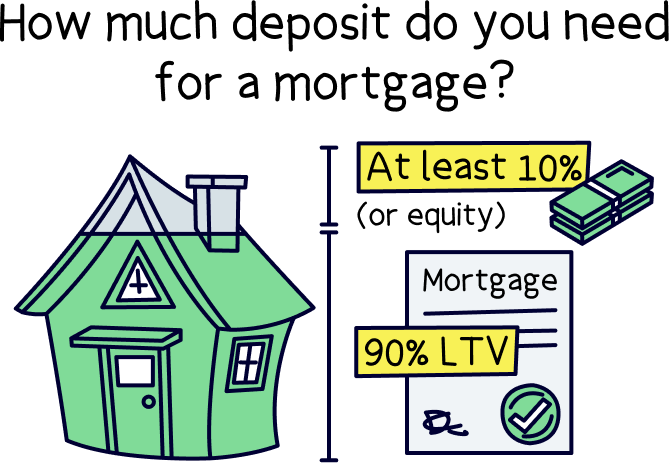

You normally can’t get a mortgage if you have less than a 10% deposit, although you may get lucky and find one at 5%, but even with a 10% deposit, it will be at a very expensive interest rate. (An interest rate is how much you’ll pay each year to the mortgage lender as a cost of borrowing the money).

So it’s often best to try and get 15% or 20% as a deposit, to first ensure you can actually get a mortgage, and second, that it’s at a good interest rate. In our example we have a deposit of 15% which is great.

However if we only had £10,000 in savings, we would only have a 6% deposit for a home of £160,000 – and so we probably wouldn’t be able to get that mortgage unfortunately. We would have to reduce how much we can borrow to around £90,000 (10%).

There’s also extra costs that your advisor will tell you about, which is Stamp Duty (tax), legal fees, and building surveys. Buying a home is expensive!

If you use Habito, they’ll do everything for you, all under one roof. However with another mortgage advisor, you’ll have to find a solicitor or conveyancer (the legal person), and a surveyor yourself – make sure they give you a good service at a good price if you are finding them yourself!

Here's another important question. (we’ve nearly finished!).

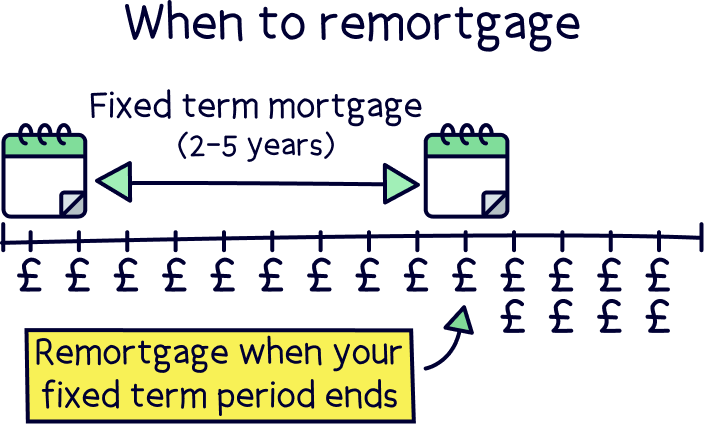

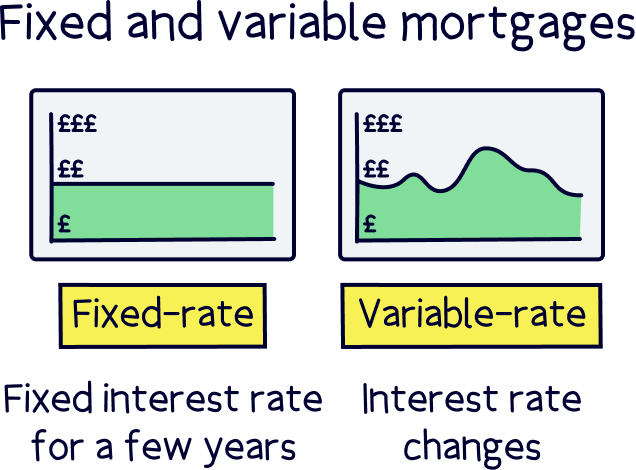

With mortgages you’ll often be given a fixed interest rate at the start of your mortgage. This is normally 'fixed' for 2 or 5 years, although it can be 7, 10 or even longer.

It's usually a pretty decent deal to entice you into a mortgage, and is how mortgage lenders compete with each other (trying to get top of a comparison table).

However, after your fixed rate period has ended, the interest rate normally shoots up to a much higher rate, which is the mortgage lenders ‘standard rate’. At which point you should often remortgage to a new deal.

It's worth noting, you can also get mortgages without a fixed rate, and this is called a variable rate mortgage (as the rate can change depending on things like if the Bank of England base rate increases or decreases).

So, with the help of your mortgage advisor, you’ll need to decide how long you want to fix your mortgage for, or at all. Fixing for a shorter period of time is often cheaper, however there’s normally hefty fees (called early repayment charges), if you change your mortgage, such as selling your home, or moving home (although not always), during the fixed rate period.

By the way, we’ve got a guide if you’re a bit unsure, should I fix my mortgage?

Now you should ask your advisor and decide together, which is the best type of mortgage for you.

Your standard mortgage that most people get when they purchase their own home to live in is called a ‘repayment mortgage’, and that’s when you pay off some of the mortgage each month, and some of the interest. So at the end of the mortgage, the house is all yours.

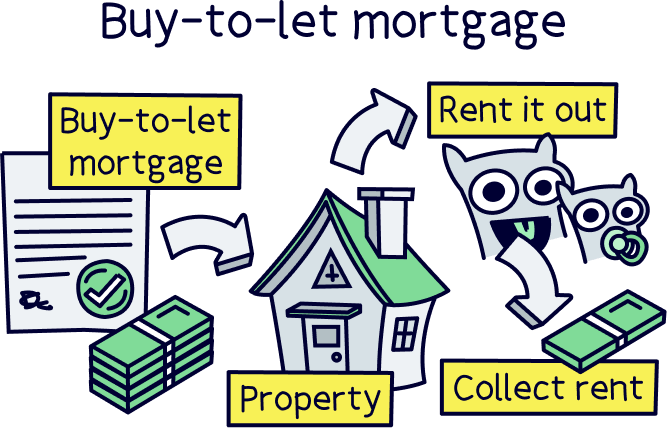

But you can also get an ‘interest only’ mortgage, which is just paying off the interest each month. These are common for landlords getting a buy-to-let mortgage.

There’s also lots more different types of mortgages, which we won’t go into here, but that’s why it’s worth asking a mortgage advisor! Some examples are a part-and-part mortgage, discounted rate, capped rate, tracker mortgage and an offset mortgage.

You also need to decide how long you want the mortgage for. Often mortgages are between 10 and 40 years. And the longer the mortgage is, the lower the monthly repayments, but also means you are ultimately paying more in interest (as you are paying interest for more years).

The typical mortgage is for 25 years, but these days, lots of people are opting for longer mortgages to make them more affordable (thanks to expensive house prices!). However it’s best to ask the advisor what they think is best for you and your financial circumstances.

And finally, what’s the best mortgage for me? The most important question!

Now your mortgage advisor knows a lot about you, and the home you want, they’ll be able to find the best mortgage for you.

It can take a few days, and sometimes longer depending on the advisor, but at the end you should have the perfect mortgage with affordable monthly repayments, and a great interest rate.

Once you have both decided on the mortgage, all that’s left is to apply. As your mortgage advisor has all your details they will apply on your behalf. It will mean a lot less admin for you. We told you they were superheroes!

To recap, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. You could be chatting to an expert it just 10 minutes. And as a bonus, get 50% off their standard fee with Nuts About Money too.

Getting your dream home is an exciting time! With the right advisor, you don’t need to worry about all the boring admin and paperwork, they’ll do everything for you, and you’ll be in your dream home as fast as possible, with the best mortgage for you.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.