Article contents

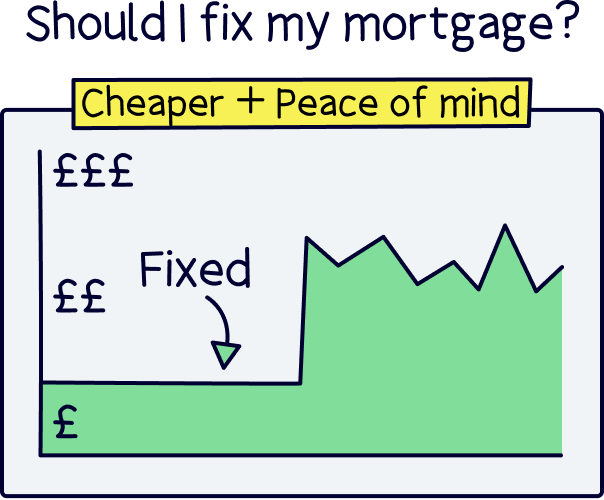

For most people, you probably should fix your mortgage as you can benefit from lower interest rates and peace of mind. The question is for how long?

One of the biggest decisions you’ll have to make when you’re applying for a mortgage is whether to fix the interest rate. In other words, you’ll need to decide whether you want to keep your monthly repayments at a fixed cost or not.

Don’t worry, it’s not as complicated as it sounds! We’ll explain it all below.

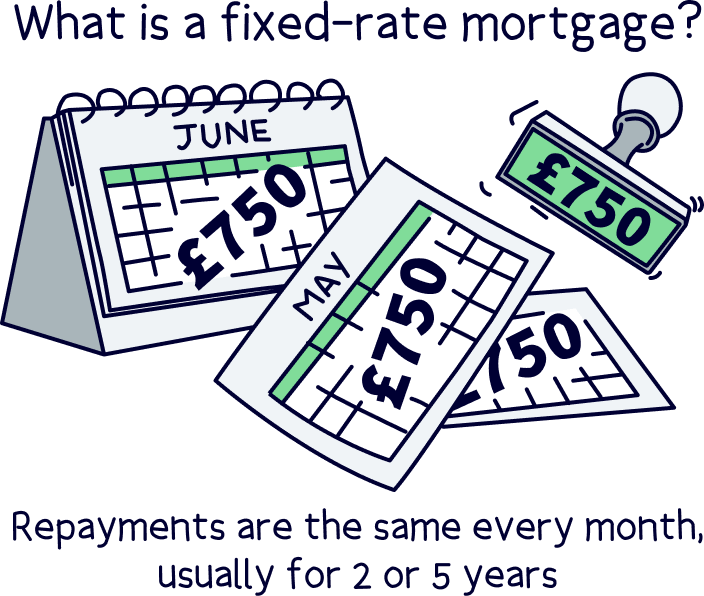

A fixed-rate mortgage is when your mortgage repayments are fixed for a certain amount of time. Usually, this will be for 2 or 5 years but it can also be 3, 7, 10 or even 15!

During this time, you’ll know exactly how much you’re paying each month and your lender can’t unexpectedly charge you more or less. Sounds good right?

And it gets even better. Lenders tend to call it the incentive period. Can you guess why? It’s because the rate you get during this time is a special, lower rate that’s designed to encourage you to sign up for it. Happy days!

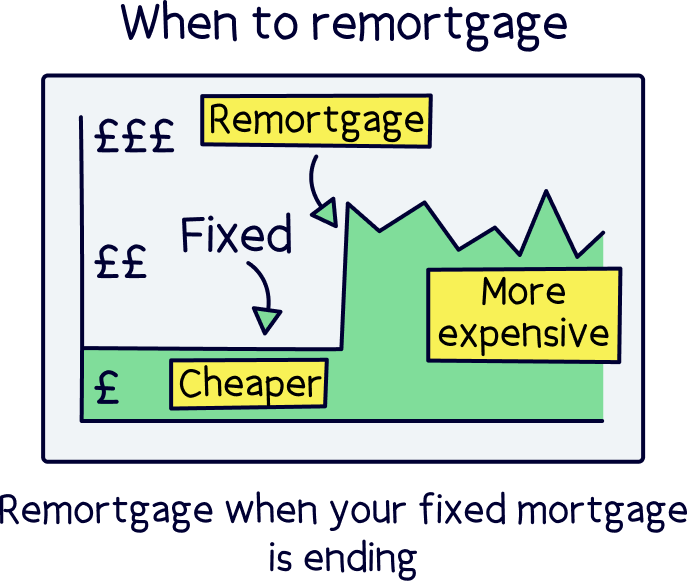

Even though this period won’t last forever, you can normally keep enjoying the benefits by remortgaging once your incentive period is up.

Essentially, that’s where you quit your current mortgage and take out a new one to get a whole new incentive period to enjoy all over again! It’s a bit like switching phone contracts to get a cheaper deal when yours runs out – our guide to what happens when your fixed-rate mortgage ends will explain it all.

HOWEVER (and this is important): it’s not the only option. Although there are more fixed-rate mortgages available than any other type of deal, only around half of borrowers in the UK are on a fixed-rate mortgage. Bear with us while we run you through the alternatives...

If you want to fix your mortgage, or need some advice explaining your options, you should chat to an independent mortgage advisor.

Not sure where to find a good mortgage advisor? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Anything that’s not a fixed-rate mortgage is known as a variable-rate mortgage. And, surprise, surprise, this means that your repayments are ‘variable’. In other words, instead of paying the same amount every month, your repayments could go up or down.

To make things that little bit more confusing, there are actually three different types of variable-rate mortgages available (sorry!). Here they are:

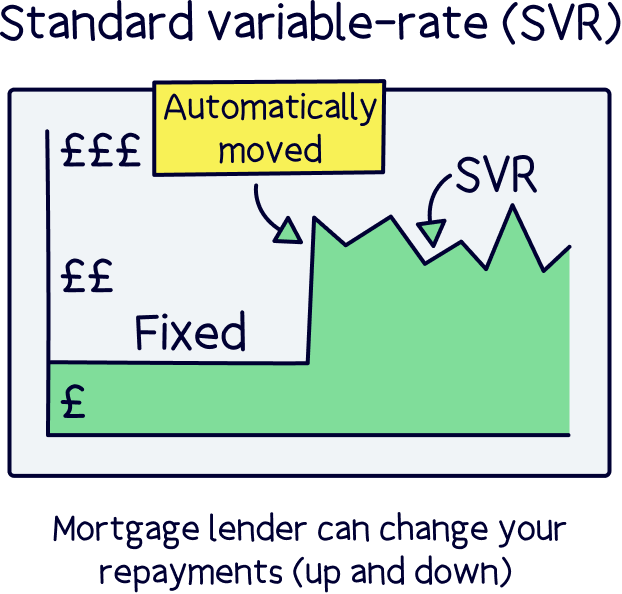

The standard variable rate, known as SVR, is what your mortgage lender will automatically move you onto if you’re on a fixed-rate mortgage and your incentive period comes to an end.

If you’re on the SVR, it means your lender can change your mortgage repayments whenever they fancy it, either up or down. Usually, your lender will move them roughly in line with what the Bank of England’s base rate (interest rate) is. An interest rate is the amount you have to pay for borrowing money, or what the banks pay you for saving money with them, and is calculated as a percentage.

So, if the base rate goes down, your repayments will likely go down. And if the base rate go up, your repayments probably will too.

That said, your lender doesn’t have to mirror the Bank of England’s rate and they can technically move your rate whenever they want. So, it’s a little risky. After all, you never know what bill’s going to come through the letterbox!

Not only this, but the SVR is usually a lot higher than what your fixed-rate mortgage would be, which is how the banks make lots of money. This is one area where loyalty just doesn’t pay, so usually if your fixed-rate deal is coming to an end, you’ll want to remortgage before your lender has a chance to move you onto the dreaded SVR.

If you find you’re on this rate, just get in touch with an independent mortgage advisor who’ll be able to help you get onto a better deal.

As a reminder, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best deal. Plus, get 50% off their fee with Nuts About Money.

We know what you’re thinking: why would anyone want to be on this type of mortgage?!

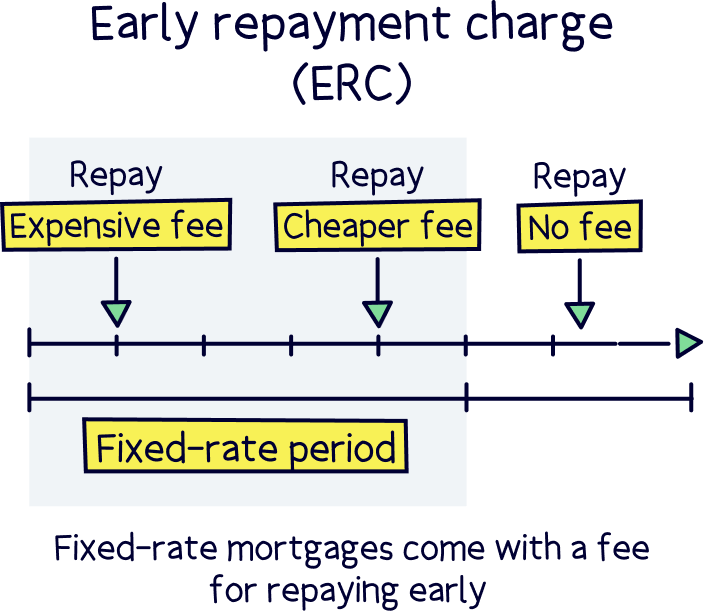

Well, the best thing about it is that there aren’t any early repayment charges. If you’re on a fixed-rate mortgage and you want to leave early, you’ll usually have to pay high fees. But if you’re on the SVR and you want to pay some (or all) of your mortgage back early, you can. This includes if you’re selling your house!

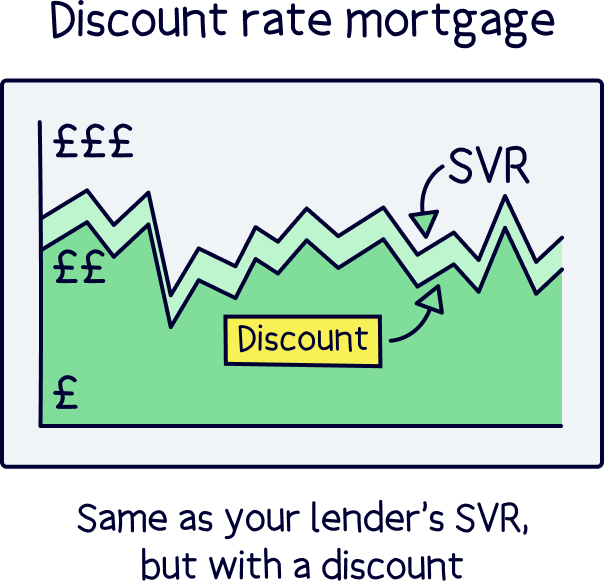

A discount rate mortgage is the same thing as your lender’s SVR, but with a discount on top. And who doesn’t love a discount?!

Let’s say your lender offers you a 2% discount. This usually means that the interest rates you’ll pay are 2% less than they would be if you were on the SVR. Often, this will give you access to the lowest starting rates.

But remember, even though you’ve got a discount, your mortgage will work in exactly the same way as the SVR. In other words, your rates can still go up or down whenever your lender feels like it, so you don’t have the same security as you would on a fixed-rate mortgage.

On top of that, most lenders will only offer these discounts for two or three years. So, if you’re on this kind of mortgage, you’ll probably want to remortgage at the end of this period in the same way as you would if you were on a fixed rate.

Just like our last two examples, a tracker mortgage can also go up or down. But the big difference is that your lender’s not allowed to move the rate around whenever they feel like it. Hallelujah! Instead, it has to follow the Bank of England’s official borrowing rate.

The good thing about this is that you’re not at the mercy of your lender. If the Bank of England’s rate goes down, you know your repayments will go down too. And if the Bank of England’s rate goes up, so will your repayments (okay, so that’s the less good part...).

The important thing to remember is that just because your rate goes up and down in line with the official borrowing rate (known as the base rate), that doesn’t mean it has to be the same. Usually, tracker mortgages are higher than this base rate, it’s just that they go up and down by the same amounts.

On top of this, lots of tracker mortgages will lock you into an agreement for a set number of years just like a fixed-rate mortgage would. That means you don’t get to leave early without facing that annoying early repayment charge. Urgh!

Tembo will find your best deal, fast, all with award-winning service.

For most people, the answer is yes, you should fix your mortgage rate. Think about it: a fixed-rate mortgage is the only one that gives you the peace of mind of knowing exactly how much you’re going to be repaying each month. And they’re also a lot cheaper than your lender’s SVR.

At the same time, there are pros and cons. Let’s take a look...

Pros:

Cons:

Ultimately, the decision comes down to how much of a risk-taker you are! You may be able to get lower starting rates by choosing a tracker or discount-rate mortgage. But on these, there’s a chance your repayments could go up.

If you have a lot of savings to play with, you might decide that this risk is worth taking. But if you can only just afford your repayments as it is, the risk probably won’t be worth it – imagine if your repayments go up. The consequences could be disastrous!

If we assume that you’re going to go ahead and fix your mortgage, then the next question is: for how long?

You’ll normally be choosing between a 2 or 5-year initial term. But your lender might also offer you a 3, 7, 10 or even 15-year fixed period. So, how do you decide?

The main thing you’ll need to ask yourself is: how long do you need the certainty for? This is likely to depend on a number of things, so let’s take a more detailed look at what you’ll need to consider.

If you’re only planning on staying in your property for a few years, there’s no point in taking out a 10-year fixed-rate mortgage. This is for two reasons:

Plus, many of us will move into a new house without much of a long-term plan. How do you know what you’re going to want to do in 5 years time? You might think that you’ll still be in the same property, but what if things change?

A shorter initial fixed period gives you more flexibility to make changes down the line. It also covers you if interest rates drop. Remember, if you’re in your incentive period, your rates won’t go down when interest rates do. By opting for a shorter initial fixed term, you’ll be able to remortgage and potentially get a cheaper deal.

That said, if you’ve forked out on a forever home and you’re absolutely sure you’re never going to leave, you may as well opt for a longer period. Even though you’ll be paying a bit more each month, remortgaging can be a bit of a hassle, so you might rather lead a stress-free life! Plus, it comes with fees. And if you’re remortgaging often, you could easily spend just as much in fees as you would by opting for a longer deal.

Let’s look at an example: over a 10 year period, some people will take out 5 separate 2-year deals while others will take out 2 separate 5-year deals.

If we imagine that you’ll be paying £1,500 in fees each time you change deals, that means the people who opted for the 2-year deals will be paying £7,500 in total. On the other hand, the people on the 5-year deals will only be paying around £3,000 in fees. That’s a big difference!

Just remember that you’ll always have to balance out the cost of fees against the possibility of early repayment charges if you leave early, as well as the risk of interest rates going down and leaving you on a higher rate.

We’d always recommend talking to an independent mortgage broker who’ll be able to help you come to a decision based on your own unique circumstances (not only that, but they’ll even do the whole application for you. Score!).

Use Tembo¹ if you're not sure where to find one, you'll get 50% off their fee with Nuts About Money.

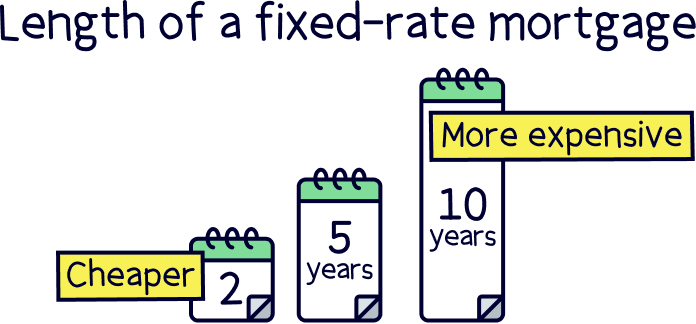

Normally, the shorter your fixed-rate period, the less you’ll pay each month. This is because on a longer fixed term, you’re paying extra for the luxury of having your rates fixed for a longer period of time.

In a nutshell, if you’re on a 10-year fixed-rate mortgage, you’ll usually be paying a little more than someone on a 2-year one. And even though it might only be a bit extra each month, it could add up to thousands over the course of 10 years.

So, think about how tight your mortgage repayments are. Can you afford to fix your payments for longer? Or are you better off paying less and then hoping you can get an even lower rate when you remortgage in a couple of years?

If you’re choosing whether to fix your mortgage for 2 or 5 years (as most people are), you’re in luck. Right now, there’s not a lot of difference between the rates you’ll be paying on either of these. Which brings us onto...

When you're deciding how long you should fix your mortgage for, you’ll want to take the current interest rates into account. If interest rates are likely to go up, it’s a great time to fix your mortgage for a longer period of time, as it will lock you into a lower rate. But if they’re likely to go down, it’s not so good. Your repayments won’t drop inline with interest rates, so you could end up paying more than you have to.

So, how long should you fix your mortgage for?

Well, the Bank of England bank rate has risen recently and could rise further. This means it could be a good time to fix your mortgage! Think about it, if you fix your mortgage now for 5 years, it means you’re guaranteed to pay a lower rate if interest rates rise again.

But don’t get too carried away. You’ll still need to take into account your future plans and the dreaded early repayment charge!! There’s no point in locking in a lovely lower rate for years and years, only to ruin it all by paying thousands of pounds in fees when you leave early!

If you’re not planning on living in the same property for years and years, a 2-year fixed-rate term might be the safest option. This way, you can sell up and leave after 2 years without having to pay that hefty early repayment charge. Or, you can just remortgage to get yourself on another fixed-rate deal if you want to stay. You may even be able to get a cheaper deal if interest rates have gone down, which is always a plus!

On top of all that, the shorter the term you go for, the less your monthly repayments will usually be. So, if you’re on a budget, this might be the best plan for you. Yes, you won’t have the peace of mind of knowing that your repayments are going to be fixed for years on end. But you’ll have certainty for a couple of years and can cross the next bridge when it comes!

A 5-year fixed-rate mortgage is a pretty good bet if you don’t want to lock yourself into a deal for years and years but you still want certainty for longer than your standard 2-year deal.

You’ll usually get lower monthly repayments than you would on a 10-year fixed-rate mortgage, and you’ll also have the flexibility of being able to leave your deal after 5 years without having to pay high fees. On top of this, the rates for a 5-year deal aren’t that much higher than they are for a 2-year deal at the moment. So, you get peace of mind for longer without having to pay a huge amount more.

It depends on how much certainty you want! If you want to know exactly how much your monthly repayments are going to be for 10 years, then this might be the best option for you.

However, we’d only recommend fixing your mortgage for 10 years if you know you’re going to be staying in your property for at least this long. Otherwise, you’ll have to pay early repayment charges when you leave.

Deciding whether to fix your mortgage, and how long for, can be a little mind-boggling, but it’s not rocket science. Just remember: it depends on what you value and how much certainty or flexibility you want.

To get some advice about what would be best for you, just have a chat with an independent mortgage broker. They’ll be able to lay out all your options and guide you through the whole thing!

Again, our top recommendation is Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.