Article contents

The actual mortgage application can be quick, but allow up to 6 weeks for a real mortgage offer from the lender, and a lot longer to actually move into your new home.

Set your heart on a forever home? You’re probably wishing you could skip forward in time to sitting cross-legged on the floor with boxes all around you and an Indian takeaway on your lap. But first, you’ll need to get your mortgage application approved!

We’ve taken a look at exactly how long it’ll take.

First things first, the big question on everyone’s mind: how long does a mortgage application actually take to be approved?

As a general rule of thumb, it’s likely to take between 2 to 6 weeks to get approved for a mortgage from the date of handing in your application. But the truth is, there’s a lot to do before you even get to that point.... like the most important thing of all: actually finding a house to buy!

Let’s take a look at what it all involves.

Tembo will find your best deal, fast, all with award-winning service.

If you’re wondering why a mortgage application takes so long, it kind of makes sense when you understand exactly what has to happen. In a nutshell, mortgage approval is normally split into two parts:

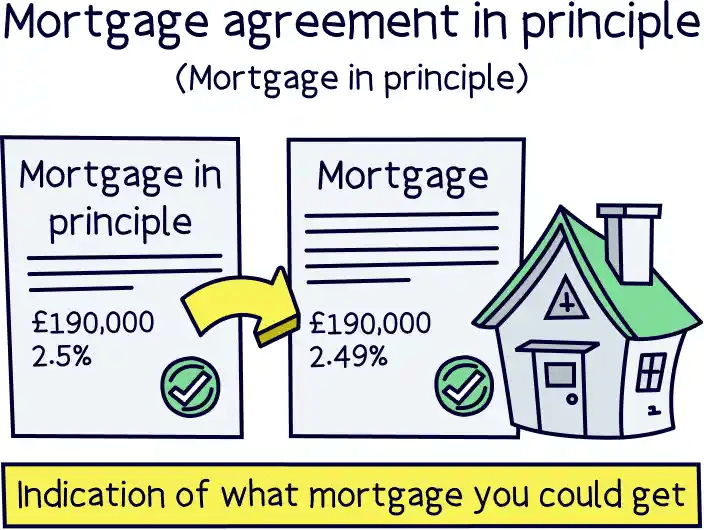

You might have heard of a ‘mortgage in principle’, an ‘agreement in principle’, a ‘decision in principle’ or a ‘mortgage promise’ before. These are all different words for the same thing – we know, confusing right?! But what exactly is it?

A mortgage in principle is an official estimate of how much a mortgage lender is willing to lend you. In other words, if a lender gives you a mortgage in principle, it means they think you’d get approved for a mortgage if you applied for one. Happy days!

For most people, this is the first step towards getting approved for a mortgage.

Normally, you’ll get your mortgage in principle before you go house hunting. They tend to last between 60 and 90 days, so it’s best to try and find a house in that time if you can. Otherwise, you’ll have to reapply!

We know what you’re thinking: why not just go straight in with the actual mortgage application? Well, here’s why you’ll want to get a mortgage in principle first...

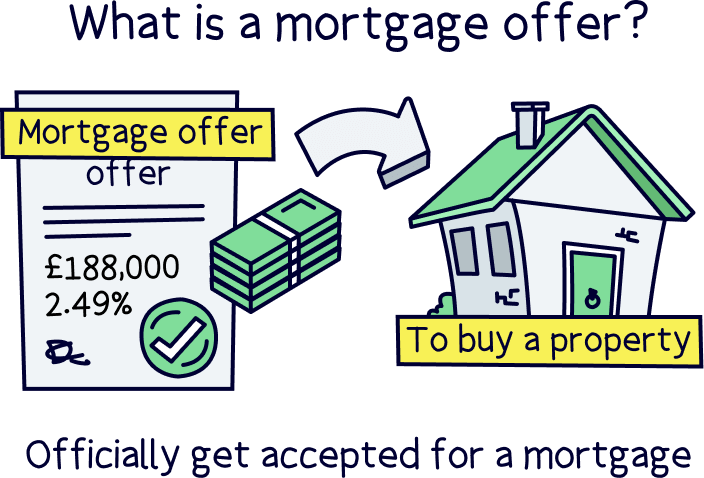

This bit happens after you’ve found a home to buy. Essentially, once you’ve found a house you like and the seller has accepted your offer, you can put in an application to turn your mortgage in principle into an actual mortgage offer.

This might seem like the scary part, but don’t worry. Your lender already knows a bit about you – and what they saw, they liked. After all, they already gave you a mortgage in principle!

That said, save the party poppers and the fancy champagne till after you’ve got your offer in the bag. Your lender will do some more checks when you put in your application, so there’s always a chance they could come across new information they don’t like. If that happens, they could still reject your application. This doesn’t happen too often though, so fingers crossed you’ll be just fine!

To keep things simple, we’ve broken the mortgage application process down into a few easy steps. Here’s how long you can expect each part of the process to take.

This bit is super quick and easy! Once you’ve got all the right documents together, getting accepted for a mortgage in principle should only take a few days. If you use a mortgage broker, it could even take as little as 1 hour (hint hint: use a mortgage broker. It’s totally worth it.).

Before giving you a mortgage in principle, your mortgage lender will normally want to see:

A mortgage in principle will usually last between 60 and 90 days. So, try to find a house to buy during this time so you don’t have to reapply.

Once you’ve fallen head over heels for a house (and the seller’s accepted your offer), you can apply to turn your mortgage in principle into an actual mortgage offer. The application should only take a few hours as you’ll already have most of the info to hand from when you applied for the mortgage in principle.

If you used a mortgage broker, this is where you get to act smug! They’ll have all your information saved so all you have to do is call them up and ask them to go ahead with the full application. Did we mention that they’ll even fill the whole thing out for you?! Told you it would be worth it.

A mortgage valuation is where your mortgage lender checks how much they think the property you’re buying is worth. Just like how you probably hate paying too much for something, your mortgage lender will want to check they are not lending you too much money before they approve your application.

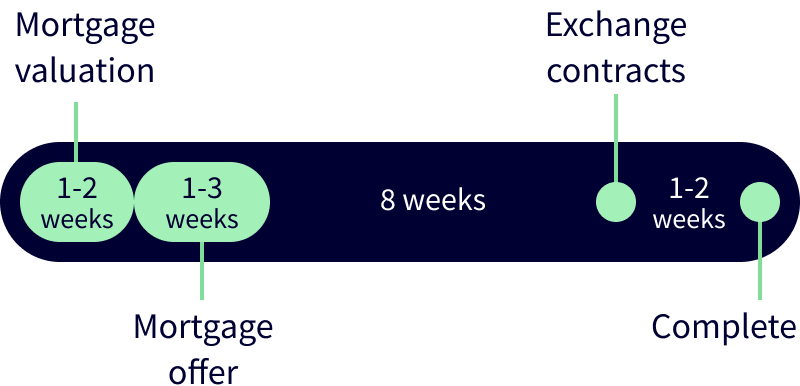

To check the value of the property, they’ll do something called a ‘valuation survey.’ This normally gets completed around 1 to 2 weeks after you send in your application. So, what does it involve?

Well, your lender might arrange for someone to go into the property to take a look, or they might do what’s called a ‘kerbside valuation’ where they drive past and look at it from the outside. However, most mortgage lenders nowadays will just do a ‘desktop valuation’. This is where they use recent sales data online, without even seeing the house in-person!

Some mortgage lenders will ask you to pay for the valuation (which could cost anywhere from £150 to £1,500). But other than that, you won’t have to worry about it at all – your lender will sort the whole thing out themselves. All you have to do is make yourself a cuppa and twiddle your thumbs for a bit.

Just beware: the mortgage lender’s valuation won’t be very detailed, so you’ll probably want to get your own survey carried out before you buy the property. That way, you can make sure you’re not overpaying.

You’ll want to make sure your surveyor is registered with a governing body that sets high standards for the work carried out, such as the Royal Institution of Chartered Surveyors (RICS) or Residential Property Surveyors Association (RPSA). To find one, you can look on the RPSA or RICS websites.

Getting a mortgage offer is the moment where you’re officially approved for a mortgage. Hooray! Normally, once your mortgage valuation’s out of the way, your lender should have everything they need to make a decision.

That said, you’ll normally still have to wait around 2 to 20 days to find out whether or not it’s good news. So, now’s a great time to start making your way through all 639 episodes of The Simpsons (you’ll need something to distract yourself, right?!).

If you’ve been approved for a mortgage, your lender will send you the offer in the post – now’s when you jump up and down excitedly before ringing everyone in your phone book! If it’s bad news – and we hope it’s not – get yourself a load of Ben + Jerry’s, wallow in self-pity and ask your mortgage broker what went wrong.

Just remember: your mortgage offer can still be withdrawn right up until the time you complete (that’s what we call it when you finally get the keys to your home.). So, lay low and don’t do anything that might put them off.

Ideally, that means no switching jobs, no big spending and no taking out additional credit agreements. You’re so nearly there!

Exchanging contracts is the moment where there’s no more turning back as both you and the seller are legally committed to getting the house sale done. Eek!

Normally, this happens around 2 months after you hand in your mortgage application. But there’s a ton of legal stuff that your solicitor will have been sorting out while you were waiting on your mortgage offer. So, at this point, it all depends on how the legal stuff is looking!

That’s right, even though you’re not waiting for your mortgage lender anymore, you are still going to have to wait for your solicitors to get their act together. Ultimately, when you’re buying a house, you’ll get pretty good at waiting!

Completion is what we call it when all the money goes through and the house is officially yours. In other words, it’s the day you get to pick up the keys and start life in your very own home!

The date of completion is normally decided by you and the seller before you exchange contracts. It’s usually around 1 to 2 weeks after the date of exchange, but it can legally happen the next day, so if you’re in a rush, it could be a lot quicker.

That said, some lenders require you to leave at least 5 working days between the two. And to be honest, a little gap’s no bad thing. After all, it gives you the chance to start packing your things, ready for the big move!

Every mortgage lender’s different. So it makes sense that some will process a mortgage application quicker than others. To help you get your head around it all, we’ve listed the average time it takes to get your mortgage application approved with some of the big lenders.

We get it: you want to get your mortgage approved as quickly as possible. Who wouldn’t when they’ve got a gorgeous new home they’re desperate to move into?!

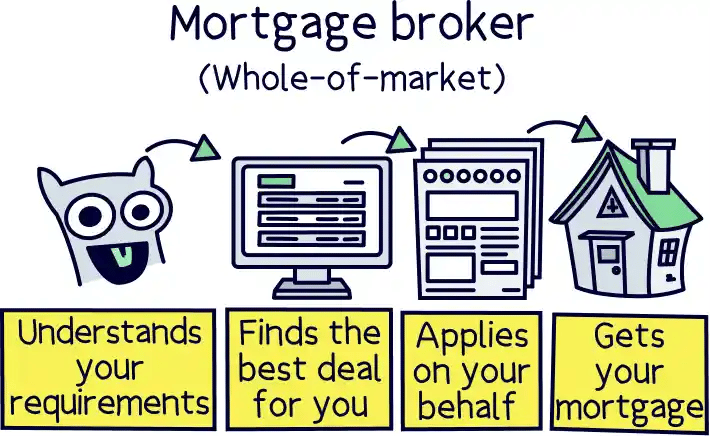

If you’re looking to speed the process up, the best thing you can do is get an independent mortgage broker involved (there’s a reason we frequently refer to them as ‘lifesavers!’). A mortgage broker will know exactly which lenders are most likely to approve your application and will be able to get you the best deals. So, you won’t have to waste time shopping around.

Plus, they’ll know exactly what each lender will need as part of the application process and will be able to get the whole application sorted for you much quicker. After all, this is what they do for a living!

Not sure where to find a great broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. You'll also get 50% off their fee with Nuts About Money. How great is that?

Okay, so it can take a while to get a mortgage application approved. But once you’re popping open the prosecco and unpacking those boxes, it’ll be so worth the wait!

If you’re ready to kick off the process, why not get in touch with a mortgage broker straight away?

Not sure where to find a good mortgage broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.