Article contents

Finding a cheap mortgage, and the best mortgage for you is actually pretty simple. Just use the experts, they do it for a living. They’ll find the best mortgage deal for you, and even handle all the paperwork too. You can’t go wrong, and some of them are even free.

Finding the cheapest mortgage for you can be the difference of £100s per month, and £1,000s over a year. Imagine all that extra cash!

It’s definitely worth the time looking for a cheap mortgage and to find the best deal for you. And it’s not as hard as you might think, in fact, that’s the job of a mortgage advisor – you only have to provide your details, and they’ll handle the rest.

A good advisor will be able to find the best mortgage for you, from every mortgage out there – there’s over 20,000 mortgages in the UK, from over 100 mortgage lenders (the people who give out mortgages). It's pretty difficult to search them all by yourself. Plus, they’ll give general mortgage advice too, and answer all of your questions.

But let’s not jump to that step straight away, let’s run through how to find the best deal:

This step is pretty essential. You need to have some idea of how much you can borrow for a mortgage before you can get started. You need to know you can actually borrow the amount you want for your new home, especially if you are a first time buyer trying to get on the property ladder.

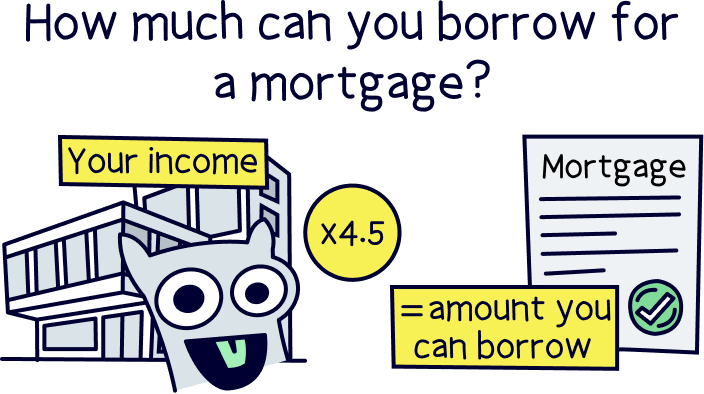

As a general rule of thumb, you can multiply your yearly income (e.g. salary) by 4.5, to get a rough idea of how much you can borrow. So, if your salary is £25,000, you can borrow up to £112,500.

You can then add your deposit to your borrowing amount to get the amount you can actually buy a new home for. However, if you only have a small deposit it can get a little complicated…

You’ll need at least 5% deposit, and often 10%, in order to actually be able to get a mortgage. So, if you only have, say a £5,000 deposit, you can only buy a property worth £100,000 (as £5,000 is 5% of £100,000). Which means you can only borrow £95,000 for a mortgage, even if your income means you can borrow more.

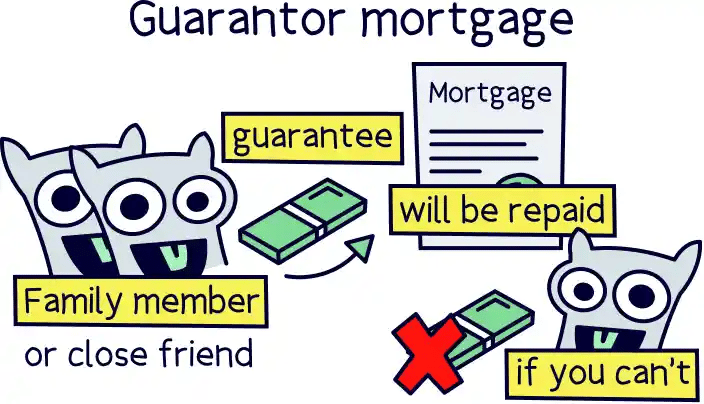

You can sometimes get a mortgage with no deposit, called a 100% mortgage if you use a guarantor mortgage (where a close family member, such as a parent, helps you out). Or, even a ‘deposit boost’, to give you a bigger deposit and therefore potentially able to borrow more money. We’ll cover how to find these later.

Luckily, you don’t have to do any of the maths yourself, simply use a mortgage calculator. You’ll get a rough idea of how much you can borrow in a few minutes. Try our favourite mortgage calculator by Tembo¹, it’s quick and very accurate.

Now you know how much you can borrow, you can work out your loan-to-value, or LTV. Your LTV will have a massive impact on the mortgage rate you will get.

We touched on it above, and it’s pretty simple to work out, it just sounds super complicated. First, work out your total borrowing amount (4.5 times your income), or if you’re remortgaging (switching deals), how much your house is worth. A rough idea at this stage is completely fine.

Then, if you’re looking to buy a home:

Pretty simple once you know how to do it right?

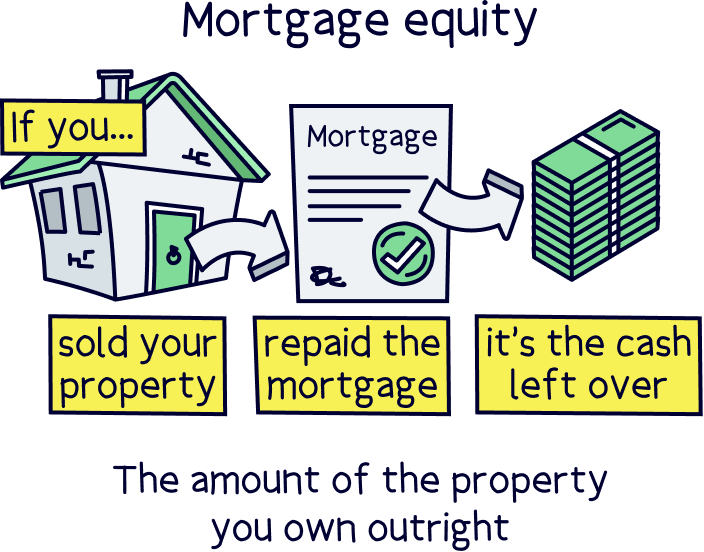

If you’re remortgaging, instead of using your deposit, work out how much ‘equity’ you have in your home. Your equity is how much of your home you effectively own yourself. If you sold it, it’s how much you’d get back after paying off the mortgage.

It works the same as a deposit, except you use your equity instead of a deposit. So, take how much mortgage you have left to pay away from the current value of the property to get your equity.

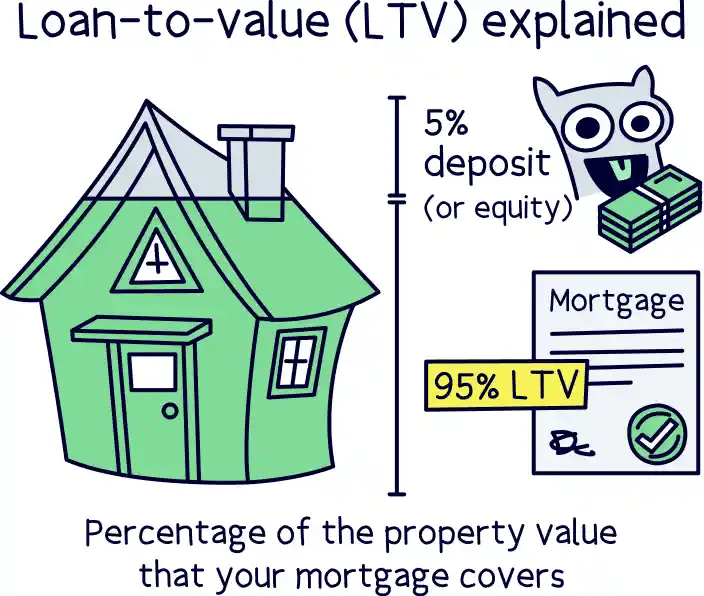

For instance, if you have a £100,000 mortgage left to pay, and your home is worth £150,000, then your equity is £50,000 (£150,000 - £100,000).

This would give you an LTV of 70%. How? You take £50,000 (your equity) and divide it by £150,000 (your property value), to get 33%, and then take that away from 100%, to get 67%.

Before you say anything, we didn't make a mistake! It’s not quite 70%. Unfortunately, mortgage lenders only work in 5% intervals, so you have to round up to the nearest ‘0’ or ‘5’. In our example 67% becomes 70% LTV.

The lower your LTV, the better mortgage deals you can get – as you’re using more of your own money to buy the property, rather than the banks money. This means it’s less risky for the bank to lend you money and so they’re happy to lend it out at a lower interest rate.

Tembo will find your best deal, fast, all with award-winning service.

Now you know how much you can borrow, and what your LTV is (or a rough idea of both anyway), it’s time to start looking at mortgage deals!

This step is just to have a quick look at what’s out there. Don’t apply for any mortgage yet! We recommend using a mortgage advisor to actually find the best deal for you, and to apply for the mortgage too – they’ll handle everything! But that’s the next step.

Before that, simply head over to a mortgage comparison table¹ to compare mortgages. This will show you what a realistic mortgage deal will look like, and allow you to play around and compare deals.

The key things to look for are:

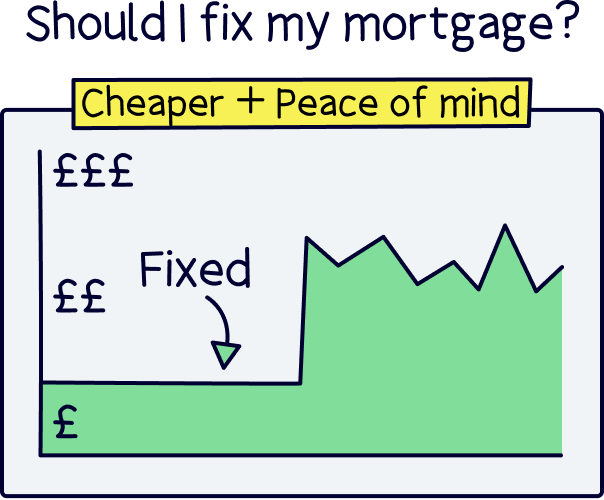

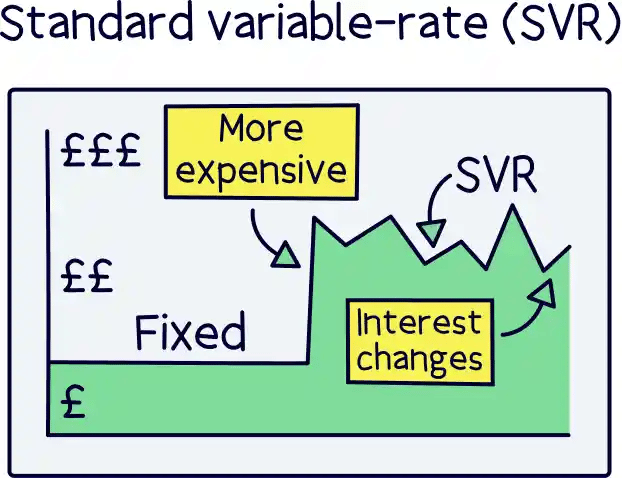

How long the deal is for is called the ‘fixed rate’ period, and sometimes ‘initial rate’, which is normally 2 or 5 years. It’s the period of time your mortgage deal is fixed at that particular interest rate. And the lower the fixed rate period, generally the cheaper the mortgage is, but you don’t have the certainty of the interest rate and monthly payments for as long…

After the fixed rate period ends, your mortgage rate will increase to the mortgage lender’s standard variable rate (SVR), which is their ‘default’ rate for their mortgages – and often very high.

It’s a good idea to switch deals (remortgage) when your fixed rate comes to an end. In fact, we recommend you start to look for a new mortgage deal 6 months before this point, as you can lock in a good deal that will start immediately after your current deal finishes!

And finally, the overall cost of the mortgage deal is the most important one! This is how much the mortgage will cost in total over the fixed rate period, and because you’re going to remortgage after the fixed rate period ends (right?), this is all that matters.

The overall cost takes into account the interest you pay, plus all the fees included within the mortgage itself, such as any fees just to get the mortgage from the lender (arrangement fees), and any other hidden fees.

So, just remember to compare overall cost, not just the interest rate. Lenders often give cheaper interest rates to get higher up on comparison tables, but then charge massive set up fees to make up for it.

Note: mortgages also show APRC, which stands for Annual Percentage Rate of Charge, and measures the average interest rate across the whole of the mortgage, i.e. 25 years (the mortgage term). However, it’s not an accurate figure to look at as you should be switching deals way before the end of your mortgage, either after 2 or 5 years. Simply look at the overall cost over the fixed rate period.

The mortgages you’ll see are often out of date – the mortgage market moves pretty fast, and one reason why our next step is getting the experts involved. There’s also some good mortgage deals that only mortgage advisors can access.

Plus, you can’t be sure you’re getting the right mortgage for you just by looking at a comparison table – there’s a lot of different types of mortgages suited to different people. It’s better to get everything checked over by an expert. You could save a lot of money, and save time too.

Right, now is the time to get serious! Once you've got an idea of your borrowing amount, your LTV and have a rough idea of what mortgages are out there, plus if you can afford them, it’s time to get an expert involved and really get the ball rolling.

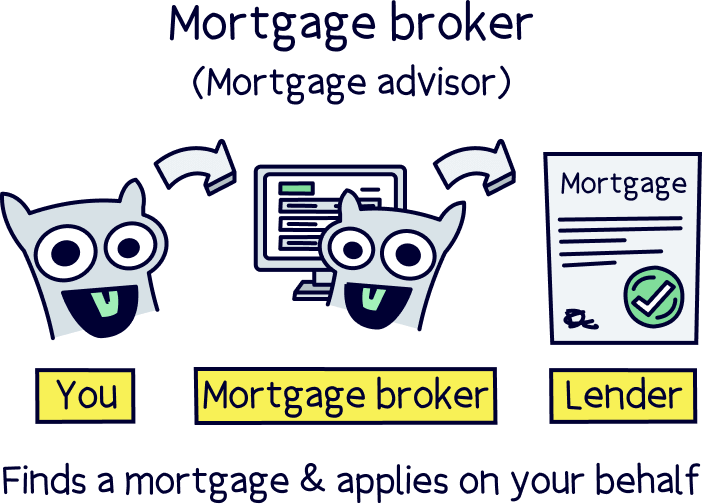

A mortgage broker (or advisor, it’s the same thing), is there to compare mortgage deals and find the right mortgage for you, based on your circumstances, and they’re very good at it. Plus, they’ll give mortgage advice in general, and help with everything.

They’re able to search every mortgage deal out there in a much quicker time than you could yourself, so you can be sure you’re getting the best mortgage for you.

First, they’ll get to know a bit about you, your personal circumstances and the type of property you’re looking to buy or remortgage. And as an added bonus, they’ll handle all the paperwork for your mortgage too. You don’t need to do a thing.

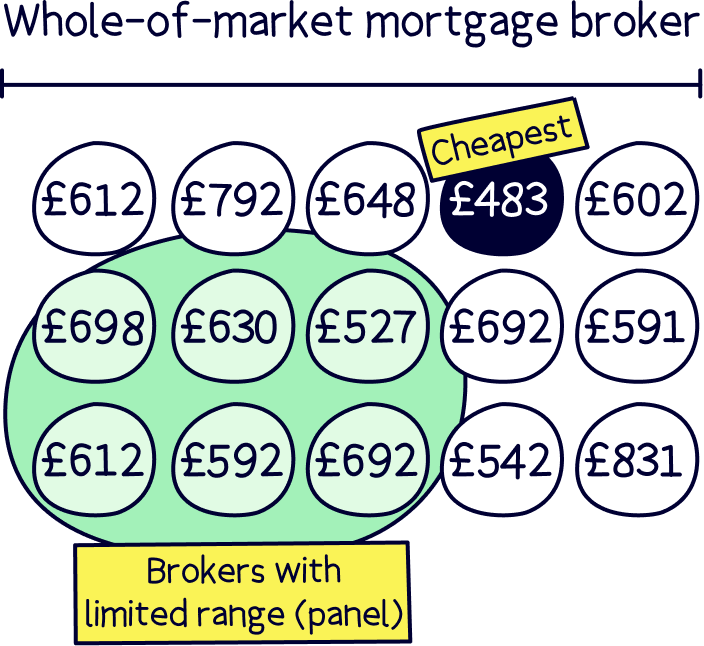

There’s just one major rule here – make sure they are a ‘whole-of-market’ broker, which means they can search every mortgage deal out there. If they can’t, then you can’t be sure you’ll be getting the best deal, which means potentially paying £100s more per month than you have to.

Some brokers can only search a handful of mortgage lenders, and if you get mortgage advice from your bank, they can only search the bank’s mortgages, which isn’t a sensible way to search for a mortgage. Never walk into your bank and ask for a mortgage! Always use a whole-of-market independent mortgage advisor.

They’ll also advise on the right type of mortgage for you. And there’s quite a range:

Not only will an advisor look for the cheapest mortgage for you, they also know all of the mortgage lenders criteria, which is what lenders use to determine if you are a good fit for their mortgages.

For instance, some might not like self-employed people, certain types of jobs, or those on a low income. There’s a whole range of things that lenders take into account, and a mortgage broker knows all of these and knows which mortgage lender is best for you.

If you do apply for a mortgage yourself and get declined, it can have a negative impact on your credit score, and can sometimes mean you won’t get a mortgage when you apply again to another lender. So, always make sure you have the highest chance of getting approved for a mortgage before you apply.

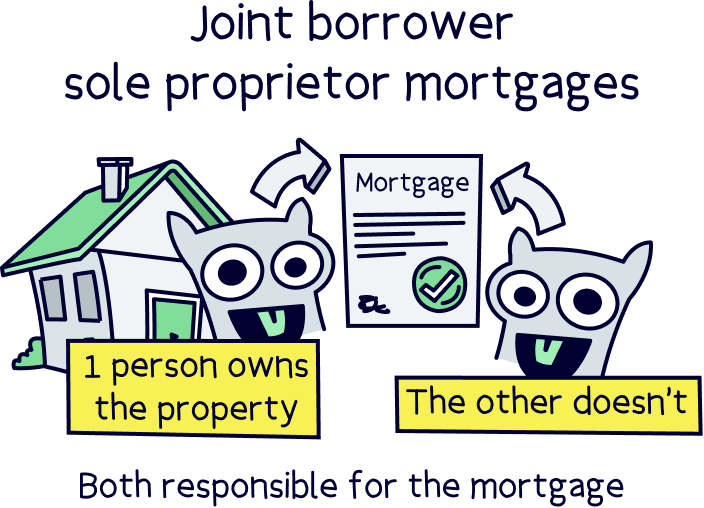

The mortgage broker will be able to determine if there’s more specialist types of mortgages available that might help you be able to borrow more money, or if you’re a first time buyer, help get a mortgage if a regular mortgage is becoming difficult. Some examples are guarantor mortgages and joint borrower, sole proprietor mortgages.

As an added benefit, using a mortgage advisor gives you the protection that if you do end up on the wrong mortgage (unlikely), you’ll be able to claim compensation from them as part of the Financial Services Compensation Scheme (FSCS).

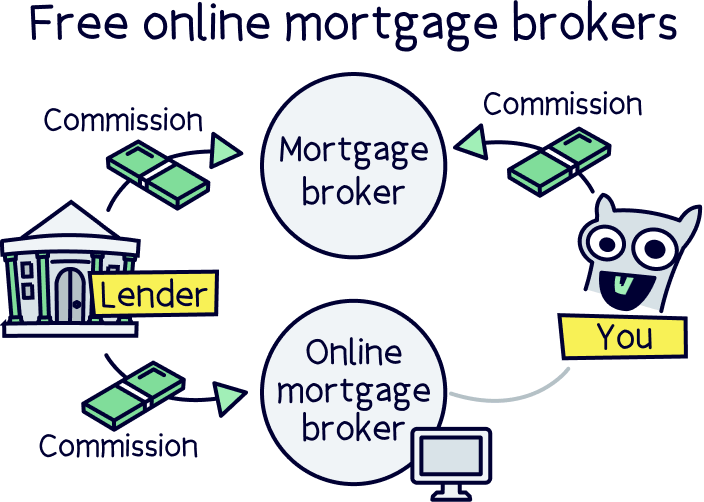

The very good news here is that some mortgage advisors are actually free! All mortgage advisors get paid commission from the mortgage lender when they find you a mortgage, but most also charge you too.

This is completely fine, and almost all local mortgage brokers will do this. Expect to pay around £500 as a broker fee. If it’s any more than this, and you’re not getting a specialist mortgage, it’s likely too much.

However, if you use an online mortgage broker, they’re typically free, plus, everything is super easy, and works to your schedule, as it’s all online. You can even do it on your phone in front of the TV!

Not sure where to find the best mortgage brokers? Here’s our recommended brokers:

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

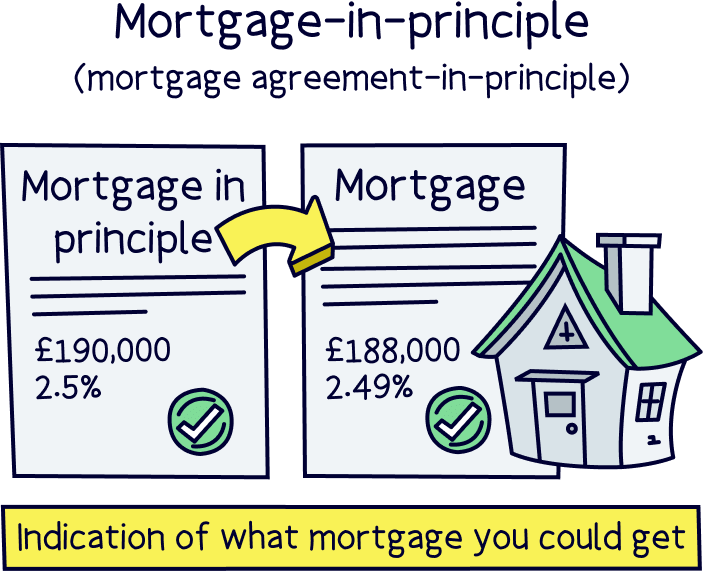

Once your mortgage advisor has got to know you and what the best mortgage will be for you is, they’ll now get a mortgage agreement in principle. This is normally a formal offer from a mortgage lender saying they’re happy to give you a mortgage. Whoop!

It will say the mortgage amount, overall cost, mortgage rate, the repayments and everything else you need to know. And providing nothing changes from your side (such as getting a new job), you’ll be able to get the mortgage when you make a ‘full mortgage application’. (The technical term for this is an ESIS mortgage Illustration or a key facts illustration.)

After that, you can go and make that offer on your dream home!

Note: you’ll most likely need a mortgage-in-principle before you go house hunting properly. Lot’s of estate agents want to see this as it shows you’re a serious buyer. Although you can get one online quickly in a few minutes with Tembo¹. This will show you how much you can likely borrow (it’s just not an official offer from a lender).

This step is optional, but if you want to be 100% sure there’s no better deal out there than the one you’ve been given, you can check all the direct-only deals too.

A direct deal is where a mortgage lender doesn’t work with mortgage brokers (or most of them), you have to go directly to them to get a mortgage. The most popular one of these is First Direct, but there’s also Yorkshire Bank.

And finally, it’s time to get the mortgage and buy your dream home! (or switch mortgage deals if you’re remortgaging).

If you’ve found your perfect home, and had your offer accepted, it's time to let your mortgage advisor know, and for them to make a full mortgage application.

This might take a while for everything to go through, and your lender might want to do a valuation on your property to make sure the mortgage amount matches up. After that, you’ll get a mortgage offer. Whoop!

Then if you’re buying a home, it’s over to your solicitor or conveyancer (the legal people) to do all the legal stuff, and to finalise any surveys you might be getting.

Note: if you’re remortgaging, the legal stuff is often carried out by the lenders themselves and free! Here’s where to learn more about costs to remortgage.

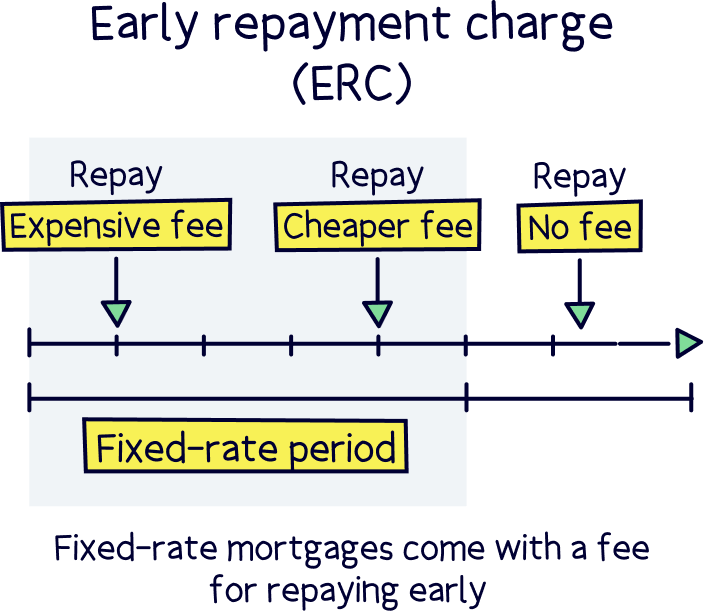

If you’re looking for a new remortgage deal. Watch out for the early repayment charges (ERC) on your current mortgage (also called exit fees). If you are still within your fixed rate period (so normally the first 2 or 5 years of your mortgage, depending on which length of time you went for), you’ll have to pay a pretty hefty fee.

It normally starts high and scales down each year, so if you have a 5 year fixed rate mortgage, the first year might be 5% of your mortgage, and then 4% for the 4th year, 3% for the 3rd year and so on.

This means it’s only worth switching deals when your fixed-rate period ends, and you are due to move onto the mortgage lender’s standard variable rate (the very expensive ‘regular’ mortgage rate from your lender) – where there are no fees to switch deals. A mortgage advisor can help you navigate these fees and if it’s worth switching deals early or not.

Finding a cheap buy-to-let mortgage is exactly the same process. You don’t need to use a specific buy-to-let mortgage advisor, a ‘regular’ mortgage advisor is just the same. Just let them know you’re looking for a buy-to-let, and possibly an interest only mortgage (where you only pay the interest every month), and they’ll handle the rest.

A bit easier than you thought? It’s pretty simple really – just let the experts handle everything. Get an idea of how much you can borrow first, the monthly repayments and overall cost, and then let a mortgage advisor take care of the rest.

You’ll be confident that you’re getting the cheapest and best mortgage for you, and you don’t even need to do a thing. They’ll handle everything, all the way through the mortgage process.

Plus, some online mortgage brokers are even free, how good is that? Just remember, only use a whole-of-market mortgage broker, otherwise you can’t be sure you’re getting the cheapest deal.

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. Plus, get 50% off their fee with Nuts About Money.

That's it! Good luck – not that you'll need it, now you know how to find the cheapest mortgage deal!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.