Article contents

Remortgaging can actually be completely free! Typical costs are just the mortgage broker fee, which can be free too. And if there’s mortgage fees, they can be combined with the mortgage (so you don’t pay upfront). Remortgaging is often worth it as you’ll end up on a much better mortgage deal.

Want to remortgage (switch mortgage deal), but worried about the costs? Don’t be!

Remortgaging doesn’t have to be expensive, and you can end up saving £100s per month.

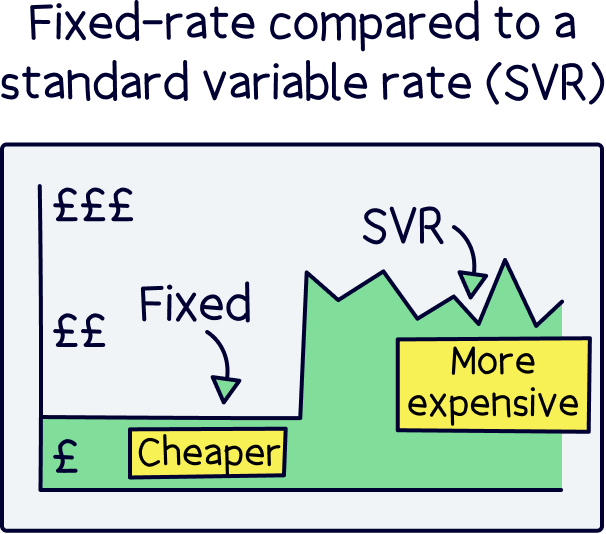

If the fixed-rate period (the cheaper bit at the start, more below) of your mortgage has ended or is finishing in the next 6 months, you should remortgage to a better deal, and potentially save thousands.

The fixed-rate period is normally the first 2 or 5 years at the start of your mortgage. Lenders (the people who give you the mortgage), normally give you a cheaper rate to start as an incentive to use them. Once this is over your interest rate will go up (to their standard variable rate, their default high rate). This is when you should remortgage!

Tembo will find your best deal, fast, all with award-winning service.

During the fixed-rate period, if you remortgage, you’ll have to pay fairly hefty fees (early repayment charges), but after this there’s no fees! (We’ll cover this in more detail below).

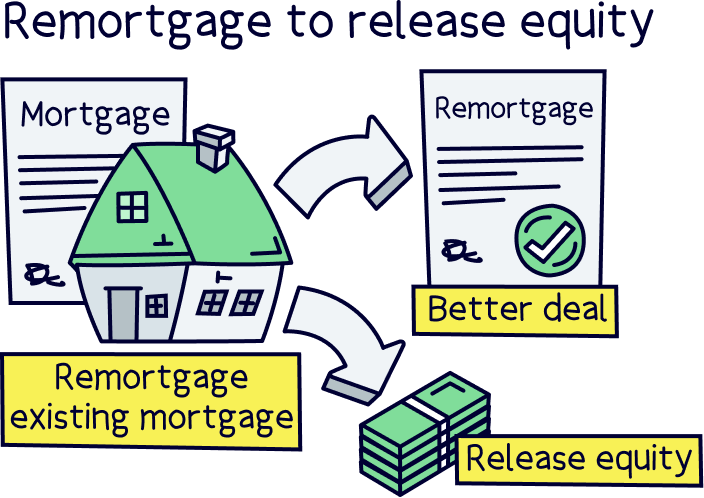

Note: if you are looking to remortgage to borrow more (release equity), you’ll be able to remortgage and get cash out, and still be on the best deal at the new mortgage amount.

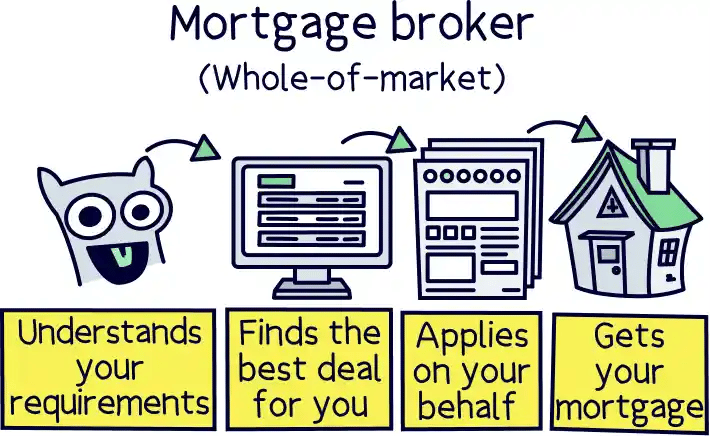

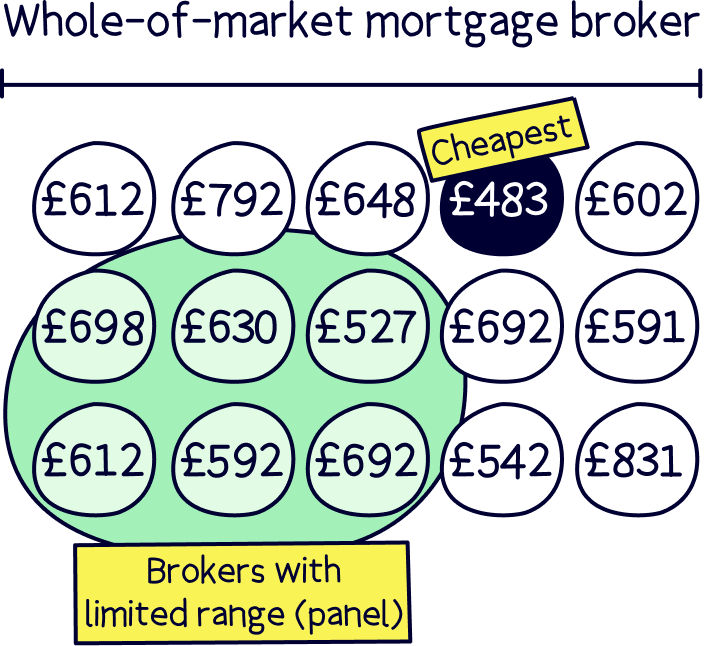

You can remortgage yourself, but you'll get a better deal if you use a whole-of-market mortgage broker (these guys will search every mortgage out there to get you the best deal). They'll also handle all the admin too, and even apply on your behalf. (More on brokers later).

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. (Get 50% off with Nuts About Money too).

Let’s run through all the costs you might be facing when you remortgage.

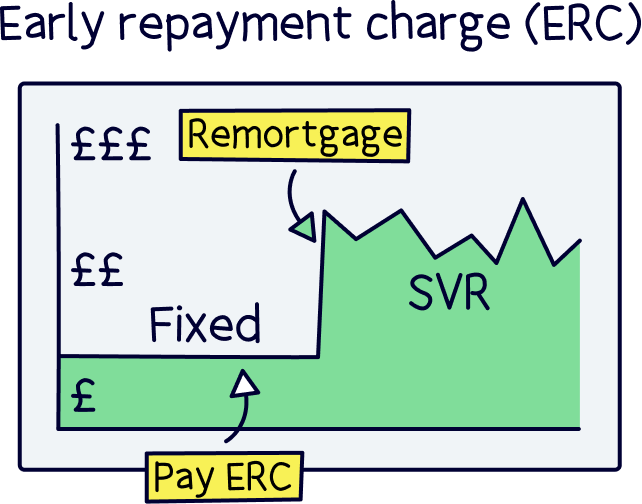

As mentioned above, if you are in your fixed-rate period, which is the incentive period you agreed to when you took out the mortgage, normally 2 or 5 years, (where the interest rate was fixed at normally a low rate).

This low rate is great unless you want to remortgage within the fixed-rate period. If you want to do that, you’ll normally have to pay an early repayment charge (ERC).

This charge (fee) is normally a percentage of the mortgage amount, and is more expensive at the start of your mortgage, then reduces as time goes on.

For instance, if you have a 5 year fixed rate deal, typical ERC charges for switching deals are:

So if you had a mortgage of £200,000 and you wanted to remortgage within the first year of taking out the mortgage, you’d have to pay £10,000 in fees! It’s very unlikely that switching to a new deal at this point would make you better off.

However, it’s worth doing the maths, it may actually work out there's potential savings in future by switching to a new mortgage deal and paying the early repayment charges.

Note: this fee does change depending on the mortgage lender, so you’ll need to check your current mortgage. A mortgage advisor can normally find this out for you too.

By the way, when you remortgage, you are actually paying off the mortgage and taking out a new one, hence the name early repayment charge.

So, providing you are coming to the end of your fixed period you can get a new deal (you can actually get a new deal in place in the last 6 months of your current mortgage). If your fixed rate period has finished, you should remortgage immediately as you are probably paying a lot more than you could be!

If you haven’t got a fixed-rate mortgage, you might have a variable rate mortgage (where the interest rate can change, normally when the Bank of England base rate changes), then you might not have any early repayment charges and can remortgage whenever you like. Check your mortgage paperwork, it should say clearly.

To find the best new mortgage deal for you, you should use a mortgage advisor (also called mortgage brokers).

Providing your advisor is able to search the whole market, they can check every mortgage deal out there to find the best one for you. The whole market just means every mortgage deal in the UK. And only use an advisor that can! Make sure you ask if you’re not sure. Here’s more questions to ask a mortgage advisor too.

A broker will also do the maths for you if you are still in your fixed rate period, and tell you if it’s worth remortgaging or waiting a bit longer.

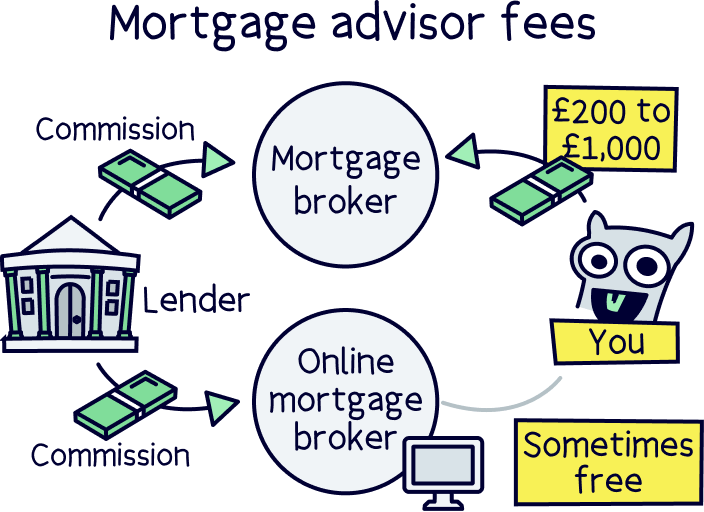

The costs for a mortgage advisor can vary, from being completely free, to as much as £1,000 and sometimes more. The average is around £500.

However there are great free options, check out Habito¹ – they’re a free online mortgage broker, who searches the whole market. And their customer service is very good (here’s our Habito review).

Or, if you prefer to chat to a mortgage broker check out Tembo¹, you could be chatting to an expert it just 10 minutes (get 50% off with Nuts About Money).

When you take out a new mortgage, there can be a mortgage arrangement fee, also called a product fee or booking fee. This is what the mortgage lender charges, and can range from £0 to around £2,000 (normally free or £999 though). However don’t let this put you off.

Arrangement fees are a bit of a game with lenders, it’s how they make a lot of their money, alongside the interest you pay on the mortgage.

In order to manipulate the interest rates, and make them lower (so customers think they are getting a good deal), they increase the arrangement fee so they still get the same amount of profit (remember banks are not your friends!).

And if you opt for a mortgage with no arrangement fee, you’ll often see the interest rate is a bit higher. This is why you should never just look at interest rates by themselves.

However, it’s still worth remortgaging, all you need to do is look at the total cost of the mortgage, which includes the arrangement fee and add it to the interest you would be paying during the incentive period of the new mortgage (the fixed rate period with a low interest rate).

That sounds a bit complicated, but a mortgage advisor will do this for you. That’s their job!

There is good news however, you’ll never have to pay this fee upfront unless you want to, you can add it to the mortgage, and it will just make your mortgage slightly bigger.

When you remortgage and switch deals to a new lender, there’s some legal work to be done (called conveyancing), which is effectively changing the mortgage to the new lender.

If you were buying a new home, you’d have to pay the legal fees yourself.

However, with remortgaging, you don’t need to worry about these, you don’t need your own solicitor (conveyancer), the mortgage lenders have their own legal teams who will sort everything out between themselves.

So, often all the legal stuff is free. It’s very unlikely you’ll be charged any legal fees, and you’ll know beforehand if you are, so you can find another lender if you want to.

If you weren't aware, your mortgage lender holds the deeds to your home, until the mortgage is paid off. The deeds are a document stating you own the property. You still own the property, they just hold the deeds.

When you remortgage, you are getting a mortgage with a new lender, and ending your current mortgage with your current lender. Therefore, your new lender needs the property deeds to your home, and your old lender needs to send them to them (via solicitors).

So sometimes your existing lender might charge a fee, this is often free however and it might not even come up, but sometimes you might have to pay somewhere between £50 and £300.

Your new mortgage lender will also want to value your property, to make sure they aren't giving you more money (the mortgage) than the property is worth (this is called negative equity).

The property may have gone up in value too, so you may find you are getting an even better mortgage deal.

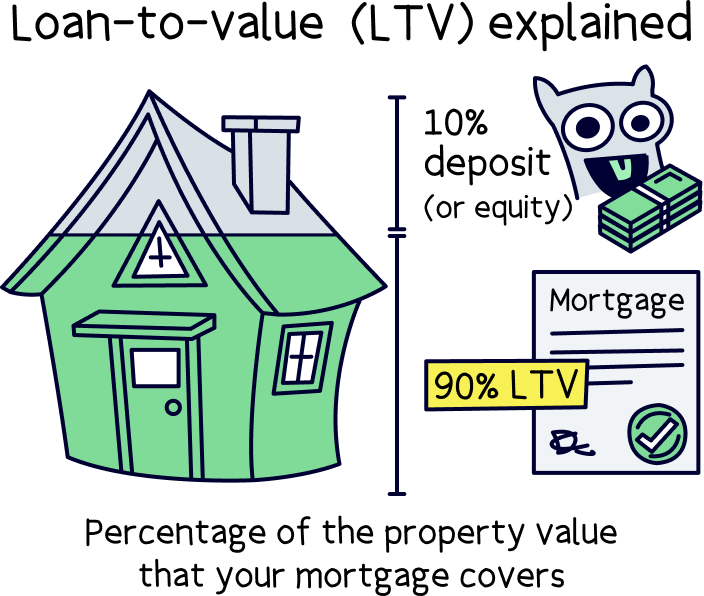

When your property is worth more and your mortgage amount stays the same, your loan-to-value (LTV) goes down. Your LTV is simply a measure of how much you are borrowing vs the value of the property.

So for instance, an LTV of 90% means you are borrowing 90% of the value of the property. When the property value goes up, this figure goes down, and so mortgage lenders often give better rates because there’s less risk for them (because you own more of the home yourself).

When you bought the home you probably paid for a property valuation, and this is normally around £500, but can be lots more. However with most remortgages this is actually free – there’s no valuation fees!

Let’s just run through that all again in a clearer way:

Wait a minute, does that mean there could be no fees at all? Well often, yep! You can often remortgage for free, with no fees at all, or no upfront fees with an arrangement fee added to your mortgage. Pretty great right?

Remortgaging is far easier than getting the mortgage in the first place, phew!

As long as you’re not in your fixed rate period (the incentive period at the start of your mortgage, normally 2 or 5 years), you shouldn’t face any big fees.

And if you’re not in your fixed rate period, you should probably look at remortgaging as soon as possible, as you’ll most likely be paying too much, and can easily save big money by switching to a new deal.

To remortgage, there’s actually not much for you to do. The best way is to simply get a mortgage advisor to handle everything for you. It’s what they do, and you can be sure you’ll be getting the best deal (if you use a whole-of-market broker).

It’s just like switching phone contracts, except you could save £100s per month!

It really is that easy! We recommend Tembo¹, they've got award-winning service and will guarantee to get you the best deal – potentially saving £100s. Get 50% off their fee with Nuts About Money too.

You’ll be on a new deal and saving money in no time!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.