Article contents

Don't fear. Mortgages for the self-employed aren't as scary or as difficult as you think. We're on your side, here's what you need to know.

Self-employed? Wishing you could get a mortgage? The good news is, you probably can! Although getting a mortgage can be a little harder for someone who’s self-employed, it’s totally doable. And we’re here to guide you through it all.

First things first, let’s iron out the most important detail of all: do you count as self-employed in the eyes of mortgage lenders?

Most mortgage lenders will count you as self-employed if you own more than 20% or 25% of the business that gives you your main income. In other words, you could be a sole trader (someone who owns and runs their own business as an individual) or you could be the partner or director of a limited company (someone who owns and runs their own business as a company, either by themselves or with other people).

You could also be a self-employed fixed-term contractor, where you’re guaranteed work from specific clients for a set amount of time – if that’s you, check out our guide to getting a mortgage on a fixed-term contract as well.

If you’ve spent your whole working life wondering: ‘Can you get a mortgage if you are self-employed?’ then we’re here to put you out of your misery. Yes, you can!

Self-employment is becoming more and more common. According to Citizen’s Advice, 1 in 7 of us now works for ourselves! That’s a lot. And most of these people are going to want a mortgage at some point or other. So, it stands to reason it’s totally possible to get one.

At the same time, it is a little trickier to get a mortgage if you’re self-employed than it would be for a full-time employee. Let’s take a look at why.

Tembo will find your best deal, fast, all with award-winning service.

Think about it: a mortgage lender isn’t going to want to lend you the money to buy a house if you’re not going to be able to pay it back.

When you’re self-employed, it can be hard to prove to a mortgage lender that you’re going to be able to keep up your mortgage repayments. That’s because you won’t have an employer who can confirm your salary. You might also be receiving different amounts of money each month, which might lead them to worry about whether your income is going to be consistent enough.

All this means that you’ll have to jump through a few more hoops to get a mortgage than someone who’s a full-time employee. But let’s get this straight: it doesn’t mean you can’t get one. It just means you’ll have to work a bit harder to prove you’re someone who’s going to be able to pay the money back.

As a general rule of thumb, you’ll need to be self-employed for around 2 years before you apply for a mortgage. That’s because most mortgage lenders will want to look at your accounts from the last 2 or 3 tax years to work out how much you’re earning.

If you’re newly self-employed and you only have 1 year’s worth of accounts or less, it’s going to be difficult to convince a mortgage lender that you can afford a mortgage. But (and there’s always a but!!) it’s not impossible, and lenders are relaxing their rules around this more and more as more of the UK goes self-employed.

Every mortgage lender is different and no two self-employed people are the same! Some mortgage lenders might be willing to lend to you if you only have 1 year’s worth of accounts, particularly if your application is strong in other areas. For example, it might help if you’ve been in the same industry for a while, or if you can prove you have some long contracts lined up.

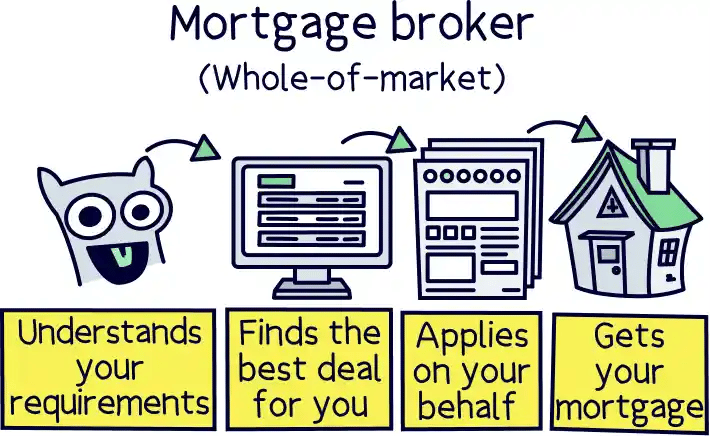

Always get in touch with a mortgage broker (also known as a lifesaver!) to find out if there’s a mortgage lender out there who can work with your circumstances. They’ll know all about the self-employed mortgage requirements for different lenders and they might even recommend a lender who specialises in mortgages for self-employed people.

Not any more! There used to be a thing called ‘self-certification mortgages’ where you could get a self-employed mortgage with no proof of income. But after the credit crunch in 2008, they were mostly withdrawn from the market, and they were eventually banned in 2014.

Why? Well, they were enabling people to get mortgages who couldn’t afford to repay them.

Look, we’re not psychics so it’s impossible to tell you whether or not you’re going to be able to get a mortgage. After all, we know nothing about your finances or your work history… or how good you are with money!

That said, we can give you an idea of some of the things that might help. Here are a few factors that mortgage lenders will usually look at when they’re deciding whether or not to give out mortgages to self-employed people.

The main thing that mortgage lenders care about is whether they’re going to be able to get their money back. In other words, are you going to have enough income to be able to afford your mortgage repayments?

They’ll want to be sure, so they’re not just going to ask you the question outright (they used to, but that’s another story… will reveal all later). Instead, they’ll want to work out whether you’ll be able to afford the repayments for themselves.

To do this, they’ll usually look at your accounts, as well as a tax overview from HMRC or your SA302 tax calculation (this is a document that you can get hold of once you’ve completed your tax return. Just visit the GOV.UK website).

If you’re a company director, they’ll also ask for proof of dividends and sometimes they’ll want to see proof of retained profits too (that’s the money that’s still in your company account that you haven’t yet paid yourself).

Have you earned a decent amount over the last few years? Great news! Most mortgage lenders will average out the profits you’ve received over the last two or three years to work out your income. That said, if you were earning a lot less a few years ago, don’t panic. Some mortgage lenders will be happy to take a more recent figure if you can show that your profits are going up each year.

Often, mortgage lenders will prefer it if your accounts have been prepared by a qualified, chartered accountant. This way, they can feel more confident that the information they’re getting is truthful and reliable.

If you’re a contractor, you might be able to make a mortgage lender even happier if you can also show them proof of any upcoming contracts you’ve got in the bag. After all, then they’ll know you’re going to be able to afford your repayments (at least for a while!).

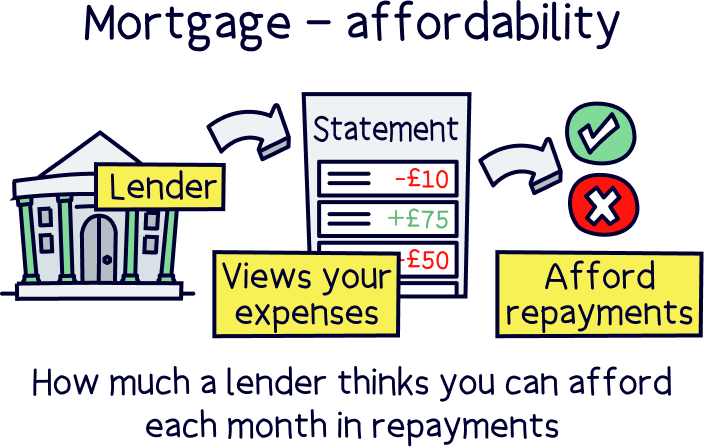

You might be rolling in cash every payday, but if you go and spend it all on the latest cars and gadgets, that’s not really going to help you afford your mortgage repayments, is it?

That’s exactly why a mortgage lender won’t normally just look at how much you earn. They’ll also look at how much you spend. So, most mortgage lenders will ask to see your bank statements.

That’s right, they’ll be sifting through all your dirty laundry to get a better idea of how much you're spending on things like childcare, holidays, bills and hobbies. So, before you apply for a mortgage, try to get a handle on your spending. That means staying away from fancy holidays and new cars until after you’ve moved into your dream home. You can do it!

Have you got a great track record of earning consistently as a self-employed worker? Crack open the champagne! If you can show you have experience paying the bills on a self-employed basis, you’ve got a good chance of continuing to do so. And that’ll make a mortgage lender very happy.

But if you’re newly self-employed, all is not lost. You might still have a ton of relevant experience (albeit as an employee). Maybe you were an in-house graphic designer and now you work for yourself in the same field? Or maybe you used to work for an accountancy firm and now you run your own limited accounting company?

Whatever your line of work, if you have previous experience working in the same job role or industry, that probably means you’re good at your job. So, a mortgage lender might feel more confident that you’re going to be successful now you’ve gone self-employed.

If your job role is in high demand, that’s even better! After all, if lots of people need your services, you’re more likely to have consistent work than you are if you’re newly self-employed in a field that’s competitive and over-saturated. Fingers crossed anyway!

Have you got a student loan? A credit card? A car on finance?

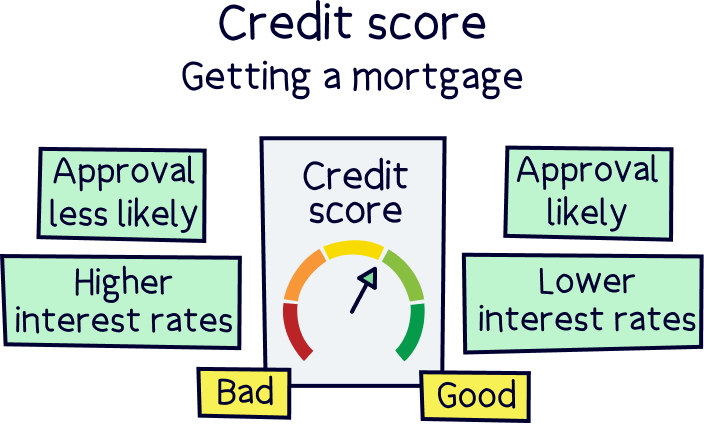

Your credit score is a number that shows mortgage lenders how good you are at paying back any money you’ve borrowed. If you always pay things back on time, you’ll usually have a good credit score, which means mortgage lenders can feel confident you’ll pay their loan back too.

But if you have any unpaid credit cards and bills, you might have a bad credit score. This could be a problem for a mortgage lender. After all, if you haven’t paid back loans in the past, how can they be confident that you’ll pay back your mortgage?

To get an idea of what shape your credit score’s in, check out our guide to what credit score you need for a mortgage.

We hate to break it to you, but getting a mortgage with bad credit is very hard. And it’s going to be even harder (if not impossible!) if you’re self-employed. So, you’ll want to spend some time improving your score before you apply.

In other words, pay off any unpaid credit cards, get up to date with your bills and don’t take out any more loans. We have faith in you!

Don’t just sit there wishing and dreaming! When it comes to getting a mortgage as a self-employed worker, there is stuff you can do to make it more likely you’ll get accepted.

So what are you waiting for? Follow these simple steps to help things along.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Okay, so you know how every mortgage lender’s different? Well, it stands to reason that some will be better for self-employed workers than others. To give you some idea, we’ve taken a look at some of the best mortgage lenders for self-employed people in the UK.

Don’t forget: we have no idea which mortgage lender is best for you. After all, we’ve never met! And there are over 100 mortgage lenders in the UK, who all have different requirements.

To find your perfect lender, get in touch with an independent mortgage broker. Not only will they take the time to get to know your circumstances and give you tailored advice, but they’ll even fill out the application for you. It’s a win-win!

Not necessarily! There’s actually no such thing as a ‘self-employed mortgage.’ Instead, you’ll mostly be applying for the exact same products as everyone else – it’s just that you’ll have to prove your income in a different way.

That said, it does help if you can put forward a big deposit. That’s because it shows mortgage lenders how serious you are about buying a property and so it makes you seem less risky. In a nutshell, a big deposit will give you access to the best deals. And who doesn’t love a deal?!

So, what are you waiting for? Is it too early to celebrate?

Whether you’re ready to put in a mortgage application tomorrow, or you need to spend a little bit longer improving your credit score, one thing’s certain: you shouldn’t let your self-employed status put you off from applying for a mortgage. After all, self-employed people get mortgages all the time!

If you’re ready to take the first step, just get in touch with an independent mortgage broker to chat things through. An independent mortgage broker will be able to search through every mortgage lender out there to find you the best one for your specific circumstances. They’ll also be able to give you advice about what’s a good deal and how you can reduce your mortgage repayments. Ultimately, they’re the superheroes of the property industry!

As a reminder, if you need to find a decent mortgage broker check Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.