Article contents

If you want to keep your property after splitting with your partner, you could buy them out. This might involve remortgaging to get hold of the cash.

Do you share your mortgage with someone else? Are they moving out?

Whether you share your mortgage with a friend, partner or spouse – and whether you’re parting ways because of a divorce, breakup or change of circumstances – by buying your partner out of the mortgage, you could continue living in your dream property for as long as you want. Sound good? Here’s all you need to know.

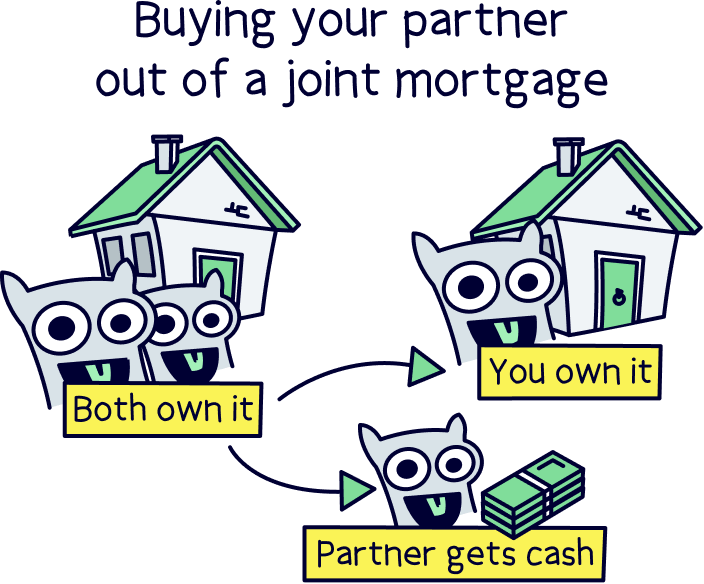

Okay, so first things first: it’s important to know that everyone listed on the mortgage is responsible for keeping up the repayments. Yep, that’s right. Even if your partner moves out of the property, they can still be chased for the mortgage repayments – unless you buy them out.

When you buy your partner out, their name is removed from both the mortgage and the property’s title deeds. In other words, you take ownership of their share of the house (known as a transfer of equity) and you become solely responsible for paying the mortgage. Your home’s all yours.

The same goes if there are more than two of you listed on the mortgage. If someone leaves, one of you could buy off their share on your own, or you could all pitch in to split it. For the time being though, we’ll assume there are only two of you!

Tembo will find your best deal, fast, all with award-winning service.

As you can imagine, buying your partner out of a joint mortgage isn’t cheap, especially if they’ve made a lot of mortgage repayments and contributed towards the deposit.

Here’s how to work out how much it’ll cost.

Confused? Don’t worry, it’s a lot easier than it sounds. Here’s an example to prove it...

Let’s say you bought your house for £200,000. Your partner put down a £20,000 deposit. And since then, you’ve paid off £60,000 of your mortgage between you. Assuming you’re splitting the value of the house in two, it’ll cost around £50,000 to pay off your partner. That’s half of the amount you paid off together (£30,000) plus the deposit your partner paid upfront (£20,000).

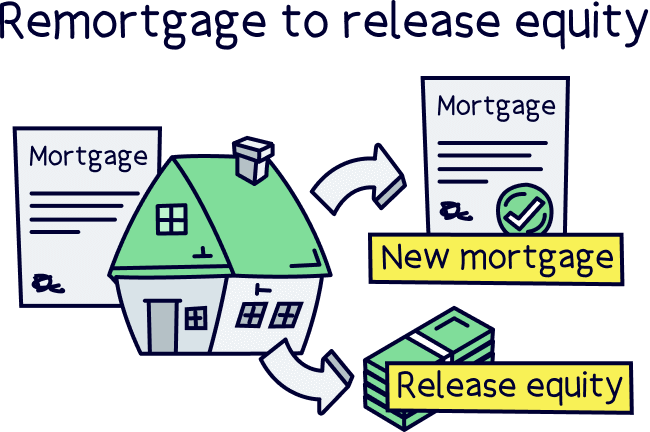

Now, obviously, £50,000 is a lot for most people to cough up in one go. So, you might need to remortgage to get hold of the cash. Which leads us onto...

Most of us can’t afford to just buy a partner out using our savings. So, it often means taking out a new, bigger mortgage (known as remortgaging) to release some equity for the partner that’s leaving. In other words, you’ll end up paying your partner off by borrowing more from your mortgage lender.

That said, if you can pay them off in cash, you may be able to stick with the same mortgage and just change the names on it, known as a ‘change of borrower.’

Either way, you’ll need to prove to your mortgage lender that you can afford the monthly repayments on your own.

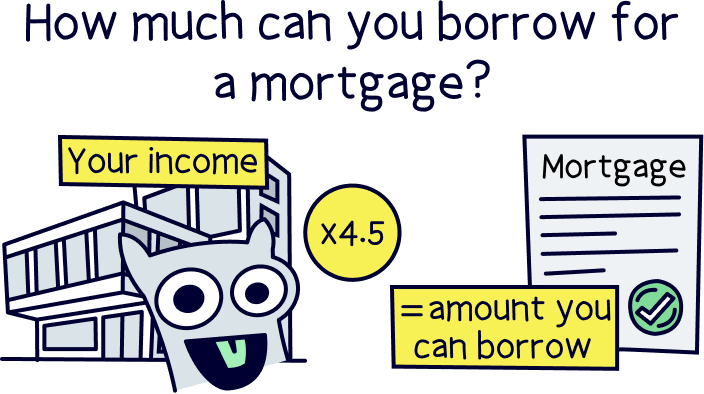

Put it like this: when your lender first agreed to give you a mortgage, they would have looked at how much you and your partner were earning together. Now that you’re hoping to repay the mortgage on your own, they might be worried that you’re not going to be able to afford it.

Normally, you can get a mortgage that’s around 4.5x the amount of your yearly income.

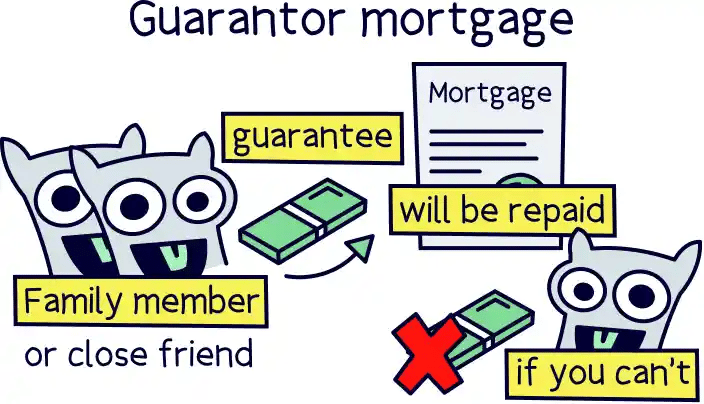

Not going to stretch far enough? Don’t panic. You could consider taking out a guarantor mortgage or a joint borrower sole proprietor mortgage. This is where someone close to you (usually a family member) agrees to pay your mortgage if you can’t.

Just be careful: these arrangements are legally binding and usually involve your guarantor putting their own property up for ‘security.’ This means that if neither of you can afford to settle your mortgage repayments, their house could get taken away from them! So, take some time to think things through carefully before jumping into anything.

If you’re interested in getting one of these mortgages, check out Tembo¹, they specialise in them. And, get 50% off their fee with Nuts About Money.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Buying your partner out of a joint mortgage isn’t your only option if you split. Here are some other things you could explore.

Whether your mate has just decided to move out or you’re facing a difficult breakup, parting ways with the person jointly responsible for your mortgage can be tough. But luckily, by buying your partner out, you won’t need to say goodbye to your home as well.

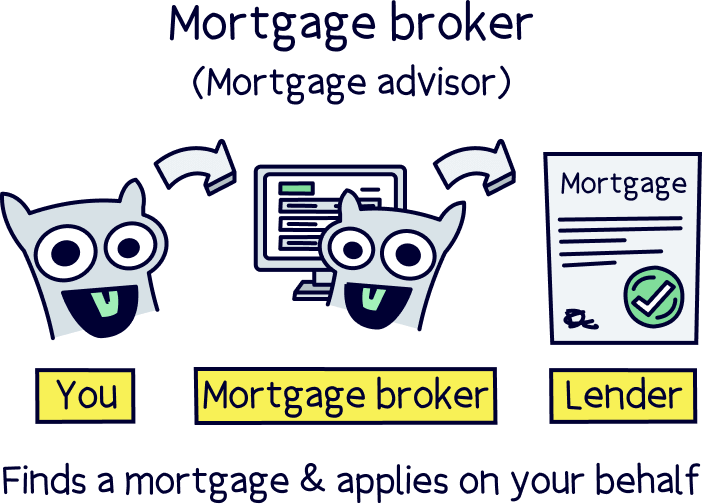

If you’re seriously thinking about buying your partner out of your joint mortgage, why not get in touch with a mortgage broker to talk things through and get some advice? In what’s likely to be a difficult time, they’re sure to make the mortgage side of things a whole lot easier!

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage. You'll also get 50% off their fee with Nuts About Money. How great is that?

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.