Article contents

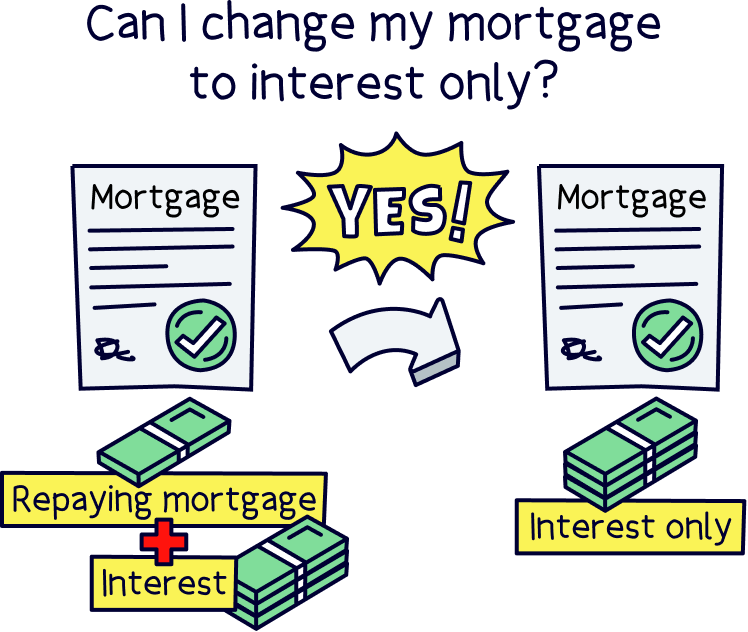

Yes! Most mortgage lenders will be open to changing your mortgage to interest only, but you’ll need a plan for how you’re going to pay the loan back once your mortgage ends.

Looking to reduce your monthly repayments? Got a plan for paying off your mortgage later down the line? An interest-only mortgage could be the answer.

Here, we’ll take a look at whether you could (and should!) swap to interest only.

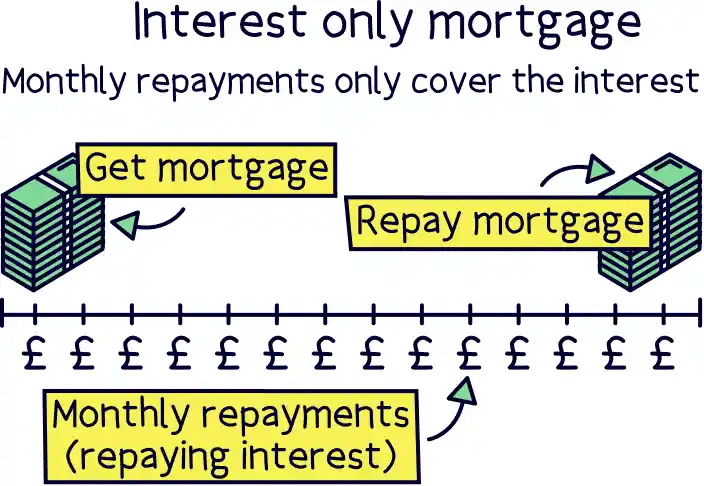

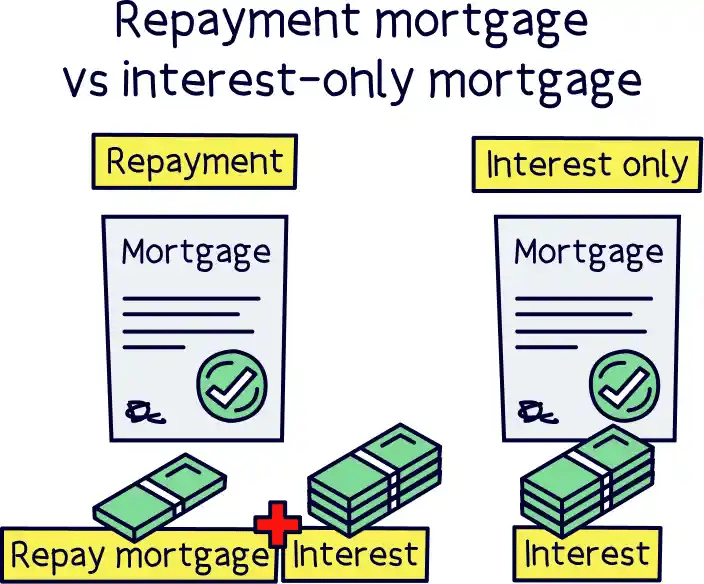

An interest-only mortgage is where your monthly repayments only cover the interest that’s building up on your loan. While that might sound pretty sweet, there is a catch. When your mortgage comes to an end, you’ll still owe your mortgage lender the full amount you initially borrowed. So, at this point, you’ll need to pay back the full loan as a lump sum (which might mean selling the property, depending on your circumstances). Eek!

On the other hand, most of us are on what’s called a repayment mortgage (also known as a ‘capital and interest mortgage’). This is where your monthly repayments go towards paying off your loan, as well as the interest. It does mean your monthly repayments are higher. But it also means that by the end of your mortgage term, you’ll have no debt left at all. In other words, you’ll finally own your property outright!

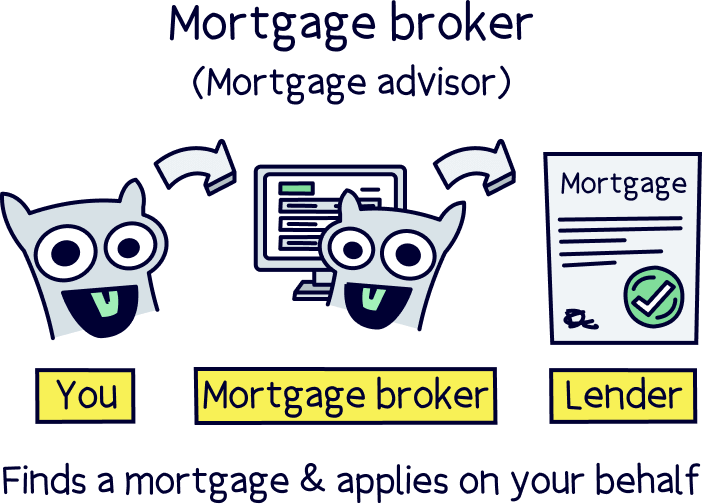

If your mind is set and you’re looking to get an interest only mortgage we recommend you first chat to an independent mortgage advisor.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. You'll also get 50% off their fee with Nuts About Money. How great is that?

Yes. Most lenders will be open to letting you change from a repayment mortgage to an interest-only mortgage. However, they’ll want to do some strict checks before they decide for sure, as they’ll need to be confident they’re going to get their money back!

The main things they’ll look at are:

Remember how we said that with an interest-only mortgage, you’ll need to pay back the whole loan as a lump sum when your mortgage comes to an end? Well, your lender’s going to want to make sure you can afford to do that. Otherwise, they’ll risk not getting their money back!

This is why you’ll need a clear repayment strategy. Don’t worry, it’s not as confusing as it sounds! A repayment strategy is basically just your plan for how you’re going to pay the lump sum back once your mortgage ends.

For example, are you planning on paying into a savings account each month? Do you have a buy-to-let property to generate the cash for you? Are you planning on putting this property on the market once your mortgage comes to an end?

Every lender will have a different set of criteria, but they’ll usually want to see proof that your plans are realistic. And if they’re not convinced, the likelihood is they won’t let you switch. It’s as simple as that!

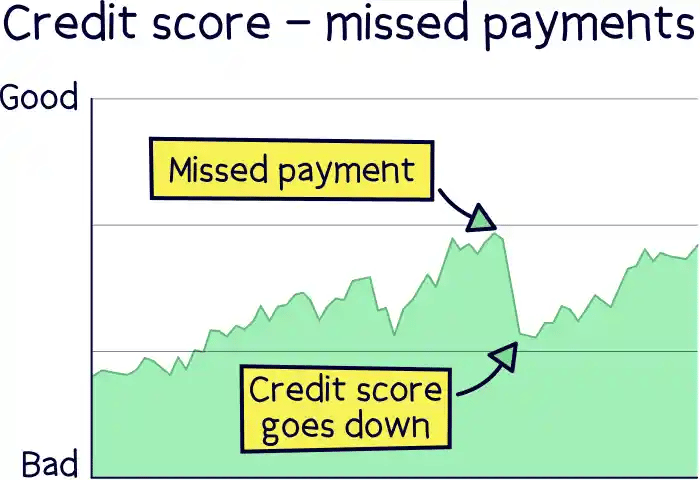

No matter what kind of mortgage you apply for, your lender will want to take a peek at your credit history before making a decision. This is what shows them how good you’ve been with money in the past, and whether or not you’ve paid back other loans on time.

If you were thinking of lending someone money, you’d probably want to check they had a good track record for paying people back first, right?!

Well, chances are lenders will look at your credit history even more carefully if you want to swap to an interest-only mortgage. Don’t worry, this isn’t because they’re trying to catch you out. It’s just because offering you an interest-only mortgage is a little riskier for them.

After all, with a repayment mortgage, you’ll start paying your lender back straight away. But with interest only, they may have to wait as long as 25 or even 35 years before you pay back a penny from the loan itself!

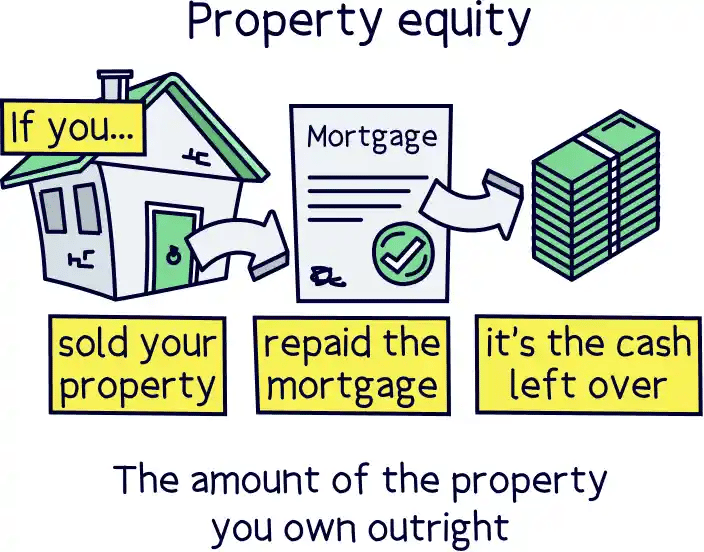

Another thing that lenders will consider carefully is how much equity you have in your property (‘equity’ refers to how much of your property you own outright).

If you own most of your property outright, happy days! Your lender will probably be more than happy to switch you over to an interest-only mortgage. However, if you don’t have much equity, you might find it tricky.

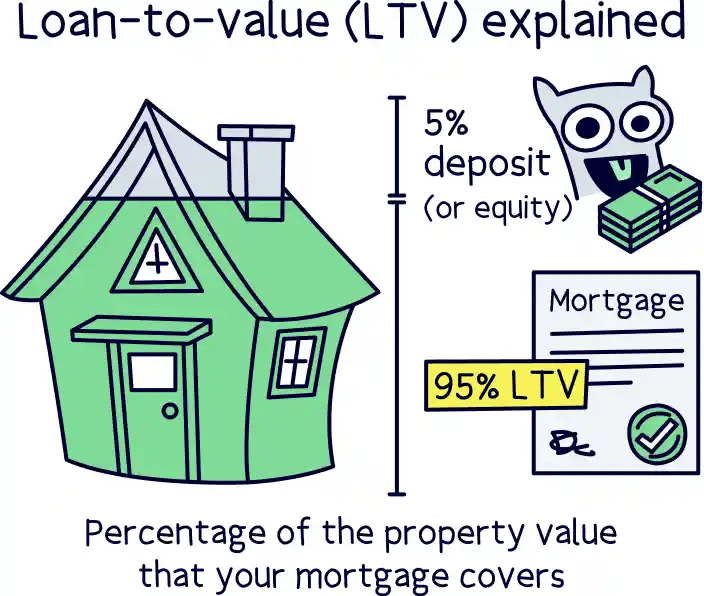

Essentially, this is all about the loan-to-value (LTV) ratio – the percentage of the property that you own outright, vs the percentage you still owe your lender.

While lots of lenders will let you borrow 95% of your property’s value on a repayment mortgage (known as a 95% LTV), they won’t normally let you borrow this much if you’re on an interest-only mortgage.

So, if you’re on a high LTV, you might need to wait until your equity increases before you switch to interest only. Normally, this is just a case of waiting until your property’s value goes up – it almost always will!

Alternatively, your mortgage lender might let you switch to a part-and-part mortgage. This is where part of your loan is repaid on an interest-only basis and part of it is repaid on a repayment basis. More on this later!

Tembo will find your best deal, fast, all with award-winning service.

For most people, the answer is no. To make an interest-only mortgage work, you’ll need to have a solid repayment plan. And even then, there’s always a risk that you don’t end up with the money you need to pay back your loan at the end of your mortgage term. So, it can be risky.

That said, there are lots of pros as well as cons. Let’s take a look at both sides of the argument...

Like the sound of your monthly repayments going down? An interest-only mortgage isn’t your only option if this is what you’re after. Here are a couple of alternatives you’ll want to consider before making a decision one way or the other.

If you’re struggling to make your monthly repayments, don’t automatically assume that an interest-only mortgage is your only bet. Instead, have a chat with your mortgage lender as soon as you can to explain the difficulties you’re having.

Many lenders will be happy to offer a mortgage holiday (also known as a payment holiday, freeze or deferral) where you can take a break from your monthly repayments for a set period of time. Or, they might offer you a partial payment holiday, where your monthly repayments are reduced for a while.

Mortgage holidays have been a particularly popular solution for those who’ve lost income due to the Coronavirus pandemic in the UK – over 1.8 million of them were taken up at the beginning of the pandemic alone, according to GOV.UK!

Just be aware that taking a mortgage holiday won’t wipe off your unpaid debt altogether (sorry!). Instead, you’ll still need to pay back what you owe once your mortgage holiday ends – usually by spreading out the missed payments over the remainder of your mortgage term. This means you’ll end up paying more interest in the long run.

A part-and-part mortgage is when you pay part of your loan back on an interest-only basis, and part of it back on a repayment basis. In other words, it’s part repayment and part interest-only!

We know what you’re thinking: ‘Is this the best of both worlds?!’

Well, that depends on what you’re after.

It’s a great alternative if your lender’s not willing to give you an interest-only mortgage, as it reduces the amount of risk for them, and it reduces the size of the loan you have to pay back in one big hit at the end.

However, you could also see it as neither here nor there – yes, your monthly repayments will be less than they would be on a repayment mortgage. But they’ll also be higher than they would be on an interest-only mortgage.

Similarly, although the lump sum you have to pay back at the end won’t be as big as it would be on an interest-only mortgage, you’ll still have to find a way to pay it. Plus, you’ll be paying more interest overall than you would be on a repayment mortgage.

So yes, in a way it’s a happy in between. But in another way, because you’re not committing one way or another, you’ll never fully reap the benefits of either.

Yes! It’s generally a lot easier to change from an interest-only mortgage to a repayment mortgage because it’s less risky for lenders. Ultimately, they’ll usually be delighted to let you swap!

That said, switching to a repayment mortgage will see your monthly repayments go up – often by quite a lot! So, you’ll need to prove that you can afford the new, higher rate you’ll be paying. Unfortunately, that means airing your dirty laundry – be prepared for a mortgage lender to do some snooping into your finances and your bank statements. And yes, that means now is probably not the best time to buy that fancy car you’ve had your eye on. Just saying!

Still thinking of swapping from a repayment to an interest-only mortgage? Or vice versa? We’d always recommend talking to an independent mortgage advisor first, as they’ll be able to give you tailored advice to suit your individual situation. Plus, they’ll handle the whole application process for you from start to finish.

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.