Article contents

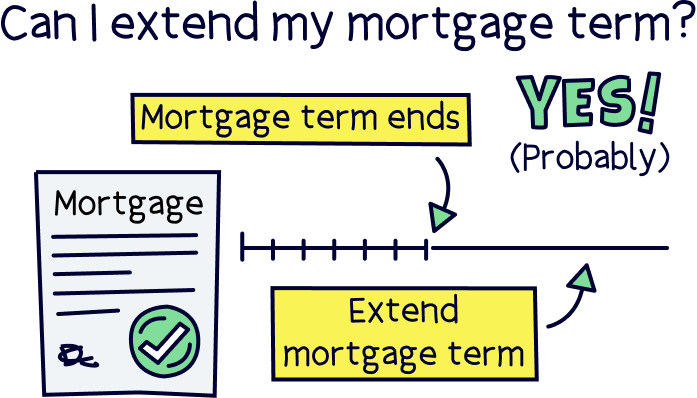

Yes you can extend your mortgage term, but only as long as you've paid it off before you retire. Extending it will mean lower monthly repayments but you'll pay more interest overall.

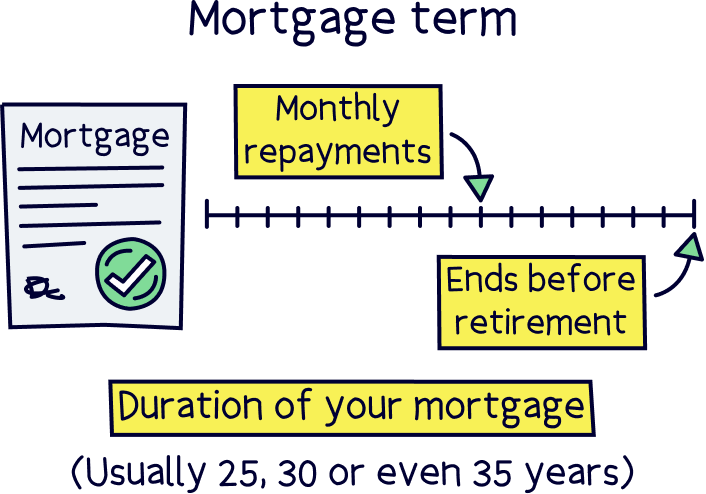

If you’ve taken out a mortgage, the chances are you’ve promised to pay it back over 25, 30 or even 35 years. This is known as your mortgage term. But the question is: once you’ve set your mortgage term, can you extend it?

In short, yes you can! We’ll explain it all below.

If you’re like most people, you’ll be on a repayment mortgage. This means that your plan and repayments are set up so that you’ll eventually own your property outright. In other words, if you’re on a 25-year term, after 25 years your house will finally be all yours. The same goes if you’re on a 15-year term, a 35-year term or anything else.

Of course, you may have moved house by the time your mortgage term comes to an end, but the point is that after this time, you’ll no longer owe the bank a penny.

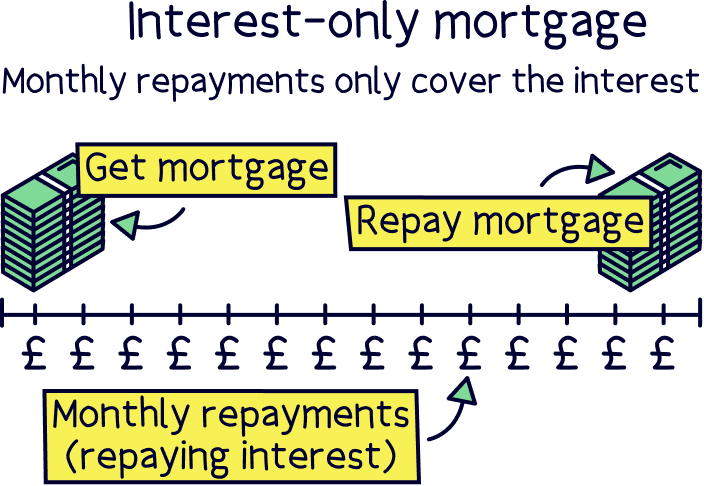

Alternatively, you may be on what’s called an interest-only mortgage. This is where your monthly repayments are only designed to pay off the interest that’s building up on your loan – not the loan itself. In this case, you’ll still have a mortgage term, but once the term’s up, you’ll need to pay back your mortgage lender what you borrowed in a lump sum.

If you’re on an interest-only mortgage, you’ll need to save up so you can pay your mortgage lender back once your mortgage term comes to an end. But coming up with such a massive amount of cash can obviously be tricky! If you need a little longer to save, some banks will let you extend your mortgage term to give you more time. Phew!

On the other hand, if you’re on a repayment mortgage, extending the term means your monthly repayments will go down. Sounds tempting, right?

Say you borrowed £200,000 and you’re paying 3% interest. On a 25-year mortgage term, that means your monthly repayments will be around £948 per month. But if you extend your term to 35 years, you’ll only need to pay around £770 per month. That’s £178 less!

Nuts About Money top tip: See what extending your mortgage term does to your monthly repayments and the interest you'll pay by using our mortgage comparison table.

Tembo will find your best deal, fast, all with award-winning service.

Bringing your monthly repayments down might seem like a great idea. After all, no-one likes paying more than they have to! However, it’s not all roses. Extending your mortgage term will actually increase the amount of interest you have to pay overall.

Don’t worry, it’s not as confusing as it sounds. Let’s go back to our previous example...

So you’ve borrowed £200,000 and you’re paying 3% interest. On a 25-year mortgage term, this means you’ll end up paying £84,478 in interest charges overall. But over a 35-year mortgage term, you’ll pay £123,201 in interest charges. That’s £38,723 more!

So, is extending your mortgage really a good idea?

Ultimately, it all comes down to how much you need those lower monthly repayments. If you’re struggling with the amount you’re having to pay each month, extending your mortgage term will probably be worth it. But if you’re managing just fine as it is, you might decide you’d rather pay off your mortgage quicker to take advantage of those lower overall interest charges (and to enjoy mortgage-free life sooner!).

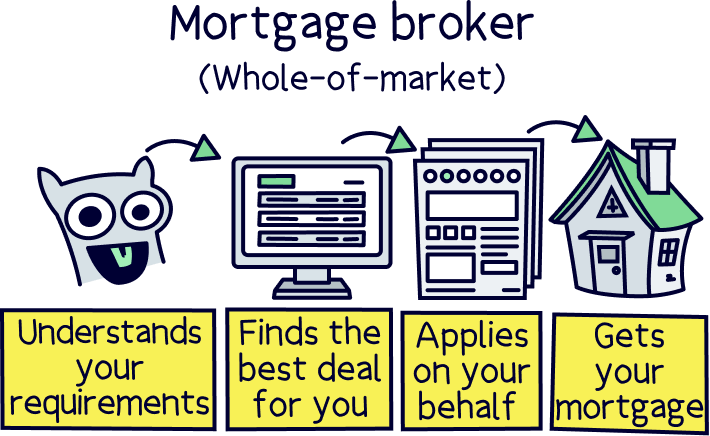

We’d always recommend chatting to an independent mortgage broker who’ll be able to give you tailored advice about what’s best for you.

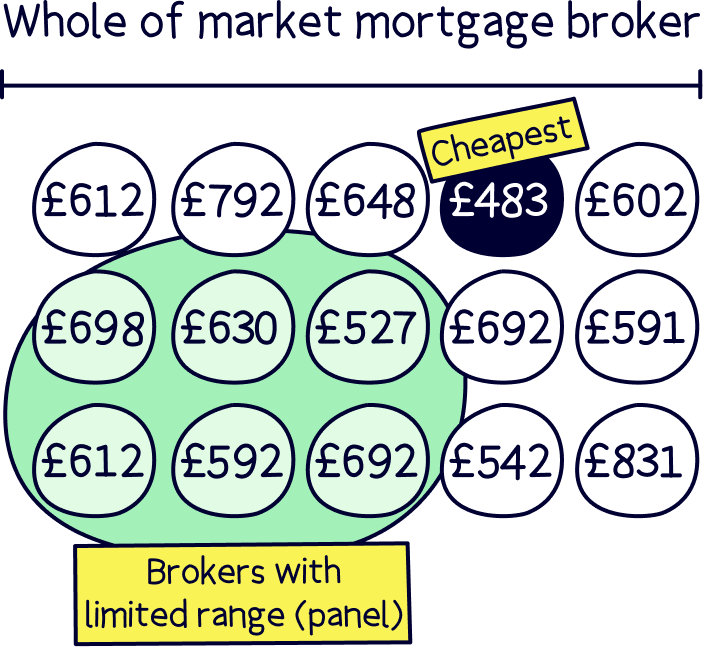

Nuts About Money tip: Make sure to use a broker who is 'whole-of-market' which means they can search every mortgage.

If you're not sure where to find a great broker, check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. You'll also get 50% off their fee with Nuts About Money.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Alternatively, you can get a rough idea of costs with different mortgage terms with our mortgage comparison table. It shows all the latest mortgage rates and you can find the best deal for you.

If you want to extend your mortgage term, you’ll just need to apply to your mortgage lender for an extension, or remortgage to a new lender on a new mortgage deal. Every mortgage lender is different, but most will take into account three key areas when they’re deciding whether or not to approve your request:

They say that age isn't about how old you are, but how old you feel. However, we hate to break it to you, but that’s not quite how mortgage lenders operate!

If you have youth on your side, lucky you. A mortgage lender is more likely to approve your request for an extension as the likelihood is you’ll be earning a salary for a long time yet. However, if you’re approaching retirement, this is where things start to get tricky – ideally, your mortgage lender will want you to pay off your mortgage before you retire. Why? Well, if you’re not going to be earning an income, you might struggle to meet your monthly repayments.

Most mortgage lenders also put a blanket age limit on mortgage products. For example, your 75th birthday.

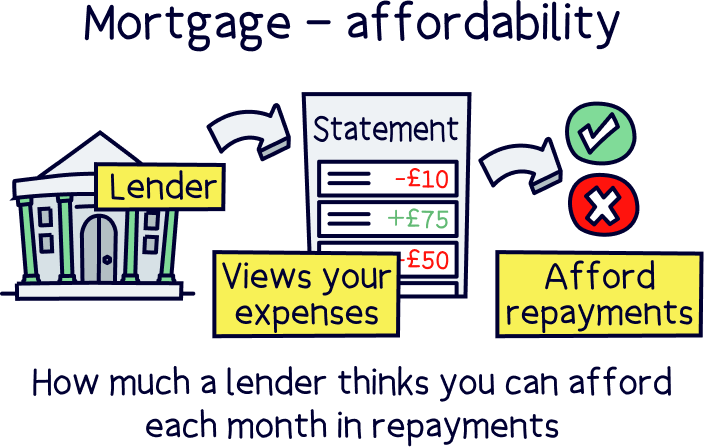

‘Affordability’ is all about whether a mortgage lender thinks you’ll be able to afford your monthly repayments. Because an extension to your mortgage term will bring down your monthly repayments, this isn’t usually a big concern.

However, if you’re approaching retirement age, that’s a different story! In this case, your lender will most likely do some checks to see whether they think you’ll be able to keep up your monthly repayments right up until the end of your new proposed term.

Even the most youthful amongst us won’t be able to extend indefinitely. Most mortgage providers won’t offer mortgages that are longer than 40 years. So, if you’re already on a 40-year mortgage, it’s unlikely you’ll be able to extend it further.

That said, this is probably a good thing. After all, who knows what you’ll be up to in 40 years’ time!

At the end of the day, everyone’s different and you’re the only one who can choose whether or not to extend your mortgage term. But a little advice can’t hurt!

If you’re umming and ah-ing about whether or not to extend, just get in touch with an independent mortgage broker. They’ll take the time to get to know your specific circumstances and will be able to help you come to a decision. Plus, they’ll even sort out the application for you.

Not sure where to find a good mortgage advisor? Check out Tembo¹, they've got award-winning service, and guarantee to find you the best deal. Plus, you'll get 50% off their fee with Nuts About Money.

And you can see what extending your mortgage term does to your monthly repayments (and how much more interest you'll pay) by using our mortgage comparison table.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.