Article contents

You need to tell your mortgage lender you are changing jobs, and, providing the job is similar and you can afford the repayments, you should be able to continue to get a mortgage.

Applying for a mortgage but changing jobs at the same time? Risky business.

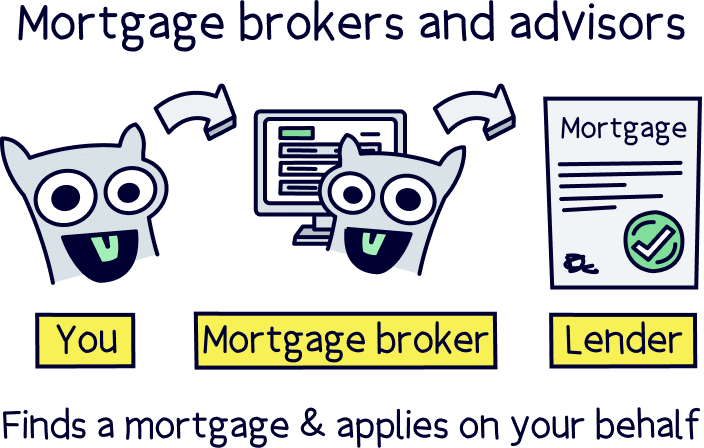

If you're changing jobs and you haven’t got a mortgage yet our advice is to chat to an independent mortgage advisor. They can run through all of your options and get you the best deal.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Alternatively, read our getting a mortgage with a new job guide.

Don’t panic! We’re not saying getting a new job isn’t ever a good idea and that you’ll be putting your security at risk. There’s just an ever so slightly higher risk of redundancy as a newer employee. You know the phrase ‘last one in, first one out.’ That’s what lenders are thinking.

Starting a new job means you’ll probably have a probationary period when you start. That’s a short period of time where your employer can end your contract at short notice. And if that happens, it could be difficult to pay your mortgage. It might be scary for you, but it’s also scary for your mortgage lender!

You may have just proved your income to get the mortgage approval, but changing jobs after means that it’s no longer true for the future. This makes the mortgage lender’s calculations invalid, and you left unable to prove your income just yet with no pay-slips. Essentially back to square one!

It means changing jobs after mortgage approval is not the best position to be in. The lender has assessed your previous situation and approved you for a mortgage, but now your situation is fairly different! That’s not to say that your mortgage is now declined, but that the lender needs to reassess their view on lending to you.

The first thing you need to do is let your mortgage broker know. They can advise on the situation and how to handle the lender. In fact, they’ll talk to the lender for you. You don’t really have to do much.

If your job is relatively similar, such as another full-time position with the same or better salary, you may be able to convince the lender to continue with the mortgage. But if you have moved to a part-time position or a fixed-term contract with a different salary, your lender is not going to like it. They are mostly concerned with your ability to repay the mortgage each month, and with a different salary, it’s going to be harder.

Tembo will find your best deal, fast, all with award-winning service.

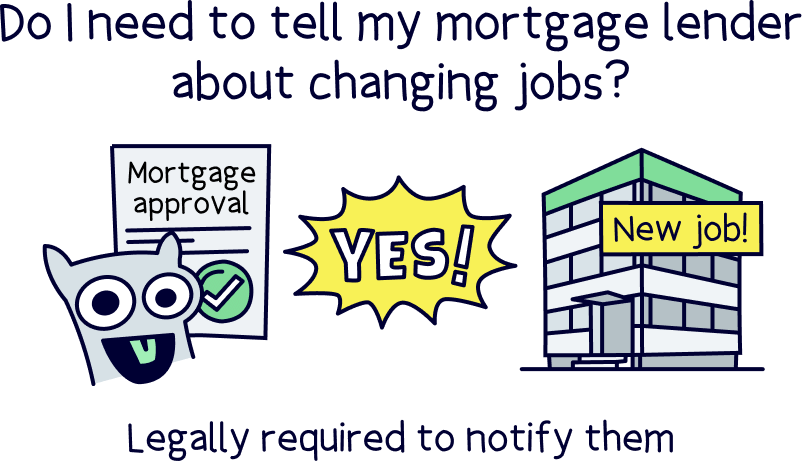

You can, but legally you have a ‘duty of disclosure’ between your mortgage application and mortgage completion (what we call it when the house sale goes through and you get the keys). This means you are legally required to notify them of any and all changes that are relevant to the mortgage application.

Lenders can also do further checks at this stage (these are often random checks and not all lenders will do them) so they could find out. Plus your employer has a duty to tell them that you are leaving your job if asked.

You need to inform your lender that you are changing jobs and put the power in their hands unfortunately. You should still be able to continue with the mortgage if you have a similar or better job to go to. After all, you’ll still be able to afford the repayments so there’s not much issue from the lenders view. No promises though!

If your job is drastically different, your mortgage offer is likely to be withdrawn and you won’t be able to get that particular mortgage., Most likely you can still get a mortgage, but you will effectively have to start the process again and hold out for a bit, until you have enough payslips to prove your new income is stable. This will typically mean waiting 3 months, and ideally passing your probationary period.

It’s all to do with affordability. Would you lend to someone if their income was about to change drastically? Probably not. Unfortunately, it’s not the best news to hear if you are in this position but don’t despair. You’ll get a lovely new home, it just might take a bit longer than you had initially hoped!

As a reminder, if you need to find a decent mortgage broker, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, you'll get 50% off with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.