Article contents

After you receive a mortgage offer, you’ll need to accept it by signing it and returning it to your lender. Then, it’s just a case of cracking on with your house purchase!

So, you’ve found your dream home, applied for a mortgage and finally got that offer you’ve been waiting for. Congratulations! But what happens next? Here, we’ll take a look at exactly what you can expect, including what to watch out for and how long you’ll have to wait till everything goes through.

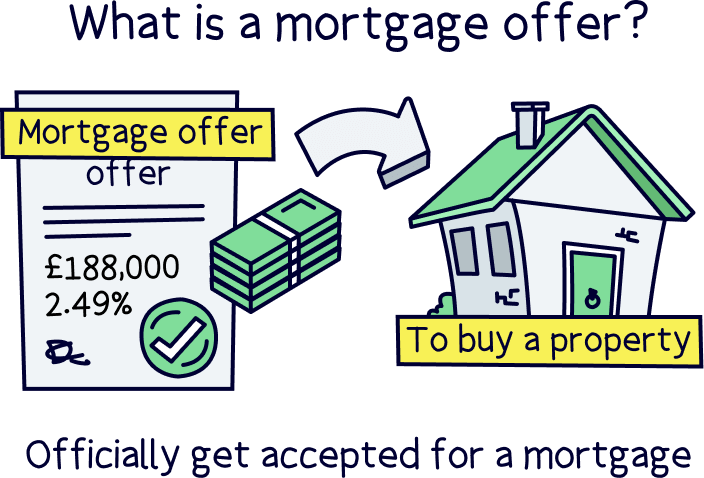

A mortgage offer is what it’s called when you officially get accepted for a mortgage. In other words, it means your lender (the organisation that you’ve asked for a mortgage from) has read your mortgage application, carried out all their checks and decided that they’re happy to give you a mortgage. Hooray!

Your mortgage offer will arrive in the post and will outline exactly how much your lender is willing to let you borrow. Sometimes it will also tell you that there are conditions attached. For example, they might want you to pay off another loan or credit card before they let you have the money.

Don’t worry, your conveyancing solicitor will also get a copy – and so will your mortgage broker if you used one – so you’ll have plenty of support if you need to chat things through.

Tembo will find your best deal, fast, all with award-winning service.

First things first, once your mortgage offer makes its way through your letterbox, it’s your chance to jump up and down, ring your friends, crack open the bubbly… you name it!

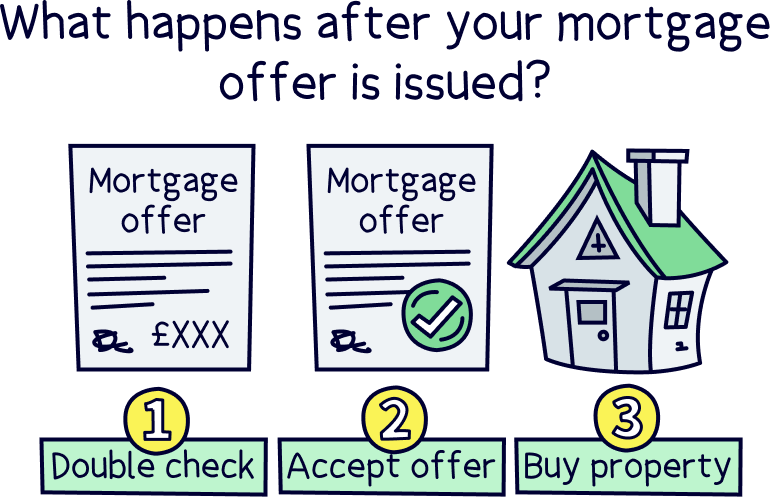

But when you’ve got over the joy of being accepted, that’s when the ball starts rolling. Here’s what needs to happen:

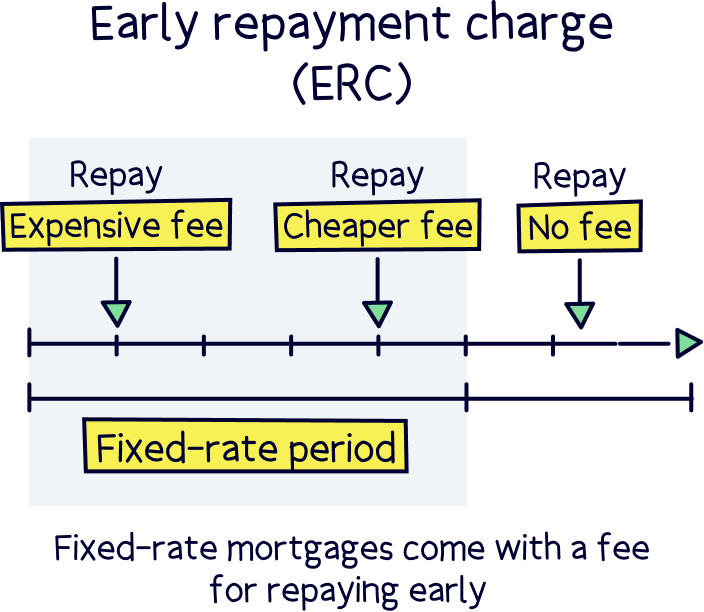

Before you accept the offer, it’s worth having a proper check through it to make sure you’re happy with everything. The offer will lay out how long your mortgage is for (known as the mortgage term), how much you’ll have to pay each month, what the interest rates will be, whether there are any fees for paying it off early (known as an early repayment charge) and more.

Yes, you’ll probably already know all this from your application, but it can’t hurt to check everything through one more time. The last thing you want is to get landed with something you regret later down the line.

Assuming you’re happy with your mortgage offer, it’s time to let your lender know you want to go ahead. Your conveyancing solicitor will tell you exactly what you need to do, but usually, you’ll just need to sign and return the mortgage offer. This is super quick and easy – often, it can simply be done online.

If there are any special conditions attached to the offer, your conveyancing solicitor might also ask you to sign a memorandum of understanding. This is an agreement between you and your lender that will confirm you accept the conditions they’ve laid out.

If you’re not sure whether or not you should accept the conditions, we’d recommend chatting it all through with your solicitor, who’ll be able to advise you on what to do.

Now that you’ve accepted your mortgage offer, your solicitor can finish off sorting out all the legal stuff, known as conveyancing, ready for your house purchase to go through. In England and Wales, this involves putting in a date to exchange contracts, which is what it’s called when you’re legally committed to buying the property. In Scotland, this point in the process is known as a ‘missive.’

Normally, you’ll be able to exchange around 2 months after you handed in your mortgage application, but this all depends on how quickly your solicitor is able to get everything ready. Check out our guide to how long a mortgage application takes to get all the timings. Ultimately, there can be a lot of waiting involved, but it’ll all be worth it once you’ve got a home to call your own!

Completion is when the whole property sale goes through and you officially own your new home! It’s also the day you can get the keys and move in. So, it’s pretty exciting!

Normally, completion takes place around 1 to 3 months after you’ve received your mortgage offer. But this can vary a lot depending on how quickly your solicitor manages to get all the information they need about the property, as well as whether you’re part of a chain (in this case, you’d need to wait until everyone in the chain was ready to complete at the same time).

Our mortgage application process timeline has the full lowdown.

Yes! Until your house purchase goes through, your mortgage offer could technically still be withdrawn if your circumstances change. Basically, your lender has offered you a mortgage based on what they know about you, your income and the property you’re buying. If any of these things vary, this could invalidate the offer.

We know what you’re thinking: how would they know if your situation had changed? Do mortgage lenders do final checks before completion?

Well, it’s pretty rare for a mortgage lender to do any further checks on your finances after sending you a mortgage offer. But you’re legally obliged to tell them if there have been any changes to your income or employment status. And the same goes if the purchase price of the property you’re buying has changed.

To make sure your offer stays valid, you’ll want to sit tight and avoid doing anything unusual. That means holding off changing jobs until after the house purchase has gone through, not taking out any new loans or credit cards and completing as soon as possible so that there’s less chance for anything to go wrong!

That said, if your situation does change, it’s not all doom and gloom. Your mortgage lender might still be happy to go ahead and give you a mortgage, particularly if the change isn’t all that drastic. For instance, you may have a new job, but if your salary’s increased that might be enough to keep you in your lender’s good books. Check out our guide to changing jobs after mortgage approval and getting a mortgage with a new job to find out more.

At the end of the day, all you can do is let them know and keep your fingers crossed.

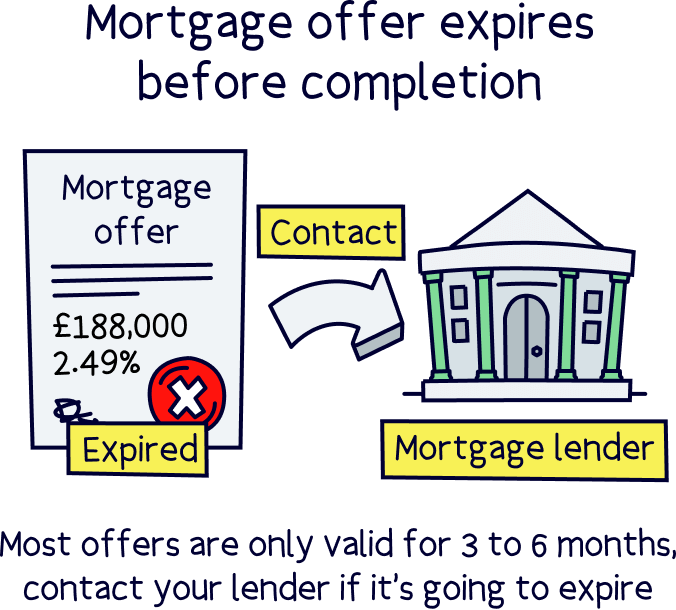

Most mortgage offers are only valid for 3 to 6 months. Although most property purchases should be completed well within this time, there is a chance that your mortgage offer could expire before you manage to actually buy your new home.

This is especially common if you’re buying a new-build property that’s not yet finished. Or if you’re part of a really long chain and you’re waiting for everyone to be ready at the same time.

So, what happens if your mortgage offer expires?

Well, most mortgage lenders are pretty understanding. If your purchase is taking a long time to go through and it’s looking like your offer could expire first, it’s best to just contact your lender to let them know. As long as you give them a few weeks’ notice, they’ll often be happy to extend your offer for you. Phew!

But what if they don’t agree to an extension or your offer’s already run out? Firstly, don’t panic. You’ll just need to reapply for a new mortgage.

If you used a mortgage broker the first time, this will be super easy. They’ll already have all your details saved, so they can just go ahead and resubmit your application without any real input from you. That’s right, you just sit back, relax and let them deal with it all for you.

If you didn't use a broker, we recommend using one now so you can be sure you're getting the best deal.

If you're not sure where to find a great broker, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

As long as your situation hasn’t changed massively, you’re pretty likely to get accepted for a new mortgage. After all, your lender’s already said yes once. Why wouldn’t they again?!

Let’s face it: getting a mortgage offer is a pretty great achievement. In fact, we’d definitely say it’s worthy of a good old pat on the back and a celebratory takeaway.

But even once you’ve received an offer, your home buying journey isn’t quite finished. You’ll still need to check that you’re happy with all the terms, accept the offer and push through with your house purchase. Only then can you truly relax and enjoy yourself in your new home.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.