Article contents

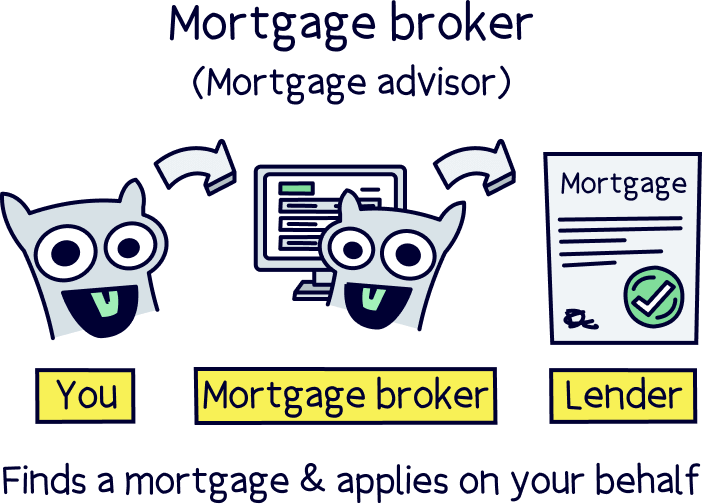

An independent mortgage broker can help you decide whether you should remortgage to fund an extension. They’ll also handle the whole process for you.

Dreaming of a picture-perfect extension? Don’t have cash in the bank? Remortgaging could be the answer. Read on to find out all you need to know about remortgaging for an extension.

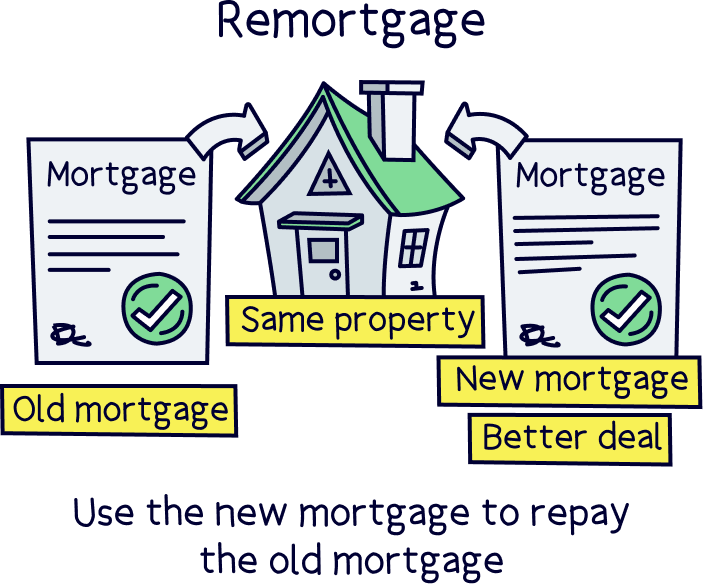

Most homeowners will remortgage at some point or other. After all, taking out a new mortgage can be a great way to get a better deal, reduce your monthly repayments or shorten your mortgage term.

However, did you know that you can also remortgage to release equity?

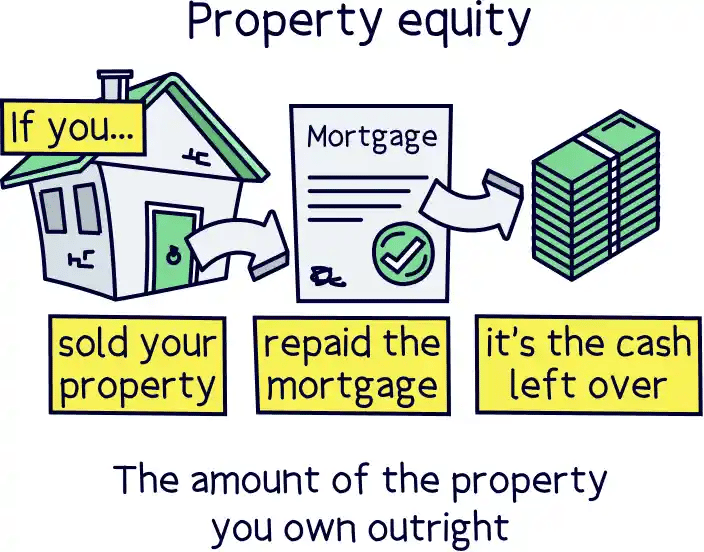

Remortgaging to release equity is when you take out a bigger mortgage, reducing the equity you own (a fancy word that refers to how much of the property you own outright) and therefore unlocking some cash that’s tied up in your property. You can then use this cash for whatever you want – to fund your child’s university education, to fix your broken boiler, to replace your embarrassing car…

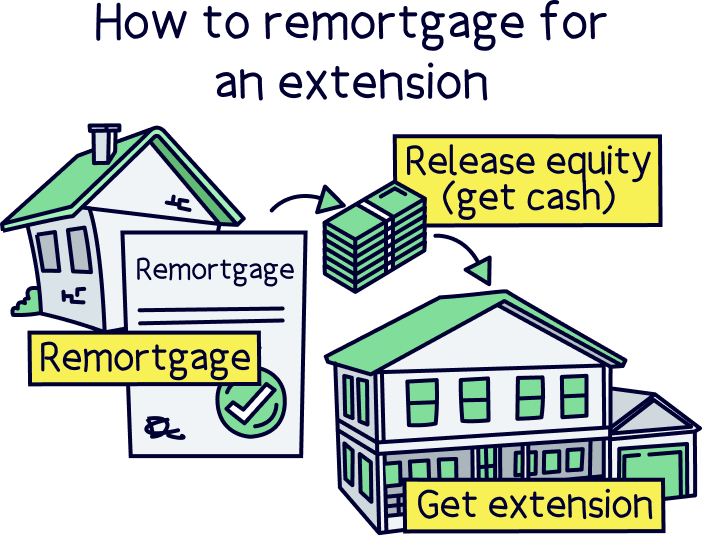

Or, to build that extension!!

Remortgaging to fund an extension can be a really smart move because if you’re careful about it, you could end up with more equity in your house than you started with. We’ll explain it all below.

Tembo will find your best deal, fast, all with award-winning service.

First things first, extensions aren’t cheap. So, if you’re keen to build one, you’ll need a way to fund it. Remortgaging can be a good way to do this as the interest rates on mortgages are lower than they are for credit cards and other kinds of loans (that said, remember that if you’re paying back the loan over a larger period of time, you’ll pay more interest overall).

Secondly, building an extension could add value to your property. Nationwide found that adding a double bedroom and en-suite to your average 3-bedroom house could increase its value by a whopping 23%.

If you increase your house’s value, you ultimately increase the amount of equity you own. And of course, the more of your house you own outright, the more money you get in your pocket when you eventually sell it. According to Zopa, the average amount of profit generated by an extension is £17,000. Not too shabby, eh?

Just beware: you won’t always be able to add value to your home by building an extension. Properties tend to have a ‘ceiling price,’ which means no matter how much work you put into it, it’s unlikely to sell for more than a certain figure. Check out nearby sold prices (using resources like the Land Registry and Rightmove) to see if you’re likely to get back the money you put in.

Before you get too carried away with dreams of open-plan kitchen diners or extra en-suites, stop and think about whether remortgaging for an extension is the right thing to do given your circumstances. Don’t get us wrong, it can be a great way to get that extra space you’re after or even to make some money. But it’s not for everybody!

Here are some questions you should ask yourself before you take the plunge.

In an ideal world, you don’t want to fork out for an extension if you’re not going to at least break even in the long run.

Yes, remortgaging to release equity might make it feel like you’re getting free money, but this isn’t quite true. By increasing the size of your loan, you’ll face higher monthly repayments or a longer mortgage term, ultimately increasing the amount of interest you have to pay overall.

To work out whether remortgaging to fund your extension is a good financial move, there are three things you’ll have to do:

We highly recommend using a mortgage advisor. Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

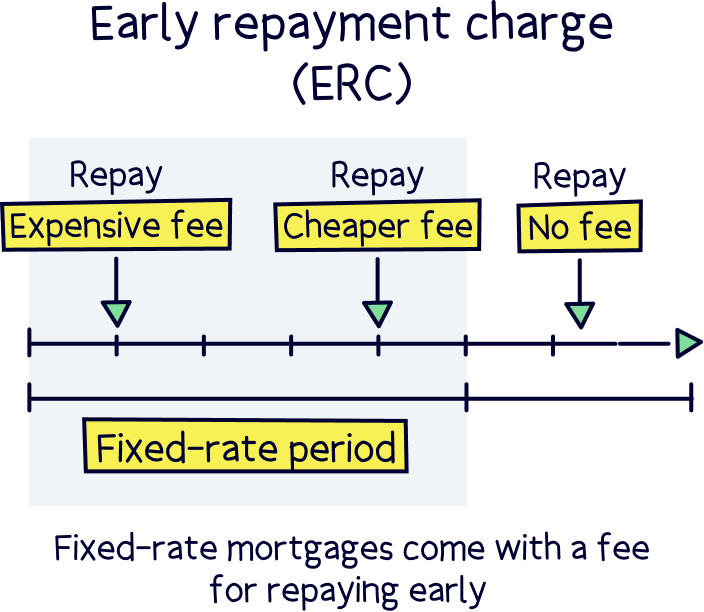

If you’re in the fixed rate period of your mortgage, you could also face an early repayment charge, which could be thousands of pounds. Make sure you bear this in mind, along with any other fees, when you’re crunching the numbers.

If it turns out that building an extension is going to lose you money in the long run, it’s probably not going to be worth it. Of course, if this is your forever home and you’re desperate for the extra space, you might decide to go ahead anyway – and who can blame you?! But this doesn’t make it a sensible financial decision.

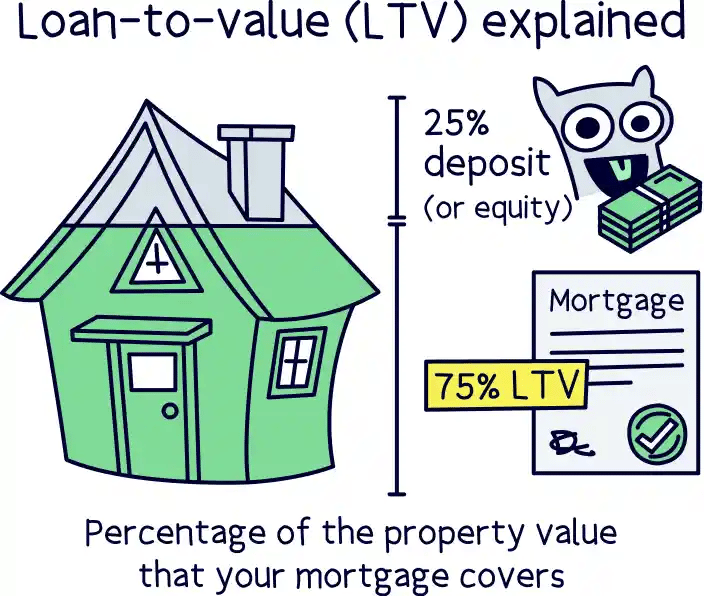

Usually, you’ll want to avoid remortgaging to release equity unless you’ve built up a fair amount of equity in your property. This is because there’s always a possibility that your property could decrease in value. The last thing you want is to end up with a loan that’s higher than the amount of equity you own, known as ‘negative equity.’ This can make it very difficult to sell your home or even remortgage in the future. Gulp.

You’ll also want to avoid falling into a worse loan-to-value bracket. The loan-to-value ratio is the amount of equity you own compared to the amount of money you still owe your lender. Usually, the more equity you own, the better deals you’ll have access to (hence why it’s always a good idea to put a big deposit forward when you’re buying a house). If you drastically reduce the amount of equity you own in your property, however, you could end up on a worse rate than the one you currently have.

To find out how much equity you own, you’ll need to work out how much your property is worth. Then, you can subtract the amount you still owe your lender from your property’s value. Ta-da! That’s how much equity you have to play with.

If you own your house outright, then now’s the time to wallow in your own awesomeness. You’re likely to get access to the very best deals! Check out our guide to remortgaging when you own your house outright to find out more.

Don’t forget that remortgaging to fund an extension essentially means taking out a bigger loan. And of course, you’re going to need to pay this loan back!

This means you’ll face higher monthly repayments or a longer mortgage term, so you’ll be paying more interest overall.

Even if you think you can afford it now, think about how your circumstances could change in the future. What happens if you have kids, for example? Or if you retire? Would you still be able to afford your repayments then?

Your mortgage lender will also have affordability on the brain when they’re deciding whether or not to approve your application to remortgage. If they think you may struggle to pay them back, they’ll most likely reject your application. Sadly, this makes things tricky if you’re approaching retirement, as they’ll want to know you’re going to be earning enough to afford your monthly repayments. Don’t shoot the messenger!

Chances are you’ll need to remortgage before building your extension. Otherwise, how will you fund it? However, if you’re one of those lucky people who has the cash to carry out the work upfront, you’ll have a choice to make: whether to remortgage before or after.

If you remortgage after building the extension, you could get a better deal. This is because your house will (hopefully!) have increased in value, which means you’ll own more equity. And, as we now know, the more equity you own, the better the deals you’ll usually have access to.

That said, remortgaging after the extension is built could be a bit of a risk. What if your house doesn’t increase in value after all? What if your remortgage application gets rejected? This could leave you out of pocket.

If you’re umming and ah-ing about what to do, just get in touch with an independent mortgage broker. They’ll be able to give you an idea of whether your application to remortgage will be approved, so you won’t be making the decision completely blind.

Remortgaging isn’t your only option if you’re looking for a way to fund your extension. Here are a few alternatives you could consider.

Got quotes for your dream extension? Made sure it’s going to add value to your property?

If that’s a ‘yes,’ then all that’s left is to contact an independent mortgage broker. They’ll sit down with you to work out whether or not remortgaging to release equity is a good idea. And if it is, they’ll fill out the whole application for you!

Our recommendations for mortgage brokers is Tembo¹, they've got award-winning service, and will guarantee to get the best deal for you. Plus, get 50% off their fee with Nuts About Money.

All you have to do is crack open the champagne and enjoy your beautiful new extension (after you’ve dealt with the dust and rubble, of course!).

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.