Article contents

Remortgaging with a Help to Buy equity loan can get fairly complicated. But you can remortgage to pay off the loan in full, part of it, or switch to a new mortgage and keep it as it is.

Purchased your lovely new home and got onto the property ladder with a Help to Buy equity loan? Congratulations on becoming a homeowner! Albeit a couple of years ago now, if you're remortgaging.

I'm sure you were fully clued up when buying – there’s loads of information on how to get the equity loan from the government and a mortgage from a lender to buy the property, but when it comes to remortgaging it gets slightly more complicated, and your options are fairly limited.

Let's run through your 3 options to remortgage and what you need to do, and what hoops you need to jump through for each option, it's not as straightforward as it might seem at first.

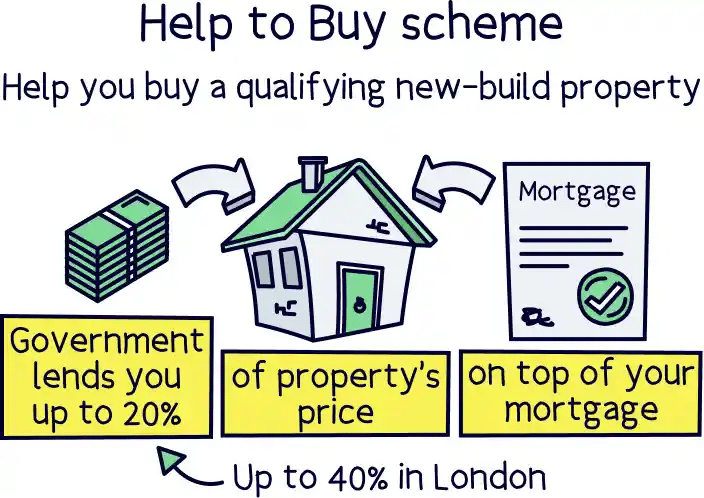

The Help to Buy equity loan scheme is a government scheme providing a loan of 20% of the property price, interest free, so you can buy your new home. As simple as that, it's help to buy. In London you can borrow up to 40%, as house prices as ridiculous compared to the average pay.

It's interest free for the first five years, and after that you'll start paying an interest rate of 1.75%, and in the following years, the interest rate increases to the increase in RPI plus 1% (retail price index - a measure used by the government and economists to work out how much prices of everyday things, such as food shopping has increased each year).

So super confusing, and starting to get expensive at this point, which is why it's often better to remortgage or sell and repay the equity loan after the first five years. Oh and don't forget the very odd £1 per month you have to pay for the duration of the loan.

The scheme has been going a while now, launched in 2013 originally and recently changed to first time buyers only and caps regionally on house prices, with new loan applications ending in 2023. The government still isn't entirely clear if it's actually helped the property market or not, but hey ho, it's helped you purchase a home.

Tembo will find your best deal, fast, all with award-winning service.

Here’s your options when remortgaging with a Help to Buy equity loan:

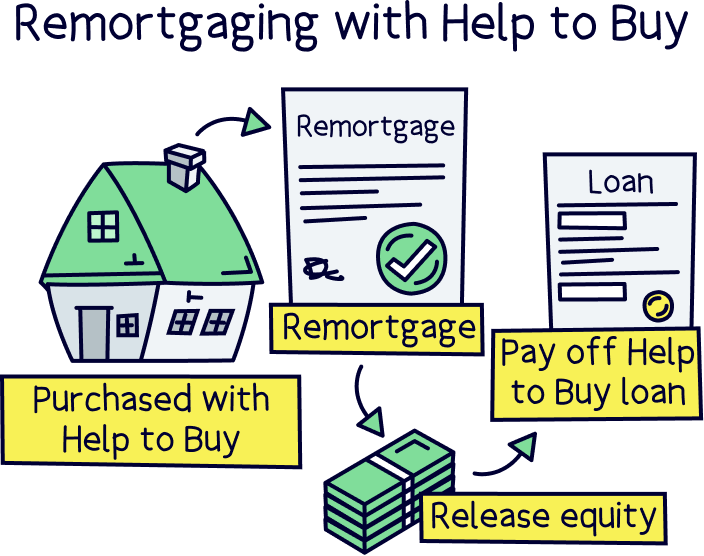

Ready to take full financial responsibility for the full value of your home? Or perhaps heading into the 6th year or your equity loan and due to pay interest. You can remortgage your current mortgage and release equity (a fancy word for cash), which means you can borrow more on your mortgage, well technically get a new mortgage for a higher amount, and using the difference to pay off the Help to Buy equity loan.

It’s fairly easy to do, providing you are able to borrow enough money to cover the full loan amount that you need to pay off the equity loan, so presuming you couldn't borrow the full amount of the property price originally, to now borrow the full amount you would need an increase in your income, such as a salary increase, better job or getting a joint mortgage with a new partner. Or, you might have paid off enough of your mortgage that you can release what you've paid off back in cash, or you might be able to do this if the value of your property has increased.

So here's what you need to repay the help to buy equity loan:

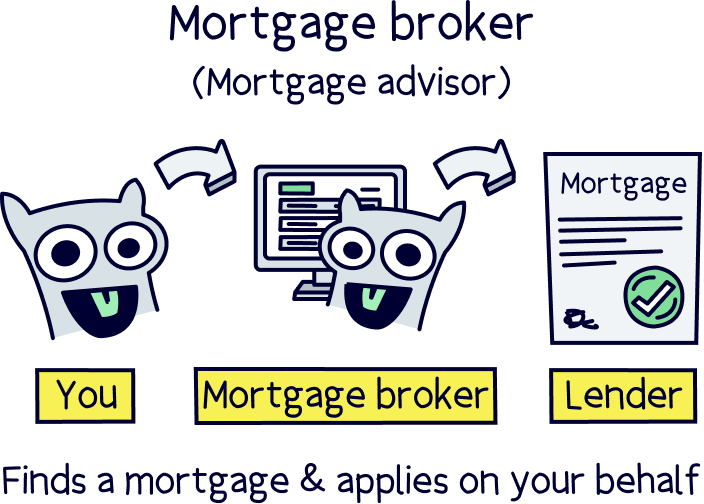

You are effectively getting a new mortgage, so will have to pass new borrowing and affordability checks to make sure you can repay the new loan, but as you’ve already got a mortgage this shouldn’t be a problem unless your circumstances have changed quite a bit, such as a new baby or a new job with a lower salary. A mortgage broker can help with advice if you have.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

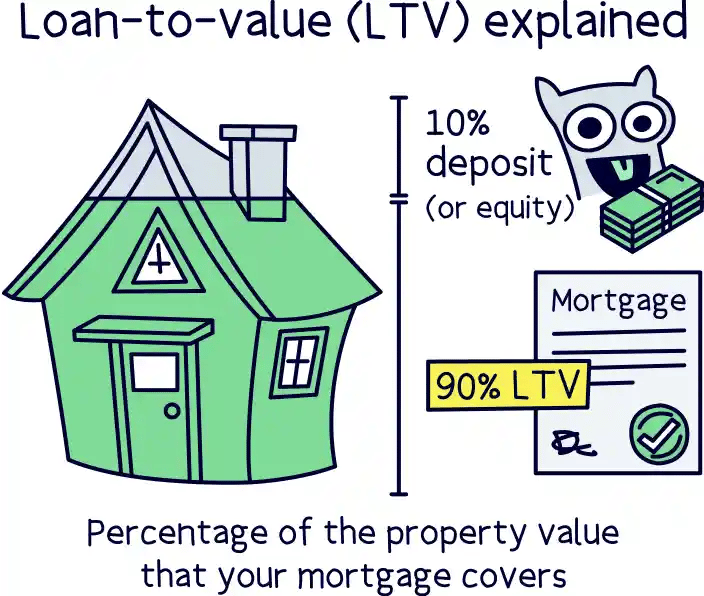

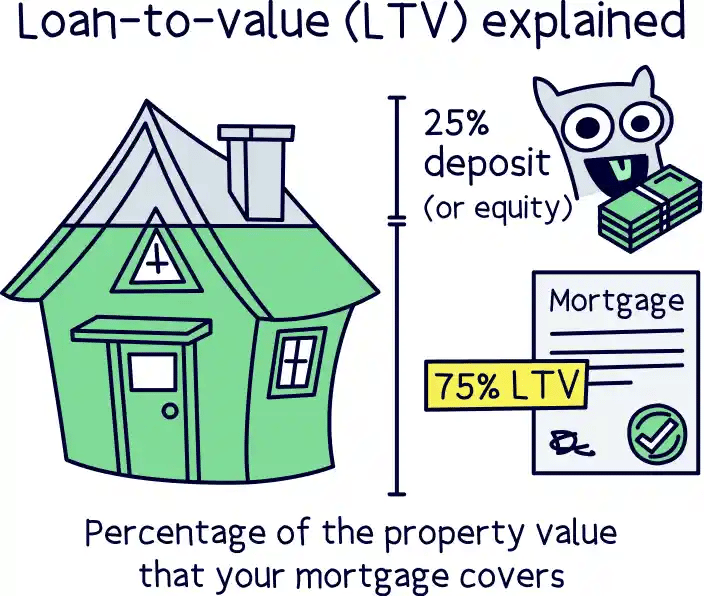

It’s very unlikely you will get a new mortgage at an LTV of 95%, so when doing the maths, set a maximum limit of 90%, so that means your equity (cash) left in the property is at least 10%.

To work out how much to repay of the Help to Buy equity loan, you’ll need to get the property valued by a RICS certified surveyor (Royal Institute of Chartered Surveyors). Remember, you repay the loan based on the value of the property, not how much you borrowed in the first place. So if your house has gone up in value by 20%, then so has the value of your loan, and you’ll be paying 20% more when you pay back the loan, but the good news is that your ‘share’, of the property has also gone up 20%!

Of course it’s property, so fees galore. Homes England will charge you £200 to repay the loan, for ‘admin’. But at least you’ll be free of the loan after this.

And that's it for repaying the loan, and well done, it can be incredibly difficult to own a home without the equity loan, but you’ve achieved it. Good work.

If you're ready to pay it off, speak to a mortgage advisor to find the best new mortgage for you. We recommend you check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. Plus, you'll get 50% off their fee with Nuts About Money.

You can also remortgage to repay part of the equity loan. This can get fairly complicated, and you need to decide if it’s really worth it first. Here’s what you need to know first:

As you are switching your mortgage from your current deal to a new deal with a new lender, you’re actually getting a whole new mortgage, so you need to prove to the new lender that you can afford the monthly repayments and qualify to borrow enough extra to repay part of the help to buy loan.

So this means you cannot borrow more than 75% of the property value as a mortgage, with the remaining as your equity, 25%. (The part not covered by a mortgage). So if you used a 5% deposit originally, and added the 20% Help to Buy equity loan, you are already at 75%, and therefore the only way you can remortgage to pay part of the loan off is if your property has gone up in value.

If you’ve got a 40% equity loan in London, your LTV would have started a lot lower at 55% if you used a 5% cash deposit, so you should be able to 'release equity' and borrow more to pay off part of the loan, if you want to.

This is a requirement by the Help to Buy scheme, that when paying back the loan, it must be at least 10%, but can be anything over this. It doesn’t have to be 10% or 20%, or 30% or 40% for that matter. And don’t forget this is the new market value of the property, not the original loan amount.

In fact it will need to be surveyed by a RICS (Royal Institute of Chartered Surveyors) chartered surveyor. They’ll work out how much the property is worth and therefore the value of the loan repayment.

They’re the people who administer the Help to Buy scheme and you will need to get their permission to do this first. You can find out how to do this on the Homes England website. You’ll also have to pay a £200 admin fee for the privilege.

So quite a lot to consider, and I’m sure your conveyancer or anyone from Home England did not explain any of this to you at the time, but there we go, that's property and 'advice'.

It might not be worth paying off just part of the loan, but it’s worth running the numbers for your own personal circumstances to see.

If you want to keep the equity loan for the time being, perhaps you only got a 2 year fixed rate mortgage initially and still have years left before you start paying interest on the equity loan (5 years interest free), then you can remortgage your existing mortgage, and keep the Help to Buy equity loan ticking over. Sounds straightforward right? But is it? Here's what you need to consider:

That’s checks on whether you can afford the monthly repayments and checks that you can borrow the full mortgage amount (that you got originally) – It’s all standard remortgaging procedure, no different to the mortgage first time round.

However if you have changed your income quite drastically, for instance changed jobs with a lower salary or gone part-time, you might have a few issues. A mortgage broker can help here, but a simple rule to go by is 4.5x your income to work out how much you can borrow.

So that’s the equity loan of 20% and your initial 5% cash deposit, making up the 25% you don’t need a mortgage on, leaving the remaining 75% you’ll need the mortgage on. If you’re in London and have up to 40% equity loan then your LTV will be quite a bit below 75% anyway, normally 55%.

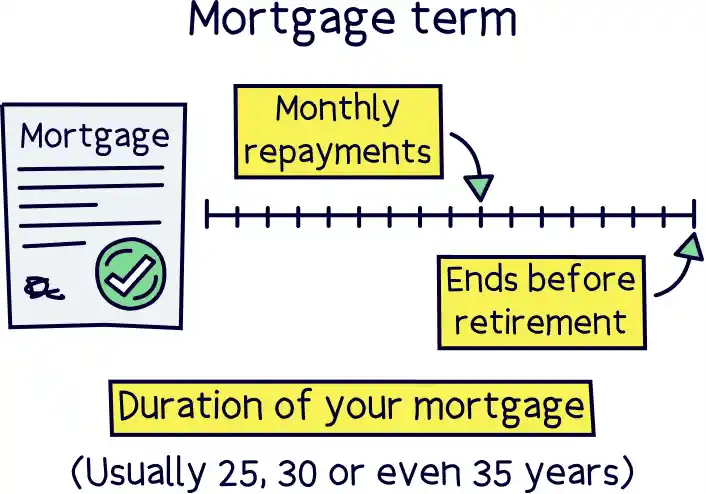

Unfortunately you can't normally extend the mortgage term when remortgaging with Help to Buy.

It must be the same duration or lower, so if you got a 35 year mortgage originally, and it’s now 2 years later, so 33 years left, you cannot remortgage back to 35 years. We're not sure why this is the case, as it's fairly normal when remortgaging to extend your term to reduce your monthly repayments. However do ask, as they may allow it in some circumstances.

And unfortunately you can’t borrow more money if you are keeping the equity loan. However, you might just be able to if you speak to Home England first. (The people running the Help to Buy scheme). Although we couldn't find any reasons for when they would accept increasing the loan amount, but probably because they want to you repay the loan first.

That means asking them for permission to remortgage, this is called a deed of postponement, and for the pleasure you’ll be charged an admin fee of £115. But not only that, to get consent you will need to send in:

So not actually that straightforward to remortgage when keeping the equity loan, but a scheme by the government was never going to be now was it? The good news is that your new lender should manage most of this for you, and be very familiar with what you need to do, and when remortgaging, lenders typically have conveyancers to sort it all out for you, so really you don’t have to do much, just make sure you stay on top of everything.

That’s pretty much all there is to it on the Help to Buy side, but don’t forget about the actual mortgage. Mortgage rates vary across lenders and vary quite considerably! It’s probably best to find your mortgage deal first, and sort the Help to Buy bits after with the help of the lender or broker.

But do keep in mind that you can’t get any old mortgage unfortunately, you have to get one specially for Help to Buy if you are keeping the loan.

If you're remortgaging to pay off the equity loan then the world's your oyster when it comes to choosing a mortgage, and good news you for, these are normally slightly lower rates too.

Also do use a mortgage broker to help you find the best one, they'll also do all the work for you, finding the deal, all the paperwork and speaking to the lender, you can just sit back and relax.

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. And, you'll get 50% off their fee with Nuts About Money.

And if you think your property has gone down in value, which happens to a lot of new builds, your equity loan will have too, so you'll be repaying less if you chose to remortgage to pay it off in full or partly. Something to think about, but definitely don't see it as an investment, do what's best for you.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.