Article contents

By remortgaging your buy-to-let property, you could get a better deal or even release equity to free up funds. Talk to a mortgage broker to compare your options.

Whether you’ve got one buy-to-let property or several, the chances are you’ll want to remortgage at some point or other. Maybe you simply want to get a better deal. Or you might want to release equity (cash) so you can afford to put down a deposit on a new property.

Whatever your circumstances, remortgaging a buy-to-let property is normally pretty easy. Here’s all you need to know about it.

Looking to convert your buy-to-let mortgage to a residential one? You’ll want to head over to our article on converting a residential mortgage to buy-to-let and vice versa instead. Enjoy!

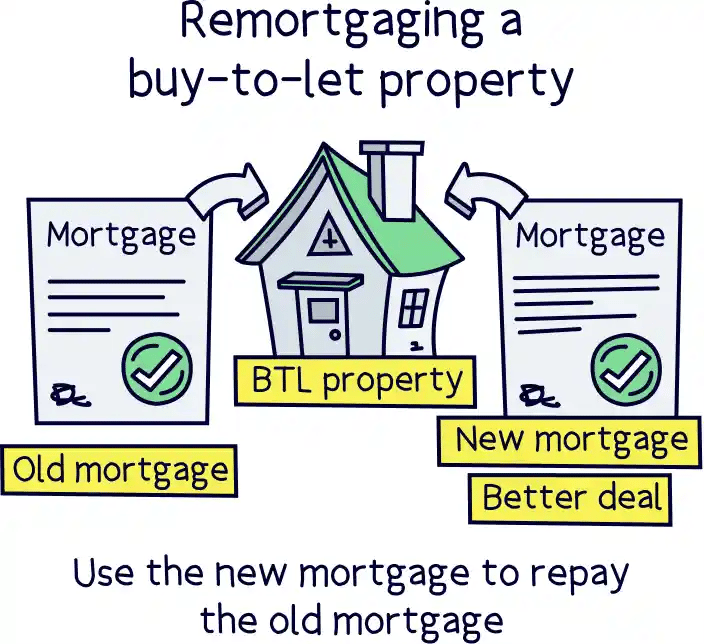

Yes! In case you weren’t sure, remortgaging just means switching your current mortgage to a new one. You can do this with a buy-to-let mortgage just the same as you can with a residential one. The only real difference is that a buy-to-let mortgage lets you rent your property out, whereas a residential mortgage lets you live in it. Simple!

You can remortgage with your current lender (the guys who gave you the mortgage you have currently) or with a new lender altogether. You’ll normally find a cheaper rate if you switch lenders, but we’ll go into that a bit later.

Either way, your lender will want to do some checks before giving you a new mortgage to make sure you’ll be able to afford to pay them back. The good news is that you’ve already been given a mortgage in the past. So, as long as your circumstances haven’t changed massively, there’s no reason why you shouldn’t qualify for a new one now.

Here are a few of the things they’ll want to check:

Nuts About Money tip: check out our buy-to-let mortgage calculator to see how much you can borrow.

Your mortgage lender will want to make sure the rent you’re charging easily covers your monthly mortgage repayments. This is known as ‘stress testing.’ Most lenders will want to see that the rent you’re charging is at least 145% of your mortgage repayments (assuming your buy-to-let mortgage is an interest-only one where you’re only paying back the interest each month. Most people’s are). And they’ll normally select a higher interest rate, around 5-5.5% to test against.

Don’t worry, it’s not as confusing as it all sounds! It just means that if your mortgage repayments are £500 per month, you’ll need to charge your tenants at least £725 per month. The idea is that this way, you’ll be able to afford your monthly repayments and have some money left over in case you end up with gaps between tenancies or you have to fork out for additional costs like property maintenance.

Some mortgage lenders will also check your salary to make sure that, even if you don’t have tenants for a while, you’ll still have enough money coming in to pay them back.

Have you been keeping up with your monthly mortgage repayments? If you decide to remortgage with your current lender, they’ll have firsthand knowledge of your ability to pay them back on time. Fingers crossed you’ve got an excellent track record so they can feel confident things are going to stay that way!

Before approving you for a remortgage, your lender will also want to check your credit score. That’s a score that shows how good you’ve been with money in the past, including whether you’ve paid back other debts like credit cards and student loans consistently. If your credit score is in a good shape, you’ll be in with a better chance of being able to remortgage.

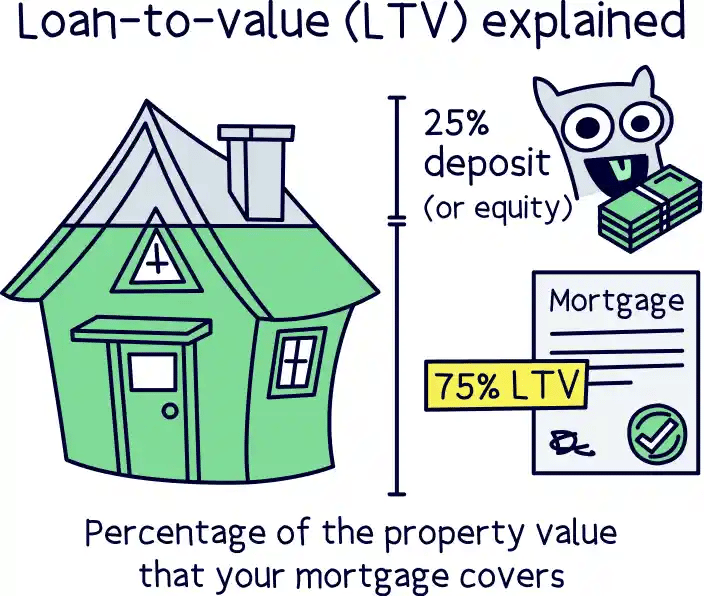

LTV refers to what percentage of the value of your property you owe your lender. Confused?

Let’s say that your property is worth £200,000. Now let’s say that you owe your lender £150,000 (75% of the property’s value). This means you have a 75% LTV. It also means that you own the remaining 25% outright, known as your equity.

The lower your LTV, and the more equity you own, the less risky you are to lenders. This is because if you end up falling behind on your mortgage repayments, your lender will need to sell your property to get their money back. There’s always a chance that your property doesn’t sell for the full asking price, so the less you owe your lender, the more likely they are to get their money back if they end up having to sell it. Make sense?

Tembo will find your best deal, fast, all with award-winning service.

There are lots of reasons why you might want to get a new mortgage on your buy-to-let property. But most are to do with saving money or releasing funds. After all, why would you stay on your current mortgage if it turns out that you can get a better deal elsewhere?

Here are some of the main reasons why it might be time to remortgage.

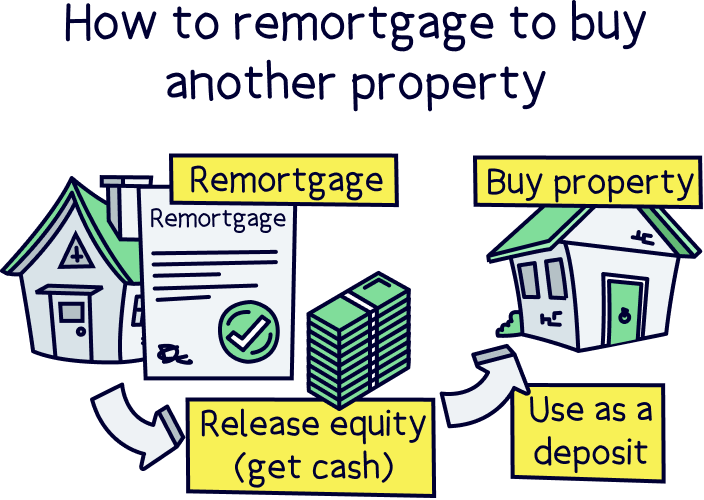

Fancy expanding your property portfolio by investing in another buy-to-let property? Well, what if we told you that you could remortgage as a way to bankroll your next investment? Let’s start at the very beginning.

As time goes on, your property will normally increase in value. This means you’ll own more and more of your property outright, known as building up equity. When you’ve built up enough, you can do something called ‘remortgaging to release equity.’

Essentially, this is where you take out a new, bigger mortgage and get the difference back in cash.

Ultimately, you can use this cash for whatever you want – to buy a car, to go on holiday… you name it! But as a buy-to-let owner, one of the coolest things you can do is use the money to put down a deposit on a new buy-to-let property – expanding your portfolio and bringing in even more rental income. Kerching!

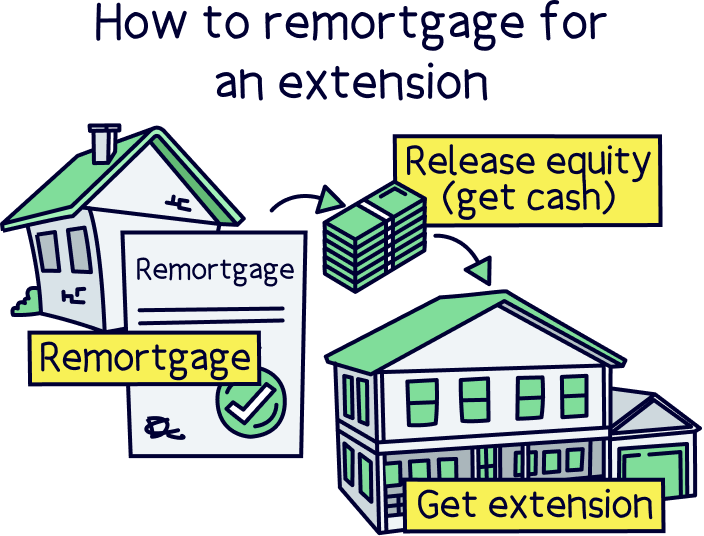

Another good use for the cash could be to do work on your property, like using it to build an extension. This way, you might be able to charge more rent. And you could also find you add more value to your property, increasing your equity in the long run. The options are endless!

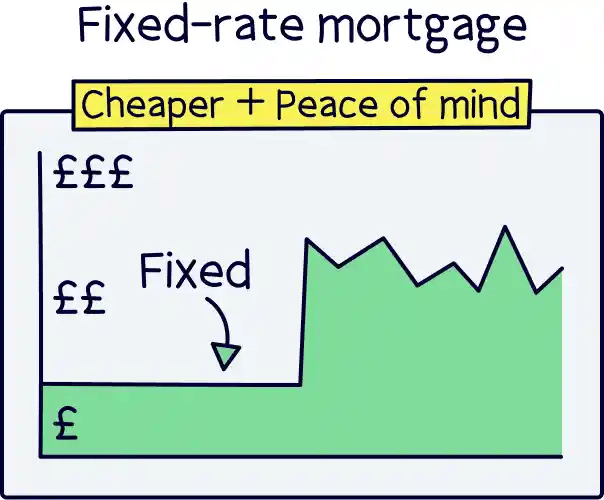

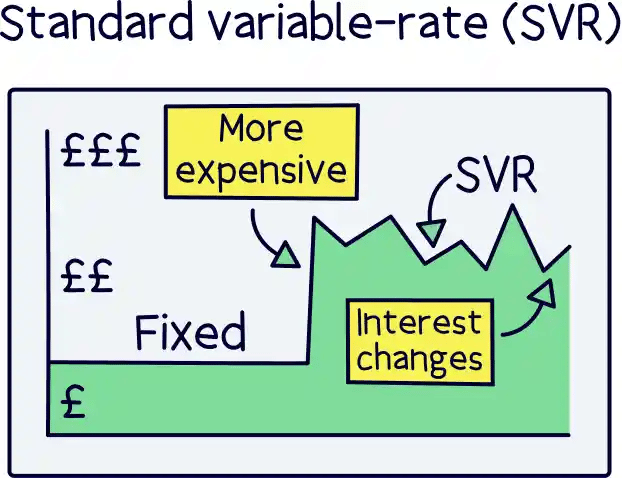

Just like residential mortgages, most buy-to-let mortgages are fixed-rate. That means your interest rates (and therefore your monthly repayments) are fixed at one rate for a certain period of time – usually 2, 5 or 10 years but it can be anything!

But watch out. When your fixed-rate period ends, your lender will automatically put you onto their standard variable rate (SVR) which is normally a lot higher. Worse still, your lender can change your monthly repayments whenever they want without asking you first. Sounds scary, right?!

That’s where remortgaging comes in. To avoid the price increases, you can just take out a new fixed-rate mortgage to benefit from those lower, fixed monthly repayments all over again. Hooray!

Think of it a bit like switching to a new mobile phone contract to get a better deal. Except, in this case, you could be saving thousands of pounds each year! What have you got to lose?!

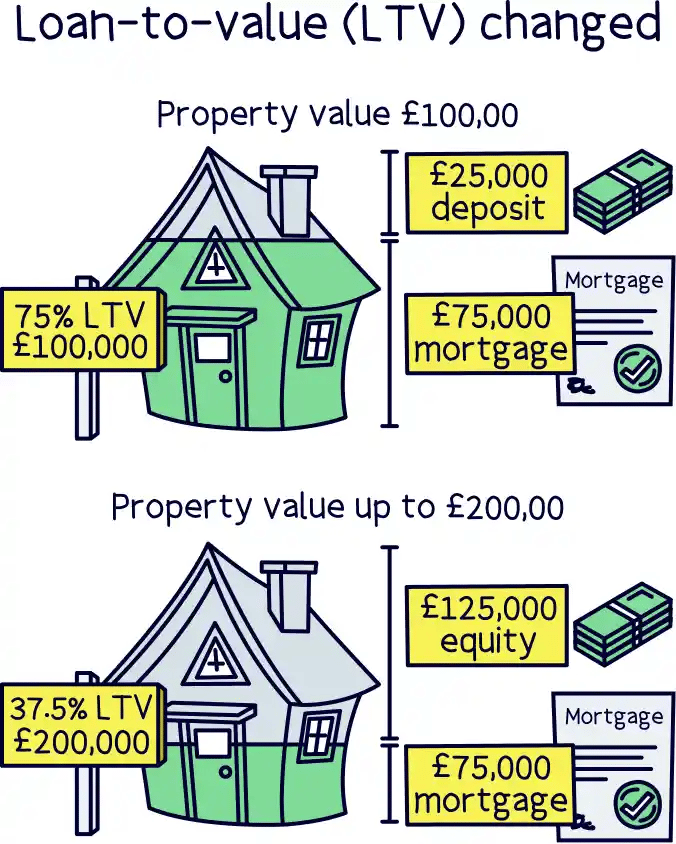

You know how we said that as time goes on, you’ll probably build up more equity in your property? Well, when you build up equity, you’re also reducing your LTV (remember that term we mentioned earlier, which refers to the percentage of your property’s value that you owe your lender?). The lower your LTV, the better deals you’ll be able to access.

Sound like gobbledygook? Let’s look at an example.

Say you bought a flat for £100,000. And say you paid £25,000 as a deposit (25%). You borrowed the remaining £75,000 (75%) from your lender, giving you an LTV of 75%.

Now imagine your flat has gone up in value and is now worth a whopping £200,000. Even though you still owe your lender £75,000, you now own £125,000 in equity. £75,000 is now just 37.5% of your property’s total value, so your LTV has dropped to 37.5%.

Because you’ve made it into a lower LTV bracket, lenders will normally be much happier to lend to you, which means you should be able to access lower interest rates and better terms. You’ll just need to remortgage first!

Just beware because if you’re on a fixed-rate mortgage, you’ll normally face an early repayment charge for leaving early. This could be thousands of pounds. So, make sure to do the maths first. If the early repayment charge just doesn’t make it worth it, it might be best to wait until your fixed-rate period comes to an end before taking the leap.

Are you a portfolio landlord? If so, things will look a little bit different when it comes to remortgaging. According to the Prudential Regulation Authority, a portfolio landlord is anyone who owns more than 3 properties that have buy-to-let mortgages on them.

Basically, if you own 6 buy-to-let properties and only 3 of them are mortgaged, it doesn’t apply to you. But if you own 5 buy-to-let properties and 4 of them are mortgaged, it does apply to you. Get it?

Okay, so now back to remortgaging. When you remortgage a buy-to-let property that’s part of a portfolio, your lender will need to check the rental income of all the properties in that portfolio, not just the one.

Remember the stress test we talked about, where lenders will check you’re charging enough rent to cover more than your monthly repayments? Well, your whole portfolio will need to be tested to make sure that none of your properties are lagging behind.

However, different lenders will interpret the rules in different ways. Most mainstream lenders will need every property in your portfolio to pass the stress test individually, which can be tricky if you have a large portfolio and one of your properties isn’t doing as well as the others. But some specialist lenders will be a bit more flexible and can apply the criteria a bit differently.

Ready to take the plunge? There are two main ways to get started when it comes to remortgaging your buy-to-let property.

So, what do you think? Time to remortgage your buy-to-let property?

Whether you’re hoping to get a better deal or release some equity to expand your property portfolio, remortgaging could be the answer. To get professional advice on what route to take, just get in touch with an independent mortgage broker. Then, crack open the bubbly and prepare to carry on reaping the rewards of your buy-to-let property for many more years to come!

Not sure where to find a good mortgage advisor? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. Get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.