Article contents

Converting your residential mortgage to buy-to-let allows you to generate income by renting out your property. You’ll just need to find a mortgage lender who’s happy to let you make the switch.

Moving out of your home? Fancy earning some extra income by renting it out? Well, you’re in luck! We’ve broken down how to convert your residential mortgage into a buy-to-let one (and how to figure out whether it’s the best option for you).

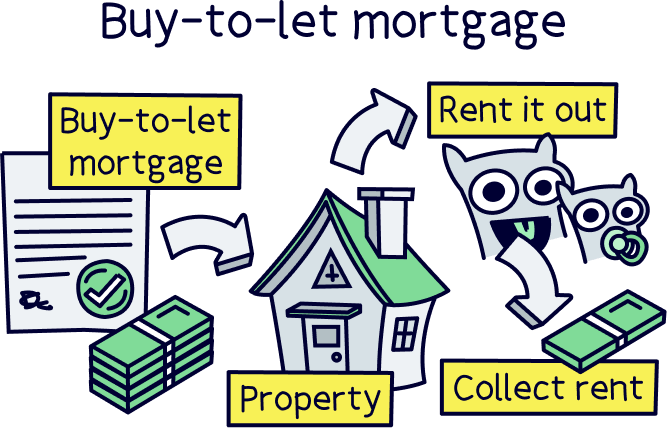

A buy-to-let mortgage is a mortgage designed for people who are buying a property to rent out and make money from, rather than to live in.

Chances are you’re on a residential mortgage right now, which is a mortgage for people who want to live in the home they’re buying. If that’s the case, there’ll be terms in your agreement that state you’re not allowed to rent your home out. If you’ve decided that you want to move out of your home and rent it out instead, that’s where a buy-to-let mortgage comes in.

A buy-to-let mortgage gives you permission to rent your home out (and generate an income from it!) for as long as you want. Kerching!

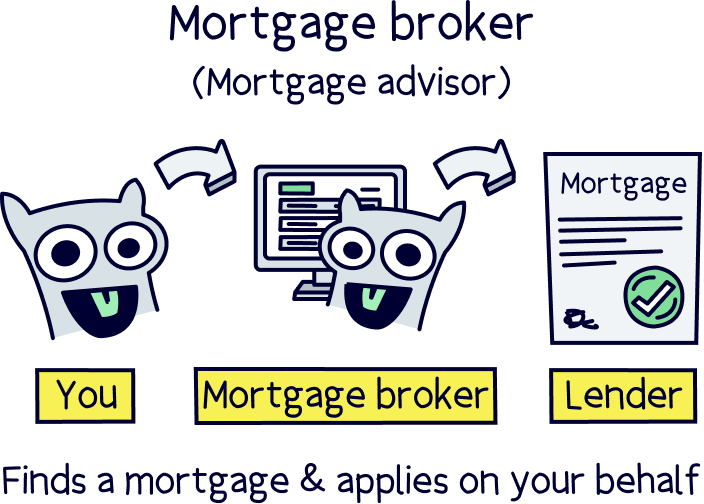

To get a buy-to-let mortgage we recommend you chat to a specialist mortgage advisor. They can give you personal advice, potentially save you thousands in repayments and handle the whole mortgage application.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. You'll also get 50% off their fee with Nuts About Money. How great is that?

Nuts About Money tip: check out our buy-to-let mortgage calculator to see how much you can borrow.

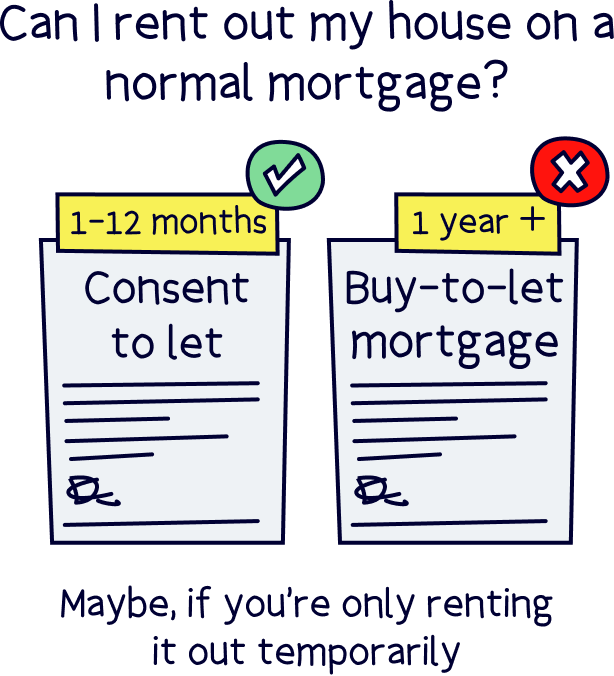

Not exactly. It all depends on why you want to rent your home out, and how long for.

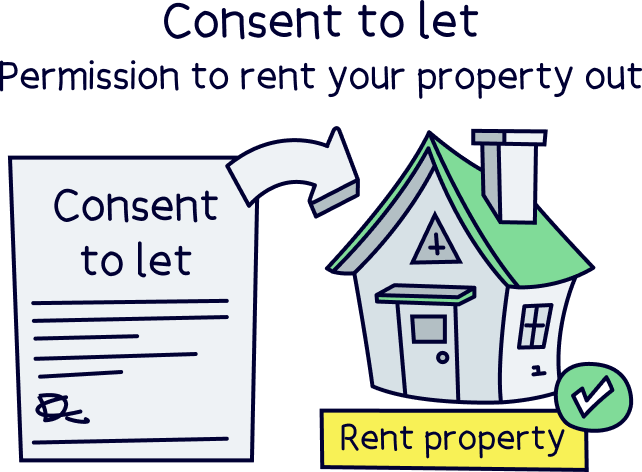

If you only want to rent your home out on a temporary basis, your lender (the guys that gave you your mortgage) might give you ‘consent to let.’ That’s when they let you stay on your current, residential mortgage while you rent your home out for a fixed period of time (normally 12 months or until your fixed-rate mortgage ends).

Consent to let is designed for ‘accidental landlords.’ In other words, it’s for people who need to rent out their home due to a temporary change in circumstances (not people who want to become permanent landlords for the cash).

For example, if you’re moving in with a partner, you might want to rent your home for a while rather than selling it, to give you a chance to test the waters. Or if you’re going away for a few months for work, you might need to rent your home out to cover your mortgage repayments while you’re gone. Check out our piece on whether you can rent your house out on a normal mortgage to find out more.

On the other hand, a buy-to-let mortgage is designed for people who want to rent their properties out long-term. Normally, this means over a year. It basically allows you to buy your property with the purpose of renting it out for as long as you want (is it just us who can see pound signs floating before our eyes right now?!).

Tembo will find your best deal, fast, all with award-winning service.

Buy-to-let mortgages work differently from residential mortgages.

Firstly, they tend to be more expensive. You’ll normally need to put down a bigger deposit, and you’ll also face higher interest rates and fees. But don’t let that put you off!

You should (fingers crossed!) be earning money from your property. So, even though your rates will be higher, you should easily be able to cover them with the rental income that you’re getting in your pocket each month. Phew!

Most buy-to-let mortgages are also interest-only. That means that your monthly repayments will only cover the interest that’s building up on your loan, and not the loan itself. Instead, you’ll have to pay your loan back in one big lump sum at the end of your mortgage term.

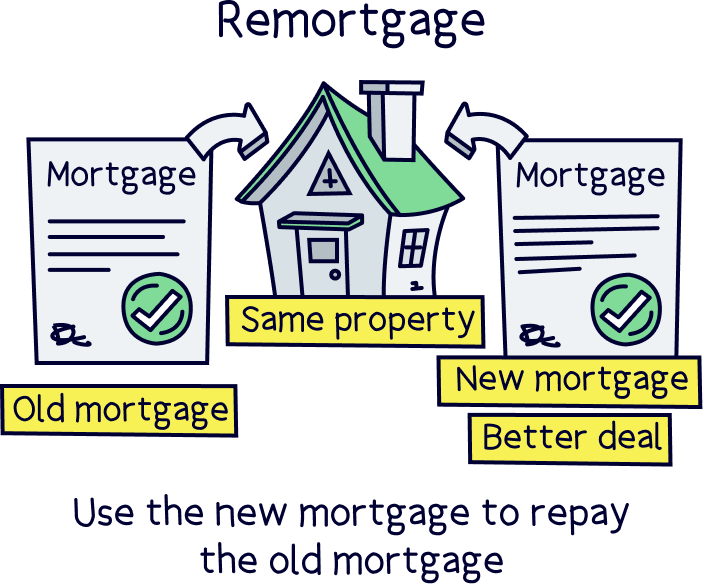

If you’re thinking ‘Eek! That’s a lot of money to fork out in one go!’ then you’re not wrong. But remember, if you’re on a buy-to-let mortgage, the idea is that your property’s an investment, there to make you money. So, most landlords will just keep remortgaging (that’s what it’s called when you switch over to a new mortgage) until they’re ready to sell their property and pay the loan back that way.

Remember, you won’t be living in your property. So, selling it to pay back your mortgage isn’t as scary as it sounds. Ultimately, it won’t make you homeless!

It’s normally a little bit harder to get approved for a buy-to-let mortgage than to get approved for a residential one. Don’t worry, that doesn’t mean you can’t get one! It just means there’ll be a little bit more umming and ahhing from your mortgage lender.

Your lender will look at all the normal things that they consider when they’re wondering whether to approve you for a residential mortgage – like your credit score (a score that shows how good you’ve been with money in the past) and your income.

But they’ll also look at a few more things:

Your lender will want to know how much rent you’re planning on charging before they decide whether to approve you for a buy-to-let mortgage. That’s because as a buy-to-let borrower, you’ll probably be relying on the rent you receive from your tenants to afford your monthly repayments.

To work out whether your rental income will be high enough to cover your mortgage, lenders will carry out something called a ‘stress test.’ To pass, you’ll normally have to make sure the rent you’re charging is at least 145% of your monthly mortgage repayments (assuming you’re on an interest-only mortgage).

Don’t worry, it’s not as complicated as it sounds. It basically means that if your mortgage repayments are £1,000 per month, you’ll need to charge your tenants at least £1,450 per month.

The idea is that this should leave you with enough money to pay your mortgage and other costs associated with being a landlord, as well as enough to spare if your property stands empty for a while. After all, you could end up with gaps between tenancies. Or you might have an empty period while you carry out maintenance work. It’s always best to be safe!

Just remember that every lender is different. Some lenders will only ask you to charge 125% of your monthly mortgage repayments, which used to be the standard. However, because of changes to taxes and regulations, it’s likely they’ll increase it to 145% at some point soon, so it’s best to plan for the worst!

To find the right lender for you, we’d always recommend using an independent mortgage broker (also known as a mortgage advisor). Yes, your current lender might be happy to let you swap to a buy-to-let mortgage, but they won’t necessarily be able to give you the best deal. An independent mortgage broker, on the other hand, will be able to compare mortgages from every lender out there to help you find the best option for you.

Are you planning on buying another house to live in while you rent out your current home? Or are you hoping to move into a rental property yourself? Whatever the answer, it could affect which lenders will be happy to lend to you.

Some lenders won’t give you a buy-to-let mortgage if you’re planning on moving into rented accommodation. The main reason is to do with rental prices.

Basically, the rent you have to pay on the house you’re living in might be higher than your mortgage repayments. So, if your tenant fails to pay their rent one month, you could be in trouble financially. Eek!

Because of this, lots of lenders will refuse to give you a buy-to-let mortgage if you don’t already own at least one other residential property. After all, they want to make sure you pay them their money back, so they won’t want to lend to you if there’s a risk you’ll struggle financially.

Don’t get us wrong, some lenders will be happy to go for it. But you’ll have fewer options available. So, make sure you get a mortgage broker to search for a lender who’ll be right for you.

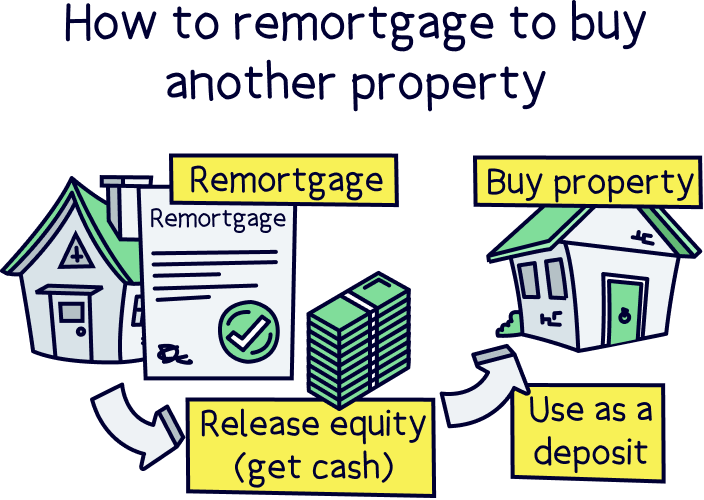

Want to rent out your current home to buy a new one? This is known as ‘let to buy’ and it’s becoming more and more popular.

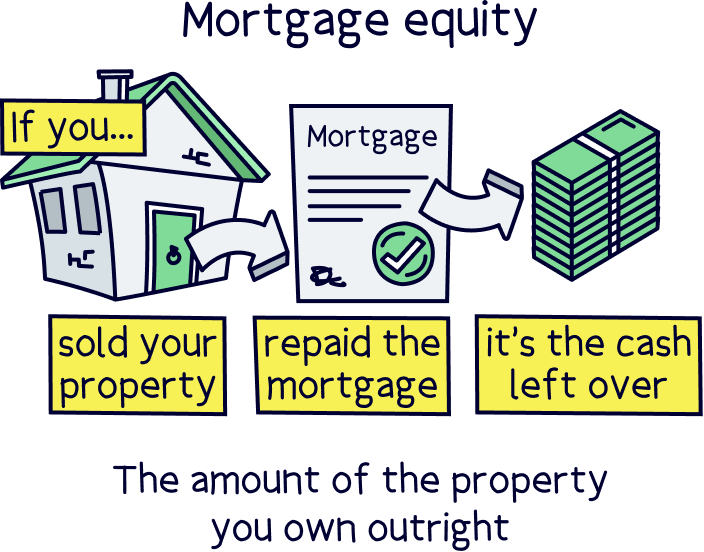

Normally, it will involve remortgaging to release equity (that’s what it’s called when you take out a new, bigger mortgage to get some cash in your pocket). That way, you can hopefully get enough cash together for a deposit on your new pad. Sounds like an amazing plan, right?!

Well, it certainly can be, but some lenders can be a little bit funny about let to buy. Don’t worry, it’s not all lenders. But there are a couple of things that make you a little bit more risky if this is your plan:

Don’t worry, some lenders will be really happy to give you a mortgage for let to buy – like we said, it’s becoming more and more popular. Nationwide and Barclays are just a couple. But you’ll need to find the right lender who’s happy with the risks involved, so get a mortgage broker to compare the options for you.

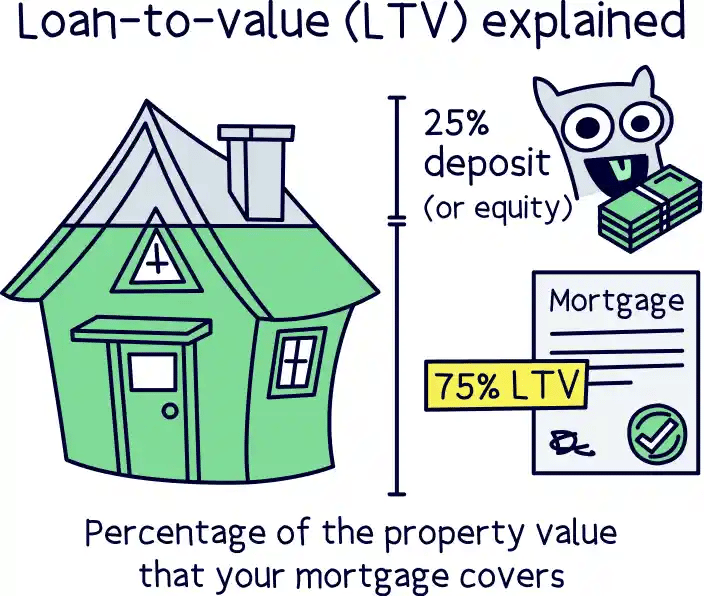

How much money can you put down as a deposit? With buy-to-let mortgages, lenders will want you to put down an even bigger deposit than you’d need to for a residential mortgage. This is partly to balance out all those extra risks we keep going on about.

Most lenders will give buy-to-let borrowers a maximum loan-to-value (LTV) of 75%. If you’re wondering ‘huh?! What on earth does that mean?!’ then don’t worry. LTV is basically just a way of communicating how much money you’re putting up as a deposit versus how much you’re borrowing as a mortgage.

Let’s say you’re buying a property for £200,000. A 75% LTV means you’re borrowing £150,000 (75% of the house’s value) and paying £50,000 upfront (the remaining 25% of the house’s value).

The same applies when you’re converting a residential mortgage to buy-to-let. Basically, your lender will work out the LTV by looking at how much equity you have in your property (in other words, how much of it you own outright) versus how much money you still owe them.

If you own less than 25% of your property outright, don’t panic just yet! It just means you might need to put more cash into your property before your lender lets you convert your mortgage. So, start thinking about where you can get that extra cash!

Changed your mind about your buy-to-let mortgage and fancy moving into your buy-to-let property? Maybe you’ve got a new job and your buy-to-let is closer. Or maybe you think you can get a better rental income by renting out the property you’re currently living in.

Whatever your situation, one thing’s super important: you mustn’t move into your buy-to-let property without first letting your mortgage lender know.

With most buy-to-let mortgages, you’re not allowed to live in the property. If you do, you could be committing mortgage fraud. And if your lender gets wind of it, they could ask you to pay your full mortgage back in one go as a result. Gulp!

Instead, you’ll need to take out a new mortgage. Even if you’re only planning on living in the property for a couple of nights!

The good news is that residential mortgages normally have lower interest rates than buy-to-let mortgages. Happy days! So, if you want to live in your buy-to-let property, you’ll be doing yourself a favour financially (as well as legally!) to swap your mortgage over as soon as possible.

That said, not all mortgage lenders will let you make the swap. First, they’ll normally want to do some checks to make sure you’re going to be able to afford your new monthly repayments. On a buy-to-let mortgage, you’ll have been using your rental income to afford them. But now you’re planning on living in the property, you’ll need to be earning a decent income elsewhere.

Not only that, but some lenders specialise in buy-to-let mortgages and not residential ones. If that sounds like your lender, they might not actually have a residential mortgage to offer you.

Ultimately, if you want to make the switch, you’re best off comparing what all the different lenders can offer to find the right deal for you. So, it’s normally wise to get in touch with an independent mortgage broker, who’ll be able to do this for you.

Does a buy-to-let mortgage sound right up your street? Are you raring to get that rental income rolling in?!

If you’re ready to start making your property work for you, the first step is to talk to a mortgage broker. Not only can they help you decide whether it’s the right move, but they’ll also compare the market to help you find the very best deal. What are you waiting for?!

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage. Get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.