Article contents

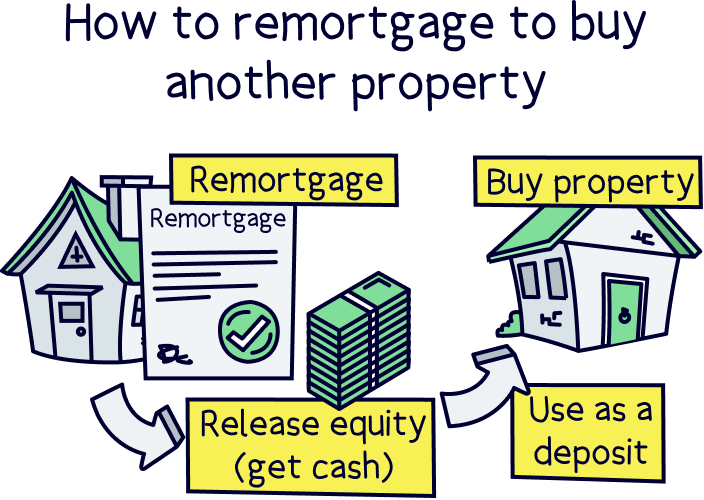

By taking out a new, bigger mortgage on your current home, you could release equity (cash) and fund a deposit on your next property.

Got your heart set on a holiday home? Dreaming of the income you could generate from a buy-to-let property? If a second property is on your wishlist but you don’t have the cash for a deposit, you could release some funds by remortgaging your current home.

Here, we’ll take a look at how it works and whether you should take the leap.

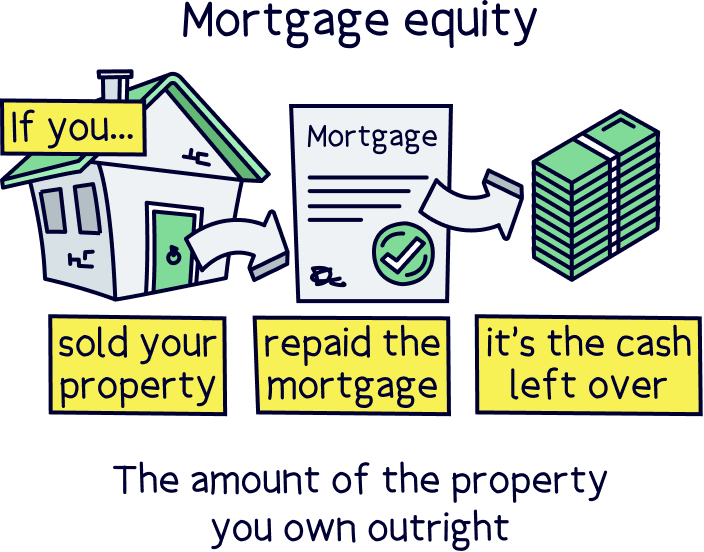

Let’s start at the very beginning. If you’ve owned your home for a while, then chances are it’s increased in value. That means you’ve probably built up a decent amount of equity (equity is how much of your property you own outright).

If you’d prefer to have some of that cash in your pocket rather than tied up in your home, you could do something called ‘remortgaging to release equity.’ This is where you take out a new, bigger mortgage and get the difference back in cash. Kerching!

Technically, you can use the cash for anything – to buy a new car, to fly away on a fancy holiday… the options are endless. When you remortgage your home to buy another property, it just means you’re using the cash to expand your property portfolio. Simple!

There are three main ways of doing this:

Tembo will find your best deal, fast, all with award-winning service.

There are lots of reasons why you might want to remortgage to afford a second property. Maybe you want to make some money by becoming a landlord. Or maybe you want a holiday home to escape to every summer. Here are some common reasons.

Want to make money by becoming a landlord? Investing in a rental property can be a great way of getting some lovely cash flowing into your pocket every month.

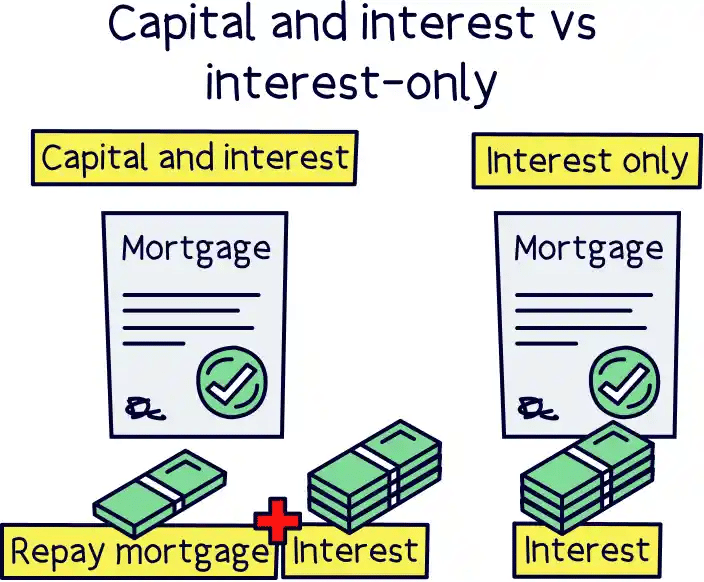

Most buy-to-let mortgages are interest-only, which means you only have to pay back the interest each month, and not the loan itself. So, even though you’ll still have two mortgages to pay, at least your monthly repayments won’t be as high. Better still, you’ll (hopefully!) be able to cover them easily with your rental income. Sounds good, right?!

Want to buy a second home near your work to avoid a lengthy commute? Or looking to splash out on a holiday home to enjoy some downtime with your family?

Remortgaging your current home to buy another one could make your life a whole lot easier (or just a lot more fun!). As if that wasn’t enough, it could also go up in value over time (although there’s no guarantee of that). So, you might even be able to sell it for more than you bought it for.

Do you run a company? Ever considered buying yourself an office or a warehouse? Most mortgage lenders (the people that give out mortgages) will be open to the idea of letting you remortgage your home to buy commercial property for your company.

Hooked on the idea of finally getting the money together to buy that second property? To find out whether it’s something that could work for you, start by asking yourself a few simple questions.

You’ll need to have built up enough equity in your home to be able to at least make a dent in a deposit for a second property. So, how do you work out whether you have enough equity?

Well, first you need to get an idea of how much your property is worth. You can do this by looking at what similar properties have sold for in your area or getting an estate agent to come over and give you an estimate. Then, you just need to subtract the amount you still owe your lender. Ta-da! That’s how much equity you own.

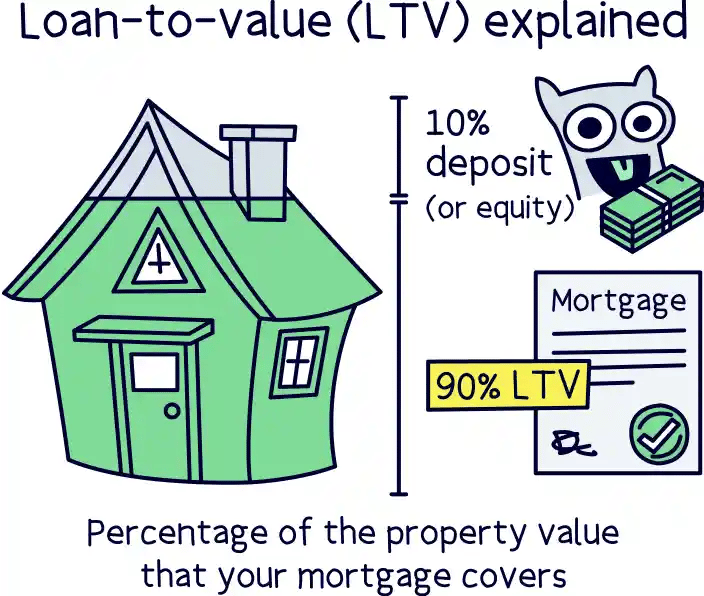

That said, you can’t release all of it. Most lenders will only be willing to lend you up to a certain percentage of your property’s value, known as your loan-to-value (LTV) ratio. Most lenders will offer a maximum LTV of 90%. This means that if your property is worth £200,000, they’ll only be willing to lend you a maximum of £180,000 (90% of your property’s value).

Not only that but ideally, you’ll want to avoid dramatically increasing your LTV – the higher your LTV bracket, the more interest your lender will normally charge you. This is all to do with the fact that a higher LTV means a bigger risk for your lender.

Basically, if you stop paying back your mortgage, your lender will need to sell your property to get their money back. This will often be at a discounted price at auction, so that they can move quickly. If your LTV is high, it’s more than likely they won’t get enough money from the sale to pay themselves back in full.

Think carefully about whether you can afford to buy a second property.

Remortgaging to release equity will involve taking out a new, bigger mortgage on your current home, which will increase your monthly repayments. And if you’re hoping to take out a mortgage on the second property as well, you’ll need to be sure that you can afford to pay back both mortgages at the same time.

This is something your lender will also be thinking about when they’re umming and ahhing about whether to approve you for a new mortgage. They’ll look carefully at your income and expenses to see how much money you’ll have left over.

If you’re planning on buying a rental property using a buy-to-let mortgage, you’ll probably be relying on your rental income to pay your lender back. So, your lender will want to make sure that you’ll be charging enough rent to easily cover your repayments.

To check this, they’ll carry out something called a ‘stress test.’ This is where they check that you’ll be earning at least 145% of your monthly mortgage repayments in rental income, and use a slightly higher interest rate as a base, normally 5-5.5% (all assuming your buy-to-let mortgage is interest-only).

Don’t worry, it’s not as complicated as it sounds! It just means that if your mortgage repayments are £1,000 per month, you’ll need to be charging £1,450 per month in rent. That way, they’ll feel comfortable that you’re going to be able to keep up with the repayments, even if you end up with gaps between tenancies.

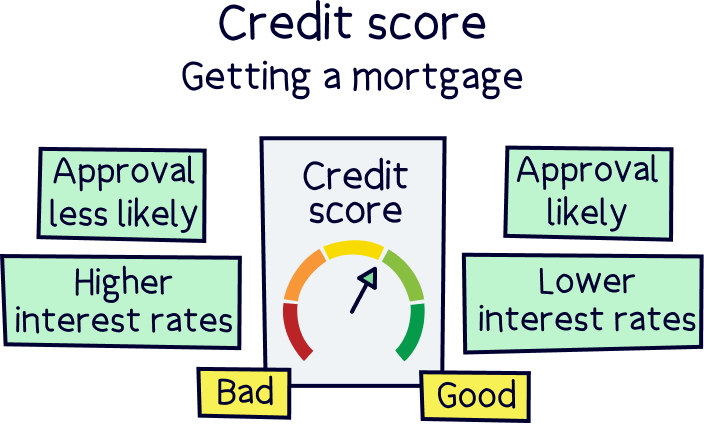

Are you up to date with your mortgage repayments? Have you been paying off your credit cards on time?

Before approving you for a new mortgage, your lender will want to check your credit score. This is a number that shows lenders how good you’ve been with money in the past.

To put it simply, if your credit score isn’t in good shape, most lenders won’t want to lend to you. Sorry! This is especially true given that remortgaging to release equity – and taking out a second mortgage – will put you under more financial strain.

You can view your credit report (the info used to generate your credit score) by heading over to Experian, Equifax or TransUnion’s websites. If your report’s looking a little bit sorry for itself, spend some time improving it before you try to remortgage and buy another property. That means paying off your credit cards, getting yourself up to date with your bills and avoiding taking out new loans for the time being. We hate to break it to you, but that car you were hoping to buy on finance will just have to wait!

So, is remortgaging your home to buy another property actually a good idea? Only you can answer that question! But these pros and cons might help.

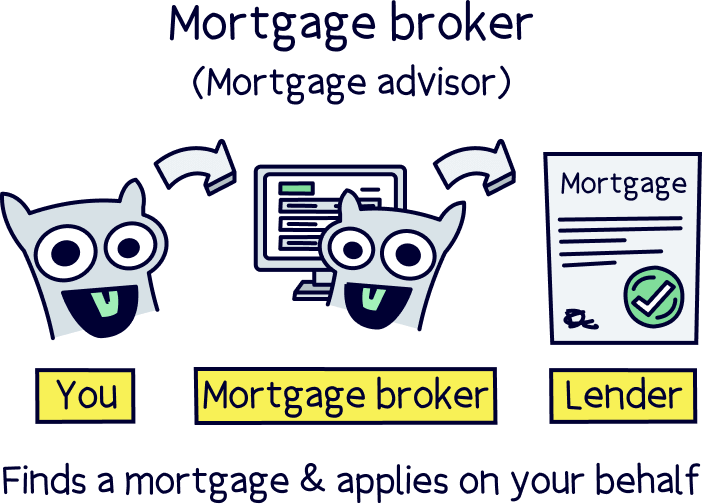

Think you’ve built up enough equity in your home to get yourself a brand new pad?! If so, what are you waiting for? Just get in touch with an independent mortgage broker (also known as a mortgage adviser) to talk through your options and see if buying another property could be a good move for you.

Touch wood, you could be collecting the keys to your second home in no time!

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. Get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.