Article contents

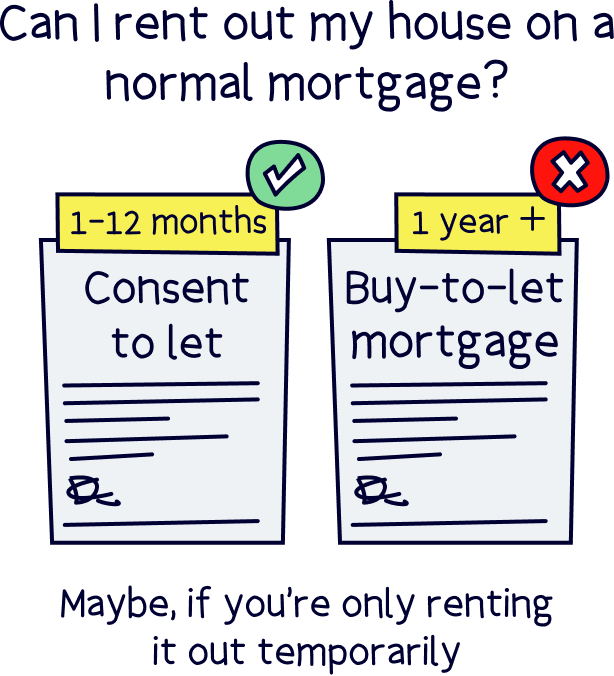

Maybe! If you’re only planning to rent your house out temporarily, your lender might be happy to give you ‘consent to let’ on your current mortgage.

Moving in with a partner and don’t fancy selling up just yet? Going away travelling or relocating for work? Whatever your reasons for moving away, renting your house out could make it easier for you to continue paying your mortgage while you’re gone. But do you need to change your mortgage or can you stay on your current one? Here’s the full lowdown.

Well, that depends on whether you want to rent your house out on a temporary basis or on a permanent one.

If it’s only a temporary thing, your lender (the person who gave you the mortgage) might give you ‘consent to let.’ That’s permission to rent out your home for a given period of time on your current, residential mortgage. Hoorah!

If they don’t give you consent, or you want to rent your home out on a permanent basis, then you won’t be able to stay on your current mortgage. Sorry! Instead, you’ll need to switch over to a buy-to-let mortgage, either with your current lender or a new one.

If you do have to change your mortgage, it’s normally worth getting a mortgage broker to compare the market for you to see where you can get the cheapest deal.

Not sure where to find a broker? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Just beware: if you want to rent your house out, you’ll need to let your lender know first. Unless you get permission, you could be committing mortgage fraud, which is pretty serious. We’ll get to that in a bit!

Tembo will find your best deal, fast, all with award-winning service.

‘Consent to let’ is exactly what it sounds like – permission to rent your house out!

If your lender gives you consent to let, it means they’re happy for you to rent your house out on your current mortgage. But it’ll only last for a set period of time – normally, this will be for a year or until your fixed-rate mortgage comes to an end.

So, who’s it for? Well, it could work for any homeowner who needs to rent their house out short-term.

Imagine you’re moving in with a partner but you want to test the water before you sell up. Consent to let will allow you to rent your house out while you decide whether you want to go ahead and sell it, or whether you’ll be moving back in.

Or say you want to go travelling for a few months. Renting out your home will help you pay your mortgage while you’re gone. And doing so with consent to let will be a lot easier than switching to a buy-to-let mortgage and then back to a residential mortgage again when you get home. Makes sense, right?!

However, it does come at a cost. Even though residential mortgages are typically cheaper than buy-to-let mortgages, most lenders will charge you for consent to let. This might be a fixed fee or you might have to pay higher interest rates. Some lenders will even make you do both!

Plus, you’ll still have to fork out for all the other costs associated with becoming a landlord, such as getting a gas safety certificate, an energy performance certificate, making sure that your building meets fire safety regulations… we could go on!

Ultimately though, the rent you get should (fingers crossed!) cover all these costs and more. So, it can be a great way of generating income. You can even use an agent to manage your property for you if you don’t want to deal with the nitty-gritty yourself. Not bad, eh?

Want to rent out your house temporarily? Here’s what most lenders will look at when they’re umming and ahhing over whether to give you consent to let.

Not sure you’ll meet the criteria for consent to let? Don’t panic just yet. You might still be able to rent out your house – it just means you’ll need to switch to a buy-to-let mortgage. Which brings us onto…

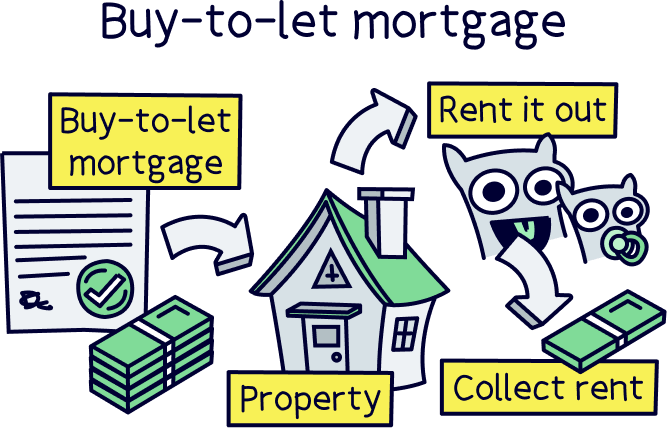

If you’re struggling to get consent to let or you fancy renting out your property for a longer period of time (normally over a year), you’ll need to switch over to a buy-to-let mortgage – in other words, a mortgage specially designed for people who want to earn an income from their property rather than living in it as a home.

The best thing about a buy-to-let mortgage is that it’ll let you rent your house out – and get that all-important rental income flowing in – for as long as you want. Pass the prosecco!

Most of these mortgages are interest-only. That’s where your monthly repayments only cover the interest building up on your loan, and not the loan itself. Then, when your mortgage term comes to an end, you’ll need to pay the full loan back in one big lump sum.

That might sound scary, but remember: your property is an investment and you won’t be living in it! So, lots of landlords will just remortgage and then eventually sell their properties to get the money together.

You should also bear in mind that buy-to-let mortgages are typically more expensive than residential mortgages. You’ll normally have to put down a bigger deposit (we’re talking in the realm of 25% to 40% of your property’s value!) and you’ll have to fork out on higher fees and interest rates as well.

Of course, the idea is that you’ll be earning an income from your property, so this shouldn’t be the end of the world. But don’t forget you’ll still need to pay your mortgage if you don’t have any tenants. So, make sure you can afford the monthly repayments without any rental income if needed.

It’s normally a bit harder to get a buy-to-let mortgage than it is to get a residential one.

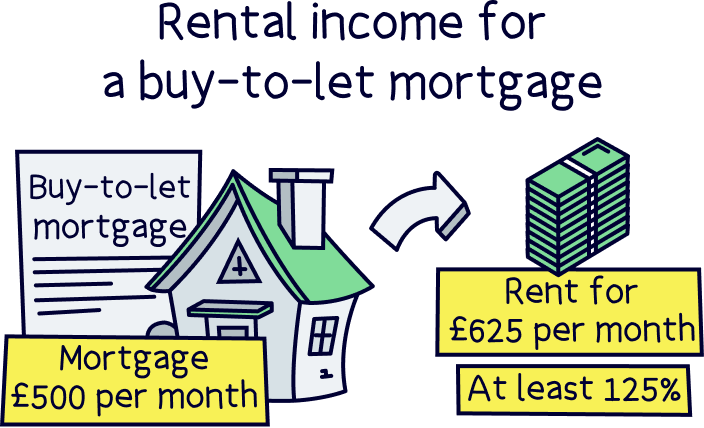

Your lender will do all the normal checks that they would for a residential mortgage, like checking your income and credit score (a score that shows how good you’ve been with money in the past). But they’ll also check how much rent you’re planning on charging.

They’ll normally need your rental income to be at least 125% of your monthly mortgage repayments (assuming it’s an interest-only mortgage). Confused? Don’t worry. Say your monthly repayments are going to be £500 per month. It just means you’d need to charge your tenants at least £625 per month as your lender will want to be sure your rental income will easily cover the repayments.

That said, your lender will also be wondering what’s going to happen if you don’t have any rental income for a while – so, they’ll want to make sure your income is high enough to cover all eventualities!

If you’re looking to switch to a buy-to-let mortgage, we’d recommend using an independent mortgage broker (also known as a mortgage advisor or, in our books, a superhero!). Your current lender might be happy to swap you over, but a mortgage broker will be able to tell you if you could get a better deal elsewhere. Here’s a tip for you: you usually can!

If you're not sure where to find a great broker, here's our top picks:

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Unbiased help you find the right mortgage broker for you from your local area. Their advisors are all rated 5*, fully qualified and search the whole-market (every mortgage deal).

Tembo will find your best deal, fast, all with award-winning service.

Yes!! If you rent out your property without getting permission from your lender first, you’ll be breaching the terms of your mortgage. If your lender finds out, they could demand that you pay your mortgage back in full instantly (and let’s be honest, how many of us could really afford to do that?!). You could also get a black mark on your credit score, which could make it harder for you to get a mortgage (and other kinds of loans) in the future.

We know what you’re thinking: would they ever actually find out though?!

Well, it’s impossible to tell, but lenders have developed some pretty crafty ways of catching unofficial landlords out. For example, if one of your tenants returns a letter in your name that was sent to your property, it could trigger an investigation.

Ultimately, the consequences are just too big to risk it. So, take our advice and make sure you get permission first.

Whether it’s a temporary change in circumstances or you’re planning on earning an income as a landlord from now on, one thing’s certain: you’ll need to tell your mortgage lender!

To get the ball rolling, just get in touch with an independent mortgage advisor. They’ll be able to help you choose between consent to let or a buy-to-let mortgage. And if the answer’s buy-to-let, they can compare the whole market to find the best deal for you. What more could you ask for?!

Remember, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will find you the best deal. Get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.