Article contents

An ISA, or Individual Savings Account, allows you to save or invest up to £20,000 each tax year without paying tax on any interest or profit. It’s a great way to help secure your financial future, whether for a rainy day, a new home, or a comfortable retirement.

Planning to save money for your future? Have you been told to open an ISA? Not entirely sure what that is? Well, you’re in the right place.

Here, we explain everything you need to know about ISAs, from what they are and how they work, to the main features and frequently asked questions.

ISA stands for “Individual Savings Account”, and it allows you to save and invest money in the UK without having to pay tax on any of the money you make.

By saving money in a savings account, you’ll be paid interest for keeping your money there. And when investing your money, it hopefully grows over time as the value of your investments grow. We’ll dive deeper into what these actually mean later, but with an ISA you don’t have to pay tax on the interest you get, or on the growth of your investments at all. It’s quite a big deal!

The Government first introduced ISAs back in 1999 to encourage people to save for the future. We've now got 5 types of ISAs to choose from: Cash ISAs, Stocks & Shares ISAs, Lifetime ISAs, Innovative Finance ISA and a Junior ISAs.

Let’s dig into each type of ISA in a little more detail…

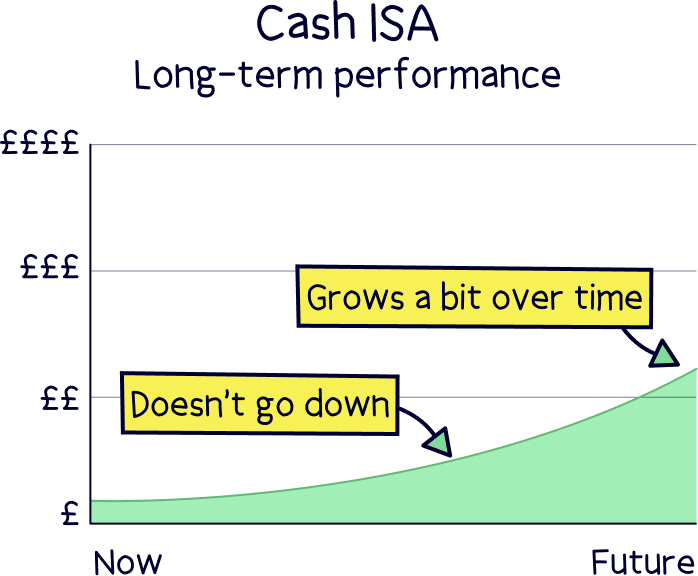

This is the most basic type of ISA. You simply put your cash into your ISA and it earns interest, tax-free. Easy-peasy.

You get Cash ISAs as either a fixed rate (meaning the interest rate stays the same for a certain length of time) or a variable rate (which can go up or down).

A fixed-rate Cash ISA usually gives you a higher interest rate than a variable rate, but you’ll have to lock your money away for between 1 and 5 years, that means you’ll be putting it in your ISA account and can’t take it out for a while. Make sure you really don't need it before this time is up.

Find out how much your Cash ISA could be worth in the future with our Cash ISA calculator.

Want to get a Cash ISA? Here's our Best Cash ISAs.

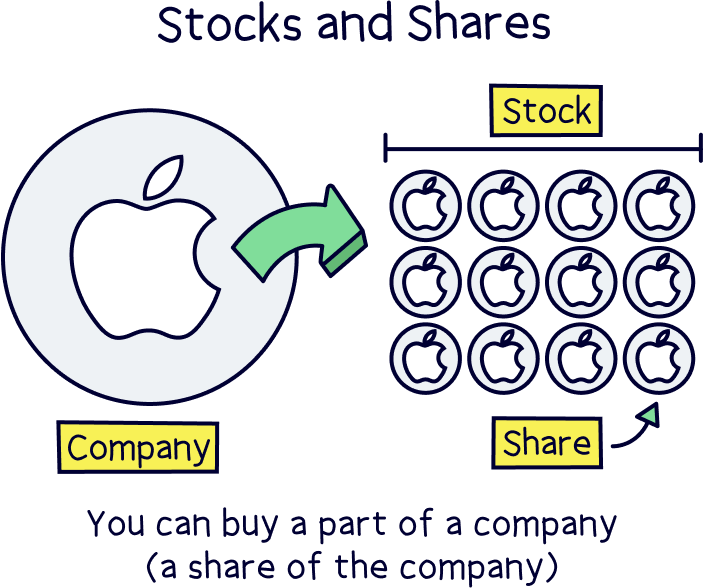

Also known as an ‘Investment ISA’, a Stocks & Shares ISA lets you invest your money instead of saving it. You can invest in various stocks & shares, bonds, or funds to help your savings grow faster.

Stocks and what now?

When you invest in a Stocks & Shares ISA, your ISA provider (the company that looks after your ISA), will work with an investment fund to manage and invest your money sensibly and safely over time.

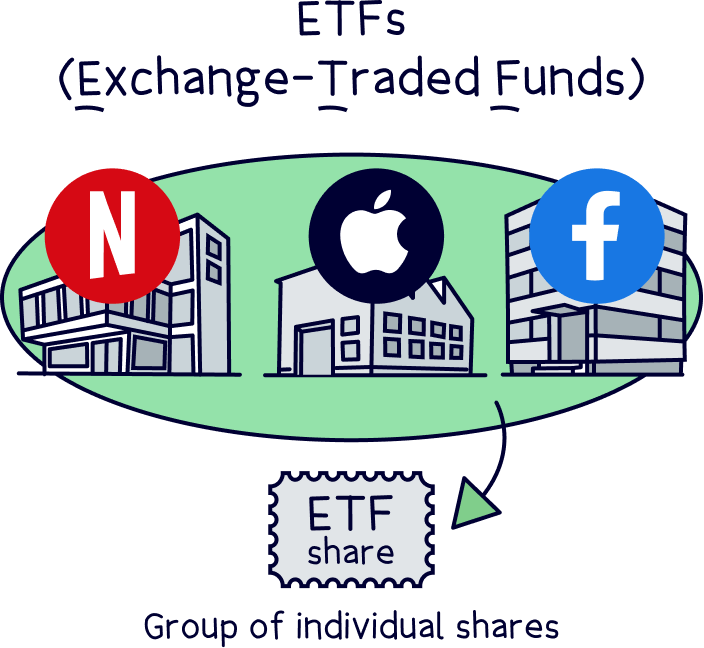

The investment fund will split your money between stocks & shares, bonds, and exchange-traded funds (ETFs) to grow your money. And over time, your savings will hopefully grow, and that money is, you guessed it, entirely tax-free!

As a long-term saving strategy, a Stocks & Shares ISA is a no-brainer. They almost always outperform Cash ISAs. Here’s a more in-depth comparison of Cash ISAs vs Stock and Shares ISAs.

Find out how much your Stocks and Shares ISA could be worth in the future with our Stocks and Shares ISA calculator.

And here's the Best Stocks and Shares ISA for beginners.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

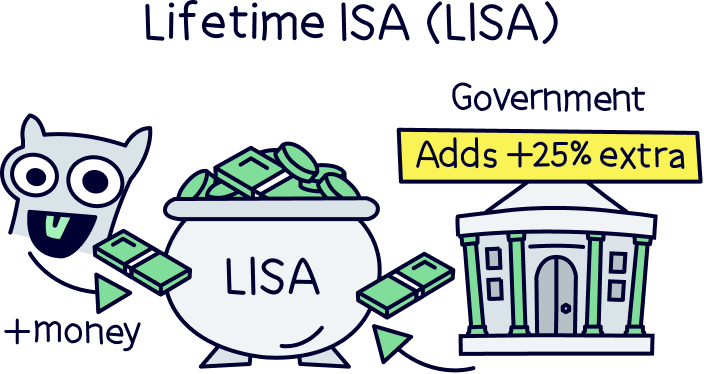

If you’re a young gun, over 18 and under 40 (hey, 40’s the new 30), and you’re eyeing up a first-time property purchase, a Lifetime ISA could be just what you need.

You can save up to £4,000 a year, tax-free, and the Government adds a 25% bonus to anything you pay in until you turn 50. That means if you manage to save the full whack of £4,000 per year, the Government will give you an extra £1,000 per year, for free. Jackpot!

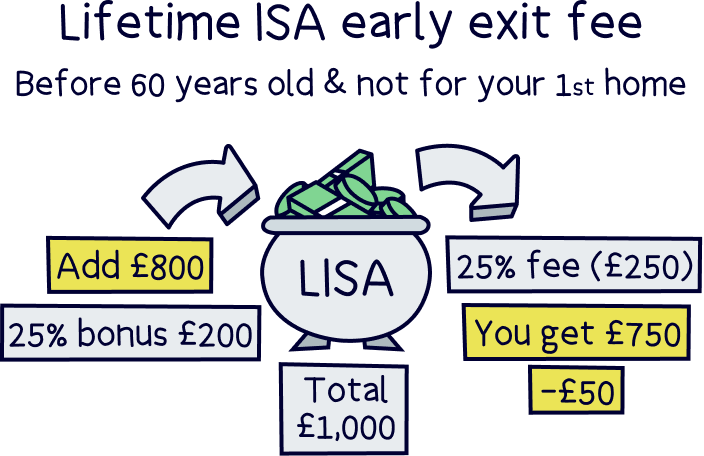

Of course, the Government isn’t handing out cash willy-nilly. There are rules! A Lifetime ISA is designed to help you buy your first home or save for your retirement, so you can only withdraw the money for those reasons.

If you do take the money out for another reason you'll pay a 25% fee. This actually works out to be more than the 25% bonus you get for adding money. Sounds crazy but it's true.

Lifetime ISAs can be either a Stocks and Shares Lifetime ISA, or a Cash Lifetime ISA. Both act just the same as a regular Stocks and Shares ISA or Cash ISA, but you get the 25% Government bonus too!

See how much you could save with our Lifetime ISA tool and compare the top Lifetime ISAs.

If you’ve already bought your first home, or you’ll need the money before you turn 60, there’s no real benefit to opening a Lifetime ISA. You’d be better off saving your money in another type of ISA – our recommendation is a cheap Stocks and Shares ISA.

Instead of saving cash or investing in stocks & shares, an Innovative Finance ISA lets you lend your money to borrowers (individuals or businesses) – called peer-to-peer (P2P) lending.

Peer-to-peer lending is an alternative to borrowing money from a bank, and it’s often used by people looking to grow their businesses.

Over time, the borrowers pay the money back, plus fees and interest. And, like the other ISAs we’ve covered, the interest you earn is completely free from tax!

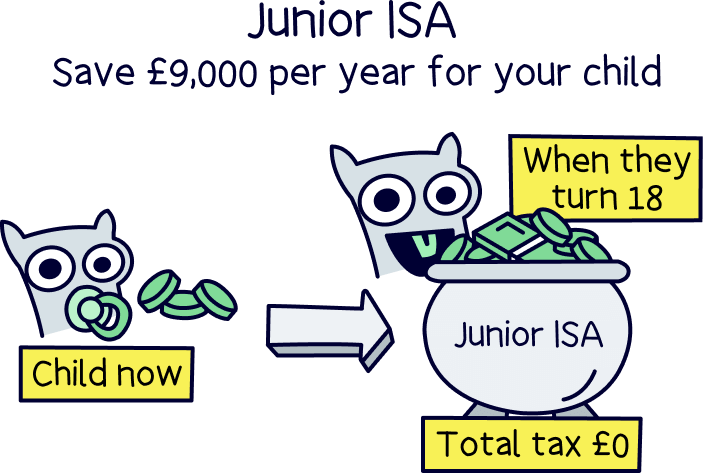

The 4 ISAs listed above are for your own savings. But if you want to open an ISA for your children, younger than 16, you can! A Junior ISA (JISA) lets you, as a parent or guardian, save for your nipper’s future. A JISA locks the cash away until your kid’s 18th birthday, after which it’s their money. Whether you tell them about it or not is up to you!

You can choose to save into a Junior Cash ISA or a Junior Stocks & Shares ISA (or split the money between the two).

Once you’ve opened your ISA, you simply pay money into it throughout the tax year (which runs from 6 April to 5 April the following year). You can make one-off top ups or set up regular top ups to automatically transfer money into your ISA.

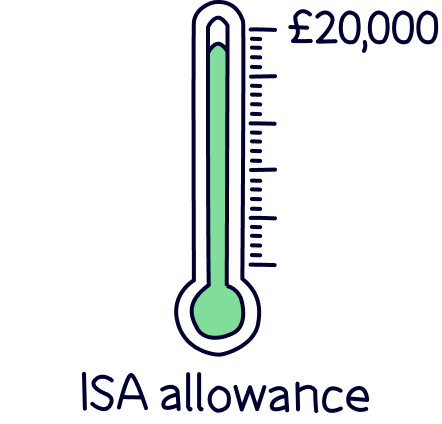

However, if your pockets are overflowing with cash, you should know there’s only so much you can put into your ISA (or ISAs) each tax year.

This is called your annual ISA allowance, and is £20,000 in total.

It’s also important to know that:

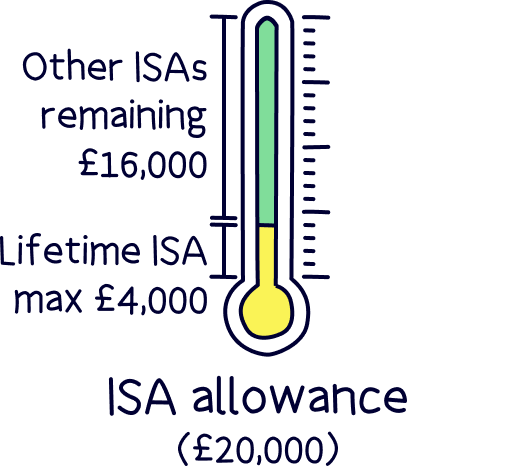

You can can as many ISAs as you like, and open several of the same type each each year too.

The only exception is that you can only save into one Lifetime ISA each tax year.

For instance, you could do this with your whole allowance (although adapt to your own budget):

Yes, ISAs can be a very safe way to save.

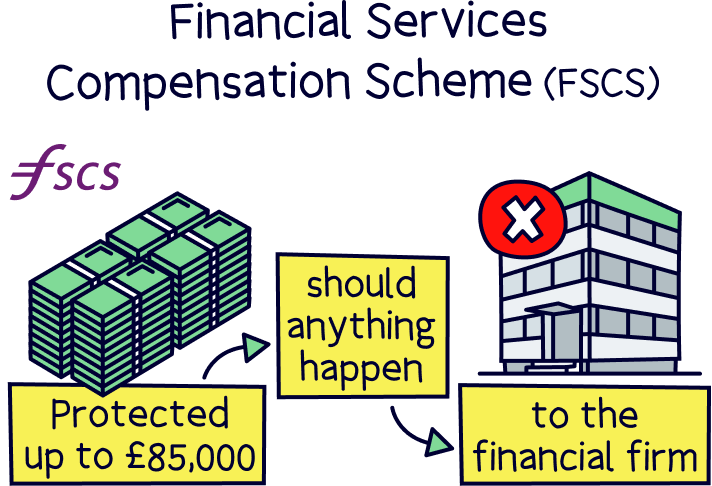

They are covered by something called the Financial Services Compensation Scheme (FSCS). That’s a scheme that guarantees your savings up to £85,000 per ISA provider. So, should anything happen to the company managing your ISA, and they go out of business, your money is still protected and you’ll get it back. If you have more than £85,000, you could spread it across several ISA providers if you wanted to be super safe.

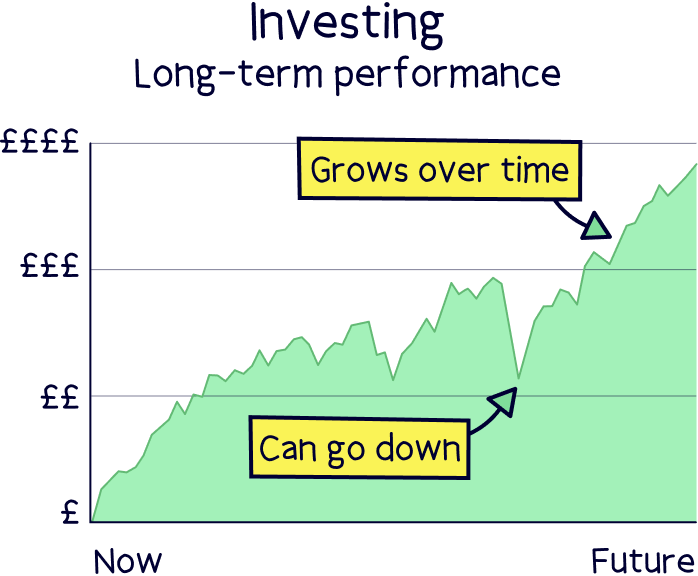

And if you’re worried about Stocks and Shares ISAs – don’t be! If you use an expert managed Stocks and Shares ISA their experts will invest your money sensibly over time (usually over 5 years). You may find your money falls initially, but don’t panic, investing is for the medium-to-long term.

You have to be a UK resident to open an ISA. If you open one in the UK then move abroad, you can’t put any more money in after the tax year that you move. You must also tell your ISA provider as soon as you’re no longer a UK resident.

The only exception is if you’re a Crown employee working overseas (such as a member of the UK armed forces, a civil servant, or a diplomat), or their spouse or civil partner.

But, moving abroad doesn’t mean you need to close your ISA. You can keep it open and enjoy UK tax relief on the money already held in it.

We don’t mean to bring you down, but you know what they say about death and taxes – the only 2 things you can be sure of!

If you die, the value of your ISA can be passed onto your spouse or civil partner — but there are a few rules when it comes to ISA inheritance.

If you have a Stocks & Shares ISA, your ISA provider can be instructed to either:

If you want to learn more, we’ve written an article specifically for what happens to your ISA when you die.

You’ve got some pretty great savings options with an ISA – Cash ISAs, Stocks and Shares ISA, Innovative Finance ISAs, and Lifetime ISAs for yourself. And a Junior ISA for your kids. Oh, and they can be called an ethical ISA too.

If you’re looking to grow your money (a lot), check out expert managed Stocks and Shares ISAs – over the medium-to-long term these are your best option – you’ll be thanking us later!

If you’re looking to save money in the short term, perhaps saving for a new car, or would like to build up an emergency fund, then check out Cash ISAs.

If you’re looking to buy your first home soon, check out a Lifetime ISA, these can be either a Stocks and Shares Lifetime ISA or a Cash Lifetime ISA, and you get a free 25% bonus from the Government to help towards saving for a deposit.

And best of all, everything you make within an ISA is completely tax-free! Why not start saving today?

Find the best place to save with our best investment platforms and our guide to investing for beginners.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.