Article contents

No! You can’t have a joint ISA. However, there is a bright side! If you and your partner each get your own ISA, you may be able to save more money between you.

If you have a partner or spouse, you’re probably used to teaming up together on all things money. You might have a joint bank account or a joint mortgage… it’s only natural that you might want a joint ISA!

However, an ISA is 1 thing that you can’t do with your partner. Sorry! Instead, an ISA can only be in 1 person’s name. Here’s everything you need to know about ISAs if you’re in a couple.

First things first, an ISA is a pretty awesome savings account designed to help you save and grow your money tax-free. Kerching!

There are a few different types of ISAs that work in slightly different ways.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

No, you can’t have a joint ISA. Sorry! You can’t share an ISA and you can’t open up an ISA in someone else’s name either (unless you’re opening a Junior ISA for a child, of course!).

You also can’t share or transfer your ISA allowance to someone else. Let us explain.

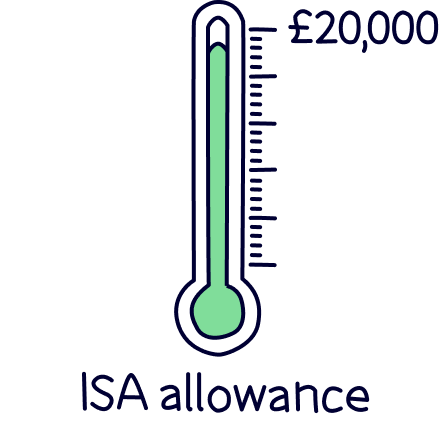

In the UK, you’re only allowed to put a certain amount of money into your ISA each year, known as your allowance. This is how the government controls how much tax-free growth your money can make. Exactly how big the allowance is can change from year to year, but at the moment it’s £20,000 (or £9,000 for junior ISAs).

This allowance isn’t transferable, which means you can’t give it to someone else. The only exception is if you die, in which case your partner gets an extra allowance that will allow them to inherit your ISA. But hopefully, you’ll be kicking around for a long time yet!

Anyway, it’s not all doom and gloom...

Not being able to have a joint ISA isn’t necessarily a bad thing if you’re in a couple. By each putting money into your own ISA, you could both make money from your savings and then, if you choose to, share the profits.

Here are the main benefits of putting your pennies to work in separate ISAs.

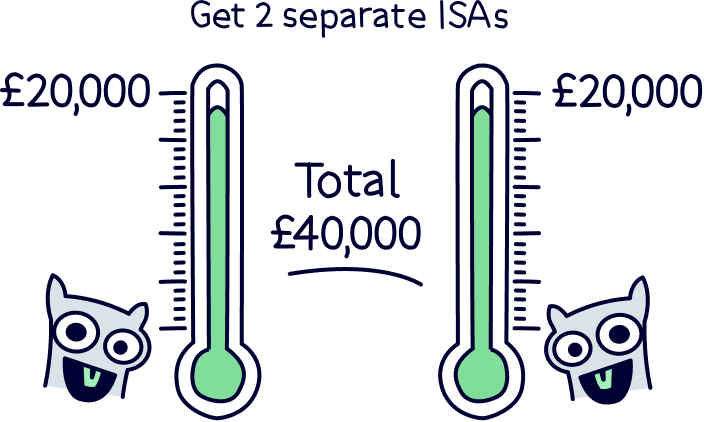

This one’s pretty obvious but it’s worth saying anyway. If only 1 of you gets an ISA, that means you’ll be limited to just investing £20,000 into an ISA each year (remember that ‘allowance’ we were telling you about earlier?).

However, if you each get your own ISA, that means you’ll have a £20,000 allowance each – £40,000 between you. The more cash you put into ISAs, the more cash your savings are likely to generate. So, by getting an ISA each, you could invest more money between you and end up with more profit to share.

Remember, you can’t technically share or combine your allowances. But if you share finances, the chances are you’ll end up sharing any cash your ISAs make!

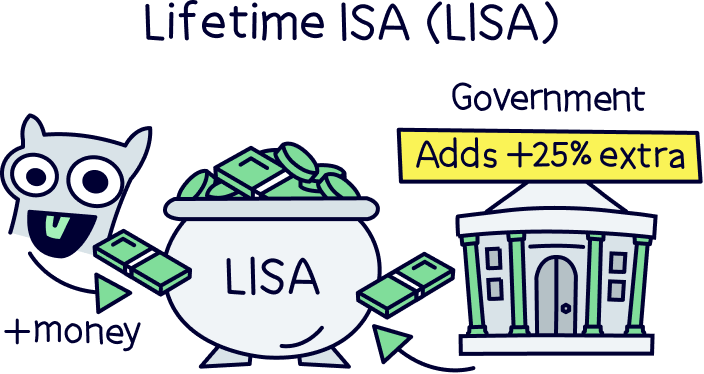

If you’re hoping to buy a house with someone else, you might think it’s a shame you can’t get a joint Lifetime ISA. Remember, with a Lifetime ISA, the government will give you a bonus of 25% of any savings you put in there (you can pay in up to £4,000 per year) to help you buy your first home.

However, getting one each is much better. Why? Well, it means you can each put up to £4,000 into your ISA every year, and you can both get a 25% bonus from the government on that money.

When you’re ready to buy a home, you can then use both of your lifetime ISAs, potentially boosting your deposit by double what you could alone. Woohoo!

If you're interested in getting a Lifetime ISA, check out our top lifetime ISA providers.

Okay, so the government rules are a bit confusing when they talk about whether you can pay into someone else’s ISA. They say:

‘Cash subscriptions from third parties can be accepted without question unless the ISA manager holds information that shows that the cash does not belong to the investor.’

In other words, you can pay into someone else’s ISA, but the money has to be theirs. Huh?!

Well, we don’t blame you if you’re a bit confused. The government’s advice is confusing! But most ISA providers take it to mean that you can pay into someone else’s ISA as long as the money is a gift. That means you can’t ask for it back and you don’t get to keep any returns it makes!

Exactly what you’ll need to do will vary from provider to provider, but if you’re hoping to contribute to someone else’s ISA, you’ll normally need to give some details, like your name, date of birth and address. You may also need to send in a signed letter confirming that you’re giving the money as a gift and that you’ll no longer have any claim to it.

Before you go ahead and pay into someone else’s ISA, however, it’s best to check what their ISA provider says and whether they have any specific criteria.

Otherwise, you could just keep things simple and transfer the money to your friend or family member as a gift. They can then do what they want with it, such as paying it into their ISA themselves. Easy!

As you now know, you can’t get a joint ISA as ISAs can only be in 1 person’s name. Sorry to be the bearer of bad news!

However, if you’re in a couple, all is not lost! Getting an ISA (or multiple ISAs!) each is a great shout as even though you can’t share your ISA, you can share any returns your ISAs make for you.

If you or your partner don’t yet have an ISA, check out the best investment platforms to find the best one for you.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.