Article contents

To get a mortgage, you’ll need to save money for a deposit, a Lifetime ISA can help (get a free 25% bonus from the government). Next, find your dream property and then apply for a mortgage. It's a great idea to use a mortgage broker who can search every UK mortgage and find the right mortgage for you, they'll even apply on your behalf. The right mortgage broker is worth their weight in gold.

Tired of living with your parents or in rental accommodation? Desperate to finally be able to hang your own pictures on the wall?

You might think that you’ll never get your foot on the property ladder, but you could be a lot closer than you think. Here, we’ll look at how to get a mortgage for your first home so that you can finally walk through a front door you can call your own! (And how to get the best mortgage deal.)

Just want a mortgage? Check out our mortgage comparison table.

Tembo will find your best deal, fast, all with award-winning service.

First things first, you’ll want to know if you can actually get a mortgage. So, can you??

Well, every lender’s criteria is different (lenders are the people that give out mortgages). So, it’s impossible to say for sure. However, all lenders will take into account things like:

Don’t worry, you don’t have to nail every single one of these factors to get a mortgage. Instead, lenders will be looking at how all of these elements balance together before making a decision.

Plus, because different lenders (mortgage companies) will be looking for different things, it’s all about finding the best lender for you. After all, there are more than 100 in the UK so the chances are that at least one of them will consider you!

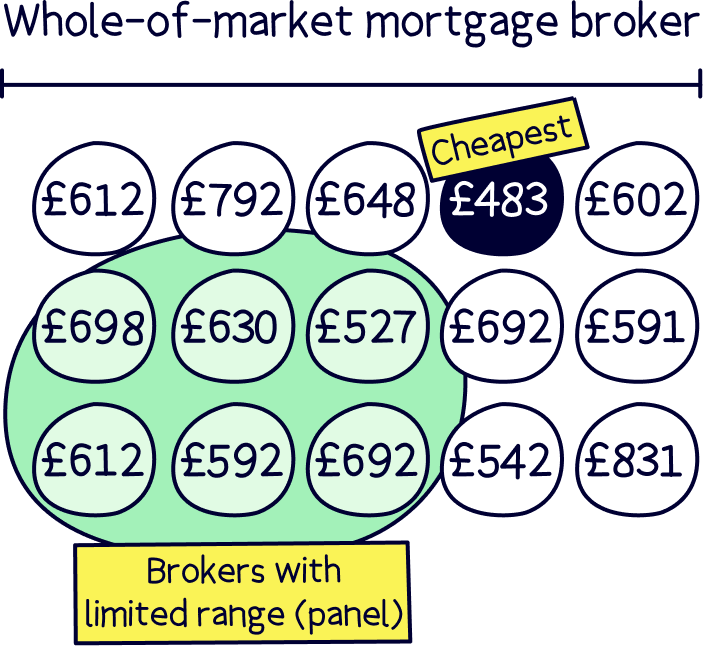

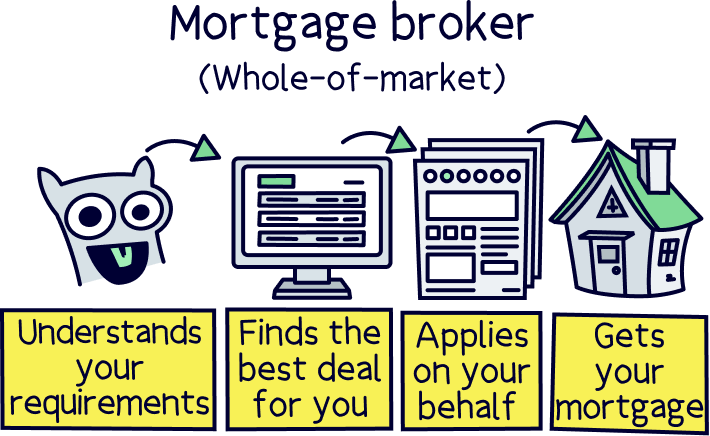

To find out exactly where you stand, it’s best to get a whole-of-market mortgage broker involved. A whole-of-market broker (also known as a whole-of-market mortgage advisor) will be able to compare all the mortgage deals available from all the lenders out there (or at least, almost all of them).

At the same time, they’ll get to know your circumstances properly so that they can give you a much clearer idea about whether you’ll be able to get a mortgage and, if so, who would be the best lender for you. They’ll also sort out the whole mortgage application for you, but we’ll get to that a bit later!

We highly recommend using a mortgage advisor. If you're not sure where to find one, check out our top mortgage brokers.

Right, now that’s out of the way, let’s look at what you need to do to get that mortgage. It’s not as complicated as you might think!

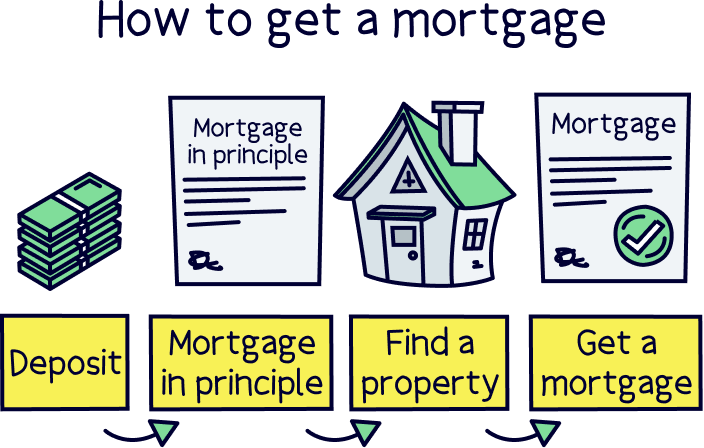

Here’s how to get a mortgage in 5 simple steps.

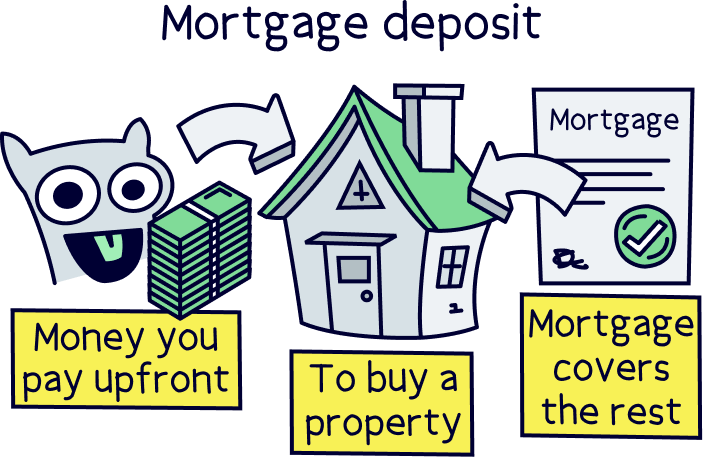

Okay, okay, so this can be easier said than done. But the first step towards getting a mortgage is to start saving.

Sadly, 100% mortgages (mortgages where you don’t need a deposit) aren’t really a thing anymore. So how much do you need to save?

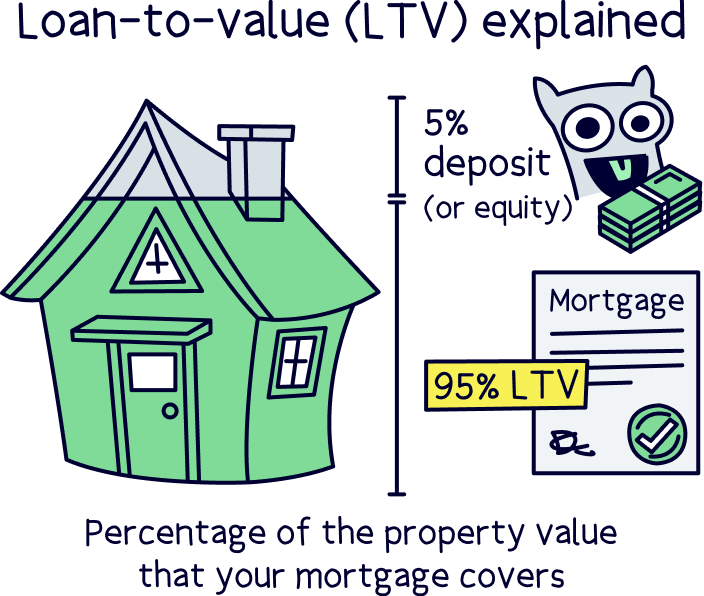

Well, it depends on the property you’re hoping to buy. Most lenders will let you borrow a maximum of 95% of the value of a property (known as a 95% LTV), which means you’ll need to be able to afford the remaining 5% yourself.

Confused? Don’t worry, let’s look at an example.

Say you want to buy a property that’s worth £200,000. Your lender will probably be willing to lend you a maximum of £190,000 (95% of 200,000 is 190,000). That means you’ll need a deposit of at least £10,000.

That said, the bigger the deposit you can put down the better, as lenders usually save the best deals for people with the lowest LTVs. Why? Well, it means you’re taking on a bigger share of the risk yourself.

Nuts About Money tip: You can check out your LTV based on your deposit and the price of the property with our mortgage repayment calculator.

Basically, it’s all to do with the worst-case scenario. If you get a mortgage and then, later down the line, you stop paying it, your mortgage lender is going to want to get their money back (makes sense, right?!). They’ll do this by selling your property at auction – normally at a discounted price as they’ll be trying to get the whole thing over and done with as quickly as possible (don’t panic, this is their absolute last resort!!).

The lower the LTV (and therefore, the bigger the deposit you pay), the more likely they are to be able to sell the property for a price that will get them their money back in full. Simple!

If you’re struggling to save enough for a decent deposit, don’t panic just yet. There is help available, like Lifetime ISAs (a great savings account that helps you save for your first home). We’ll take a look at this and some other schemes for first-time buyers in a bit.

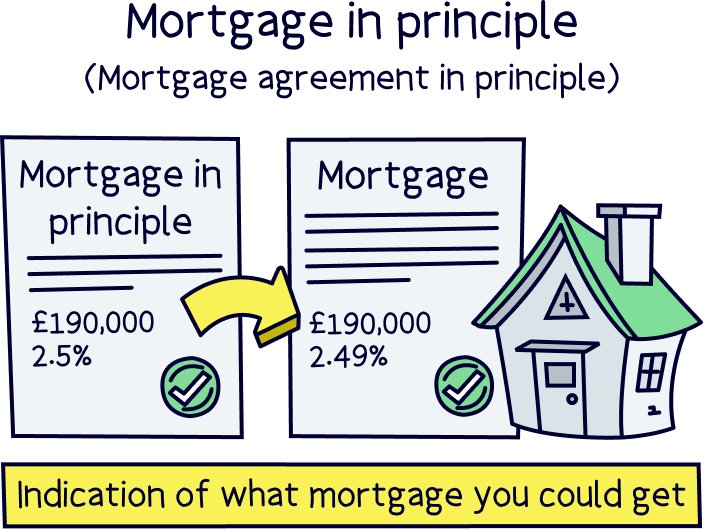

Once you’ve saved up a bit, the next step is to get a mortgage agreement in principle. You might have also heard it called a mortgage in principle, agreement in principle, decision in principle or mortgage promise.

It’s basically an official document from a lender that says they think you’d get accepted for a mortgage if you applied for one. It also confirms how much they’re likely to lend you.

Although you don’t have to get one, for most people, it’s an important step towards buying a home. Here are a few reasons why.

Mortgages in principle sound pretty great, huh? However, before you get too excited, bear in mind that they don’t guarantee you’ll get approved for a mortgage. Instead, they’re just a good early indication.

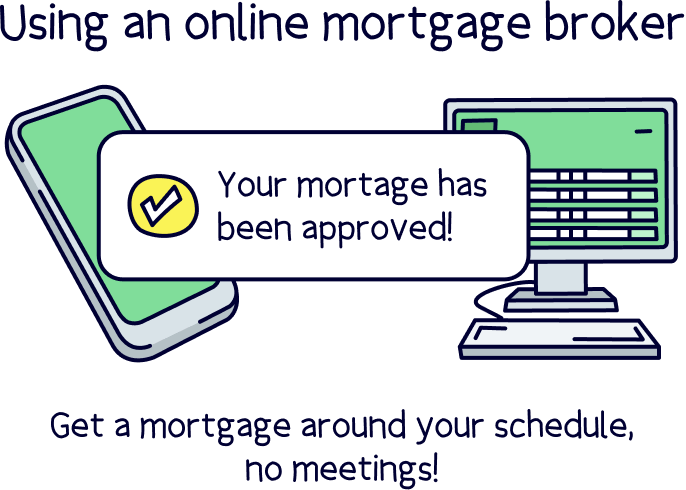

Anyway, the easiest way to get one is to go to one of those whole-of-market mortgage advisors we mentioned earlier (it’s super fast with an online mortgage broker too). They’ll be able to tell you which mortgage lenders are right for you, get you a mortgage in principle and even get you the best mortgage deal.

Later, when you’re ready to apply, they’ll handle the whole mortgage application process for you too.

You can go straight to the lender and apply for the mortgage in principle yourself instead. But let’s be honest, it’ll probably take you three times as long. Not only that, but you won’t have any way of knowing that you’ve picked the best lender, and you’ll be more likely to make a mistake that could lead to you getting rejected.

Ultimately, a mortgage broker can do all the hard work for you and potentially save you thousands of pounds a year. Meanwhile, you get to just put your feet up and watch Netflix. Sounds like a done deal to us!

You can’t apply for a mortgage until you’ve had an offer accepted on a property. So, now for the exciting part. This is where you get to snoop around other people’s houses pretending you’re on ‘Location, Location, Location’.

Most mortgages in principle only last 60 to 90 days, so ideally you’d want to find a property within this time. However, if you don’t, it’s really not the end of the world. Remember that buying a home is a huge investment (probably the biggest you’ll ever make!) so it’s important you take your time and don’t rush yourself.

If your mortgage in principle expires before you’ve fallen in love with a property, you can just apply for another one. Or, you could even just let it expire as you don’t actually need a mortgage agreement in principle in order to be able to buy a property.

The most important thing is that you find the right property for you, at a price you can afford. The rest will follow when you’re ready!

Nuts About Money tip: if you want to know how much you can afford, check out our take-home pay calculator.

Once you’ve had an offer accepted on your dream property, you can finally go ahead and actually apply for a mortgage!

If you got your mortgage agreement in principle through a mortgage advisor, you won’t have to do much at this point as they’ll already have all your details saved. That means you can just give them the go-ahead. They’ll pull together a mortgage application and submit it all for you while you twiddle your thumbs!

If you decided to go straight in with an offer without getting a mortgage in principle, that’s fine too. We’d still recommend getting a mortgage broker involved so they can nail your mortgage application and give you the best possible chance of getting approved. Not to mention the fact that it’ll just be a whole lot less stressful for you!

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Last but not least, you’ll just have to hold your breath and wait for your mortgage offer to come through.

You’ll normally get your lender’s decision around 2 to 6 weeks after your mortgage application is handed in, as they’ll need to carry out some checks – this includes something called a valuation survey, where they check how much they think your property is worth. So, it can be a bit nail-biting! Check out the mortgage application process to find out exactly what happens during this time.

Assuming all the checks go okay, it’ll all be worth the agonising wait. As soon as your mortgage offer makes its way through your inbox, it’s time to ring all your friends and family and scream down the phone to let them know you’re practically a homeowner! Congrats!

Just bear in mind that the home buying process isn’t over yet and, until you get the keys to your new pad, things could still fall through at any moment (although we’re keeping our fingers crossed for you that all goes to plan!). With that in mind, here are two things to remember:

Anyway, back to the positives. You’ve got yourself a well-deserved mortgage offer which calls for a big pat on the back and an even bigger bottle of bubbly. Happy days!

Of course, saving for a deposit is hard. And earning enough to prove you can afford the mortgage repayments can be hard too! So, you’ll be pleased to hear that there is support available if you’re buying your first home.

Here are some ways that you could get help, either from the government or from family and friends.

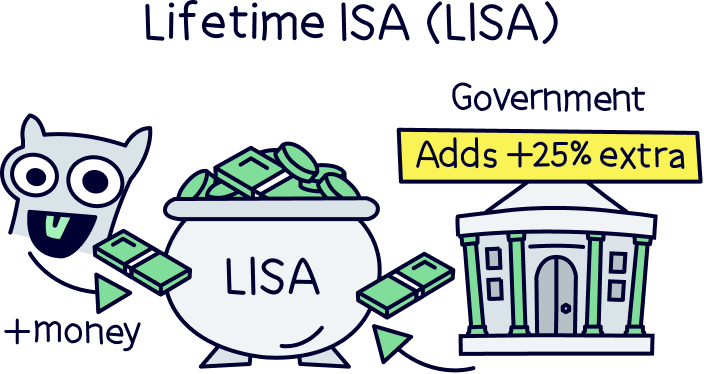

A Lifetime ISA is an amazing type of saving account designed to help first time buyers save to buy your first home (under £450,000), or to tide you over later on in life (over 60).

Each year, the government will give you a 25% bonus on any money you put in there (up to £4,000). Kerching!

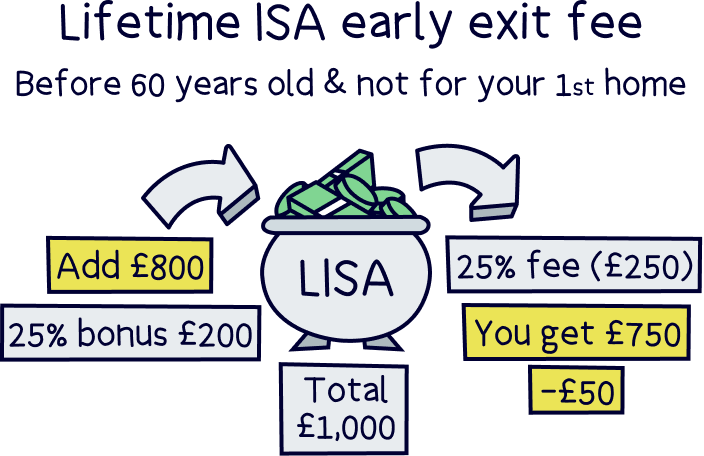

The catch? Well, if you want to withdraw your money for any other purpose, you’ll have to pay a hefty 25% withdrawal fee, which basically means you’ll be giving back more money than what the government gave you. So, you really need to make sure you use your ISA for the purposes it’s made for.

Just make sure that you make your first payment into the account before you’re 40, otherwise, you’re not going to be able to use it. Sadly, once you turn 50, you won’t be able to add to it anymore either, so it’s not really designed for anyone other than people buying their first home.

See how much you could save with our Lifetime ISA tool and compare the top Lifetime ISAs.

Shared Ownership is a government scheme for people who can prove they can’t afford to buy a home without help. On specific properties, it allows you to buy a share of a home instead of buying the whole thing. You then have to pay your mortgage on the part you own, and pay rent on the part you don’t own.

Sounds good?

Well, to be honest, we really wouldn’t recommend it. Most people never manage to buy the property outright. Instead, they’re faced with hidden fees and service charges that are expensive and unpredictable.

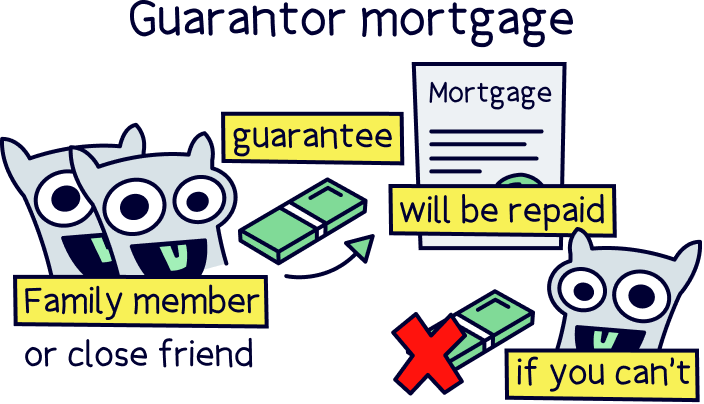

Lucky enough to have a friend or family member who wants to help you buy a property? Then applying for a guarantor mortgage could be a great shout.

A guarantor mortgage is where someone in a better financial position than you agrees to pay your mortgage repayments if you can’t. This can be really helpful if you’re struggling to prove to a mortgage lender that you’re going to be able to afford the repayments.

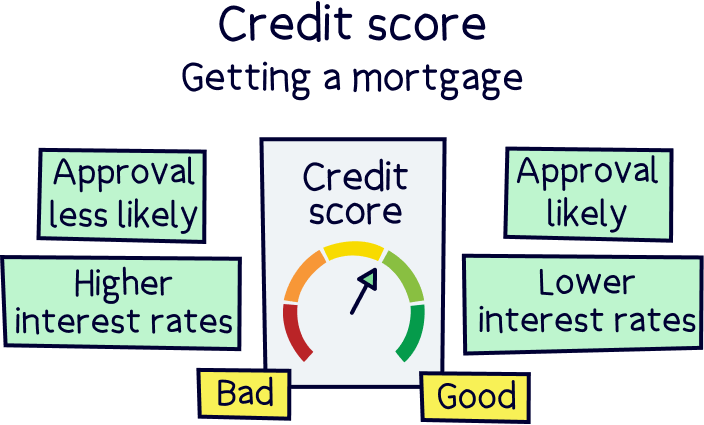

Maybe you don’t earn a lot. Or maybe you have a bad credit score which is putting lenders off. By promising to cover the repayments if you can’t, your guarantor will be able to ease your lender’s worries and make it more likely that your mortgage application is approved.

Just watch out though. If you don’t pay your mortgage, your guarantor will be legally obliged to pay it for you, which could even mean putting their house on the line if necessary. So, it’s a big commitment!

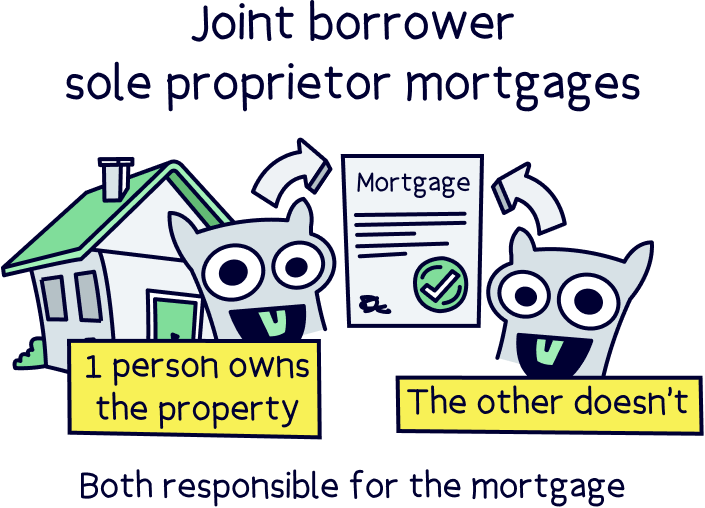

Another similar solution is a joint borrower sole proprietor mortgage (JBSP). This is similar to a guarantor mortgage in that it allows your friend or family member to help you get a mortgage. But in this case, they’ll be jointly responsible for paying your mortgage, even though they won’t own any part of the property. With a guarantor mortgage, on the other hand, your friend or family member is just there as a Plan B.

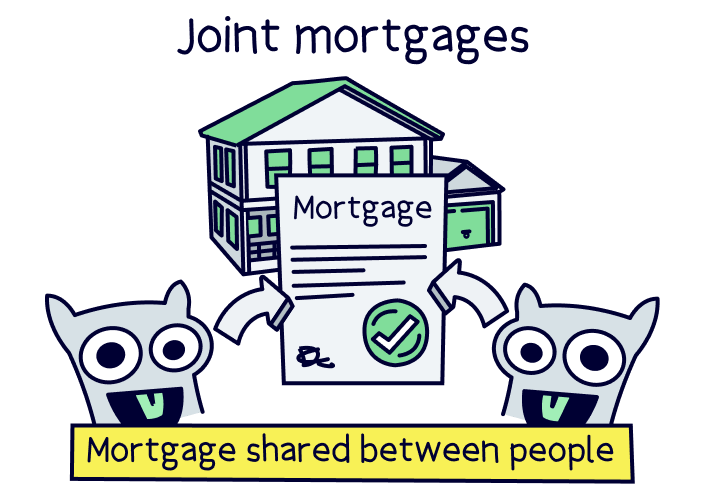

If you can’t afford to get a mortgage on your own, you could consider teaming up with someone else to get a mortgage and buy a house together, known as a joint mortgage.

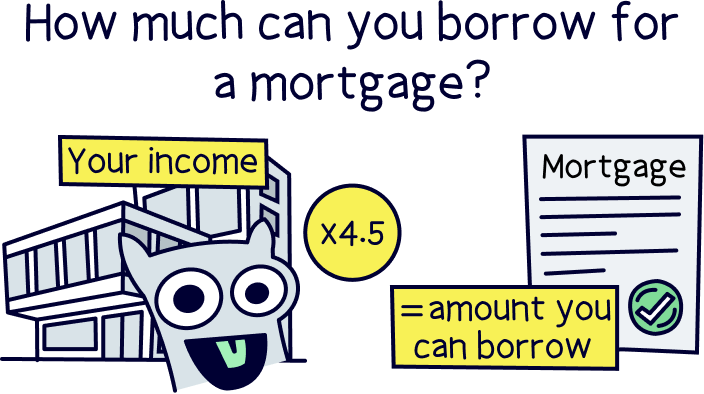

You know how we said that you’ll normally be able to borrow around 4.5 x your yearly income? Well, if there are two of you, you can add your incomes together to borrow more.

A bit lost? Let’s break it down.

Say you earn £20,000 a year. On your own, you’d probably be able to borrow around £90,000 (20,000 x 4.5 = 90,000). Now say your friend earns £20,000 as well. That means that together, you earn £40,000 and can probably borrow around £180,000 (40,000 x 4.5 = 180,000). That’s a big difference!

The only thing we would say is that you will jointly own the property. So, things could get a bit messy if you have an argument and fall out. And, if your friend doesn’t pay their share of the mortgage, you’ll be legally responsible.

Good question! A first time buyer is an official term that lenders and the government use to define anyone who hasn’t purchased a property before and is getting their first mortgage. As the government wants people to buy their own homes, first time buyers get special treatment.

The biggest benefit you have is that you get an even bigger allowance before you have to pay Stamp Duty Land Tax (that’s a tax on a property purchase). You won’t pay any Stamp Duty if the property price is less than £300,000. This is called first time buyer Stamp Duty relief.

If you’re not a first time buyer this would only be £125,000. The rate first time buyers will pay after this is 5% up to £925,000, and then 10% up to £1.5 million, and then 12% above that.

Nuts About Money tip: To find out how much Stamp Duty you might have to pay check out our Stamp Duty tool if you are buying in England or Northern Ireland. We also have a Land and Buildings Transaction Tax tool if you are buying in Scotland and a Land Transaction Tax tool for Wales.

And with mortgage lenders, often they’ll have first time buyer mortgages just for you, which can have different interest rates and criteria.

By the way, if you’ve purchased a property as a buy-to-let before, unfortunately you normally won’t count as a first time buyer.

Whether you need help or you’ve managed to save up enough yourself, getting a mortgage isn’t as hard as you might think – especially if you get a mortgage broker involved. Not only will they be able to help you find the right lender for you, but they can also give you tailored advice on how to make it more likely you’ll get approved.

You’ll see. You’ll be unpacking boxes in your own home before you know it!

As a reminder, if you need to find a mortgage broker, check out our top mortgage brokers. You can also see the latest interest rates with our mortgage comparison tool.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.