Article contents

If you want to make your own investment decisions the best Stocks and Shares ISAs for beginners are Lightyear and InvestEngine, they have low fees and a great range of investment options. Beach and Moneyfarm are great if you want a hands off approach – they’ll handle everything for you, have great investment records and low fees.

Ready to start saving for your future? Good thinking. Investing using a sensible investment strategy, can really pay off in the future – your savings can really grow and grow over the years!

For beginners, we recommend simply letting the experts handle everything for you. They’ll aim to grow your money over time, using tried and tested strategies – all you need to do is add your money. As simple as that. Plus, they’ll guide you through it all if you’d like (although the best ones are super simple to use too).

So, without further ado, here we go:

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Get up to £100 free share

Lightyear is a great, low cost investing and stock trading platform. There’s a good range of investment options (over 3,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

Company accounts: you can also invest as a business (e.g. limited company), and benefit from all the same low fees and great experience. Just select 'business' in the top of their website after you click through.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Great app

A great and easy to use investing app. Add money from your bank or transfer your existing ISA, with the investments handled by experts. There’s a pension pot too.

The customer service is excellent, with support based in the UK.

Beach is an easy to use investing app (and easy to set up), just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total savings whenever you like.

You’ll get an easy access pot (access money in around a week), which can be an ISA where all the money you make is tax-free (save up to £20,000 per tax year), and a standard account for those saving in addition to this (or who don’t want an ISA), where there’s no contribution limits (but also no tax-free benefits).

The investments are managed by experts from the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

There’s also an optional pension pot to save for retirement, so you can keep all your savings in one place, and if you’ve got lost or old pensions, Beach can also find them and move them over too.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Keen to learn a bit more about how we determined the best ISAs for you? Here’s the key criteria we looked at:

The Stocks & Shares ISAs we recommend above are all great for beginners, and we recommend them to our friends and family (and readers of course). We also use them ourselves here at Nuts About Money. Whichever, one you decide to go with, you can be confident your money is in safe hands.

They’re not just for beginners either, they’re super popular with experienced investors too – as letting the experts manage and grow your money is often the best way to invest.

It’s unlikely you’ll be able to do a better job yourself, there’s a lot to learn, and managing your own investments takes a lot of time, effort and it can be stressful!

Leaving it to the experts means you’ve got more time to do the things you love, and you can relax, knowing your money will be in safe hands.

Note: here's where to learn more about how we test.

A Stocks and Shares ISA (also known as an investment ISA), is perfect for saving and investing your cash while still having access to it whenever you need it (although we recommend investing for the long-term).

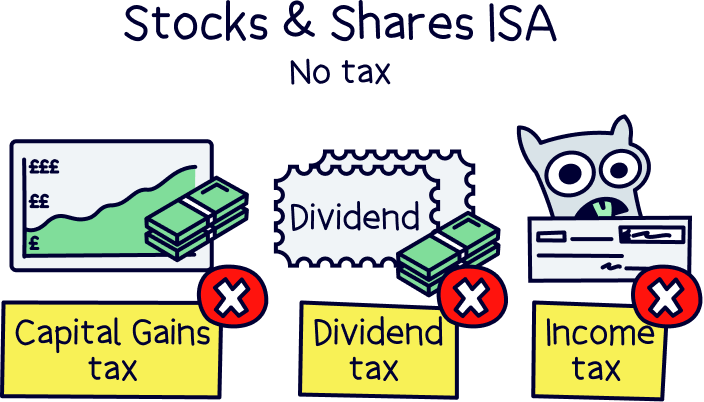

You’ll be able to save and invest completely tax-free, which means you don’t have to worry about Capital Gains Tax, Income Tax, or Dividend Tax – all different types of taxes you might pay on investments outside of an ISA.

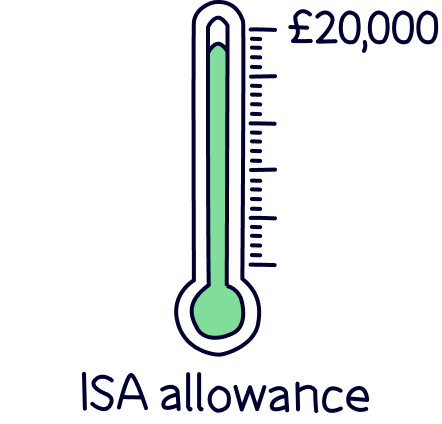

You can invest up to £20,000 per year into a Stocks and Shares ISA (and as many as you like), which is called your annual ISA allowance. And this is actually a total across all of your ISAs – for instance, a Cash ISA (where you save cash in return for interest) and a Lifetime ISA too (to help save for your first home).

Note: ISA stands for Individual Savings Account, and it’s a government scheme to help you save more.

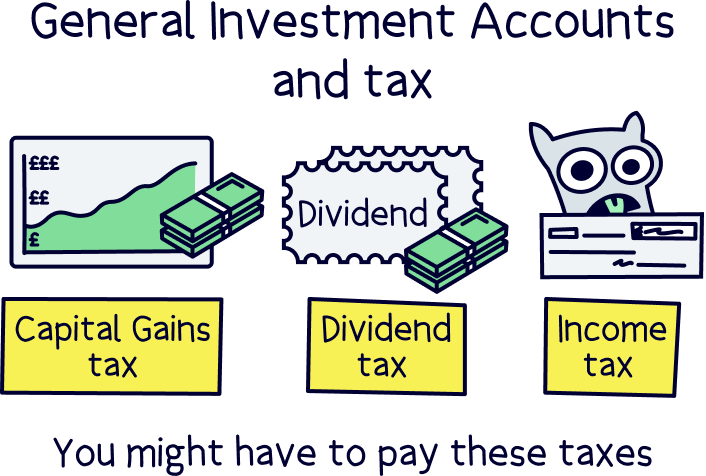

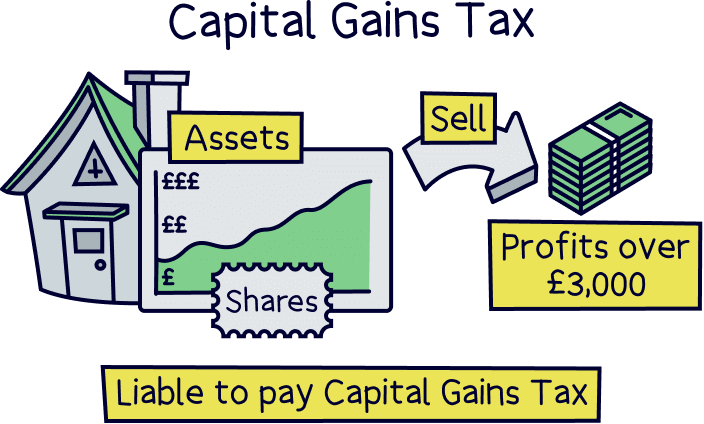

A General Investment Account is a ‘standard’ investing account that has no tax-free benefits. So, you might have to pay tax if you make a profit from your investments within a tax year (if they’re above your allowances).

For instance, you’ll have to pay Capital Gains Tax if you make a profit of over £3,000 per year, if you sell your investments. You’ll either pay 10% if you’re a basic rate taxpayer (earn less than £50,270) or 20% if you’re a higher rate taxpayer (earn over £50,270).

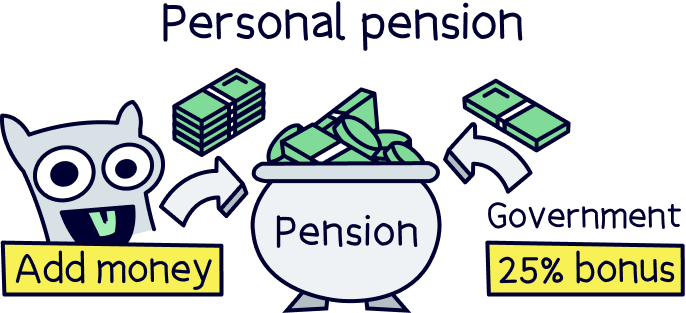

A Personal pension is a great investment account to save for retirement. In fact, it’s amazing.

You get a massive 25% bonus on all of your pension contributions, and if you’re a higher rate taxpayer (40%), or additional rate taxpayer (45%), you can claim back some of the tax paid at those rates too. This is done on your Self Assessment tax return.

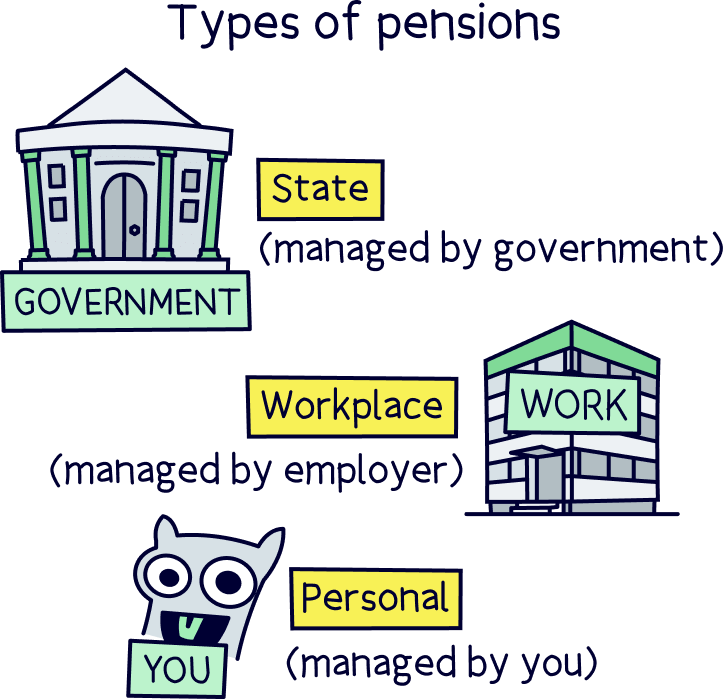

You can use a personal pension in addition to a workplace pension (a pension your employer will set up for you if you’re employed), and alongside the State Pension (the government pension), which you’ll get when you reach retirement age (currently 66), if you make enough National Insurance contributions over the years (at least 10 years but 35 years to get the full pension amount).

You won’t be able to access your money until you’re at least 55 years old (57 from 2028), so make sure you’re happy to lock it away for retirement – and we recommend keeping it saved for as long as possible, so it keeps growing until you do retire.

If this sounds interesting to you, we recommend getting started with PensionBee¹ – they make pensions super easy, have low fees and a great record of growing money over time. And, check out the best personal pensions to learn more and find all the best options.

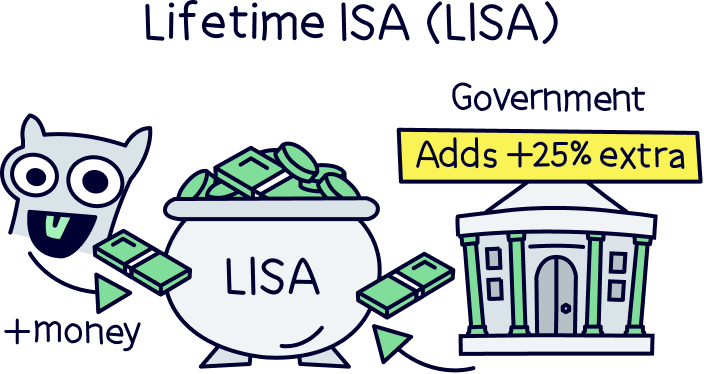

If you’re saving for your first home, you might want to consider a Lifetime ISA. You’ll be able to save up to £4,000 per tax year, and get a 25% bonus on your contributions (so up to £1,000 per year free).

You can only use this to buy your first home, or you’ll have to wait until you’re 60 before you can access the cash without paying a large 25% fee – which works out as more than you get from the bonus. Not fair right?!

The best Lifetime ISA is Tembo¹, with one of the highest interest rates out there.

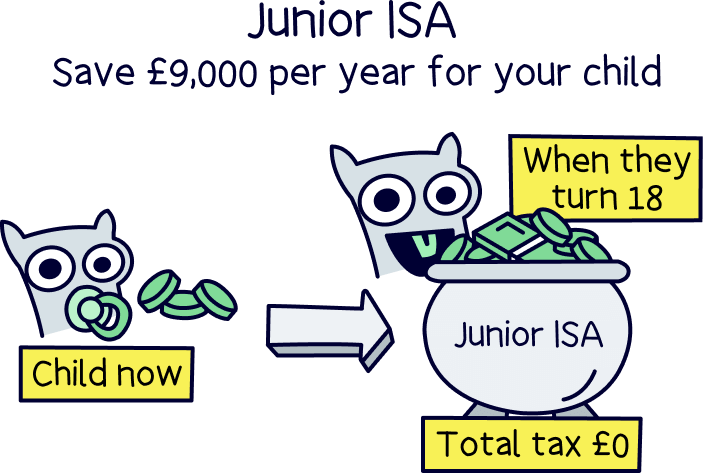

If you have kids, you can also build up some savings all in their name, called a Junior ISA, and all tax-free.

You can save up to £9,000 per year (per child), which is completely separate from your own annual ISA allowance.

You can use the same expert-managed Stocks & Shares ISA provider for Junior ISAs too (normally), so you can use one of the best ones out there, such as Moneyfarm¹, and benefit from potentially great investment performance, low fees and expert help.

Unless you’re one of the lucky ones in life, as a beginner, you likely won’t have much savings yet. And that’s okay. You can actually start investing with as little as £1 if you use Lightyear¹.

If you’re able to invest more than £500 as a lump sum to start with, you can use Moneyfarm¹. They’ve got expert advisors on hand to help you get started and answer any questions you might have – although it’s super easy to get started anyway.

Curious how your money actually grows within a Stocks and Shares ISA? Here’s the low down.

With experts looking after your investments, they’ll use sensible investment strategies suited to grow your money in a gradual way over the years, all suited to your financial goals.

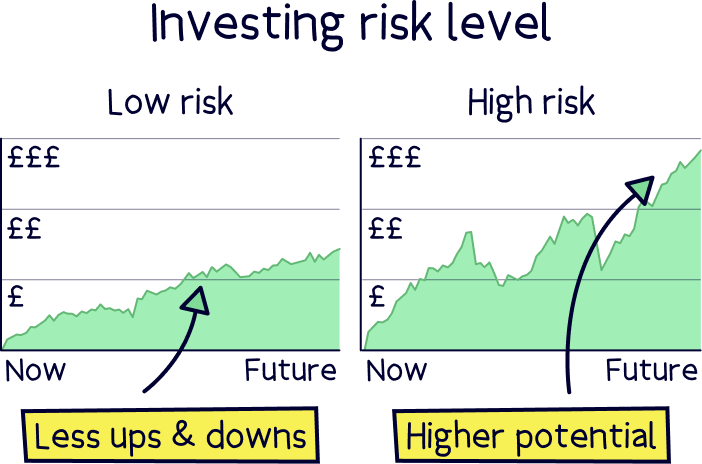

That works by first identifying the best investment strategy for you, from a few set options, normally categorised into risk options (don’t let the word risk put you off). And these range from lower risk to higher risk.

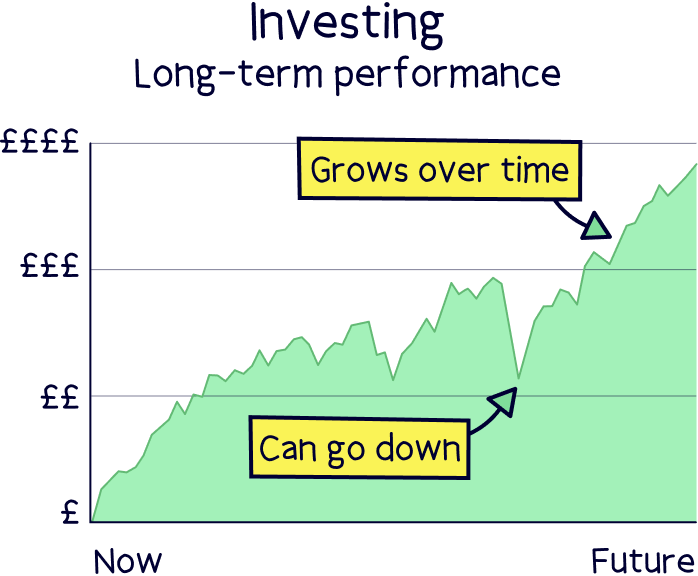

With higher risk, your money is likely to grow much more over the long-term. But, there will be more ups-and-downs along the way. These are great if you’re investing for over 5 years, and often with a more longer term view (long-term is often seen as the best investment strategy).

With lower risk options, there’s less up-and-downs, but your money is likely to grow slower. If you think you might need the cash within the next few years, these can be a better option.

Depending on which risk option you choose, your money will be invested in a range of different investments (called an investment portfolio), which include stocks and shares, investment funds, bonds and property:

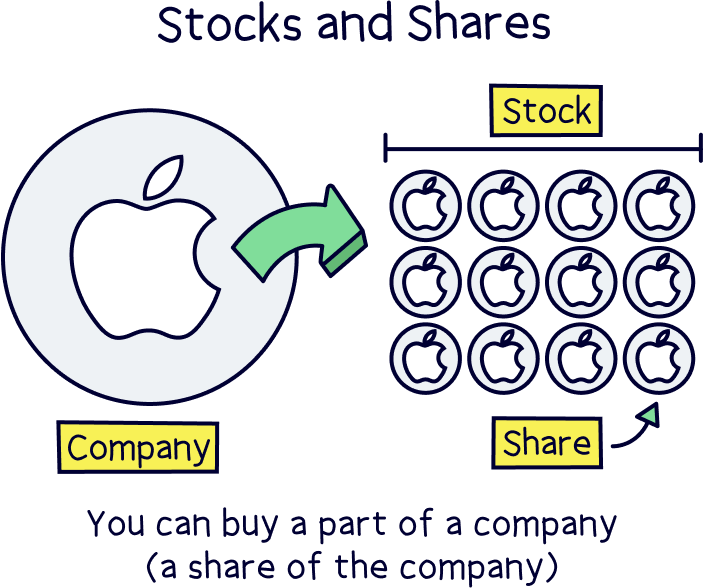

Shares are where you own part of a company, a ‘share’ of the company. And they can be bought and sold on stock exchanges across the world, such as the London Stock Exchange (LSE), in the UK.

All the shares combined equal the value of the company, and this value changes both up and down, depending on the performance of the company or the stock market in general.

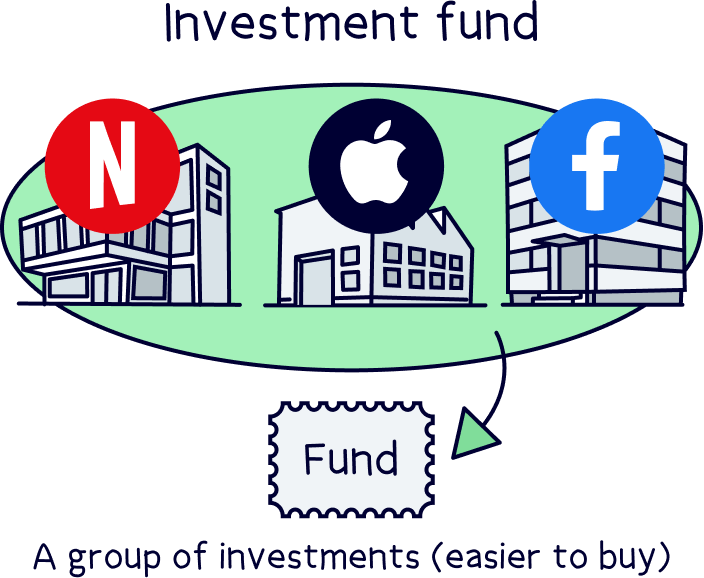

An investment fund is a group of lots of different investments all pooled into one single investment and managed by experts (called a fund manager). For instance, lots of individual company shares grouped into one investment, such as green energy companies or electric vehicle companies. And even things like the top 100 largest companies in the UK, called the FTSE 100.

Thousands of investment funds can be bought and sold on stock exchanges, making them much easier to buy, and these are called exchange-traded funds (ETFs). And they’re super popular with both beginners and experts.

Bonds are where you effectively lend your money to governments or large corporations (corporate bonds) in exchange from interest payments. These are typically seen as lower risk than stocks and shares.

This is often commercial property, such as offices and shops, and provides a rental income.

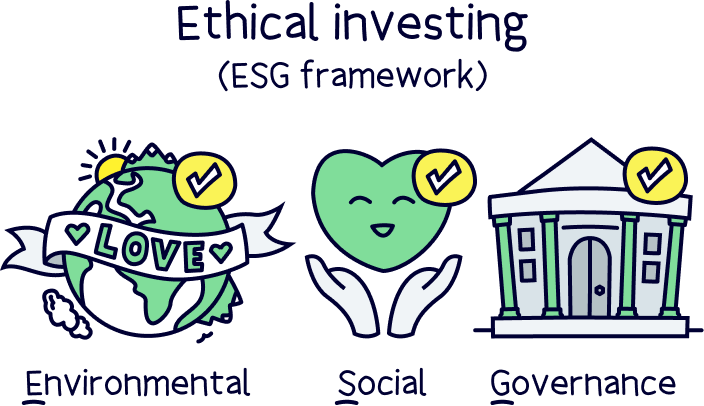

You can also choose to have your money only in socially responsible investments too. By doing this your money is invested into businesses that have a positive impact on the planet and people, such as improving the environment (e.g. no fossil fuels), or not using forced labour or very low pay in producing goods (such as clothes).

That's it in a nutshell, but really there's a lot more to it – and overall the category is called ESG, which stands for environmental, Social and governance. Or, impact investing (which is typically a bit stricter in terms of the positive impact on the planet).

Here at Nuts About Money, we’ve carried out some in-depth analysis on the best performing investment ISAs to find the best out there.

We found the best performing Stocks and Shares ISA over the last 5 years to be Moneyfarm – they really walked away with it compared to the other top ISA providers Nutmeg and Wealthify, and in the industry average in general.

You can read lots more about it and view all the results with our guide to the best performing Stocks and Shares ISAs.

As an example, on a higher risk investment option, which is common for long-term investing, here’s compared they compared:

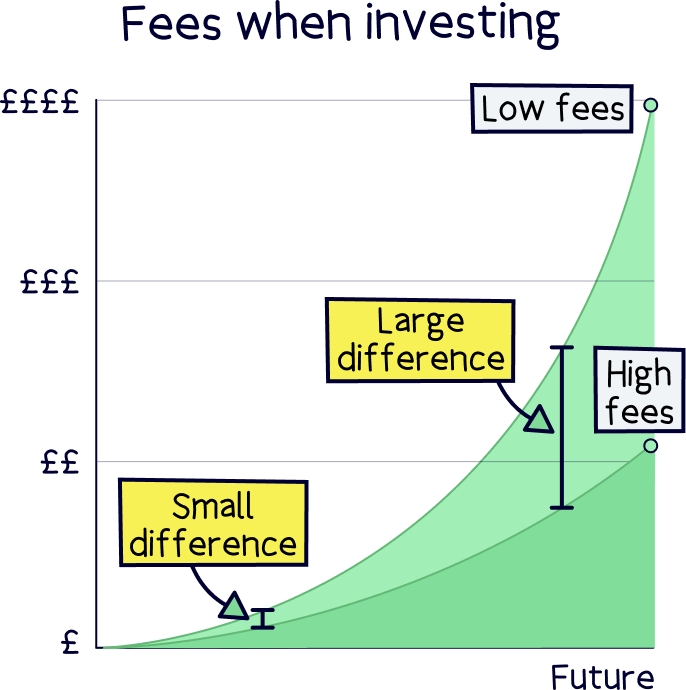

You might be surprised to know that Stocks and Shares ISAs can be pretty low cost these days – even when the experts handle the investments for you.

With expert-managed investment ISAs, you pay a percentage of the total amount you have invested every year, and this can range from 0.25% to 1.5%+.

This is made up of an annual account fee (or platform fee), which the ISA provider charges to look after your money, and then fees for the investments themselves (which go to the experts, called fund managers), and this can also include investment trading fees (fees to actually buy and sell investments).

If you’re keen to make your own investments with a self-managed Stocks and Shares ISA, it works a bit differently, and depends on which ISA provider you use.

Typically, there will be an account management fee, which can be a percentage of the amount you have invested (or a flat fee per month), and then a share dealing fee, which is a fee to buy and sell investments.

It’s completely safe to use a Stocks and Shares ISA for your money and to make investments.

Every ISA provider must be authorised by the Financial Conduct Authority (FCA). That means they’ve been reviewed and approved to look after your money. They’ll also be constantly monitored to make sure they’re looking after your best interests.

You can check the FCA register to make sure a financial firm is authorised by the FCA. All of our recommendations are FCA authorised.

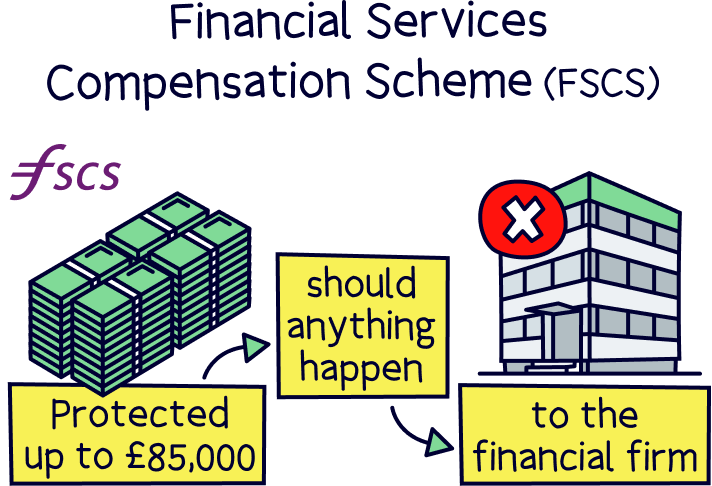

This also means you are protected by the Financial Services Compensation Scheme (FSCS). This covers you for up to £85,000 if something bad happens to your ISA provider, such as going out of business (highly unlikely).

However, your money and investments are actually held with a separate, large bank, with the investments all in your name, and can only be returned to you.

But, this doesn’t mean you can’t lose money if your investments go down in value. This can happen in the short-term (remember those ups-and-downs?), but given long enough, and using the right investment strategy, over the long term these up-and-downs should smooth out.

There we go – the best Stocks and Shares ISAs for beginners. We hope that’s made investing a bit easier to understand, especially the great tax benefits of ISAs. And most importantly, how easy it actually is to invest – simply let the experts handle things!

Investing using a sensible investment strategy over the long-term can really improve your financial future, and it’s highly recommended. If you want to learn even more about investing, here’s a guide to the best Stocks and Shares ISAs overall.

Well done for taking the plunge and looking into Stocks and Shares ISAs, your future self will really thank you!

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.