Article contents

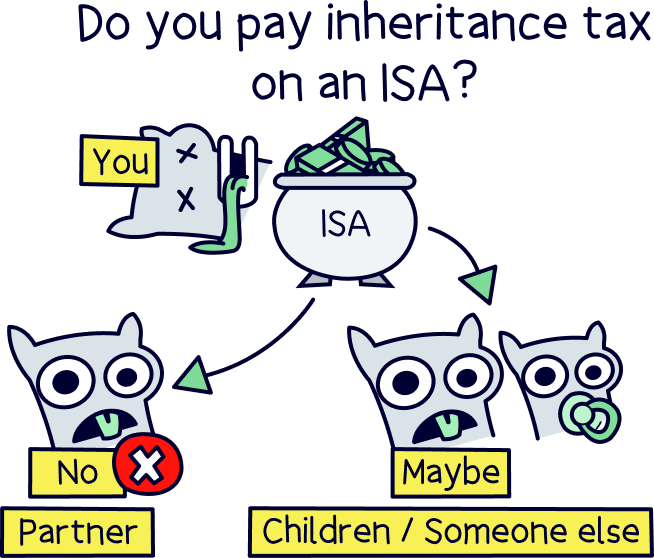

Yes. You’ll pay inheritance tax on an ISA. However, if you leave behind a partner, they won’t need to pay any inheritance tax. If you’re leaving it to someone else, they’ll only pay inheritance tax if the total value of all your assets is worth over £325,000 (things like your house, savings etc).

Tax can be a complicated topic, and ISAs are no different. Here’s what you need to know about ISAs and inheritance tax.

An ISA does count for inheritance tax, however that doesn’t mean that tax will necessarily be paid on your ISA, or inheritance tax at all on anything. It all depends on the personal circumstances and the family or friends left behind.

Let’s explain a bit more.

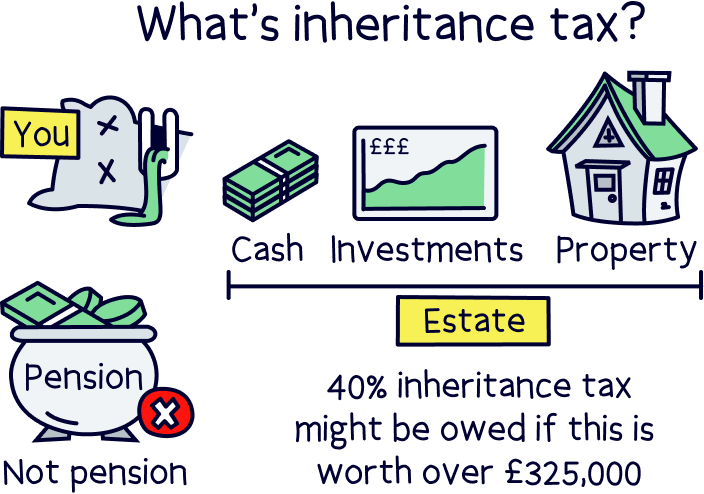

First up, let’s clarify what inheritance tax actually is.

It’s a tax that’s paid when a person passes away, and intended more for those who have a fair amount in assets (that’s things like cash, investments, property). All of your assets added up are called your estate (except your pension, more on that later).

Inheritance tax doesn’t apply unless the total of your estate is over £325,000. Anything above that figure, you’ll pay 40% tax, pretty hefty right?

To make things more complicated, if you leave everything to either your spouse (a husband or wife), a civil partner, or a charity or a community amateur sports club, there won’t be any tax at all, even above £325,000.

Further still, if you own your own home, and you leave it to your children or grandchildren the amount increases to £500,000 (unless your total estate is worth over £2 million).

So just to recap, you should only expect inheritance tax to be paid if you don’t pass on your estate to your partner, and the rate paid is 40% on anything above £325,000 (unless you own your home and then it can increase to £500,000 if passed onto your children).

By the way, your pensions don't count towards your estate when you die – they’re passed to whoever you name with your pension provider. That’s one of the many reasons why a personal pension is a great idea (you also get great tax benefits). If you haven’t got one yet, find the best private pension provider for you.

We've reviewed the best Stocks & Shares ISAs. Make sure you're using the best.

An ISA (Individual Savings Account) is a great idea to save your money, you can either choose a Cash ISA, or a Stocks and Shares ISA (or both), and everything you make inside your ISA is completely tax-free.

That’s the interest you get from your cash savings, which you might have paid income tax on (which is the same tax as your earnings, such as a salary). Capital Gains Tax, which is tax on any increase in value of your investments. And Dividend Tax, which is what you’d pay if a business you own pays out profits to its owners (for instance if you owned shares in a company).

Not paying any of these taxes means your money can grow much faster than if you did have to pay tax on it.

You can save up to £20,000 per year, which is called your ISA allowance.

So what about ISAs and inheritance tax then?

Well, ISAs will form part of your estate – which is the value of everything you own. So, if you’re passing your estate onto your partner, there’s nothing to pay.

If you’re not passing your estate onto your partner, for instance passing it onto your children, then if your estate is over £325,000, it will be liable to inheritance tax (on the part that’s above £325,000), which is currently 40%.

If you die before your partner (spouse or civil partner), then they can get the value of your ISA added to their ISA, so they can effectively top up their ISA with the value of your ISA. This is called an Additional Permitted Subscription (APS).

So, if you had £50,000 within your ISA, and you pass away, your partner can now add £50,000 into their own ISA, and it won’t affect their own allowance. So they can keep saving tax-free, just as your ISA would have done.

If you have a Stocks & Shares ISA, they can also request that your ISA is transferred as it is, instead of having to sell your assets to then add money into their ISA.

They’ll have up to 3 years to do this, or if the transfer of the asset takes longer, then they’ll have 180 days after the administration of your estate has been completed.

You might be thinking potentially giving away 40% of your ISA is quite a lot, and it is! That’s effectively what would happen if you already had an estate over £325,000, and if you didn’t have a surviving partner.

There’s one way to avoid paying inheritance tax with your ISA, but it’s not recommended. And it only applies to Stocks & Shares ISA.

You could sell all of your current investments and then purchase investments in businesses with certain exemptions from inheritance tax (the exemption is called business relief).

These businesses are on the AIM stock market (Alternative Investment Market), which is a part of the London Stock Exchange, but for smaller companies. This way, your ISA wouldn’t be liable for any inheritance tax.

However, as the companies are smaller, their stock price is more volatile (moves up and down a lot more), and therefore it’s very risky, as you may find the value of your portfolio drops significantly (although it could increase significantly too).

Not every business on the AIM market qualifies however, so it’s worth getting professional advice. There are even ISAs specifically for this, called inheritance tax ISAs. Check out Unbiased¹ to find the right financial advisor for you.

So there we have it. Your tax-free ISA is unfortunately not completely tax-free, ultimately inheritance tax could be paid on it if you were to pass it down to your children, or someone that’s not your partner.

It’s a bit different to a private pension, which is exempt from inheritance tax, and you can pass this onto whoever you like – it’s not part of your estate.

However, you might not need to worry about inheritance tax unless your estate is going to be over £325,000, and even then only if you don’t pass this onto your surviving partner.

If you’re interested in learning more, it’s best to speak to a financial advisor about your specific circumstances. You can find the best one for you with Unbiased¹.

We've reviewed the best Stocks & Shares ISAs. Make sure you're using the best.

We've reviewed the best Stocks & Shares ISAs. Make sure you're using the best.

We've reviewed the best Stocks & Shares ISAs. Make sure you're using the best.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We've reviewed the best Stocks & Shares ISAs. Make sure you're using the best.