Article contents

Bonuses are taxed in exactly the same way as your normal salary. So you’d pay income tax and national insurance on it, plus any other deductions such as a student loan. However, there is a legal way to avoid paying tax.

Earning a bonus should be a cause for celebration, your hard work has paid off, and you’ve earned yourself a good reward for all that effort. But now worried about losing all of that in tax?

It’s a genuine concern, tax is not always kind to bonuses.

Technically you will have to pay exactly the same tax rates as you would on your salary, as a bonus counts as earnings. Which means you’ll be paying income tax and you’d also pay National Insurance Contributions (NIC), plus any other deductions such as a student loan.

But luckily it’s all managed by your employer through your pay – if you are employed of course.

However, there is actually a legal way to avoid paying tax on your bonus! We’ll get to that below, first let’s take a look at how much you’ll actually be paying.

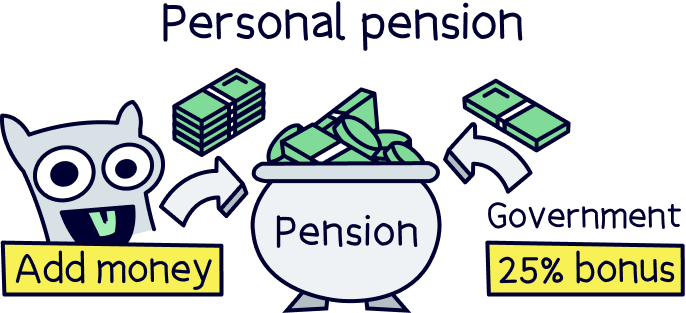

Save into a personal pension with Beach and you'll get a 25% tax bonus every time you save.

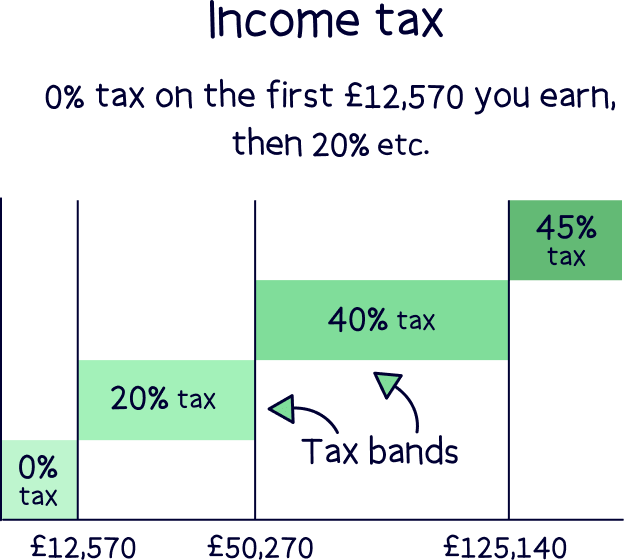

Let’s start with income tax, in the table below is what you’d pay in England, Wales and Northern Ireland.

The first £12,570 you earn is completely tax free, and then you’ll pay 20% tax on anything after that up to £50,270 and then 40% tax on anything above that up to £125,140, and then 45% on anything above £125,140.

And if you’re in Scotland, this is what you’d pay:

There’s also a hidden tax that is rarely mentioned by the Government, it’s almost like they don’t want you to know about it... It’s known as the 60% tax trap, and it exists on earnings between £100,000 and £125,000 per year.

60%?! Yep. What happens is, your personal allowance, that’s the first £12,570 of your earnings where you don’t pay any tax - is reduced by £1 for every £2 you earn over £100,000, until you reach £125,140. And after that you don’t get a personal allowance at all.

That works out to 20% more tax on your earnings between £100,000 and £125,140, and that’s on top of you paying 40% (41% in Scotland) as a higher rate tax payer, so effectively you are paying 60% tax. Sorry to be the bearer of bad news!

National insurance is a bit simpler, depending on which income range your bonus falls into, you’ll simply pay the corresponding rate on the bonus, so if you earn £35,000 per year and get a bonus of £5,000, your bonus will be in the ‘£12,571 to £50,270’ range and you’ll pay 8% on that.

If you’ve got a student loan, you’ll have to make repayments from your bonus, just as you would with your normal salary.

If you normally make pension contributions, these won’t necessarily be deducted from your bonus automatically, as pensions and other variable payments such as overtime are normally excluded from automatic contributions. However, if your employer has opted to use a system that is based on total earnings, then pension contributions would be deducted from your bonus.

However, your pension could be a bit of a life-saver for you retaining as much money as possible from your bonus. We’ll dive into that below.

If you have children living with you, and you or your partner (if you have one) claim Child Benefit, and if you earn over £60,000, you’ll also be liable to pay the High Income Child Benefit Charge. If both of you earn over £60,000, the higher earner would pay the charge.

The charge is 1% of your Child Benefit payment for every £100 of income over £60,000. And over £80,000 you effectively lose your Child Benefit. Learn more about the charge here.

We don’t recommend trying to evade tax at all, and we’re not here to give advice on that. However, working hard for your bonus to then effectively give a lot of it away might not make sense for you, especially if you are a higher earner.

There is a way specific to bonus payments, where you can effectively reduce the amount of tax you’ll pay, but you also forfeit getting the cash straight away. The answer? You pay it all into your pension instead.

Let’s run through an example:

Imagine you earned £100,000 per year as a base salary, and were given a £10,000 bonus.

First you’d be paying income tax of 40% on your bonus, which is £4,000.

You’d then be paying National Insurance Contributions of 2%, which is £200.

And then you’d be losing £1 of your personal allowance for every £2 you make over £100,000 (up to £125,140 when you lose your whole personal allowance). So that’s a £5,000 reduction in your personal allowance, which means you would now pay 40% income tax on the £5,000 too, which gives you a figure of £2,000 extra income tax to be paid.

Which gives us:

-£4,000 paid in income tax

-£200 paid in National Insurance Contributions

-£2,000 extra in income tax due to reduction in your personal allowance

For a total of £6,200. You’ll be taking home £3,800 of your £10,000 bonus. Not exactly what you were expecting was it? And if you had a student loan and any other deductions, they’d come off too.

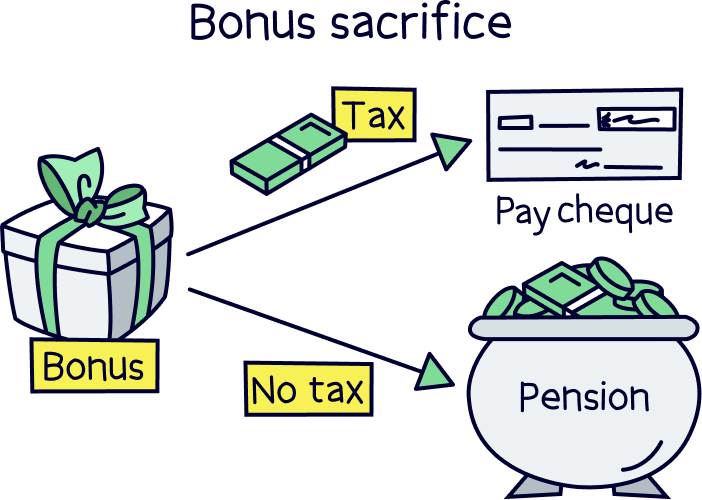

Now, there is a way to avoid paying all of this tax, National Insurance Contributions and additional deductions if you wanted to, but unfortunately doesn’t mean you can walk away with all the cash tax free!

The answer is to pay your bonus into your pension via your employer – called bonus sacrifice.

This way, you won’t pay any income tax or National Insurance Contributions at all, or any additional deductions if you have them.

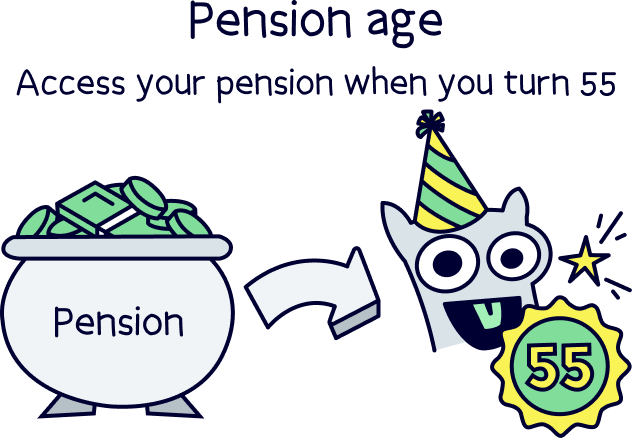

The downside is you won’t get the cash until you retire, at the earliest, currently 55 (57 from 2028).

All you need to do is tell your employer you want it paid into your pension instead, and they should take care of it all.

Better yet, your employer will also save on employer National Insurance Contributions, so they may even pay this saving into your pension too (it’s worth asking them, if you don’t ask you don’t get!), and they’ll normally top up your pension with employer pension contributions too.

This means you could be walking away with more money than your actual bonus was, with all the additions!

Nuts About Money tip: while we're on the topic of pensions. It could be a good idea to set up a personal pension to help you financially when you retire (you'll get a 25% bonus to return some tax you are owed).

If you're interested, check out PensionBee¹, they're 5* rated, easy to use, have low fees and a great track record of growing pensions over time. Here’s our PensionBee review to learn more. Beach¹ is also really great, they don’t just cater for pensions, they have an easy access account too (a tax-free ISA), plus the app is easy to use and the customer service is excellent. Alternatively, you can compare the best pension providers.

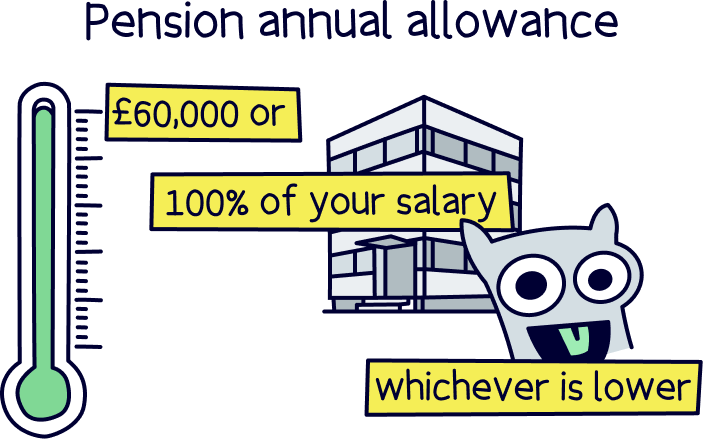

There are some limitations to this method however – pension contributions aren’t unlimited.

You can only pay £60,000 or 100% of your salary (whichever is lower) per year into your pension tax free.

But, if you haven’t hit this limit in previous years, you can actually use the previous 3 years unused allowance too. This is called ‘pension carry forward’. Technically you could invest £160,000 into your pension in one year if you haven’t paid into it for 3 years.

If you are lucky enough to earn over £260,000 per year, your pension contribution allowance also reduces by £1 for every £2 above this figure, to a minimum of £10,000 into your pension per year (so you'll always have an allowance of £10,000, whatever your income).

Tax is a complicated world. And bonuses are right in the middle of it. It’s up to you if you want to take your bonus in cash or put it into your pension, but it certainly makes sense for higher earners to seriously consider it, especially if you are earning between £100,000 and £125,000 where you’ll end up paying 60% tax on your bonus.

It’s a complex topic, and we’ve tried to simplify it, but if you’ve got more questions, chat with your employer – they would have dealt with this many times before, so just reach out for help and advice if you need it.

You’re not doing anything wrong by paying it into your pension, and you’ll be making a very sensible decision for your retirement, the only downside is you can’t spend it on that new car just yet!

Save into a personal pension with Beach and you'll get a 25% tax bonus every time you save.

Save into a personal pension with Beach and you'll get a 25% tax bonus every time you save.

Save into a personal pension with Beach and you'll get a 25% tax bonus every time you save.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Save into a personal pension with Beach and you'll get a 25% tax bonus every time you save.