Article contents

Self-select ISAs are investment accounts where you make the investment decisions. The best self-select ISAs are Lightyear, InvestEngine and AJ Bell. They’re all low cost, have great, easy to use apps and a great range of investment options.

Keen to make your own investments within your ISA? Here’s the best self-select ISAs:

Get up to £100 free share

Lightyear is an awesome mobile app with very low cost investing.

There’s a decent range of investment options (over 4,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

You can invest with a tax-free ISA, a regular account and a business account.

And if you’ve got cash savings, you’ll also get one of the best rates possible with their Cash ISA (it matches the Bank of England base rate).

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

Easy to use

A great and easy to use investing app. Add money from your bank or transfer your existing ISA, with the investments handled by experts. There’s a pension pot too.

The customer service is excellent, and has email and phone support based in the UK.

Beach is an easy to use investing app (and easy to set up), just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total savings whenever you like.

You’ll get an easy access pot (access money in around a week), which can be an ISA where all the money you make is tax-free (save up to £20,000 per tax year), and a standard account for those saving in addition to this (or who don’t want an ISA), where there’s no contribution limits (but also no tax-free benefits).

The investments are managed by experts from the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

There’s also an optional pension pot to save for retirement, so you can keep all your savings in one place, and if you’ve got lost or old pensions, Beach can also find them and move them over too.

Fees: a simple annual fee of up to 0.98% (minimum £4.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Pros

Cons

We’ve reviewed almost every self-select ISA out there to determine the best, and even the best managed Stocks and Shares ISAs (we’ll cover those below).

Here’s the criteria we used:

There’s loads of options out there, but we’re only recommending the very best self-select ISAs – one’s that we recommend to our friends and family (and readers of course). Our team also uses them here at Nuts About Money.

So, whichever ISA you choose from the ones above, you can be sure you’re using one of the best out there, with the lowest fees and a great range of investment options.

Self-select ISAs can have quite a few names, a self-select ISA, self Investment ISA, a self-managed Stocks and Shares ISA, an investment ISA, trading ISA – the list goes on…

However, what they officially are is a Stock and Shares ISA, and one where you make the investments yourself, you self-select them. So, you’ll be choosing which investments to buy, which to sell, and when to buy and sell – everything is up to you.

And hopefully with the intention of building a well diversified portfolio for long-term growth (your total investments).

Typically, the ISA is with an investment platform (a place to buy and sell investments), often also called a stock broker.

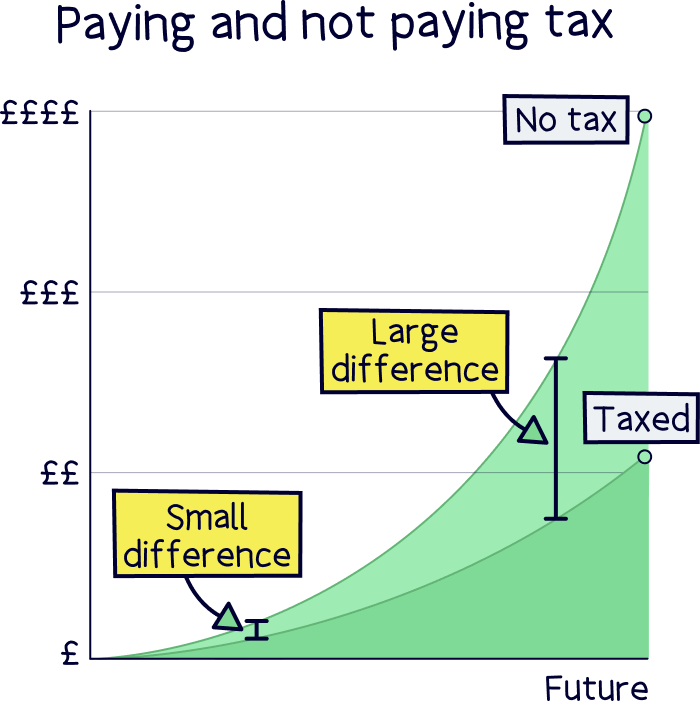

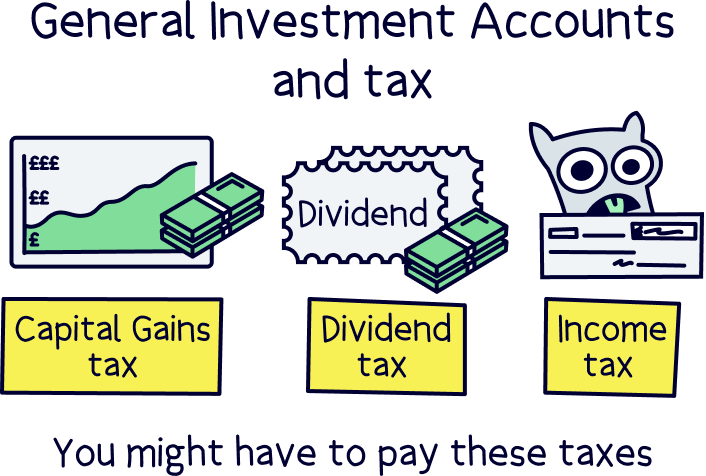

With an ISA you’ll benefit from tax-free investing, so you’ll save on Capital Gains Tax, Income Tax and Dividend Tax – forever! This can be a massive saving over the years as your total investments grow (providing you’re using a sensible long-term investment strategy).

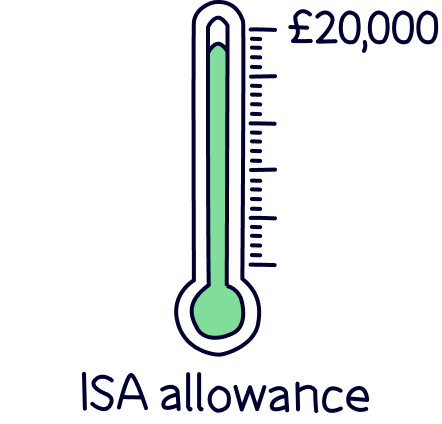

You can invest as much as £20,000 per year into your ISA, which is called your annual ISA allowance. And this is shared across all the different types of ISAs (if you have more), such as a Cash ISA (for cash savings), or Lifetime ISA (for buying your first home).

The alternative to a self-select ISA, and a great option, is an expert-managed Stocks and Shares ISA, where the experts handle the investments…

Note: ‘ISA’ simply stands for Individual Savings Account, a government scheme to help you save more – and tax-free.

Expert-managed Stocks and Shares ISAs are amazing. You don’t have to do much, simply add your money, and the experts will take care of the investments – they’ll aim to grow your money over time in a safe and sensible way. And they’re typically very good at it.

We highly recommend them here at Nuts About Money. Leave it to the experts to build a well diversified investment portfolio for long-term growth.

If you’re new to investing, check out the best Stocks and Shares ISAs for beginners, you’ll find the right expert-managed investment options for you, or simply check out the best investment platforms for all your options.

This doesn’t necessarily mean you only have to use the experts to manage all of your investments, you can make your own investments alongside an expert-managed ISA with a regular investment account, called a General Investment Account (GIA), or even a self-invested personal pension (SIPP) – let’s dive into those.

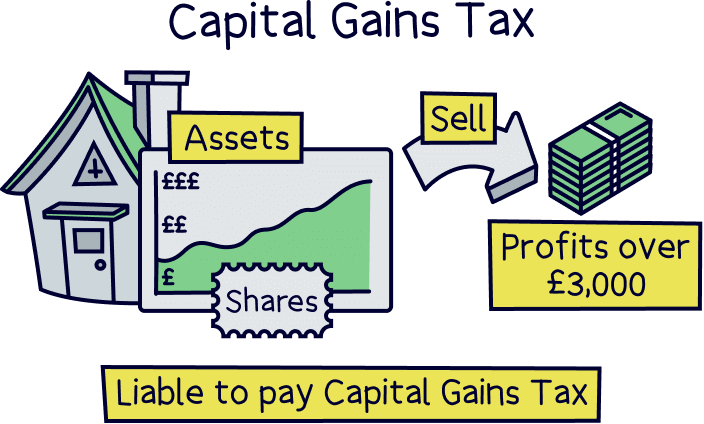

A General Investment Account is your standard account that you’ll be able to get with almost every investment platform and stock broker. There’s no tax-free benefits, but there’s also no contribution limits.

Often, you’ll pay Capital Gains Tax on your profits if they’re over £3,000 (when you sell), within a tax year (April 6th to April 5th the following year). And this is 10% if you’re earning less than £50,270 in income per year (e.g. your salary), and 20% if you earn more than that (e.g. a higher rate taxpayer).

They’re a great addition to an expert-managed investment ISA, which could hold the majority of your savings, so in the safe hands of the experts. And then make your own investments with a GIA, where you might not end up paying tax anyway.

If you are interested in getting a GIA check out the best GIA platforms.

And for expert-managed ISAs, we recommend interactive investor¹ – they have a great investment performance and low fees. Learn more with the best performing Stocks and Shares ISAs.

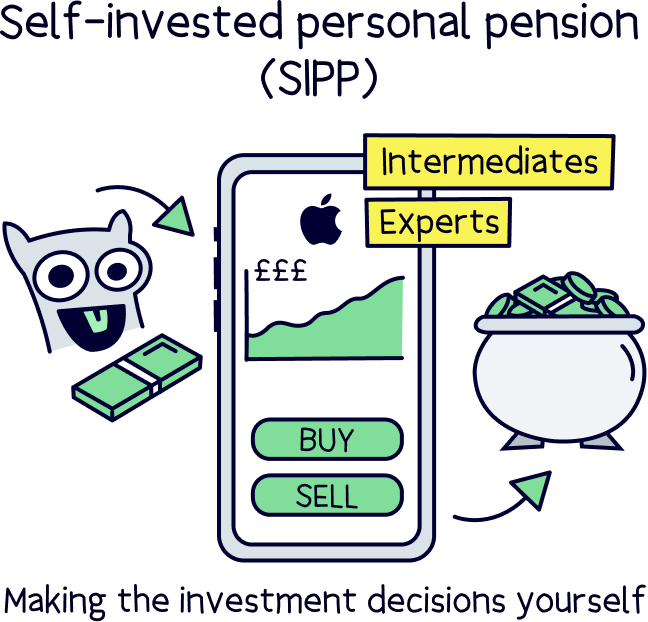

You’ve also got the option to invest within a personal pension, and if you’re making your own investments, a self-invested personal pension (SIPP).

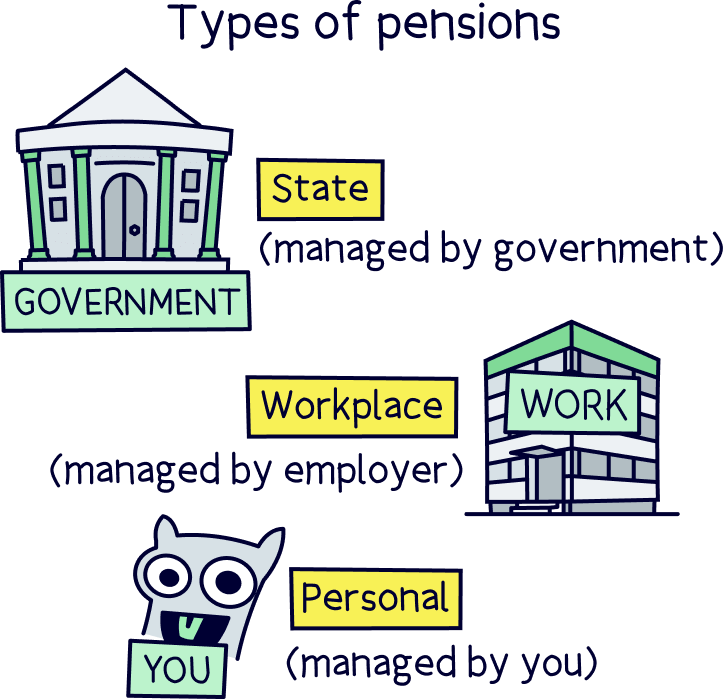

These are great, and the best option for long-term saving and building a big pension pot ready for retirement. Often used in addition to the State Pension (government pension) and a workplace pension (if you have one), which is a pension your employer sets up for you if you’re employed.

Nuts About Money tip: Check the age you'll get the State Pension with our State Pension age calculator.

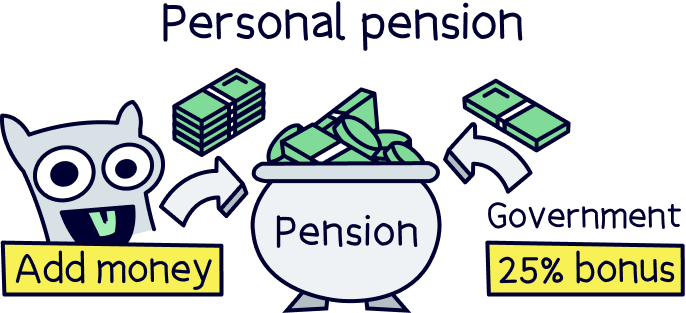

When you contribute to a personal pension, you’ll get a massive 25% bonus added automatically by the government. We’re not joking! And if you’re a higher rate taxpayer (40%) or additional rate taxpayer (45%), you can claim back some tax that you’ve paid at those rates too – which is done on your Self Assessment tax return. If you want help with your Self Assessment tax return, Taxfix¹ can help, their service is low cost and 5* rated.

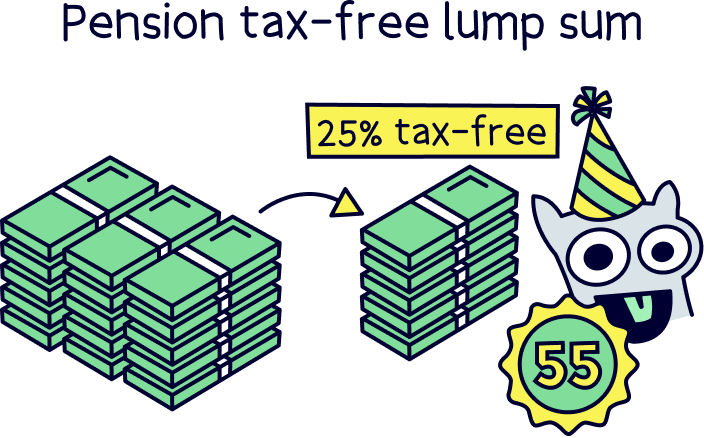

Your money will also grow tax-free too, just like an ISA. However, you will have to pay tax when you start withdrawing it later down the line, and you can only withdraw once you're 55, although ideally you’d keep saving until you officially retire (or need the money).

The first 25% of your pension is completely tax-free, and you can take this as a tax-free lump sum if you like. The remaining 75% counts as income, and you’ll pay Income Tax on it – although how much you pay depends on how much your income actually is at the time.

Nuts About Money tip: Confused? It’s often a good idea to chat to a financial advisor, here's where to learn more about financial advisors.

If you think a personal pension sounds like a good idea to you (and we agree), check out PensionBee¹ – their experts will handle everything and grow your money over time. Plus, they’ve got a great track record of growing money over time,, the fees are low too, and it’s super easy to use.

Or, if you want to make your own investments within a SIPP, check out the best and cheapest SIPP providers.

You could also check out all your options for both expert-managed and self-managed pensions with our comparison table of the best pension providers.

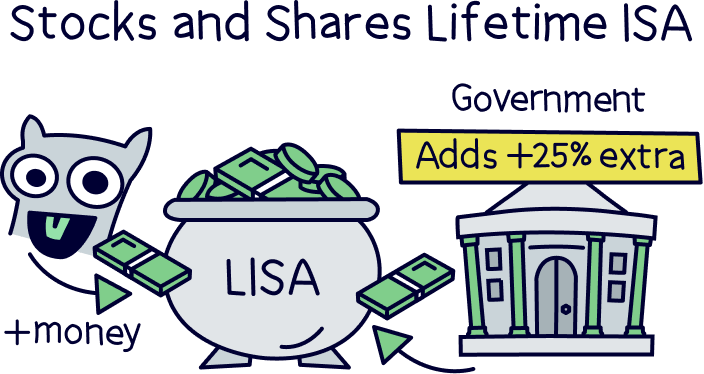

If you’re saving for your first home, you’ve also got the option of saving within a Stocks and Shares Lifetime ISA.

This is where you can save up to £4,000 per year, and get a 25% bonus on your contributions!

You can either choose to let the experts handle things, or make your own investments with a self-select platform.

You’ll only be able to use it to buy your first home however, otherwise you’ll have to wait until you’re 60 to withdraw the cash without facing a large fee – 25% of your total (which works out as more than the free contributions you get, not fair right?!)

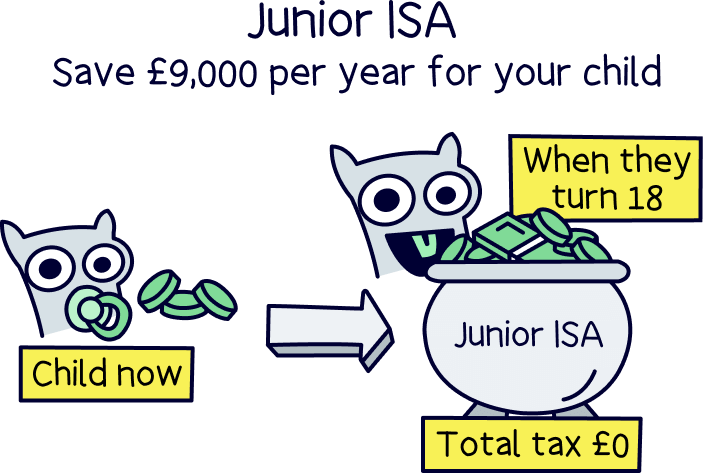

If you’ve got kids, you can also save for them tax-free, all in their name, and build a nice big savings pot for when they turn 18 – at which point they’ll be able to access it.

You can save and invest up to £9,000 per year (per child), which is separate to your own annual ISA allowance.

Not sure what one to use? Here's the best Stocks and Shares Junior ISAs.

Trading 212¹ and InvestEngine¹ have the lowest fees. In fact, there’s almost no fees at all. There’s no annual management fee (a fee to hold investments, also called a platform fee) or any share dealing fees (fees to buy investments).

InvestEngine is completely free. However, you can only buy ETFs (exchange-traded funds) – more on those below.

And with Trading 212, you’ll only pay a currency conversion fee, which is a fee to buy foreign stocks, such as in US Dollars (e.g. Amazon shares). And even then, it’s only 0.15% (very low).

You’ll still pay fees on investment funds if you buy them, which is a fee that goes to the fund manager (the experts managing the fund), also called a fund management fee. The exact amount will depend on which investments you buy. (We’ll cover investment funds below.)

With a self-select ISA, you’ve got a wide range of investment options to choose from, the main types are:

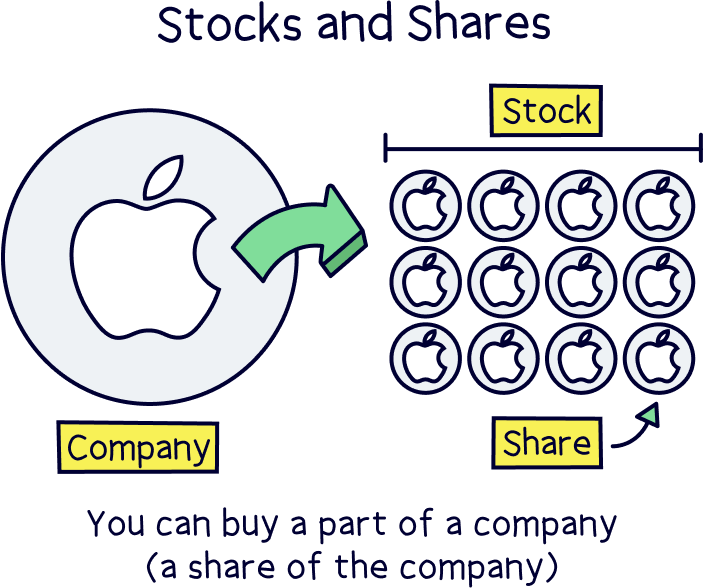

These are where you own part of a company, a ‘share’ of a company. Shares are bought and sold on stock exchanges (stock markets) all across the world, for instance the London Stock Exchange (LSE) in the UK.

All the shares combined add up to the total value of a company (it’s market capitalisation), and this can change over time depending on how the business performs, and the stock market in general.

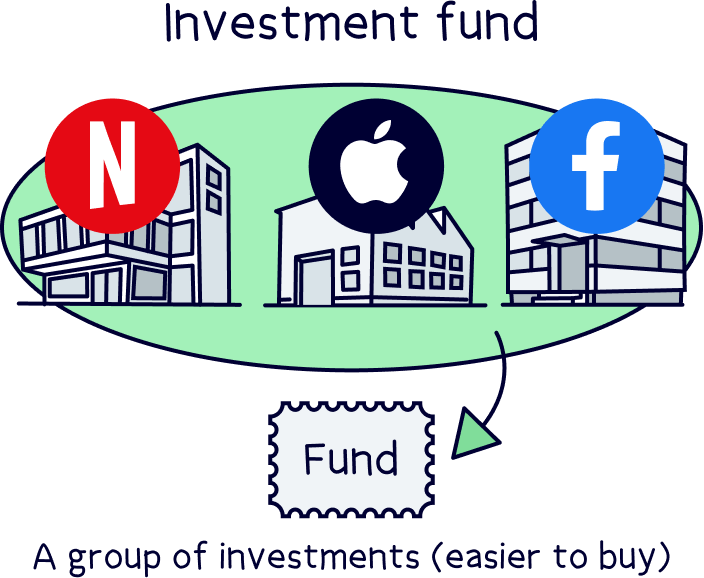

Investment funds, often known as mutual funds, are a collection of lots of different investments all pooled together into a single investment. For instance, the top 100 companies in the UK (the FTSE 100), or companies in the clean energy industry, or financial technology.

Lots of investment funds can also be bought and sold on stock exchanges too, just like shares, and these are called exchange-traded funds, or ETFs. And they’re super popular!

They make building an investment portfolio much cheaper and easier, as you only need to buy an ETF, or investment fund, rather than all the individual shares themselves. If you want to invest in ETFs check out our recommended ETF platforms.

Bonds are where you loan your money to governments or large corporations (corporate bonds), in exchange for interest payments. They’re typically seen as lower risk than stocks and shares.

Property can also feature in investment funds, and typically commercial property, such as offices and shops. This normally generates income from rent.

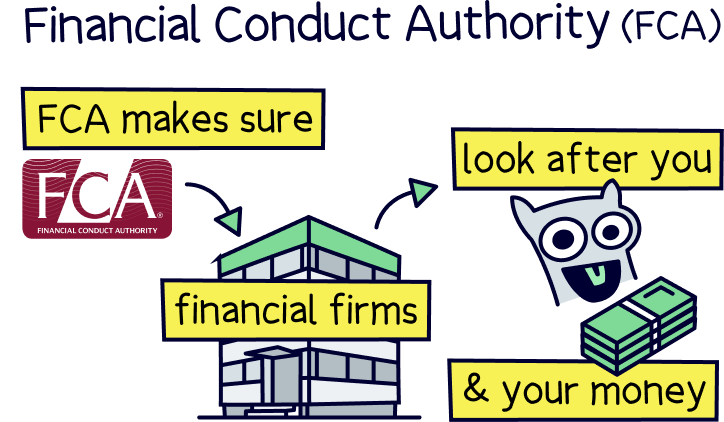

Yep. All ISAs are perfectly safe to save and invest. ISA providers are regulated and authorised by the Financial Conduct Authority (FCA), they’re the people who make sure your money is well looked after by the ISA providers.

If you’re not sure if a financial firm is authorised by the FCA, check the FCA register.

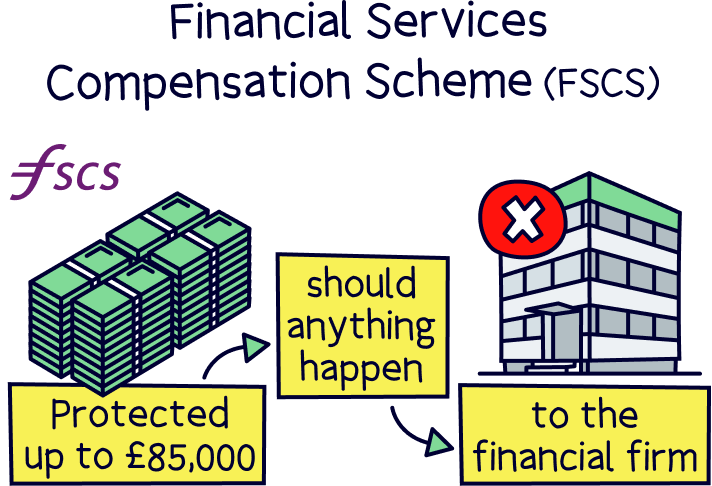

This also means that your money is protected by the Financial Services Compensation Scheme (FSCS). And gives you protection up to £85,000 should anything happen to the ISA provider (such as going out of business).

However, your investments are typically held with separate large banks, all in your name, and can only be returned to you.

This doesn’t mean you can’t lose money if your investments go down in value. Although using a sensible long-term investment strategy should typically work out well over time.

Hopefully this all makes sense with self-select ISAs. They’re Stocks and Shares ISAs where you make all the investments – so you decide which investments to make and which investment strategy to use. Scroll up to see the best self-select Stocks and Shares ISAs.

We only recommend them for experienced investors. Often, it’s simply better to let the experts handle things with an expert-managed ISA – they’ll grow your money using sensible, tried and tested investment strategies for long-term growth. It couldn’t be easier! Scroll up to see the best self-select ISAs managed by experts.

And that’s all there is to it – we hope this has helped!

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible