Article contents

If you’ve paid enough National Insurance throughout your working life, you’ll be able to start claiming your State Pension when you reach State Pension age. That’s currently 66, but it’s gradually increasing to 68.

The State Pension is a weekly payment you can get from the government when you reach a certain age. Kerching! So, we bet you can’t wait to start claiming it!

But when exactly can you start getting your State Pension? Here’s the full lowdown.

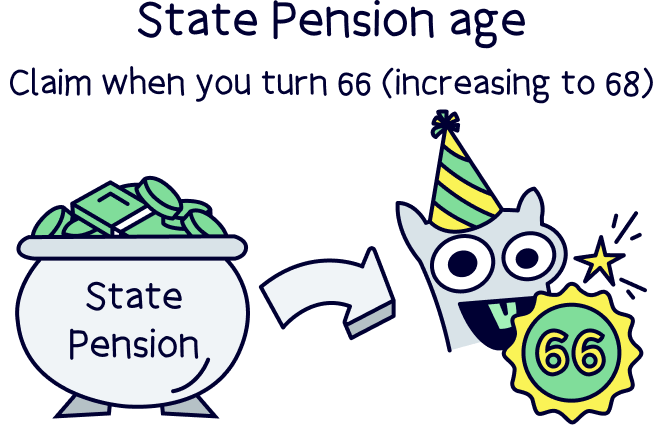

You can start getting the State Pension once you reach something called ‘State Pension age.’

If you’re thinking ‘Huh? What’s that?’ then we don’t blame you – it can be tricky to keep track because it keeps changing! At the moment, State Pension age is 66. However, it’s gradually increasing to 68.

That means if you’re reaching State Pension age now, you’ll be able to start claiming your State Pension at the age of 66. Woohoo! But if you were born after the 5th of April 1960, you’ll need to wait a little longer. Doh!

You can check when you’ll reach State Pension age using the government’s handy State Pension age checker.

However to claim the State Pension, you’ll need to have made enough National Insurance contributions over the years. At least 10 years worth on your National Insurance record, and to get the full amount you’ll need 35 years.

Here’s where to check your National Insurance record for how many years you’ve paid National Insurance contributions (you’ll need your National Insurance number).

Find the best personal pension for you – you could be £1,000s better off.

It’s important not to confuse State Pension age with retirement age.

In the UK, there isn’t a set age that you have to retire anymore. So that means you can technically retire whenever you want, as long as you have the finances to do so!

If you want to retire before you hit State Pension age, you can. However, you won’t be able to start claiming the State Pension early. Boo!

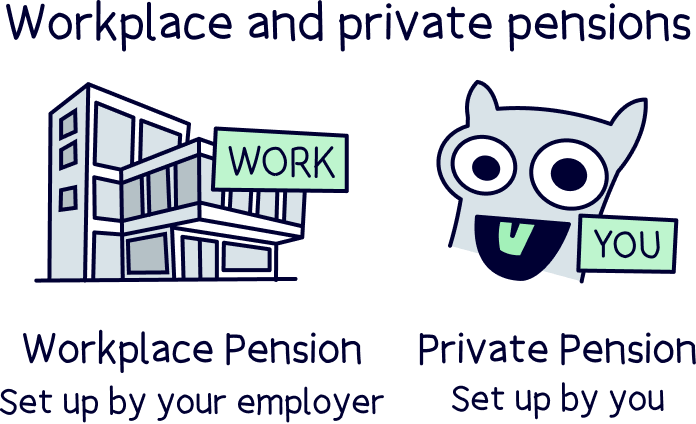

Instead, you’ll need to find another way of supporting yourself financially until you reach State Pension age – like with the help of a workplace pension (a pension your employer sets up for you) or a personal pension (one you set up yourself).

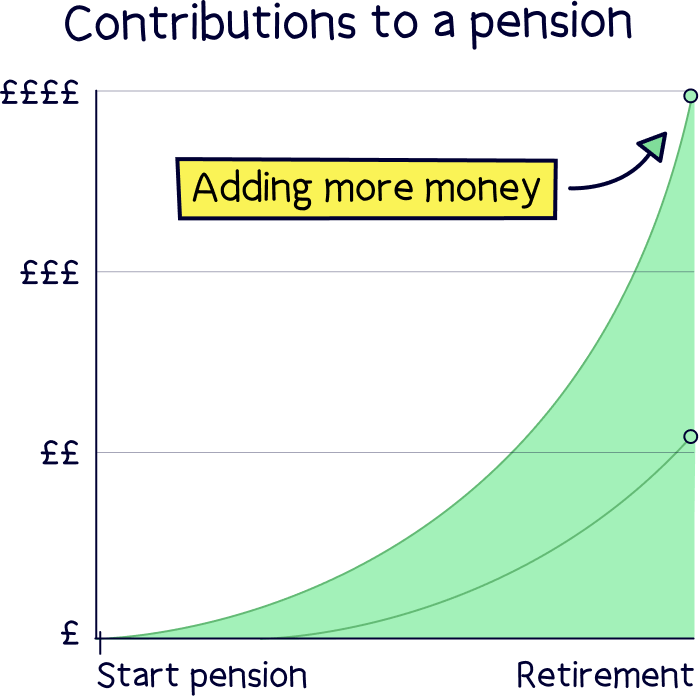

These work a bit like a piggybank – you pay into them throughout your working life, and when you reach a certain age, you can start taking an income from them. Except they’re even better than piggybanks, because your money will grow while it’s sat in your pension pot, without you having to do a thing! And there’s this super awesome thing called tax relief, which means you don’t have to pay any tax on the earnings you put into your pension. Get in!

Anyway, you can normally start taking money from workplace and personal pensions when you turn 55 (although the government has proposed changing this to 57 from 2028). This makes them a great shout if you’re keen to retire early – but they’re also great for boosting your income alongside your State Pension when the time comes.

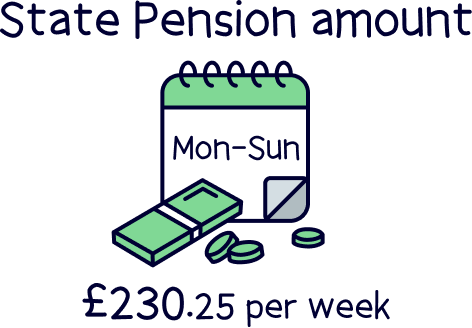

The full new State Pension (the maximum you can get) is just £230.25 per week, which comes to £11,973 per year. So, while it’s nice to have, it’s not a lot to live on if you’re relying on that alone! By starting a pension, you can top up your State Pension income to make sure you can live a comfortable life in your sunset years.

If you’re not sure how to start a pension, check out our review for PensionBee, they're one of our favourite pension providers (companies that can give you a pension and look after it for you). They make it really easy to start a pension and save for retirement as they both have handy mobile apps on Apple and Android that let you quickly add money and watch it grow. Plus, their customer service is great and the fees are pretty low too!

Yep! Contrary to what you might think, you don’t have to retire in order to start claiming the State Pension. Instead, you can carry on working and get the State Pension at the same time!

Remember how we said that the maximum State Pension you can get comes to just £9,628 per year? Well, a lot of people would struggle to live on that alone. That means part-time work can be a really useful way to top up your State Pension and give you the cash you need to really make the most of your sunset years (cruises around the Caribbean anyone?!).

If you want, you can even carry on working full-time while you’re claiming the State Pension. There’s nothing stopping you!

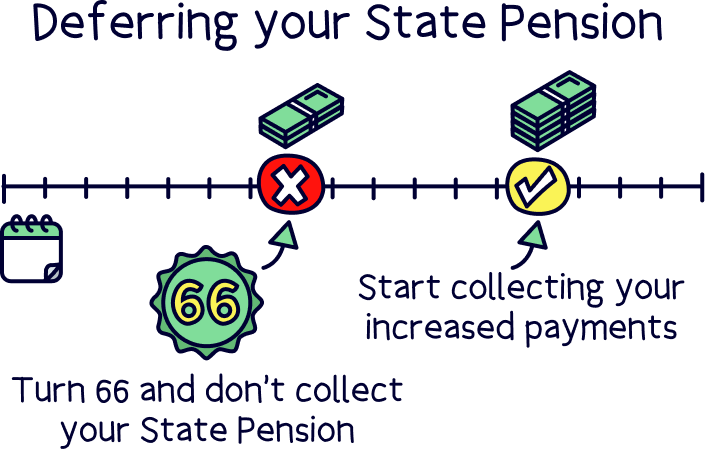

Here’s something you might not know about: you don’t actually have to start taking the State Pension once you hit State Pension age. You can choose to delay taking it instead, known as deferring it.

We know what you’re thinking: ‘Why would I want to delay getting a lovely weekly payment from the government?’

Well, because as long as you delay taking it for at least 9 weeks, your State Pension will increase for every week you defer it. Exactly how much it increases by will depend on lots of different things, like how long you defer it for and when you reach State Pension age.

So, should you defer your State Pension?

Well, if you reach State Pension age and find you don’t really need those weekly payments, then deferring it for a while could be a good idea. That way, you’ll get more when you eventually do start taking it.

Just make sure that you don’t put off taking it for too many years. After all, you want to make sure you have a chance to enjoy your State Pension before you pop your clogs (sorry to put a downer on things!). Check out our article on what happens to your pension when you die to learn more.

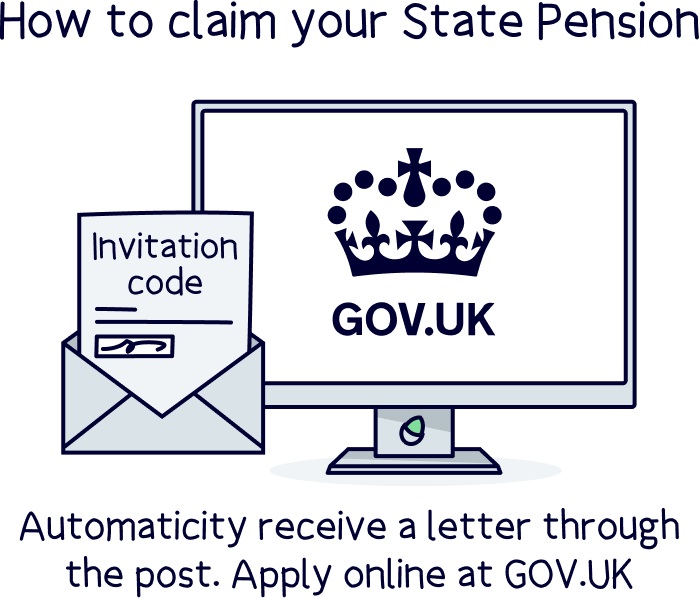

Okay, listen up. You won’t just get given the State Pension automatically once you reach State Pension age. Instead, you have to claim your State Pension. In other words, you need to tell the government that you want to start receiving it.

Don’t worry, it’s really easy!

When you’re a couple of months off from turning State Pension age, you should get a letter telling you what to do if you want to claim your State Pension. The quickest and easiest way is to apply for it on the GOV.UK website. You just need:

If you don’t get a letter, don’t panic! You can still claim your State Pension. You’ll just need to request an invitation code on the GOV.UK website.

Unless you’ve deferred your State Pension, you’ll normally get the first payment into your account less than 5 weeks after you’ve reached State Pension age, and every 4 weeks after that. Nice!

Getting super excited about claiming that juicy State Pension? Hold your horses for just a moment. You’ll only actually be able to claim the State Pension if you qualify for it.

Let’s rewind for a second.

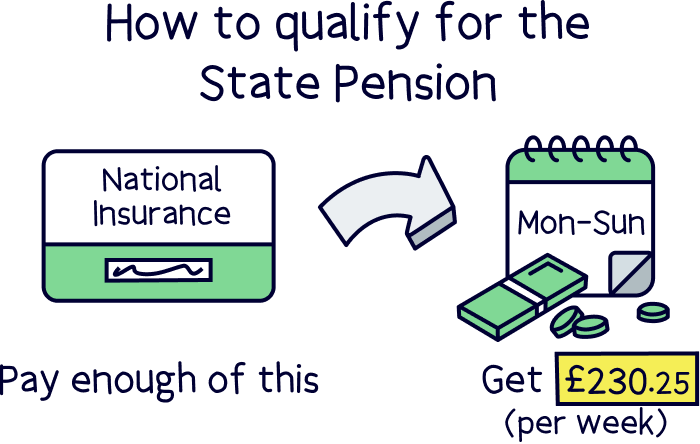

To qualify for the State Pension, you need to make enough National Insurance payments throughout your working life (National Insurance is a charge you pay to the government alongside your taxes to cover things like healthcare).

You’ll need to have paid National Insurance for at least 10 years to get any State Pension at all. But to get the full State Pension (that £230.25 per week we were telling you about), you’ll need to pay National Insurance for at least 35 years.

Now, the chances are you’ll qualify automatically, as most people have to pay National Insurance. However, if you earn very little, you may not need to pay it – which might sound great until you realise that this could mean no State Pension for you. Eek!

Here’s the deal…

Just bear in mind that these thresholds can change from year to year – these are for the year 2022-2023, but you can keep an eye on the most National Insurance earning thresholds on the GOV.UK website.

Anyway, if you’re earning less than £123 per week and you’re worried about not qualifying for the State Pension, don’t worry! There is a way round it. You can make voluntary National Insurance contributions, meaning you can voluntarily pay National Insurance even though you don’t have to.

We know, we know, nobody likes paying for things unnecessarily – but if you can afford to, it could be a really good idea so you can unlock those nice weekly payments later on in life. Your older self will thank you!

To find out whether you’re on track to qualify for the State Pension, you can use the government’s handy State Pension forecast tool. This will show you how many qualifying years you have under your belt so far.

If it turns out you’re a little short on qualifying years, don’t stress. If you can afford to, you can normally make voluntary National Insurance contributions for the past 6 years to make up the numbers. That way, you can make sure you’re still getting that cash coming into your pocket from the government when you’re old and grey!

Not happy with just the State Pension? Neither are we! £230.25 per week is pretty hard to live on. It’s good to have, but it’s not going to cover all those cruises!

Apart from deferring your State Pension, you have lots of options when it comes to saving more for retirement. If you are employed, you should have a workplace pension set up as part of the auto enrolment scheme.

A workplace pension is where at least 5% of your salary will be taken automatically from your salary, and put into a workplace pension scheme. And, your employer will add at least 3% too (by law).

You can also set up your own pension, called a personal pension (a personal pension and workplace pension are both types of private pensions. The government pension is a public pension).

With a personal pension, you can save in addition to the State Pension, and a workplace pension. It’s a pension you manage and you decide how much you want to save.

Well, we say manage, you can simply let the experts handle everything! You just pick which personal pension provider you’d like, and let them handle the rest. Here’s where to find the best personal pensions.

If you do want to manage your investments, you can do this with a self-invested personal pension (SIPPs). We’ve got the best self-invested personal pensions too.

First, the good news: as long as you qualify for the State Pension, you’ll be able to get that lovely weekly payment landing in your pocket once you reach State Pension age without having to do a whole lot. All you have to do is fill out a few details and voila! You’ll normally get your first payment just a few weeks after reaching State Pension age.

Now for the less good news. Even if you qualify for the full State Pension, it’s still not an awful lot of money. So, you might struggle to live on the State Pension alone.

To help tide you over in retirement, we’d always recommend making sure you have another source of income alongside the State Pension – like a personal pension. That way, you can take control of your savings and make sure you have the cash you need to live your golden years to the full!

If starting a pension sounds like your cup of tea, you’ll love our favourite pension provider, PensionBee. They have a super easy-to-use mobile app on Apple and Android, where you can quickly add money and watch it grow. Plus, their fees are pretty low and their customer service is top-notch too!

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.