Article contents

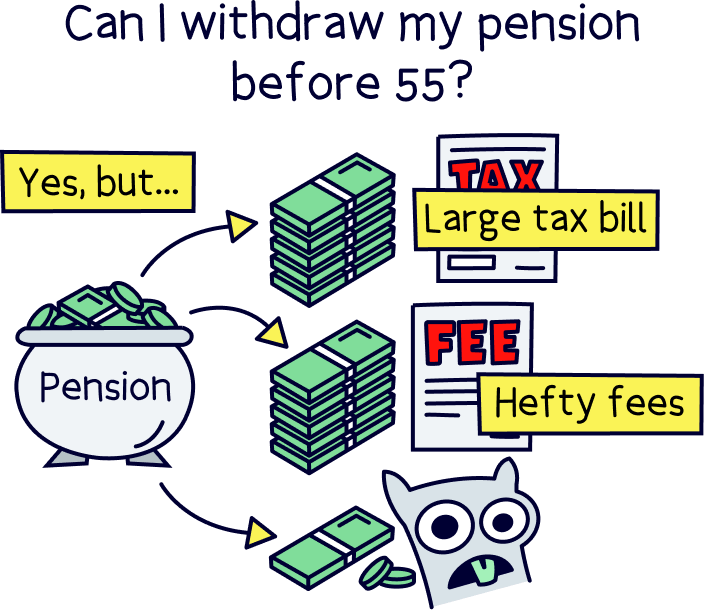

Yes… but it’s normally a very bad idea. You’ll usually be charged a massive amount of tax! The exception is if you meet very specific criteria, like being seriously ill or expected to live for less than a year.

Wondering if you can dip into your pension before you hit 55? We don’t blame you – if you’ve been squirrelling money away into your pension ready for retirement, it can be hard to see it all sitting there without being able to touch it. Especially if you’re short on cash!

Most pension providers won’t let you take money from your pension until you’re at least 55 (your pension provider is the company that gives you your pension and looks after it for you). But there’s nothing legally stopping you from withdrawing your pension before then... it’s just that it’s normally a very bad idea! Here’s the full lowdown on early pension withdrawal.

Normally, you can start taking money from your pension when you turn 55 (although the government has proposed changing this to 57 from 2028). This applies to both personal pensions (pensions that you set up yourself) and workplace pensions (pensions that your employer sets up for you).

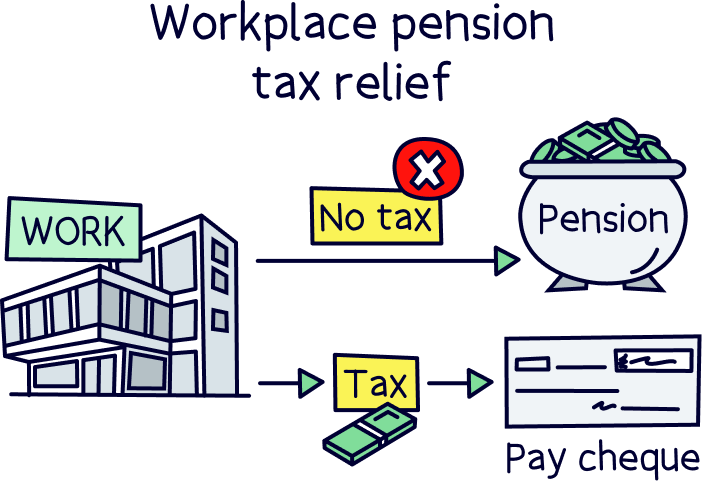

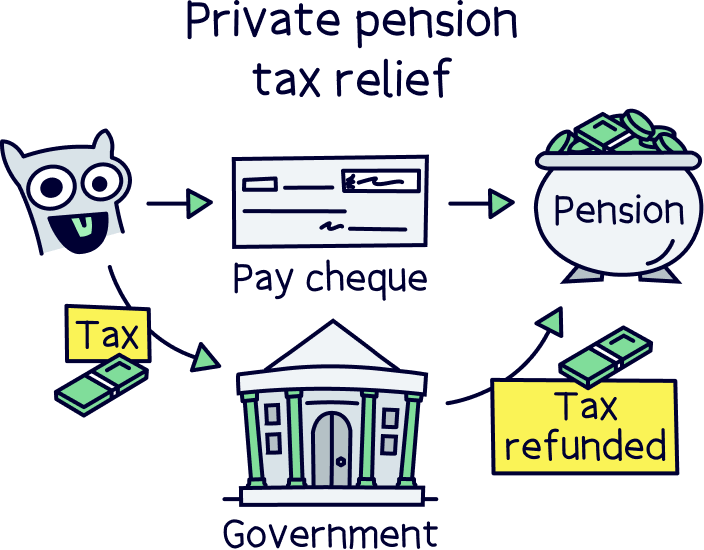

In the UK, saving into these pensions comes with amazing tax benefits. Basically, the government wants to encourage you to save up for retirement so they’re not left propping you up when you’re old and grey. That means you won’t have to pay any tax on the money you put into your pension pot, known as tax relief. Kerching!

Tax relief can work in one of two ways.

So, why exactly are we telling you this (apart from the fact that it’s obviously good news if you’ve been squirrelling money away over your working life!)? Well, the tax benefits come with a very specific condition – that you can’t access the money you’ve paid into your pension until you’re at least 55.

That means if you withdraw your money early, you’ll normally lose your tax benefits and will therefore get charged a huge amount of tax. And we mean HUGE! Which brings us onto…

Find the best personal pension for you – you could be £1,000s better off.

Unless you meet very specific criteria (which we’ll look at later), withdrawing money from your pension will land you with a hefty tax bill. You could be taxed as much as 55% on the money you take out!

Because of this, it’s not normally wise to withdraw your pension early. And because of that, most reputable pension providers won’t let you do early withdrawal. We should thank them really!

That said, it’s not against the law to take money from your pension early. So, if you really want to, you can.

If you want to do this, it's probably a good idea to chat to a financial advisor first. Check out Unbiased¹ to find a great one for you.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

As your pension provider likely won’t let you, you’ll probably have to withdraw money from your pension through another company. In other words, you’ll have to transfer your pension to a different pension provider who’ll let you withdraw it early.

It might sound simple, but there are a couple of catches.

First, they’ll normally charge you a lot of money. That’s right, as well as having to foot the hefty tax bill, you’ll also have to pay a fee to the company you’ve used to withdraw your pension – this can be as high as 30%! That means you could end up getting as little as 15% of your pension in your pocket!

On top of that, most pension providers who’ll help you to withdraw your pension early won’t be regulated by the Financial Conduct Authority (that’s an organisation in the UK that makes sure financial services are behaving well and protects consumers). So, it’ll be harder to tell if the company is genuine, and you won’t have any protection if something goes wrong. Not ideal!

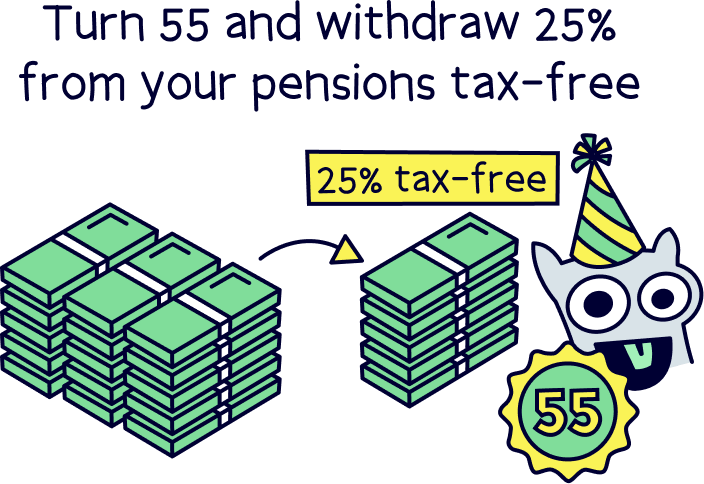

In contrast, if you wait until you’re at least 55 before withdrawing money from your pension, you’ll be able to withdraw the first 25% tax-free – getting the maximum amount of the cash you’ve carefully saved in your own pocket. Some things are just worth waiting for!

Now, before we put you off early pension withdrawals completely, there are a few scenarios where you can take money from your pension early, without having to worry about all those hefty taxes and fees. Here’s when taking money from your pension before 55 might be okay:

Think you might be able to start taking your pension early? Before you do, make sure to check in with your pension provider to make absolutely sure. You don’t want to be faced with an unexpected tax bill after!

Have you been unexpectedly offered the chance to take your pension early? Then you might be on cloud nine right now! However, hold your horses – the chances are it’s a scam.

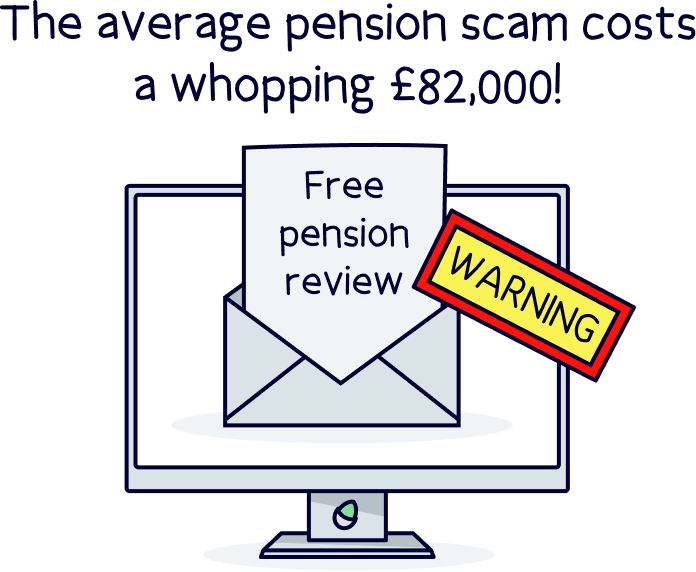

Yep, we hate to break it to you, but there are some nasty scammers out there doing their best to get in on your pension funds. And according to the Financial Conduct Authority, the average pension scam victim loses a whopping £82,000!

Pension scams are all different, but most start with a ‘free pension review.’ It’s clever really – who doesn’t like free things?!

After this, you’ll normally be told that a number of schemes would benefit you. This is where they might tell you that you can take your pension early (normally not true!). They might also tell you that you can access more of your pension tax-free than what the law allows, or that they can grow your money much more quickly than your current pension provider can. Again, likely untrue!

Pension scams are really scary because if you fall for them and move your pension to a scammer, you could lose all the money you’ve saved up for retirement!

Even if the company that’s contacted you can genuinely help you to get your money out from your pension early, it’s still best to be wary. Remember, not only could you be hit with a massive 55% tax bill, but the company will normally charge you through the roof too – sometimes as much as 30%, meaning very little of your money will actually end up in your pocket. And they normally won’t be regulated by the Financial Conduct Authority either, so you won’t be protected if something goes wrong.

Ultimately, unless you meet the very specific criteria we’ve listed above or you’ve heard that you can take your funds directly from your own pension provider, we’d recommend not trusting any third parties who get in touch about your pension. It’s better to be safe than sorry!

If you’re not sure if you’re being scammed, you can contact the Financial Conduct Authority which should be able to help. Or, if you think you might have already been the victim of a pension scam, call your pension provider straight away. They might be able to stop the transfer in time!

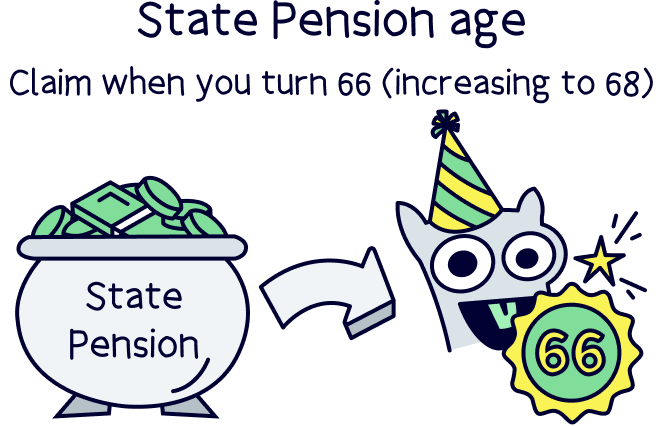

We hate to be the bearers of bad news, but you can’t take your State Pension early. Sorry! In fact, you’ll have to wait a lot longer to claim your State Pension than you will to take an income from your other pensions – you can’t start claiming it until you hit State Pension age, which is currently 66 but gradually climbing to 68. Urgh!

Let’s rewind for a second. The State Pension is a weekly payment you can get from the government later on in life. You don’t have to put money into it yourself like you do with other pensions – instead, you’ll qualify for it if you make enough National Insurance payments throughout your working life (National Insurance is a payment you fork out alongside your taxes to cover things like healthcare).

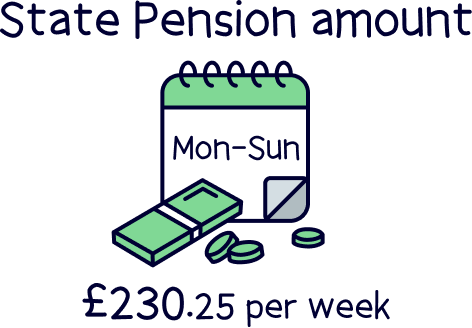

Normally, you’ll qualify for it automatically, as unless you earn very little, you have to pay National Insurance. The full State Pension (which you’ll get if you’ve paid National Insurance for at least 35 years) is £230.25 per week – which comes to £11,973 per year. That might be hard to live on by itself, but luckily you can take it on top of your other pensions (or on top of earning an income in other ways), so it’s a really nice extra!

If you don’t already have another source of income for retirement, we’d recommend starting a personal pension. That way, you can take control over saving for your sunset years and make the most of all those lovely tax benefits we told you about earlier. To get started, check out our top pension providers.

To summarise, you can legally withdraw your pension before 55 (unless we’re talking about your State Pension, in which case you can’t start claiming it until you reach State Pension age, which is currently 66!). But that doesn’t mean it’s a good idea!

Unless you’re seriously ill, have been given less than a year to live or have a very special pension designed for certain professions (like elite footballers), taking your pension early will see you get hit with a massive tax bill and hefty fees. And that will leave very little of your pension left for you to enjoy!

On the other hand, waiting until you’re 55 means you’ll get to actually enjoy all that cash you’ve worked so hard to squirrel away. You can even take the first 25% tax-free!

All this means it’s super important to think carefully about how much you can realistically afford to pay into your pension during your working life. Of course, the more you pay in, the more financially secure you’ll be in your sunset years. But at the same time, be careful not to overstretch yourself – you don’t want to find yourself in a position where you need that cash you’ve stashed away before you’re 55! Read our guide to starting a pension to learn more.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.