These categories are explained below.

PensionBee makes pensions simple – they'll handle everything for you. They're highly rated, easy to use and have low fees.

Find and combine lost pensions into one with Beach. It's an easy to use mobile app. Get started in minutes.

Let the experts do all the work – sit back, relax and watch your pension grow.

Get £50 added to your pension

T&Cs apply. Capital at risk.

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Best for: those looking for an easy to use, low cost pension with great investment performance

• Easy to use

• Easy to understand pension plans

• They'll find all your pensions and move them over (consolidate)

• Low fees

• Great customer service

• Great if you’re self-employed (or a company director)

• Socially responsible investment option

• Minimum deposit: £1

• No financial advice, but can explain your options

T&Cs apply. Capital at risk.

Moneyfarm is one of the best options out there for saving and investing. It's super easy to use – the experts simply take care of everything. And, they're on hand to help you with guidance and any questions too.

They have one of the top performing investment records, and great socially responsible investing options. The fees are low, and reduce as you save more. Plus, the customer service is outstanding. Overall, a fantastic option to save and invest.

Best for: those looking for an easy to use, low cost pension with great investment performance

• Easy to use

• Free personal investment advisor

• Offers an ISA and a pension

• Great track record for growing money

• Socially responsible options

• Have to invest at least £500

AJ Bell's Ready-made pension is a great option for those looking for an easy-to-understand option to save for retirement.

There are four easy-to-understand options to choose from, suited to slightly different retirement savers (these are explained when you get started). And that's it – their experts will look after your pension investments, aiming to grow them over time.

It's low cost overall, with investment fund options ranging from 0.45% to 0.60% (in addition to some extra fees).

They'll also find any lost pension you might have for free too – and transfer them to your new AJ Bell pension.

Best for: those looking for a well established provider with easy-to-understand options

• Well established

• Low cost overall

• Can find lost pensions and transfer them over

• Great customer service

• No financial advice

Take control of your pension – you decide which investments to make.

Offers available

Capital at risk. Terms & fees apply.

Interactive Investor is a well established company, and very popular.

Instead of paying a percentage of the investments in your account (like other investment companies), you’ll instead pay a fixed fee per month – and it’s pretty low, starting at just £5.99 per month for a pension (SIPP).

This makes it one of the cheapest SIPP providers out there, especially if you have a fairly sizable amount within your pension (e.g. over £30,000).

On top of that, there's a huge range of investment options (e.g. shares and funds) – one of the largest.

The customer service is excellent too.

A great choice overall.

Minimum deposit: £1

Best for: experienced investors with a growing portfolio (benefit from the flat fee)

• Flat monthly fee

• Great value for larger portfolios

• Huge range of investment options

• Great customer service

• No minimum investment

• No share dealing fee for regular investments

• Expensive for small portfolios

• Can be complicated to use

AJ Bell is a great traditional broker, with good customer service and solid reputation.

There’s a huge range of investment options.

AJ Bell is low cost – you'll pay a low annual charge and then fees per deal, which are £1.50 for funds and £5 for shares (online), which reduces to £3.50 if there were 10 deals or more in the previous per month.

Plus, there's a great phone app too.

Minimum deposit: £500 (or £25 per month)

Best for: experienced investors looking for a low cost, well established platform

• Well established

• Cheapest traditional broker

• Huge range of investment options

• Ready made pension portfolios

• Great customer service

• Low dealing fee for funds (£1.50)

• Can be complicated to use

Up to £1,500 cashback

T&Cs apply. Investment involves risk.

You can benefit from their award-winning customer service, trust, and integrity, while managing your own investments – and get professional financial advice and coaching if you’d like it.

On the platform, you’re able to manage your own investments within a regular investment account, a tax-free ISA, and a pension (SIPP). And there’s a Junior ISA if you’ve got kids.

There’s a wide range of investment options (over 12,500), including stocks and funds from various providers, and funds managed by Charles Stanley themselves.

The fees are reasonable overall, and depend on which investments you want to make. If you opt for Charles Stanley’s own funds, there’s no fees to use the platform (fees within the fund itself).

Best for: those looking for a well established platform with a focus on customer service

• Well established

• Award-winning customer service

• Good range of investment options

• ISA

• Pension (SIPP)

• Junior ISA

• Expert-managed options

• Get financial advice and coaching (separate service)

• Can be complicated to use initially

• No fractional shares

Free share up to £100

Capital at risk. Other charges may apply.

Freetrade is one of the most popular investment apps in the UK, with over 1.5 million customers!

The app itself is pretty awesome, and easy to use. There’s a wide range of investment options from across the world, and it’s commission-free (you’ll pay a monthly fee if you want an ISA or a pension).

Minimum deposit: £1

Best for: beginners and experienced investors looking for a great mobile investment app

• Commission-free

• Great mobile app

• Wide range of investment options

• Stocks and Shares ISA

• Pension

• No minimum investment

• Fractional shares

• ISA and pension aren’t free (monthly fee)

• Not multi-currency (e.g. can’t hold Euros)

• No phone support

Fidelity is a traditional investment company with a solid history and great service. SIPPs fees start at 0.35% per year (and reduce), and £7.50 per share trade – so average for costs. An okay range of investment options.

Minimum deposit: £800 (or £20 per month)

Best for: those looking for a well established platform with a focus on customer service

• Well established

• Offers financial advice

• Complicated to use

• Small range of investment options

• High share dealing fee (£7.50)

Vanguard is very cheap compared to traditional options, with an annual fee of just 0.15%, capped at £375 per year. You can only buy Vanguard funds however, so a limited range, but their funds are very popular. A good option for less active investors.

Minimum deposit: £500 (or £100 per month)

Best for: those looking for a low cost platform

• Well established

• Low cost

• Only offers Vanguard investment funds

Hargreaves Lansdown is a very traditional broker, and very expensive. A SIPP costs 0.45% per year, and £11.95 per trade. A good reputation and customer service but you're paying a lot for it.

Minimum deposit: £100 (or £25 per month).

Best for: those looking for a well established platform and wide range of investment options

• Huge range of investment options

• Well established

• Great customer support

• Complicated to use

• Expensive

• Very high share dealing fees (£11.95)

Pensions you can set up yourself and managed by experts - pay in directly, or through your business.

Get £50 added to your pension

T&Cs apply. Capital at risk.

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Best for: those looking for an easy to use, low cost pension with great investment performance

• Easy to use

• Easy to understand pension plans

• They'll find all your pensions and move them over (consolidate)

• Low fees

• Great customer service

• Great if you’re self-employed (or a company director)

• Socially responsible investment option

• Minimum deposit: £1

• No financial advice, but can explain your options

Up to £3,000 cashback

T&Cs apply. Capital at risk.

Moneyfarm is one of the best options out there for saving and investing. It's super easy to use – the experts simply take care of everything. And, they're on hand to help you with guidance and any questions too.

They have one of the top performing investment records, and great socially responsible investing options. The fees are low, and reduce as you save more. Plus, the customer service is outstanding. Overall, a fantastic option to save and invest.

Best for: those looking for an easy to use, low cost pension with great investment performance

• Easy to use

• Free personal investment advisor

• Offers an ISA and a pension

• Great track record for growing money

• Socially responsible options

• Have to invest at least £500

These pension providers are suited to most people – think of them like a pension from work, where you pick a specific pension plan (or a default plan), and the experts will manage your money and investments with the aim of growing it larger and larger over time.

These providers are where you make your own investments within a pension account, called a self-invested personal pension (SIPP).

You can typically pick from a wide range of investment options, such as investment funds and stocks and shares (more on those below).

These are typically only recommended for more experienced investors.

These providers are great for those self-employed, where you’re able to make contributions into your pension yourself (and still benefit from saving tax), and via a limited company if you run your business as one.

Our top picks are managed by experts, so your money is in a great place with the view to grow larger over time.

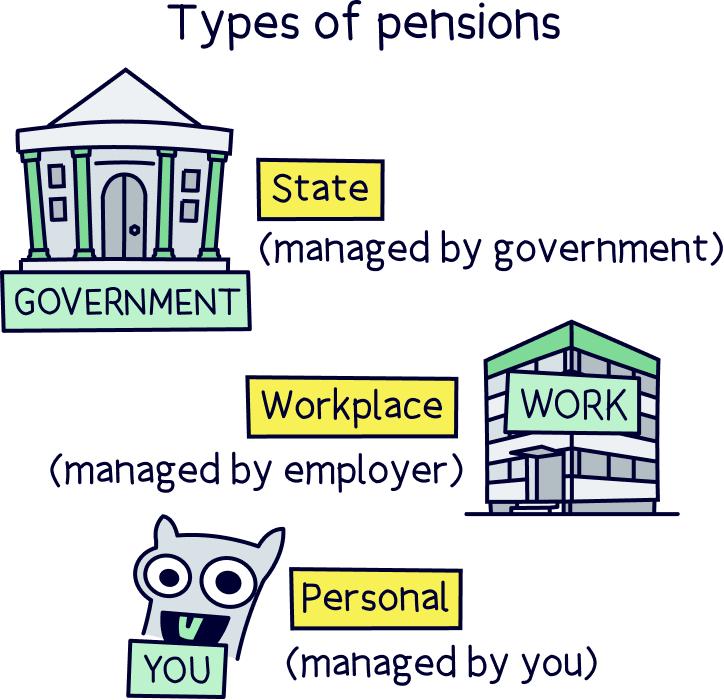

Our table is our top picks for personal pensions, which are ones you set up yourself (and pretty great all round), but there’s also two other main types of pension:

This is the pension from the government you’ll get when you reach 66 years old (but rising to 68 in future). You might struggle to live on just this. More on this below.

Set up by your employer. If you’re employed, you’ll probably have a workplace pension. More on this below too.

Saving for your future is super important, and if you haven’t started yet, start now! There’s loads of tax-free benefits too (all covered below).

Picking the right pension provider for you is super important too, and we know it’s all a bit confusing when it comes to pensions. That’s why we’ve researched a huge range of pension providers in the UK to narrow it down to the very best – including both expert-managed pension providers, and self-invested pension providers (SIPPs).

Here’s the criteria we used:

There’s a huge range of providers, but we’re just showing you the very best private pensions – ones that we recommend to our friends and family, and use ourselves here at Nuts About Money. Whichever pension provider you choose, you can be confident they’re one of the very best in the UK.

Interested in learning more? Here’s our full review methodology and how we test.

Nuts About Money tip: not sure how much to be saving? Learn more with our pension calculator.

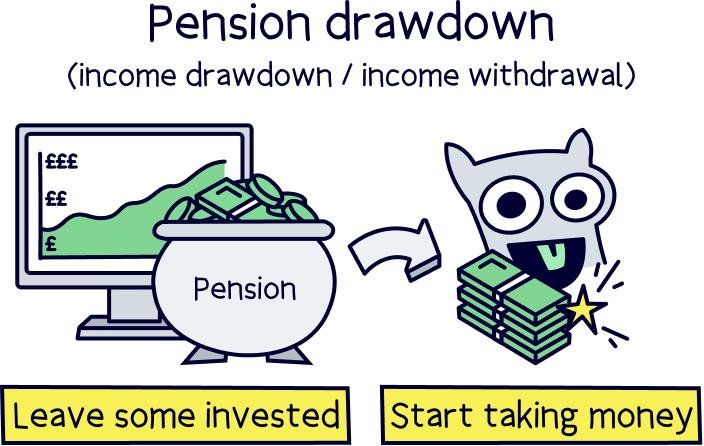

Getting ready to retire? Or just looking to withdraw cash from your pension? Switching to a pension drawdown provider could be a great option.

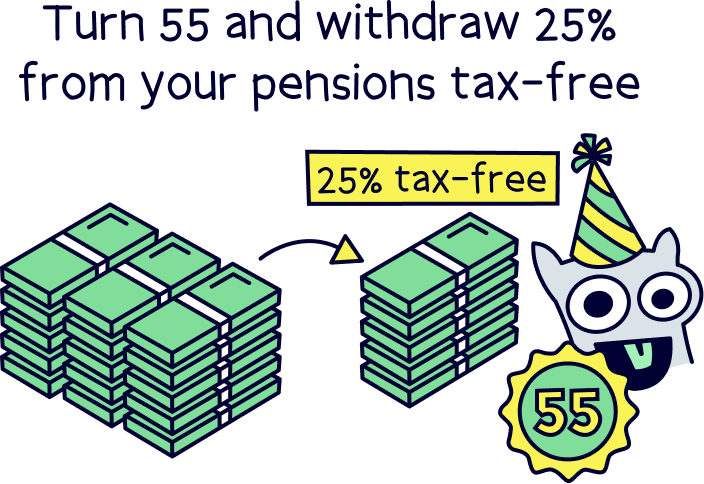

As long as you’re 55 (57 from 2028), you can start taking cash from your pension (if you want to), and you can take the first 25% of it completely tax-free, and as a lump sum if you want to.

Without boring you too much with the details about pension drawdown, we’ve put together the best pension drawdown providers – so if you’re keen to learn more, do check it out.

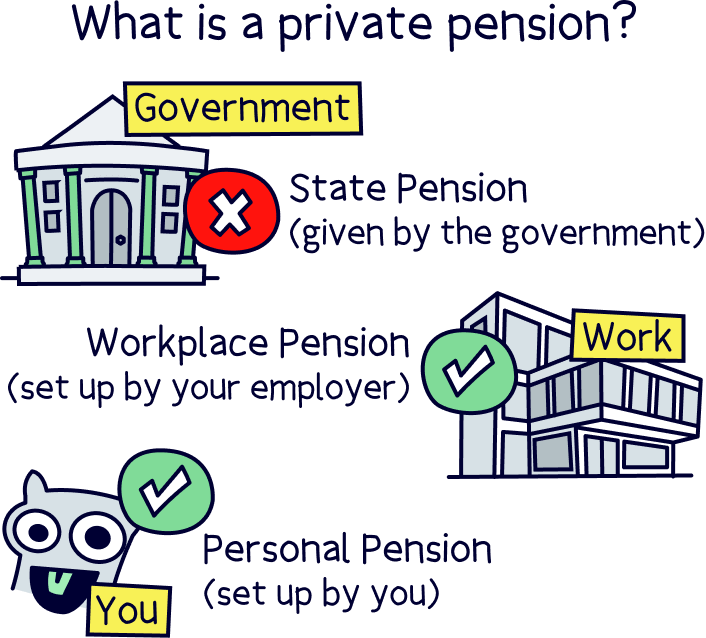

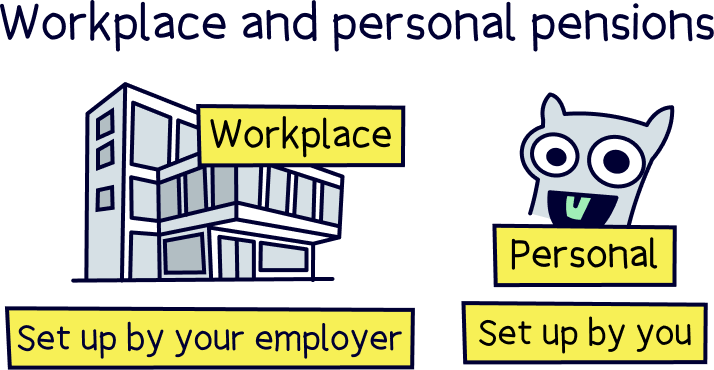

A personal pension is a pension set up by you, rather than the government (called the State Pension), or your employer (called a workplace pension).

It’s a pension that's all in your name, and it’s all your money. You decide who your pension is with and how much you put in.

It works similar to a pension you might have from your workplace, and technically a personal pension and a workplace pension are both types of private pensions. They’re all yours – and if you pass away, they’ll be passed onto your family (or next of kin).

Whereas the State Pension is a public pension, as it’s provided by the government (a public service), and if you pass away, it probably won’t be passed onto your family.

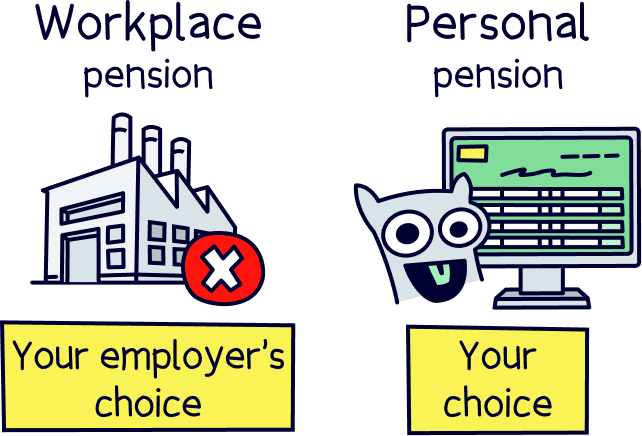

And with a personal pension, unlike a workplace pension, where your employer decides everything, you get full control over where and how your pension is managed. Don’t worry, it’s simple and you can let the experts handle everything, you just get the choice of which pension company you use, called a pension provider.

As you decide the provider, that means you can shop around for the best rates (lowest fees), and best investment performance (looking at previous performance). Or, you might like a provider with a great phone app, or expert advisors there if you need them. The choice is yours!

And if you’re more experienced, you can open a self-invested personal pension (SIPP), where you can make the investment decisions for yourself too, and buy and sell investments. Here’s the best SIPPs.

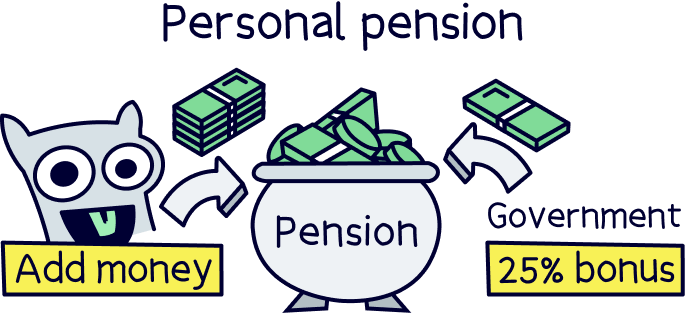

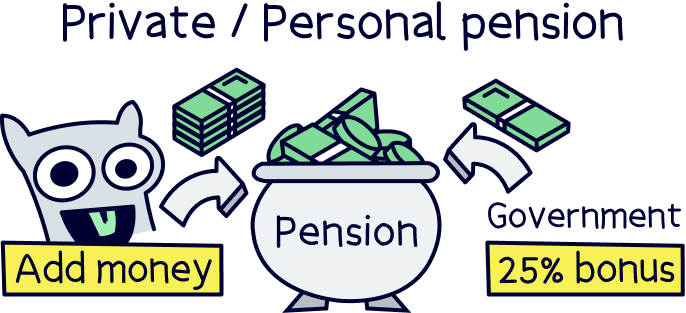

Best of all, with all pension pots, you’ll get a bonus from the government, which starts at 25% of what you put in. More on this below!

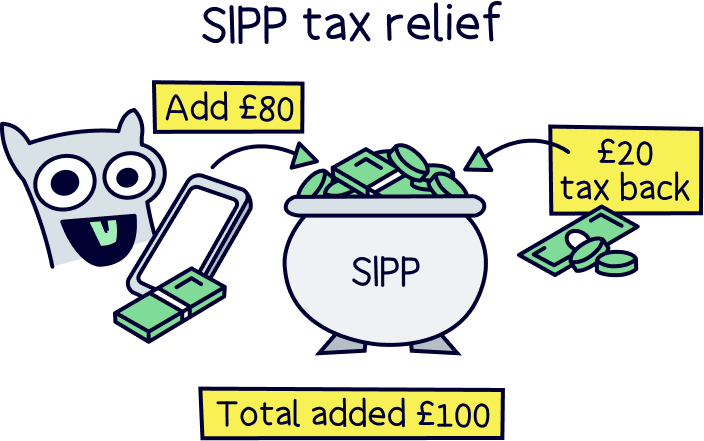

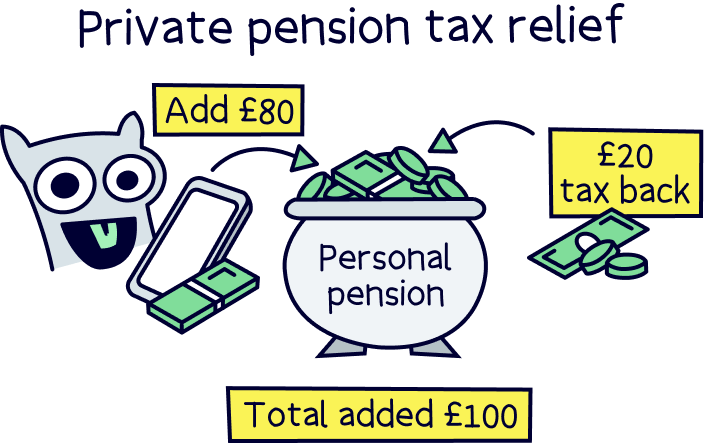

With a pension pot, you’ll get a bonus from the government – a massive 25% top-up on what you put in.

This top-up is intended to reimburse the amount of tax (basic rate tax) you’ve already paid – as paying into your pension is intended to be tax free. Technically it’s called tax relief.

Why tax free? Well, the government want people to save as much as they can for their retirement, as the state pension is probably not going to be enough for people to live on just by itself any more.

If you’re a higher rate tax payer (meaning you earn more than £50,270), you’ll actually get 40% back (but only on the amount you pay 40% tax on), and the same if you’re an additional rate taxpayer, getting 45% back. Winning!

With the 25% bonus, your pension provider (the company who is looking after your pension), will automatically claim this bonus from the government and add it on to your balance.

With higher rate (40%) and additional rate (45%) taxpayers, you’ll claim this each year as part of your Self Assessment tax return – which is an online form you can fill out after each tax year (which ends of April 5th every year), telling the government you’ve been paying into a personal pension and would like to claim your tax back (your pension bonus).

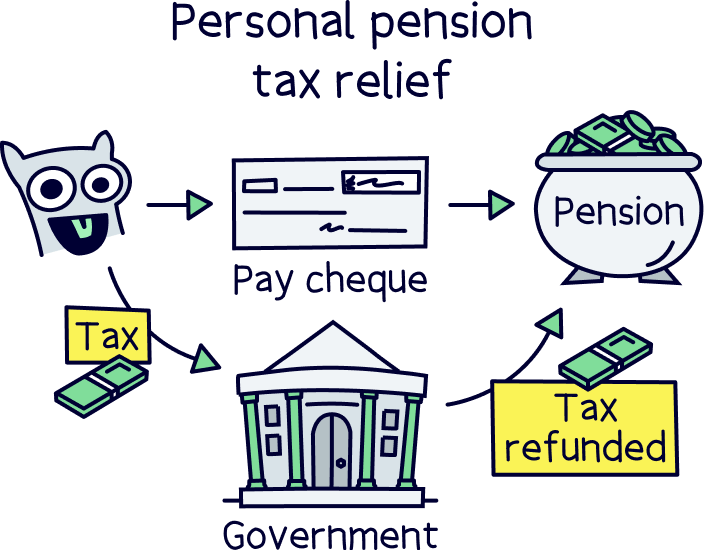

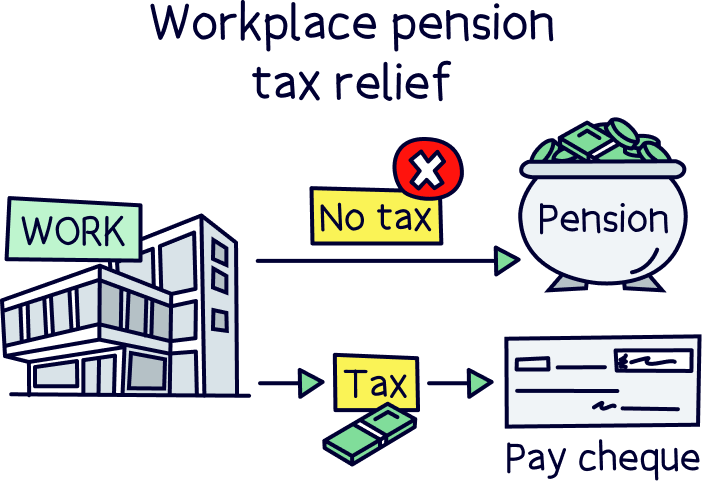

This is different to a workplace pension scheme (the pension set up by your employer). With a workplace pension, first, your money goes into your pension before you pay tax, then the tax is deducted from what is left over. So, you haven’t actually paid any tax on the money you’re paying into your pension. It’s all handled by your employer.

However, with a personal pension, you’re using money that you’ve already paid tax on (e.g. your salary after you’ve paid tax), and so you get the amount you’d paid in tax, back as a bonus.

It sounds confusing but it’s really quite simple, you just get your tax back on the amount you pay in!

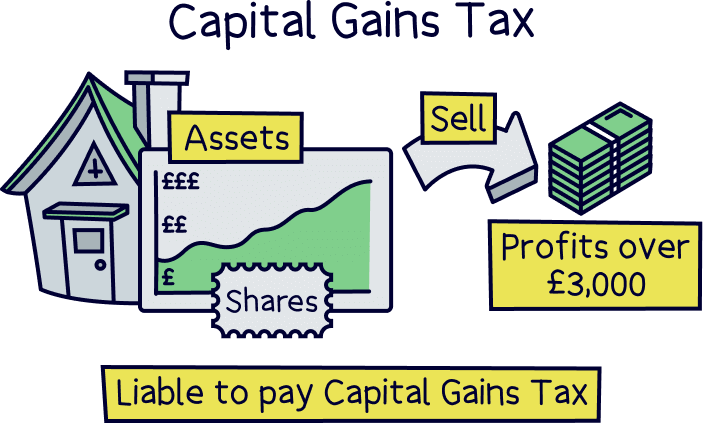

With the money within your pension pot – it’s effectively tax-free when it’s growing, meaning you won’t pay Capital Gains Tax, which is a tax you sometimes pay when your money has increased from assets growing in value – such as if you buy an investment and then sell it later and make a profit. This is great news as your money will grow much faster!

You will pay tax when you start withdrawing your money from your pension pot however. The first 25% is tax-free, and you can take this as a tax-free lump sum in one go when you reach 55 (57 in 2028), or if you take little bits here and there, you won’t pay tax on 25% of what you take out.

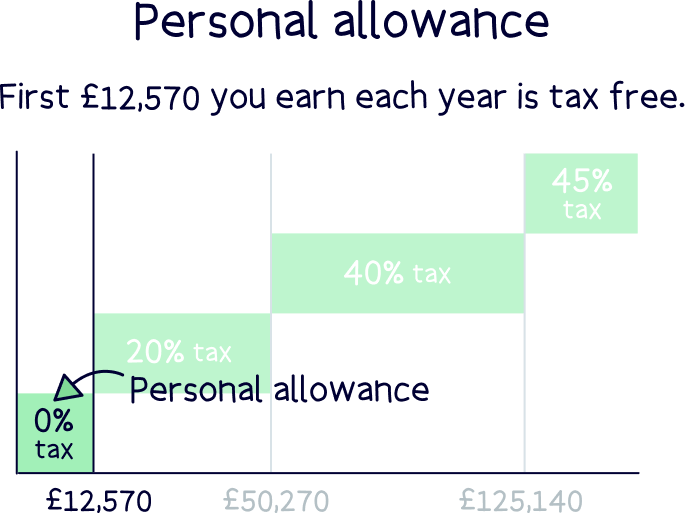

With the remaining 75% of your pension, you’ll pay income tax on it. So, that means if your yearly earnings are above the current tax personal allowance of £12,570 per year, you’ll pay 20% tax, and if your earnings are over £50,270 per year, you’ll pay 40% tax on the money above that (and 45% above £125,140).

So effectively it’s just the same as a job, but ideally you would have retired! And your pension could be the only income you have which could mean you’re not paying any tax at all later in life.

You can actually pay as much as you like into your private pension, however, there are limits on how much tax relief you can claim on your workplace pension and limits on the tax benefits on a personal one (i.e. the juicy 25% bonus from the government).

If you’re lucky enough to have lots of cash burning a hole in your pocket, you might want to pay as much as possible into your pension to benefit from the government bonus. But, there are limits on the amount you can pay into your pension and still claim the bonus (tax back). Which are:

These limits could change over time, and all the latest limits can be found on the gov.uk website.

A private pension is a pension that’s in your name, and that you contribute to yourself. For instance a workplace pension, that’s set up by your employer, but it’s all yours and you’ll contribute to it through your salary.

A personal pension is a type of private pension, it’s just like an employer pension (workplace pension), except you set it up yourself, and can move it around and contribute however much you like! It’s a great way to increase your retirement savings in addition to a workplace pension.

The State Pension is a bit different, this is the pension you’ll get from the government when you turn 66 (and 68 in the future). This is also called a public pension. You don’t have much control over it, and the government can make changes if they like. Whereas a private pension is more like a savings account, it’s all yours.

A workplace pension scheme is also a private pension, but it’s one your employer sets up and manages for you (if you are employed). If you’re self-employed, you’ll have to set up your own personal pension.

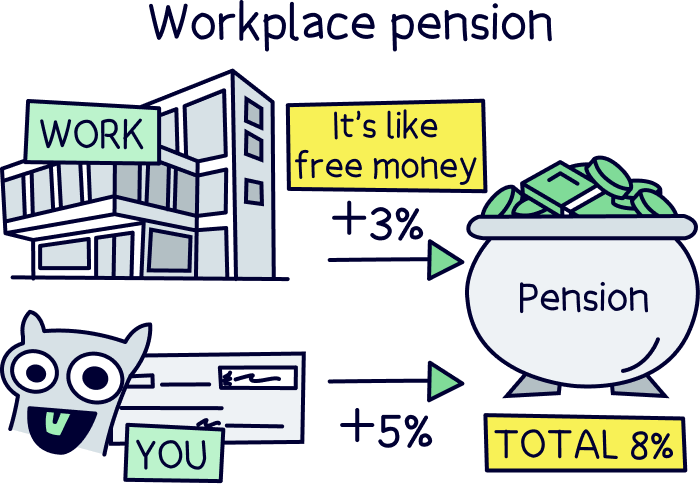

Anyway, with workplace pensions, your employer will almost definitely be part of the auto-enrolment scheme, which is where they have to set you up with a pension unless you opt out (it’s a government scheme).

And, this is where it gets good, they have to contribute to your pension too!

The standard contributions are, if you add 5% of your salary into your pension, your employer has to add at least 3% (by law), and sometimes they might add even more if you add more (called matched contributions). It’s basically free money!

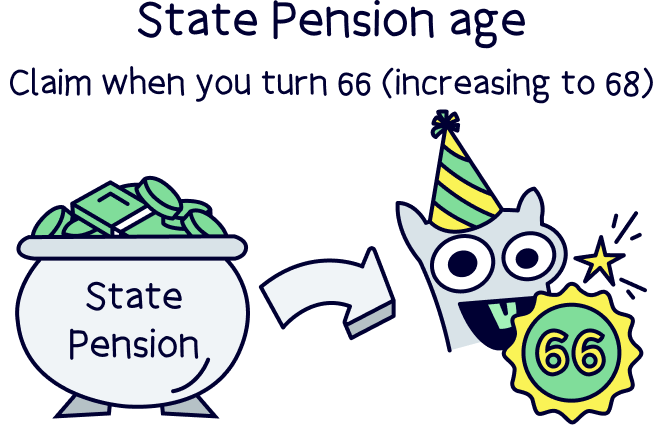

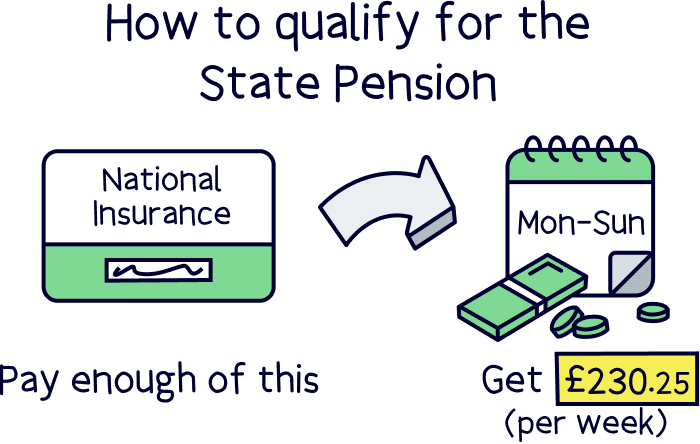

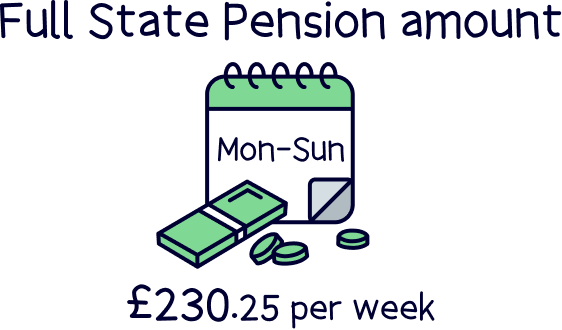

The State Pension (technically called the new State Pension), is what you’ll get from the government when you reach State Pension age, which is 66, but slowly increasing to 68.

However, to qualify, you’ll need to have made National Insurance contributions for at least 10 years, and to get the full amount, you’ll need to have made 35 years worth of contributions. These are recorded on your National Insurance record.

It’s currently £230.25 per week – so not a huge amount. That’s why we recommend making use of a workplace pension scheme if you have one, and a personal pension too – to increase your retirement savings as much as possible.

Both of these will boost your retirement income quite significantly when it comes to retirement, especially if you start your pension early!

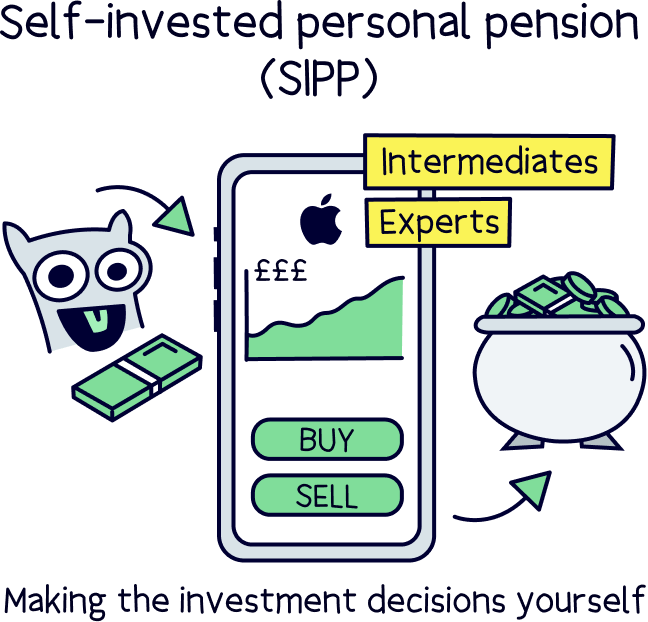

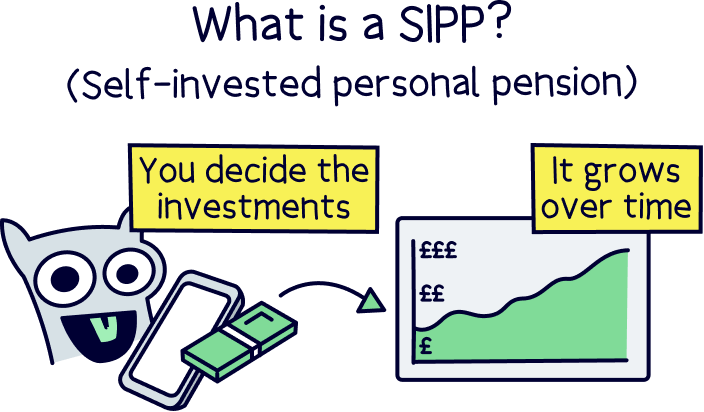

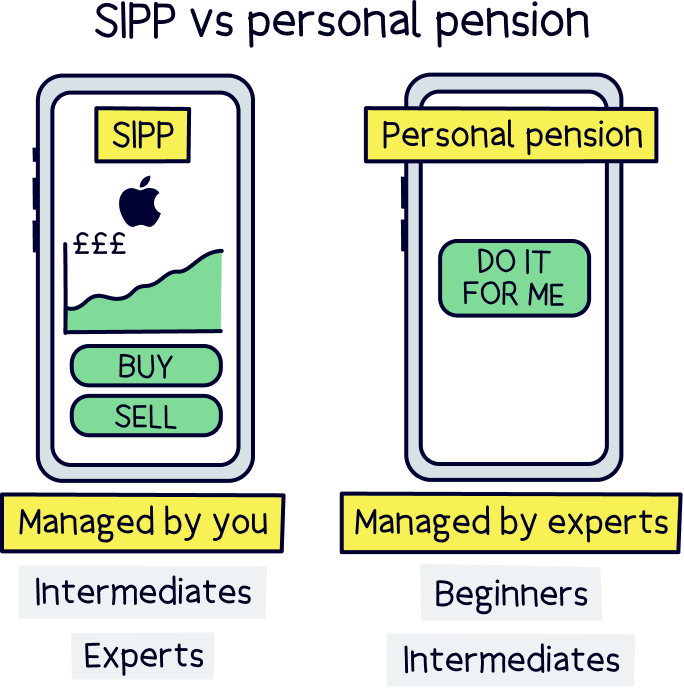

A self-invested personal pension (SIPP) is a pension you can easily set up yourself, and it gives you the ability to invest your money however you like.

So you could buy shares of a specific company, such as Google or Amazon, or you could invest in specific investment funds (groups of investments packaged together) that you like.

You’ll still get the government bonus too – a 25% top-up of whatever you pay into your account (and 40% if you’ve paid higher rate tax on some of your income).

We recommend SIPPs for more experienced investors as you’ll need a solid investment strategy to outperform the experts at other pension providers. But if you think it’s for you, check out the best SIPP providers.

Nuts About Money tip: if you’re keen to learn more about SIPPs, check out our guide: what is a SIPP?

A ready-made personal pension is one where your investment decisions are all handled for you. All you need to do is add your money – either as a one-off payment or a regular monthly payment (recommended).

They're often set up by online stock brokers or investment platforms, who offer SIPPs – and their experts have designed a portfolio (a range of investments) that is perfect for anyone to get going with their pension. You simply pick the ready-made portfolio, and you're all set.

They're very similar to expert- managed personal pensions. However, often expert-managed pensions solely offer pensions, so it's a bit easier to get up and running – you don't need to register with the stock broker or the investment platform first and then make your investment decisions. You simply register with the expert-managed pension provider and that's it! They'll take care of everything else.

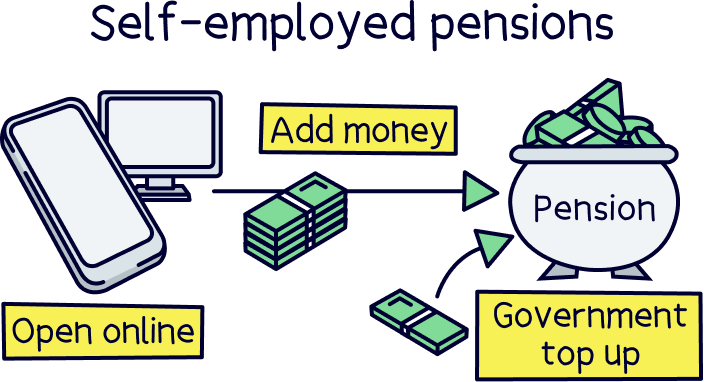

If you’re self-employed, you’ve got lots of benefits – like being your own boss, and choosing your own hours.

But when it comes to pensions, you don’t have an employer to set up a pension pot for you (actually the only good bit about an employer setting up your pension is that they have to add at least 3% into it themselves by law).

In general, personal pensions are far better than workplace pensions. You get to decide which pension provider you want to use, so you can shop around for the best rates (lowest fees), and best investment performance (in previous years) from the best pension companies – and a provider with a phone app, or expert advisors ready to answer your questions. The choice is yours!

The only downside is you don’t get the contributions from your employer as you do with workplace pensions. But you’ll still get the government bonus, starting at 25% of what you put into your pension (for basic rate tax payers).

So, to set up your pension, you’ll have to choose a personal pension provider and set it up yourself (it’s easy, really!).

Your best option is to go with a personal pension managed by the experts. The experts will handle everything for you, just like a pension you’d have if you were employed.

All you need to do is add cash, and you’ve got the flexibility to make contributions whenever and for however much you’d like to.

Nuts About Money: learn more with our guide to self-employed pensions.

Pensions might seem complicated, but they’re actually really simple these days.

The hardest part is finding the right pension company for you, but luckily we’re here to help and have done the hard work for you and researched and reviewed the best – all in the private pensions table above.

Once you’ve found one you like and signed up, it’s all over to them. They’ll handle everything for you, that’s transferring existing pensions over if you have them, to setting up any regular payments you’d like to make.

You’ll normally have to choose how you’d like your money invested, for instance if you’d only like ethical investments (so no oil or gas companies for instance), but they’ll help you with this too.

They’ll even collect the government bonus for you – that’s the 25% you get free on everything you put into your pension pot.

So really, all you need to do is put your feet up, add to it regularly if you can, and watch your pension grow over time.

You’ll be able to access your private pension pots much earlier than your State Pension (which is from age 66). From 55 you can access your private pension(s), but it’ll be 57 from 2028, unless you are diagnosed as terminally ill, then you can access it immediately.

When you’re able to access it, you can take up to 25% completely tax-free! The rest may be taxable, depending on how much income you are getting, so you might want to wait until you officially retire before you think about taking the cash, so you reduce the amount of tax paid overall.

Nuts About Money tip: here’s more information on pensions and taxes.

With a private pension, as it’s all your cash (and not the government's cash like the State Pension), it will pass to your next of kin or someone you specify with your pension provider. It’s not lost forever.

Nuts About Money tip: here’s more information on what happens to your pension when you die.

A self-invested personal pension (SIPP) is where you decide where your money is invested, and you buy and sell these investments yourself, through your pension account.

Whereas a typical personal pension is where experts make all the decisions for you. You don’t need to lift a finger, just sit back, let them do work, while you watch your pension grow over time. Often called a ready-made personal pension.

SIPPs are more flexible as you have more investment options, but they’re suited to experienced investors with a solid investment strategy. And often already have a personal pension managed by the experts, but want to add a few extra investments on top.

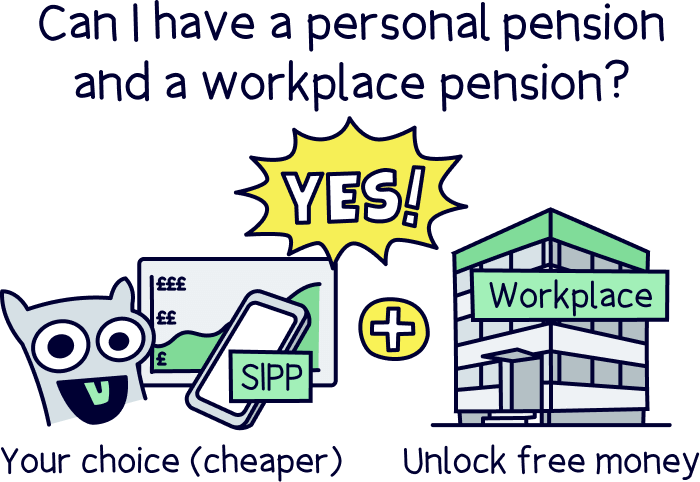

Yep! And it’s highly recommended, and very common. It's the best way to boost your total pension pot for a comfortable retirement.

A workplace pension is set up by your employer and it’s their choice who they decide your pension is with (and often not the best choice, with expensive fees and poor performance).

With a personal pension, you have control over who your pension is with, and can transfer to another company whenever you like. So you can choose a pension provider with low fees, good performance and perhaps have a great phone app that allows you to track your pension whenever you like.

You’ll also get all the same benefits as a workplace pension, such as tax-free contributions thanks to the government bonus, but you won’t get the employer contributions (which your employer is forced to make by law, and is a minimum of 3%).

If you’re lucky and have an employer who matches your contributions up to a certain point, it’s often better to pay into your workplace pension up until the point where your employer no longer matches your contributions (which is basically free money).

And after that point start paying into your own personal pension instead, to benefit from potential cheaper fees, better performance and more control over your money.

A stakeholder pension is another type of private pension, but an older type of pension, and not often used, but are still available, and some employers still work with stakeholder pension providers. However you most likely do not have one.

Stakeholder pensions were designed for those who might struggle to get access to a ‘regular’ pension – such as those on low incomes or who work part time (your employer is not required to open a pension for you in these circumstances), or you could be self-employed with fluctuating income.

However, they’ve mostly been replaced by personal pensions and self-invested personal pensions (and all the best private pension plan providers are listed above).

They’re slightly different however, they must follow 3 rules:

Although this all sounds great, and it is, most private pensions also have low fees and low minimum payments – so they’re not really that much different, and there’s also restrictions on where your money can be invested with a stakeholder pension, so they might actually grow slower than other pensions too.

When you transfer your pension pot (pension plan) from one pension provider to another (transferring your pension), you might have to pay an exit fee. And previously this used to be quite a lot, but the Financial Conduct Authority has cracked down big time.

Here’s the new rules:

Some pension providers were particularly greedy and had super high exit fees (as much as 10%) to deter you from transferring to a better provider, and staying with them. The downside is they often had very high management fees too. Which means it’s actually still better to pay the exit fee and change to a lower cost provider, as in the long run it would be cheaper.

Anyway, your new pension provider will let you know if there’s going to be an exit fee and how much it is – so you don’t have to continue the pension transfer if you don’t want to. Often, there won’t be any exit fees, so don’t let the anticipation of a fee put you off.

The pension lifetime allowance has now been scrapped, which is great news for those saving big cash – which could be you if you’re saving into your pension regularly.

Previously, there was a limit on how much you could withdraw and still benefit from the great tax rules pensions have, which was £1,073,100.

If you withdrew money above this amount, you’d have to pay 55% tax on the extra.

However, it’s now been abolished, and whatever you withdraw, that’s not part of your 25% tax-free allowance, will be taxed at the same rate as Income Tax – how much you actually pay will depend on how much your income is at the time. Here’s a run through of the current Income Tax bands:

Now this bit is important if you have got a big pension (or likely to). The 25% tax-free allowance isn’t unlimited. This has been kept at the same limit as before, when there was a lifetime allowance. Confusing right?

So, you can only take 25% of £1,073,100 out tax-free (as a maximum), which is £268,275 (which is still a lot!). Anything above this will be taxed at the same rate as Income Tax (rates above). Make sense?

With pensions, the fees can be a bit confusing, and can be different for different pension companies, and again for each different personal pension plan (the investments).

Note: we’ve looked at fees as part of comparison into the best private pension schemes.

The main fee you’ll pay is to your pension company, and typically, it’s an annual management fee (or annual platform fee), which is a percentage of the money you have saved with them. This can be anything up to 1.5% of your pension per year.

After that, wherever your money is invested, for example, the pension fund (investment fund), will have its own fees too, which goes to the fund managers. This is also known as an annual management fee, or fund fee, and is taken directly from the money invested within the pension fund.

This can range from 0.10% to 2%+ per year, it really depends on which investments are within your pension portfolio.

And, if you’re managing your own investments (within your own pension portfolio), with a self-invested personal pension, you’ll have a fee per investment fund, and you might have a fee when you buy and sell investments, often called a share dealing fee.

On top of that, if you’re using a financial advisor, they’ll also charge a fee – which can be a one-off, fixed fee for the financial advice, such as a percentage of your pension, or a set amount, such as £500.

Or, they could also charge an ongoing fee, either as part of the annual management fee, or separately, which is typically a percentage of your retirement funds.

We said it was confusing right?

So, bringing that all together, depending on which pension company you choose, you could pay a fee for the advice (determining the best pension plans for you), a fee for the private pension provider, and a fee for the investments (the personal pension scheme).

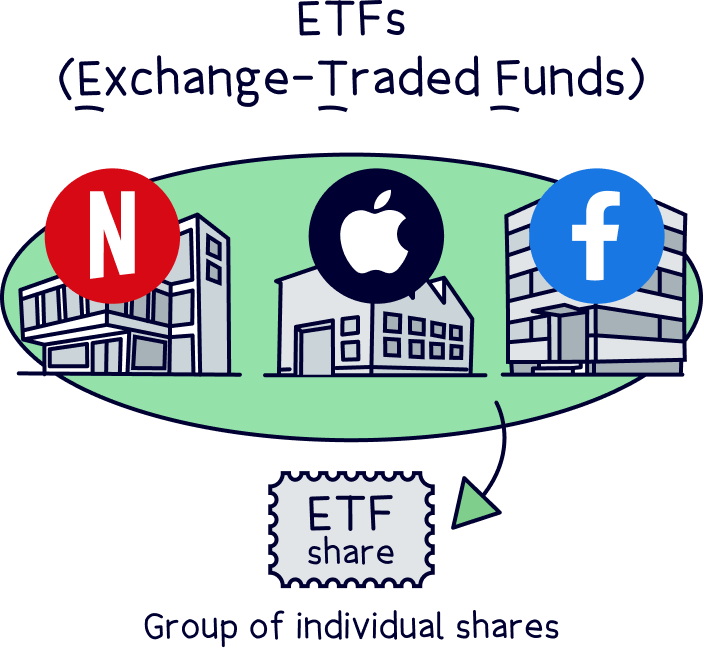

A pension fund is a bit different to your actual private pension provider. A fund is a collection of loads of cash from lots of different people – everyone’s pension pot. And this money is invested by the fund (often called the pension plan), with the aim to of growing it safely over time – so you have lots of money in retirement savings when you retire!

The investments they make are often in exchange-traded funds (ETFs), which are groups of stocks and shares (tiny portions of ownership of a company), alongside other investments such as bonds (which are effectively loans to businesses and governments that pay interest) and sometimes property.

Pension funds have their own fees in addition to pension providers (mostly), and they’re deducted from your pension pot itself each year - you don’t need to pay anything extra yourself. These are called fund management costs, or sometimes an annual service fee.

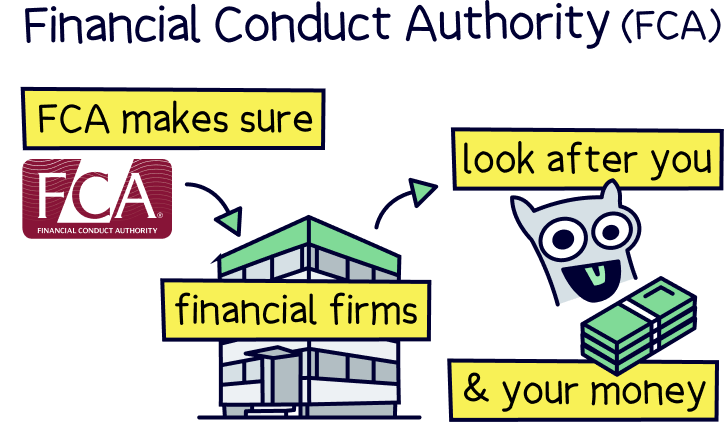

Yep! All pensions are regulated by the Financial Conduct Authority (FCA) – they’re the people who authorise and review companies to look after your money. And are very conscious of pension scams.

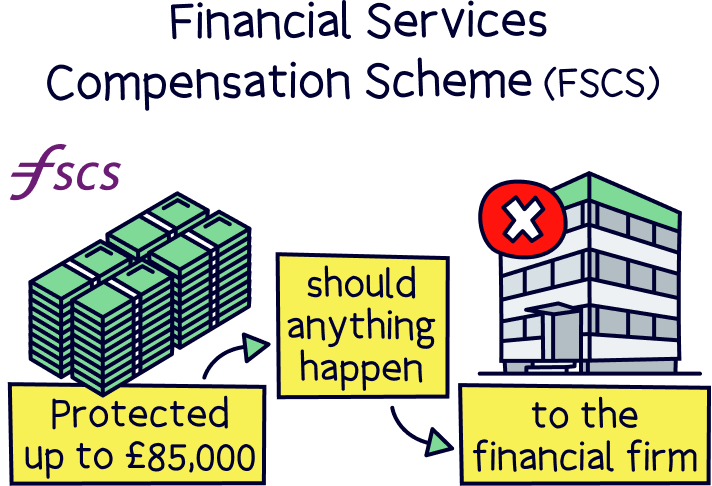

Your money is also protected by the Financial Services Compensation Scheme (FSCS), which means if the company looking after your pension closed down or went out of business, you’d get some or all of your money back.

If your pension provider closed down, you’d get all of your money back.

Plus, there’s a regulator just for workplace pensions, called The Pensions Regulator, to make sure workplace pension schemes are looking after your money.

If it was an SIPP operator, you would get back up to £85,000. However, with an SIPP your money is actually within the investments themselves, which are in your name, and can only be returned to you (the SIPP provider cannot access them). You are also covered per company, not in total.

If a financial adviser gives you bad advice, you could also get up to £85,000 compensation.

Of course, if the value of your investments go down, you are not protected. Your capital is at risk as they say. However pension funds aim to grow your money safely and securely over time in low risk funds.

When it comes to actually retiring, hopefully your pension pots will now be bulging!

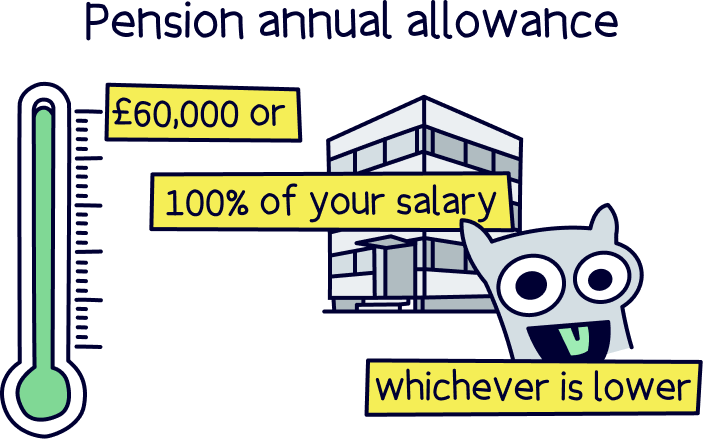

With a private pension, you can start taking money out of your pension when you’re 55 (57 from 2028) – you don’t actually have to officially retire. However, often when you start taking money out, your allowance reduces to £10,000 per year, so you need to be sure. This is called the Money Purchase Annual Allowance (MPAA).

Before taking money out, you’d be able to add up to your whole income, or up to £60,000, whichever is lower, every tax year.

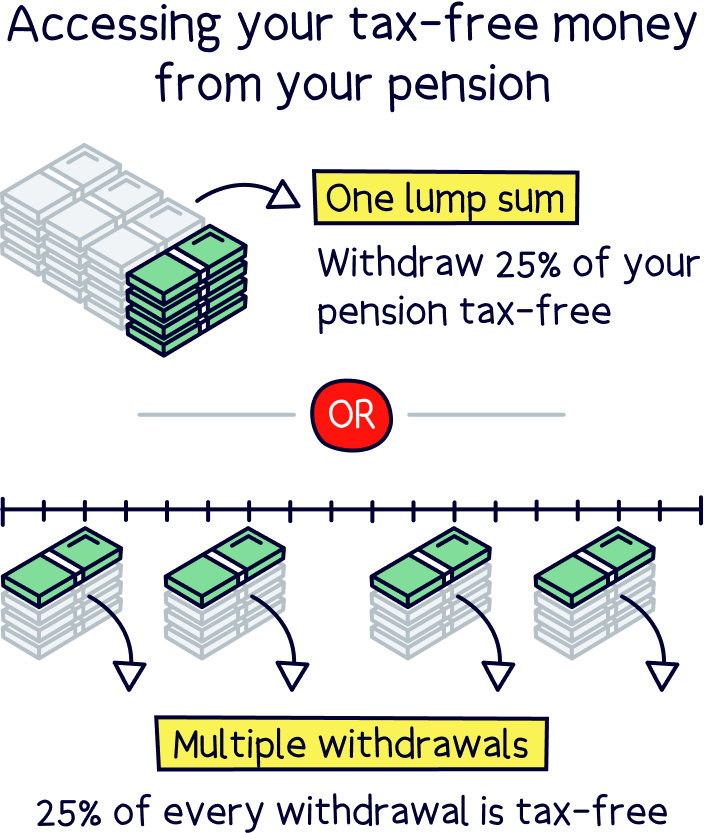

When you do want to retire and start spending your hard earned pension savings, the first 25% of your pension will be completely tax free! And you can take this as a tax free lump sum if you like. (This won’t reduce your annual contribution allowance.)

Or, if you take it as regular income, the first 25% of what you take will be tax free. Pretty good right?

Then you’ll pay Income Tax on the remaining 75%. Which is just the same as your income now (e.g. your salary), so you’ll have a Personal Allowance if £12,570 per year before you actually have to pay any tax, after that you’ll pay 20% (basic rate), on anything up to £50,270, and then 40% (higher rate) up to £125,140, and 45% after than (additional rate).

Taking money from your pension pots as income is called drawdown (sometimes called flexi-drawdown), but you also have another option, you could use your pension funds to buy a guaranteed income for the rest of your life (or for a set number of years). This is called an annuity.

You can only start claiming the State Pension when you reach retirement age (officially), which is currently 66, even if you retire early.

It’s best to speak to a financial advisor if you want advice for your personal circumstances. It is your retirement income after all! You can speak to a advisor for free with Pension Wise (a government scheme).

If you’re not convinced about personal pensions yet – let’s do a quick recap, with a run through of the pros and cons.

So, there we go. That’s all the information you need to know to compare the best private pension providers. And really they’re personal pension providers, you don’t get much say over which pension your employer chooses for you (the other type of private pension).

All that’s left to do is choose the best pension provider for you, and start saving money to increase that pension pot for a secure financial future.

Slow and steady wins the race – add as much as you can afford when you can afford it, and automatic regular payments are a great idea.

All the best with your pension savings!

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

PensionBee makes pensions simple – they'll handle everything for you. They're highly rated, easy to use and have low fees.