Article contents

You can normally take the first 25% of your pension tax-free as a lump sum. But after that, it will be taxed just like any other form of income. That means you won’t have to pay tax if your income is less than £12,570 (including your pension) but you will if it’s more.

Ready to start taking your sweet, sweet pension? Or just being super organised and planning ahead? Either way, you’ll probably be wondering how much is going to go in your own pocket, and how much will be going to the government’s instead.

Here, we’ll look at how pensions are taxed so you can get your head around the numbers and plan how to spend that lovely retirement income!

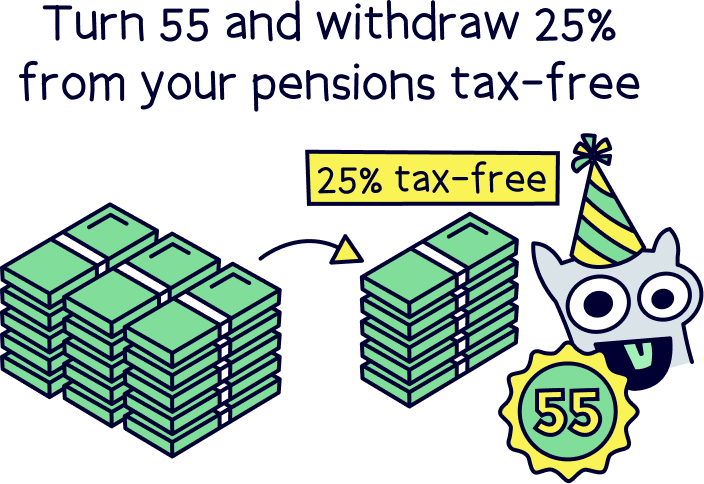

Been squirrelling money away into a pension throughout your working life? Then you’ll be pleased to know that once you reach 55, you can normally take the first 25% tax-free. Hooray!

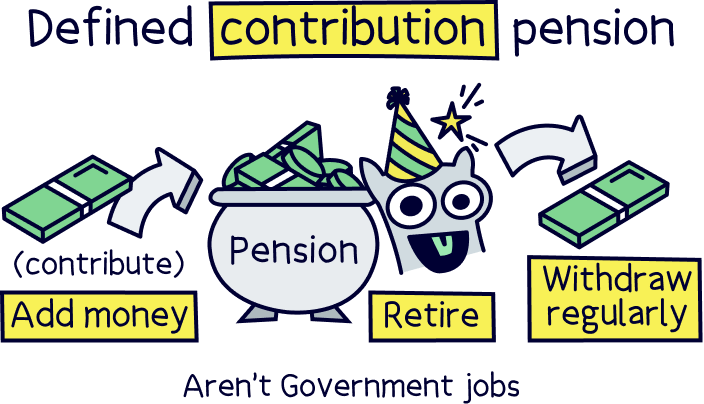

We say ‘normally’ because this is assuming you have a ‘defined contribution pension’ like most people – that’s one that works a bit like a piggybank. You save into it and then get to access your savings when you’re old enough. In fact, it’s better than a piggybank as your money will also grow while it sits there without you having to do a thing. And you won’t have to pay any tax on the earnings you put into your pension, thanks to this awesome thing called tax relief!

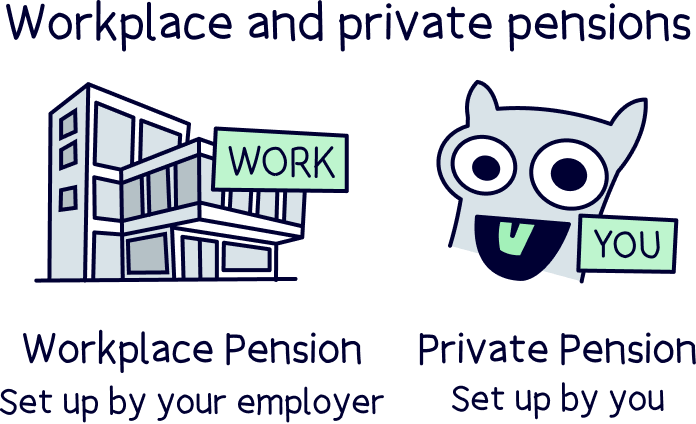

If you’re not sure what kind of pension you have, it’ll almost certainly be one of these. Most workplace pensions (ones that your work sets up for you) and all personal pensions (ones you set up yourself) work like this.

A workplace pension and personal pension are both called private pensions. The State Pension is called a public pension.

Anyway, to get that first 25% tax-free, most people take a quarter of their pension pot out in one go, as a big lump sum. However, if the idea of taking all that money out in one go scares you, don’t worry! You can also opt to take a series of smaller payments.

If you decide you want to take a series of smaller payments instead, 25% of each payment you take will be tax-free. The remaining 75% of each payment will be taxed as normal.

Find the best personal pension for you – you could be £1,000s better off.

One of the many good things about saving within a pension, including a personal pension (one that you start and manage yourself), is that you don’t pay tax when the money grows (often from the investments increasing in value within your pension).

That means you don’t pay Capital Gains Tax, Income Tax or Dividend Tax on any money while you save. Pretty great right? Let’s run through them quickly:

So saving within a pension means you don’t pay any of these taxes while your pension pot is growing nicely waiting for you to retire.

However, when you begin to take money from your pension, normally when you retire. That’s when you’ll have to start paying tax. And the tax you pay is Income Tax.

Your pension is treated just like a salary or any income you have while you’re working. It’s technically called ‘taxable income’.

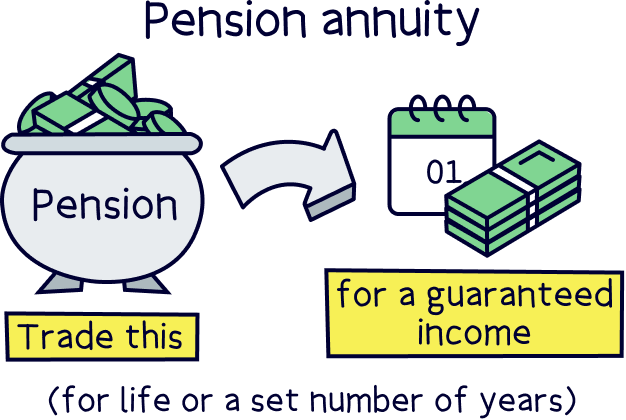

This includes annuity income, which you might have if you use your pension to buy an annuity with your pension, which is a guaranteed income for the rest of your life (normally).

If you have an older-style pension, known as a defined benefit pension – which pays you a set income when you retire (such as a final salary pension). It’s the same too.

Let’s run through how Income Tax actually works with a pension.

Here’s the thing. After you’ve taken that initial bit of tax-free income from your pension, any money you withdraw from it will be taxable. That’s because the money you get from your pension will be seen as a form of income, just like having a job or renting out a property.

Now, that doesn’t necessarily mean you have to pay tax on it. Instead, it’ll all depend on how much money you have coming into your bank account each year. Let us explain.

In the UK, you can earn a certain amount of money tax-free every year. This is known as your Personal Allowance and it’s currently £12,570.

Anything you earn up to that amount you won’t have to pay tax on. But anything you earn beyond that amount will be taxed.

Let’s say you’re taking £15,000 from your pension each year, and that’s the only income you’re getting. Thanks to the Personal Allowance, you’ll get £12,570 tax-free – however, you’ll have to pay tax on the remaining £2,430 (£15,000 - £12,570 = £2,430). Income tax for basic-rate taxpayers (people earning less than £50,270 per year) is 20%, so altogether, you’ll pay £486 in tax (20% of £2,430 is £486).

Now let’s imagine you’re taking just £10,000 from your pension each year – that’s less than the Personal Allowance, so if this was all you were earning, you wouldn’t have to pay tax. However, in this case, let’s imagine you also have a part-time job where you earn £8,000 per year. Altogether, that means you have an income of £18,000 which is above the tax-free threshold. You’ll get taxed on £5,430 of it (£18,000 - £12,570 = £5,430) and your tax bill will be £1,086 (20% of £5,430 = £1,086).

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

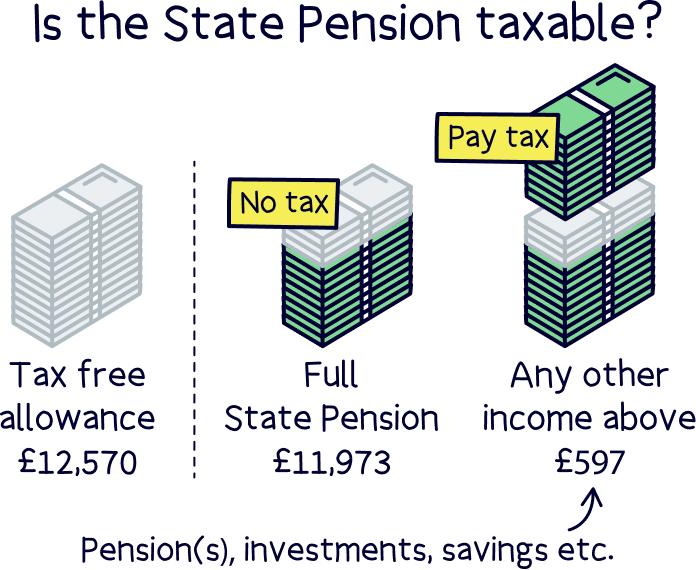

Yes! The State Pension is taxable, just like any other form of income.

In fact, remember how we said that with most personal pensions, you can take the first 25% tax-free? Well sadly, that doesn’t apply to the State Pension, so all the money you get from it will count towards your Personal Allowance (sorry!).

Let’s rewind for a second.

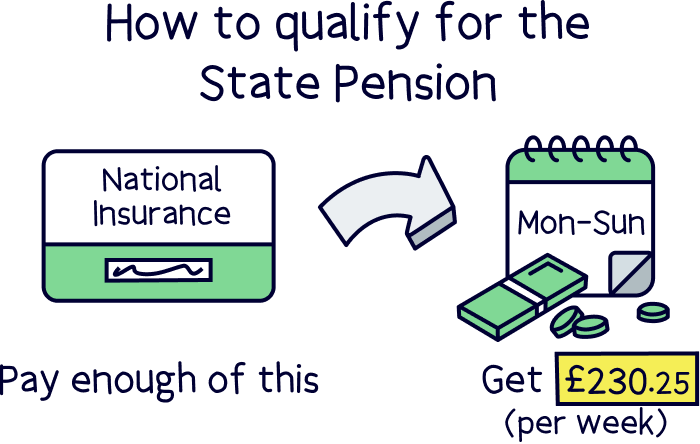

The State Pension is a weekly payment you’ll probably be able to get from the government when you reach something called State Pension age (currently 66 but gradually increasing to 68). You’ll qualify for it if you’ve made enough National Insurance contributions throughout your working life (National Insurance is a charge you pay to the government alongside your taxes, to cover things like healthcare).

Now, the maximum State Pension you can get (known as the full State Pension) is just £230.25 per week – which comes to £11,973 per year. This is below the £12,570 Personal Allowance, which means if your only form of income is the State Pension, you won’t have to pay tax.

But don’t go celebrating too soon! £11,973 isn’t a lot to live on, so if you can top it up in other ways, like through a personal pension or a part-time job, that’s probably going to be a good idea. Yes, that might mean you end up having to pay tax, but you’ll also have more money to enjoy your sunset years with!

If you’re thinking about starting a pension to boost your income in retirement, check out our favourite pension providers, PensionBee¹ and Beach¹ (pension providers are the guys that give you your pension and look after it for you). They have handy mobile apps to make it even easier to save money for your retirement – you can track your money and watch it grow all from your phone!

Remember, your pension itself isn’t being taxed – instead, your income is being taxed as a whole, and your pension simply counts towards your overall income. Because of that, there are a few different ways that you might end up paying tax if you’re over the tax-free threshold in retirement.

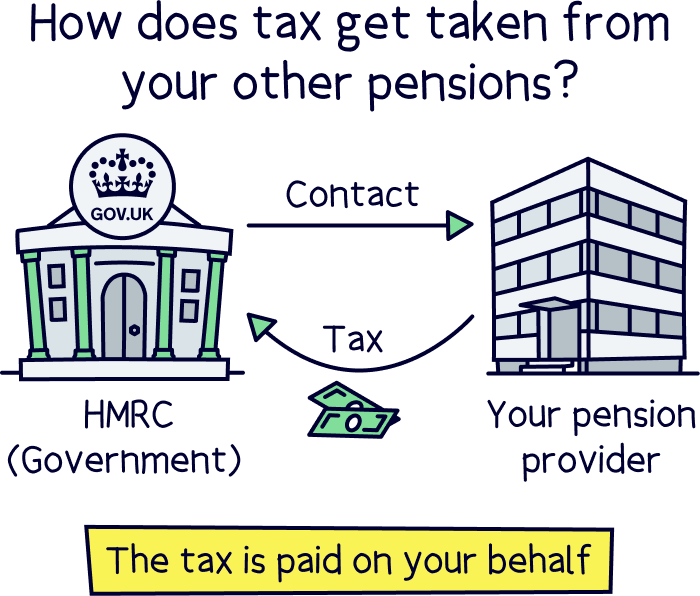

If you have a personal pension or a workplace pension, then HMRC (the part of the government that deals with taxes) will get in touch with your pension provider to tell them how much tax you owe.

Your pension provider will then pay the tax bill on your behalf by deducting it from the amount that’s being paid to you. That’s right, you don’t have to do a thing – your pension provider and HMRC will sort it all out for you!

If you also get the State Pension, your tax bill will probably be a bit higher as you’ll be further over the Personal Allowance. Instead of deducting tax from your State Pension payments, you’ll normally just pay a bit more through your personal or workplace pension to make up the difference.

There’s nothing to stop you from having a part-time – or even a full-time job while you’re getting income from a pension. In fact, it can be a great way of boosting your earnings in retirement.

If your earnings are over the Personal Allowance and you’re an employee, HMRC will get in touch with your employer to tell them how much tax you owe. The tax will then get deducted from your payslip before it’s given to you.

If you’re getting the State Pension and you’re topping up your income through full-time or part-time work, you’ll probably have a bit more tax deducted to make up for the fact you haven’t had any tax taken off your State Pension. That way, you’ll be paying the right amount of tax overall.

If you’re self-employed or you earn money in other ways, like by renting out a property, you’ll usually have to fill out something called a Self-Assessment tax return each year.

This is basically a form where you tell HMRC how much you’ve earned that year (don’t forget to include all your pension income!) and how much tax you’ve already paid (if any). The form then calculates how much tax you owe so that you can pay it. Simple!

Self-Assessment tax returns can look a little bit intimidating at first, but don’t worry – they’re not as tricky as they look and you’ll get used to them soon enough! If you want some help though, that’s fine too. You can find an accountant to help you fill yours in using Unbiased¹. Or use Taxfix¹, an online service to help with your Self Assessment tax return.

Want to minimise the amount of tax you have to pay once you retire? Then here’s the trick: only take what you need from your pension pot. At the end of the day, the lower your income, the less tax you’ll have to pay!

Don’t get us wrong, you should definitely take what you need to live on comfortably – there’s no need to scrimp and scrape by, just to avoid paying tax!

However, unlike being on a salary, there’s no point in taking more money than you need and putting it into savings. Instead, it’s usually best to leave the money in your pension pot until you’re ready to spend it. That way, you’re only taking what you need, so you won’t end up paying tax on earnings you’re not using. Makes sense, right?

If you’ve already started taking money from your pension (such as a regular income), the amount you save each year back into your pension now reduces too.

(That’s if you did want to add more money back into your pension of course).

This is called your Money Purchase Annual Allowance (MPAA). And it reduces to £10,000 per year once you start taking money from your pension.

Before this, you could have paid in up to your whole income (e.g. your salary), or up to £60,000, whichever is lower.

However, there are some rules where your allowance might not be reduced. Learn more about this on the Money Helper website.

So, to recap… if you have a personal pension or a workplace pension, you can normally take the first 25% completely tax-free. Kerching!

However, after that, the money you take from your pension will be taxable. That means if your total income (including your pensions) comes to more than the tax-free threshold of £12,570, known as the Personal Allowance, you’ll need to pay tax. And this applies to the State Pension too!

If you don’t yet have a pension, you can start a personal pension quickly and easily. Our favourite pension providers, PensionBee¹ and Beach¹ both are easy to use pension providers with great apps.

Or, if you’re ready to start taking an income from your pension, remember to take as little from your pension as you need. That way, you won’t get taxed on any money that’s sitting around and doing nothing in your bank account.

A financial advisor can help you work out exactly how much money to take from your pension, and how to take it – if you’re not sure where to find one, you can chat to our friends at Unbiased¹.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.