Article contents

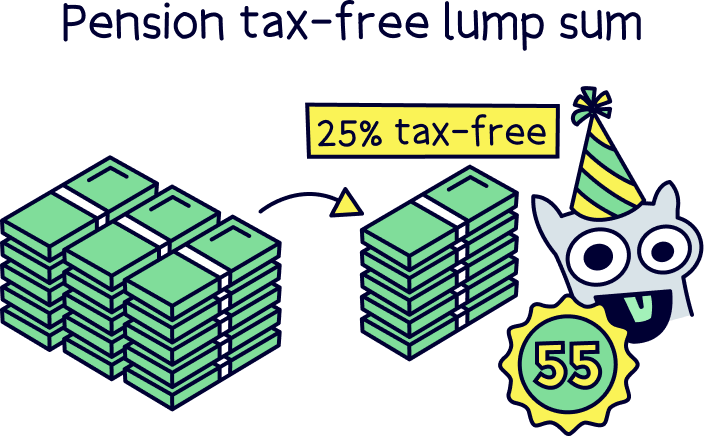

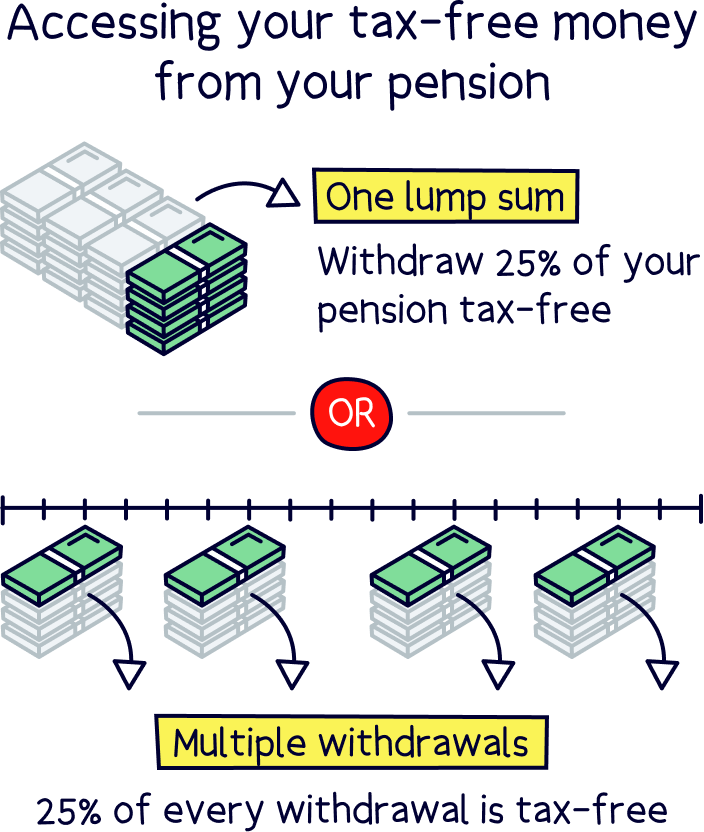

You’ll normally be able to take 25% of your pension tax-free. Kerching! You can either take that all in one go, as a single tax-free lump sum. Or, you can take it bit by bit as several smaller payments.

If you’ve been squirreling money away into a pension throughout your working life, you probably can’t wait until the day you can get your hands on all that cash! But how much can you get tax-free, and how much will wing its way to government via your tax bill?

Well, you’re in luck because we’ve broken it all down for you here. Enjoy!

Did you know that you can normally get 25% of your pension tax-free? That’s right, you’ll be able to avoid paying a penny of tax on a quarter of your workplace pension (if you have a pension that your employer has set up for you) or a personal pension (if you’ve set up a pension yourself). Hooray!

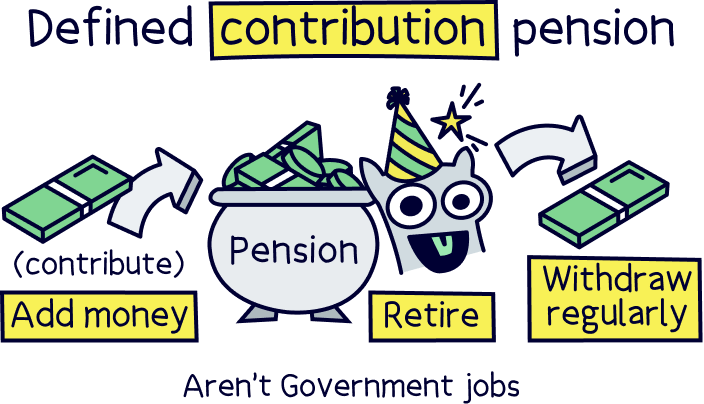

We’re saying ‘normally’ because this is assuming you have what’s called a ‘defined contribution pension,’ like most people do. That’s a pension that works a bit like a piggybank – you pay into it throughout your working life, and then when you get to a certain age (normally 55), you can get access to your savings.

In fact, it’s way better than a piggybank because your savings will grow while they’re sat there without you having to do a thing. Oh, and as well as getting 25% of your pension tax-free when you’re ready to take money out of your pension, you won’t have to pay any tax on the earnings you pay into it either. This is known as tax relief.

If you’re not sure what kind of pension you have, the chances are it’s one of these. Why? Well, because nearly all workplace pensions are defined contribution pensions and all personal pensions are too.

Anyway, once you’re ready to start taking an income from your pension, you’ll often be able to take the first 25% of your pension in one go, as one big tax-free lump sum. Nice! Alternatively, if you’d rather spread it out, you could choose to take several payments of any amount, with 25% of each one tax-free. Either way, the remaining 75% of your pension will be taxable.

Here’s the less good news… other than that 25% tax-free lump sum, the rest of your pension will be taxed just like any other form of income.

We know what you’re thinking: ‘Income?! Isn’t the money sat in my pension mine already?!’ Well, yes, but once you start taking your money as cash, it will get treated as income, just the same as if you have a job or you’re making money from renting out a property. It might seem unfair but remember, you won’t yet have paid any tax on the money sitting in your pension pot, thanks to that lovely thing we told you about earlier called tax relief.

So, how much tax will you actually have to pay on it?

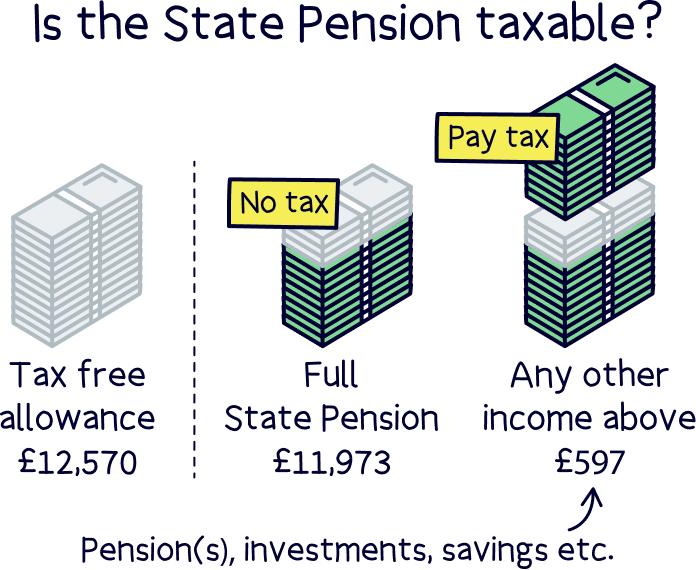

Well, that depends on how much money you have coming into your bank account. In the UK, you can earn a certain amount of money tax-free every year, known as your Personal Allowance – for the year 2022-23, that’s £12,570. Any income on top of this (including money you get from pensions) will be taxed.

Confused? Let’s say you take £11,000 from your pension this year and you don’t have any other form of income. In this case, you won’t have to pay any tax at all, as you’re earning less than the Personal Allowance. Get in!

Now let’s say you take £11,000 from your pension and you also have a part-time job where you earn £5,000 this year. Altogether, that comes to £16,000, but you’ll only get taxed on £3,430 of it as you can still get the first £12,570 tax-free (£16,000 - £12,570 = £3,430). Income tax for basic-rate taxpayers (people earning less than £50,270 per year) is 20%, so in total, that means your tax bill will be £686 (20% of £3,430 is £686).

If you have a lot of money coming into your bank account, you might have to pay 40% tax on some of your income. Some taxpayers even have to pay 45% on some of the money they have coming in. Here are the current income tax bands in the UK.

Find the best personal pension for you – you could be £1,000s better off.

Ultimately, the more you earn, the more tax you have to pay. So, the best way to reduce your tax bill in retirement is to only take what you need from your pension.

Don’t get us wrong, you should absolutely take what you need in order to live comfortably (we’re not sure that living on beans on toast for years is worth it just to reduce your tax bill!). However, unlike with a salary, there’s no point in taking more money than you need and putting anything extra in savings.

That’s because your pension pot is already a kind of savings account. You might as well leave any money you don’t need straight away in there – that way, you still have it put aside and it’s there if you need it, but you also avoid having to pay tax on it for now. Makes sense, right?

Okay, so we’ve now covered how much of your pension you can get tax-free, and how you get taxed on the rest of it. BUT there are a few different ways that you can take money from your pension, and this might affect how you want to get that tax-free lump sum.

These are:

Not got a clue what any of those are? Don’t worry, we’ll break them each down for you in a second. But before we do, it might help to know that you don’t necessarily need to choose just one way of taking your pension income. Instead, you may be able to mix and match, or use a combination of a couple. Here’s the lowdown…

Lots of pension providers will let you take cash straight out of your pension pot once you reach the age of 55 (your pension provider is the company that looks after your pension).

This involves treating your pension pot like a bank account – you can take as much or as little cash from it as you want, whenever you want. Any money in your pension that you don’t need yet can carry on sitting right where it is! And you can carry on adding money back into your pension if you fancy too (although if you want to pay in more than £4,000, you’ll need to pay tax on it).

Different pension providers will have different rules, so you’ll need to check what your pension provider will let you do. Generally though, you can choose whether to:

Make sure to check if your pension provider can handle cash withdrawals, as not all of them can. Some that do let you withdraw cash from your pension might also limit the number of times you can do this, or they might have high fees. Don’t worry if this is the case, as you can just move your pension to another provider (called a pension transfer) to find one that works better for you.

Income drawdown, also known as pension drawdown, flexi-access drawdown or flexible retirement income, involves paying yourself a regular income using your pension funds.

Your money will usually get moved from your normal pension pot into a separate but similar pension fund where it can keep growing. You can often do this with your existing pension provider, but it’s a good idea to shop around to see if there’s a pension provider with an income drawdown scheme you prefer.

Like with normal cash withdrawals from your pension, you can normally choose whether to take your tax-free cash upfront (so, 25% of your pension) as a single tax-free lump sum, or whether to split up the tax-free cash you’re entitled to and take it little by little across a number of withdrawals. But the rest of your money will be used to give you a regular monthly payment – a bit like a salary but better, as you can increase or decrease it whenever you need, to suit your changing circumstances!

Lots of people love this option as it gives you the security of monthly payments, but with the flexibility to change your mind or pay yourself more or less when necessary. That said, it’s important not to get too hasty increasing those monthly payments – make sure that you plan for the long term and leave yourself enough money to last throughout retirement!

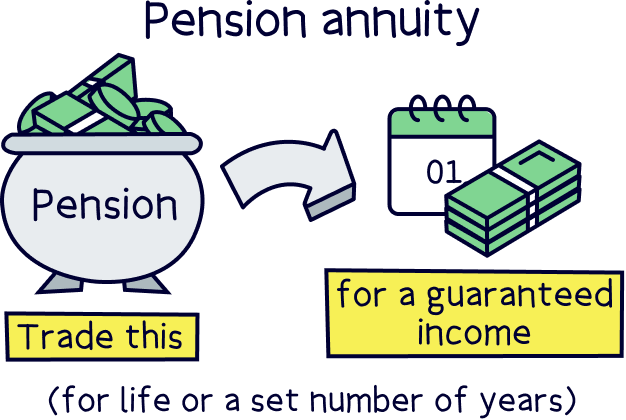

An annuity is a guaranteed income. Essentially, you can take the first 25% of your pension as a tax-free lump sum as usual. Then, you can use some or all of the remaining 75% to buy an annuity from an annuity provider.

You can choose to buy either…

The annuity will pay you a guaranteed income every month, just like a salary (and, surprise surprise, you’ll be taxed on it just like you would be with a salary too – the government always gets its money one way or another!!).

This means you can feel safe that you’re going to have enough money going into your bank account every month. Unlike income drawdown, your pension pot can’t run out and you’re guaranteed to get that nice monthly payment for the duration of your annuity, no matter what happens!

Just make sure you’re absolutely sure before you agree to an annuity. As great as they can be, once you’ve opted for one, you can’t change your mind – you’ll get the amount you’ve agreed every month and you won’t have the flexibility to get a little extra on the months where you need it.

Plus, unlike with cash withdrawals and income drawdown, your loved ones won’t inherit anything if you die before you’ve finished taking your pension. Some annuities will give a portion of your monthly payment to your spouse if you pass away, but others won’t pay anything out at all, so think carefully if this is the right option for you.

We’d always recommend speaking to a financial advisor before deciding how to take an income from your pension – if you’re not sure where to start, you can find the right financial advisor for you using Unbiased¹.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

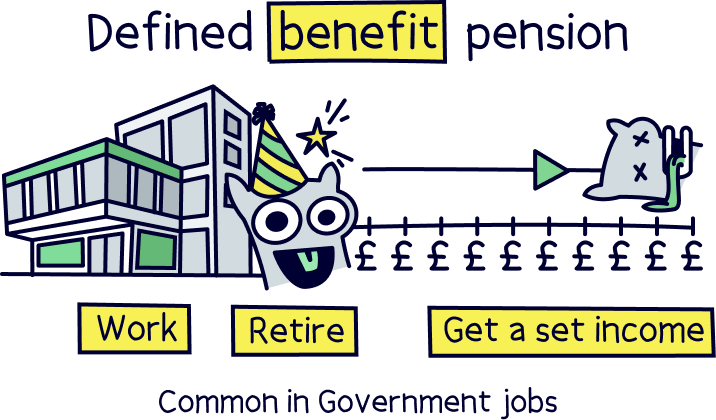

Remember how we said that the chances are you have a defined contribution pension? Well, there’s a very small chance that you have a different kind instead, called a defined benefit pension.

A defined benefit pension, also known as a ‘final salary’ pension, is a rare type of workplace pension that pays you an income when you retire based on your salary and the number of years you’ve worked for your employer. This is different from a defined contribution pension, where the amount of money you can get in retirement is based on how much you’ve paid into your pension pot over time!

Basically, your employer will set up a ‘scheme’ and make sure there’s enough money in it to pay all the employees who retire. They’ll then carry on paying you a set amount every month over the course of your retirement years.

But here’s the question we bet you’re waiting for: ‘can you still get your tax-free lump sum with a defined benefit pension?’

Thanks to some new pension rules, the answer is yes! You can still get that 25% tax-free lump sum. However, it’s a bit more complicated as your employer will then need to reduce the amount that they pay you each month to make up for it.

Don’t worry, it’s totally doable – just contact your pension provider to find out how exactly it will work in your case.

Nope! Sadly, there’s no tax-free lump sum when it comes to the State Pension, so every penny you receive from the State Pension is taxable.

Let’s rewind for a second.

The State Pension is a weekly payment you can get from the government when you reach a certain age. To qualify for it, you just need to make enough National Insurance payments throughout your working life (National Insurance is a charge you pay the government alongside your taxes to cover things like healthcare).

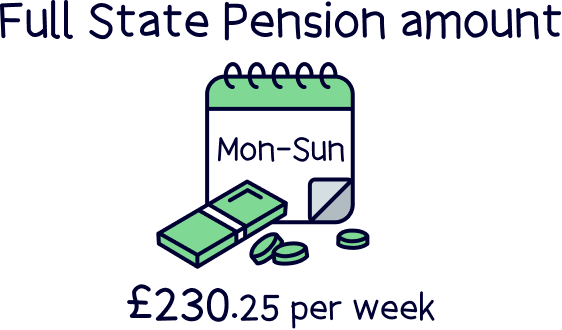

It tends to increase each year, but the maximum State Pension (known as the full State Pension) is £230.25 per week. That comes to £11,973 per year – so, even though it is technically taxable, it’s under the £12,570 Personal Allowance.

That means if your only income is the State Pension, you won’t need to pay tax on it!

That said, before you celebrate, £11,973 isn’t a lot to live off. We know, we know, it’s very nice to have. But the chances are you might struggle to live on that alone.

Luckily, you can claim the State Pension alongside other income, like personal pensions, workplace pensions and part-time jobs – which are all great ways of topping your income up in retirement! Yes, you might end up tipping yourself over the Personal Allowance and having to pay tax. But we’d say that’ll probably be worth it in order to live out your sunset years comfortably (and don’t forget you can take 25% of it tax-free!).

If you haven’t yet started a pension, why not check out our favourite pension providers? If you want a quick and simple way to track your money and watch it grow, you’ll love PensionBee with its easy-to-use mobile app. There’s also Beach¹, you can save within a pension and an ISA (for general savings) at the same time.

Pensions are wonderful things that make it super easy to save for retirement. And they’re really tax-efficient too! Not only do you get this lovely thing called tax relief when you pay money into your pension, but you also get to take 25% of your pension tax-free once you turn 55. Kerching!

Depending on your pension provider and the way you choose to take income from your pension when you retire, you can either take that tax-free 25% upfront, as one big lump sum payment. Or, you can split it over multiple payments – you’ll still get 25% of your pension tax-free, but you’ll take this part of your pension more slowly. Whichever way you choose, we bet you’ll enjoy spending it once it hits your pocket!

If you don’t yet have a pension, it’s really simple to set one up, especially with modern pension providers like PensionBee and Beach¹. They both have handy mobile apps that make it easy to watch your money grow whenever, wherever. And both have excellent customer service too.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.