Estimate your total pension pot at retirement and your yearly retirement income.

(Separate from your work pension)

About you

Your career

Advanced options

(Government pension most people will get)

(You can take 25% tax-free at 57 or older)

Here's our assumptions, FAQs and more information about the pension calculator and pensions in general.

Just a quick heads up, this calculator is intended as guidance when planning for your future.

Although we've given you figures to aim for based on the information you've provided, there's lots of moving parts which means things could change over time (check back regularly to see if your forecast has changed).

If you would like a specific retirement plan for you and your circumstances, speak to a financial advisor. You can find top rated ones with Unbiased¹.

Are you an advisor? Feel free to reference this calculator on your website or send directly to clients – no need to ask permission. Feedback for improvement is always welcome too.

Here’s what we’ve calculated to get the pension pot and retirement income figures personalised for you.

To help you plan what you might need as a retirement income in future, there’s three retirement income categories to use as a guide. These are 'minimum', 'moderate' and 'comfortable'.

They’re officially called the Retirement Living Standards, and were put together by the Pensions and Lifetime Savings Association. They’re reviewed each year to account for things increasing in price (so they increase every year).

These are a guide to how much you will likely spend in retirement, not how much your income should be – and therefore we have planned a higher income to account for tax you’ll pay on your income.

Note: none of the standards include any housing costs, for instance rent or a mortgage (it’s presumed you will have paid off your mortgage by retirement). If you expect to have these costs, you’ll need to increase your estimated pension pot.

This is the very least you’ll need in retirement in order to pay your household bills. There’s no money for a car, and not much for new clothes, or presents for friends and family. You might be able to afford a week holiday in the UK per year.

In today’s money, this is £13,400 per year for a single person, and £21,600 per year for a couple.

This provides more financial security, with all the bills covered, and more for food. There’s a little bit of money to eat out once per month, and you’ll be able to run a small, 3 year old car, and replace it around every 7 years.

There's a bit for luxuries, and new clothes and presents, and you’ll be able to afford a low cost holiday in Europe per year.

In today’s money, this is £31,700 per year for a single person, and £43,900 for a couple.

This is to provide more financial freedom, without having to worry about finances too much. There’s more for food each week, you can replace your car around every 5 years (still a cheap car). There’s also a bit to make repairs on your home.

There’s enough for a more expensive holiday in Europe and weekend breaks in the UK. There’s also more for new clothes or extra luxuries, and more for things like birthday presents for the family.

In today’s money, this is £43,900 per year for a single person, and £60,600 for a couple.

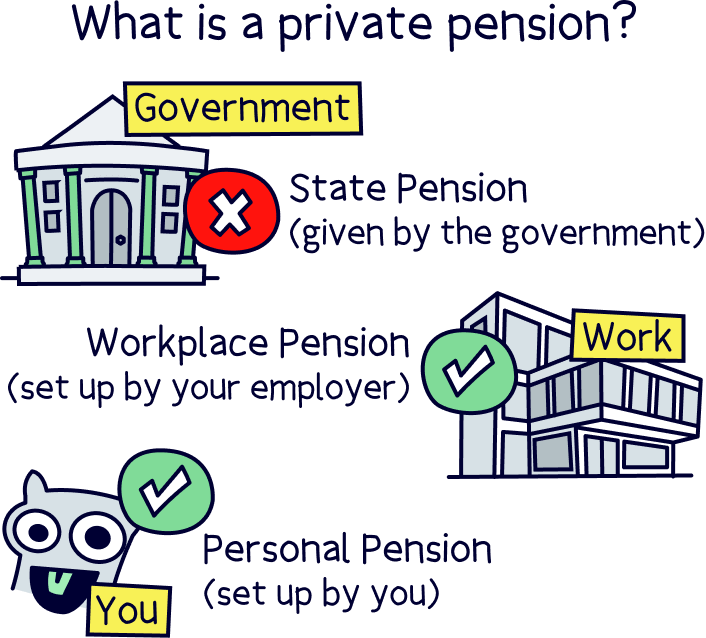

A private pension is a private that’s in your name, you decide how much to save into it, and later when to withdraw it (it’s a pension all private to you, rather than the government providing it).

They come in two main types, a workplace pension, and a personal pension.

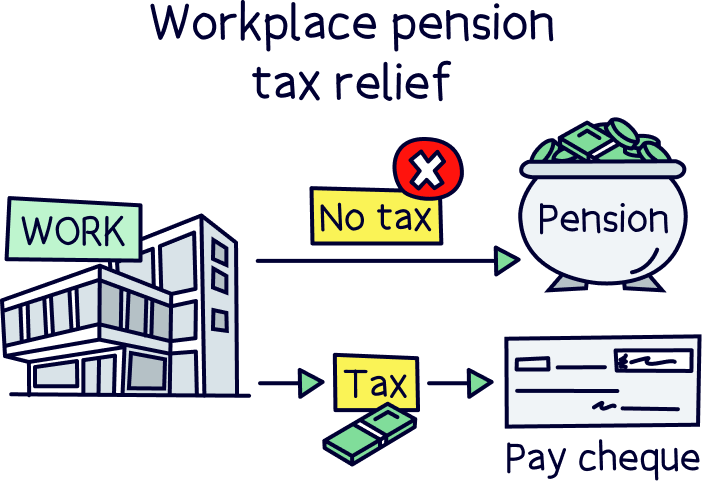

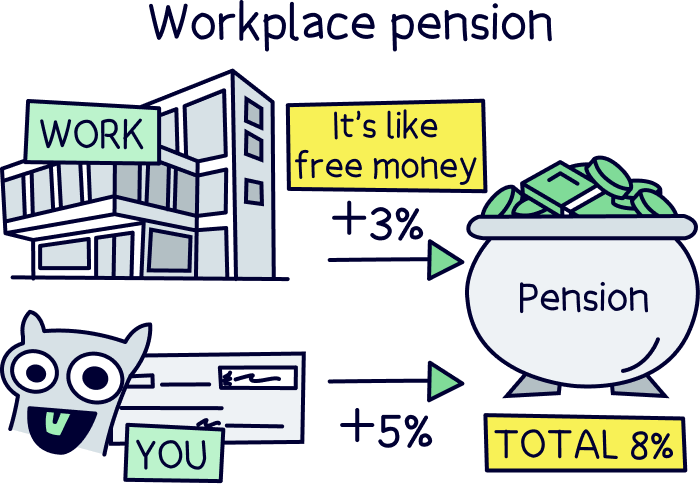

A workplace pension is one your employer will set up for you (if you’re employed). They’ll take your contributions directly from your salary and put them into your pension pot before you pay tax.

They’ll also add 3% to it themselves, as long as you add 5% (which is a legal requirement).

For this reason, in the settings above we've defaulted the 'work pension' to 8% of your salary.

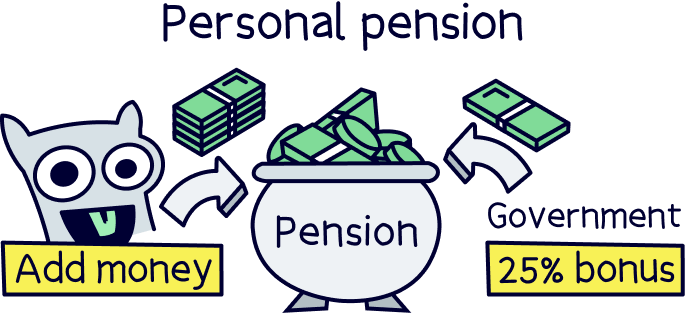

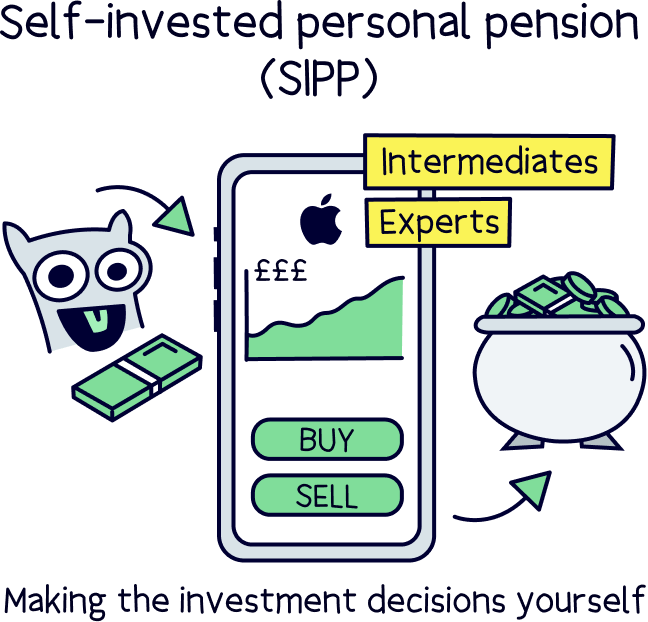

A personal pension is one you set up yourself. You can decide which pension provider to use, which pension plan to use (such as ethical, with no investments in fossil fuel companies), or even make your own investments (via a self-invested personal pension).

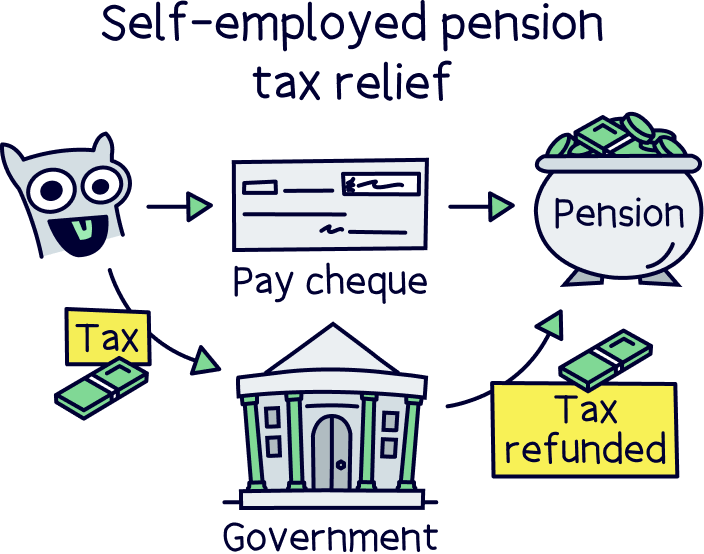

You’ll still be able to save tax-free (get tax relief), however, you’ll get it refunded back into your pension pot (as a 25% bonus from the government), or if you pay 40% or 45% tax, you can claim it back on a Self Assessment tax return.

This is the amount that you are already, or might want to save, either in addition to your pension from work, or if you’re self-employed it's the only way to save into a pension.

Making personal contributions is becoming very popular, and a great way to boost your overall pension pot to build up a more comfortable retirement income.

If you are employed, these contributions could be into your work pension (although we’ve got a work pension section for that on the calculator) – but more commonly, they’re into a personal pension, which is a pension you set up yourself.

A personal pension gives you much more control over your pension savings, as you can pick which pension provider you want to use (so can pick a great one), how much to save, and when (although we’ve assumed you’ll save monthly).

You can decide where your pension is invested (e.g. a pension plan managed by experts, perhaps ethically, or you can even make your own investment decisions with a self-invested personal pension (SIPP).

You can also transfer pensions from old jobs into a personal pension to keep your money all in one place (and not forget about them).

Remember, whenever you save money into a personal pension you’ll get a 25% bonus from the government (to refund tax paid on your income), and can claim back 40% or 45% tax if you’ve paid it – more on all that below.

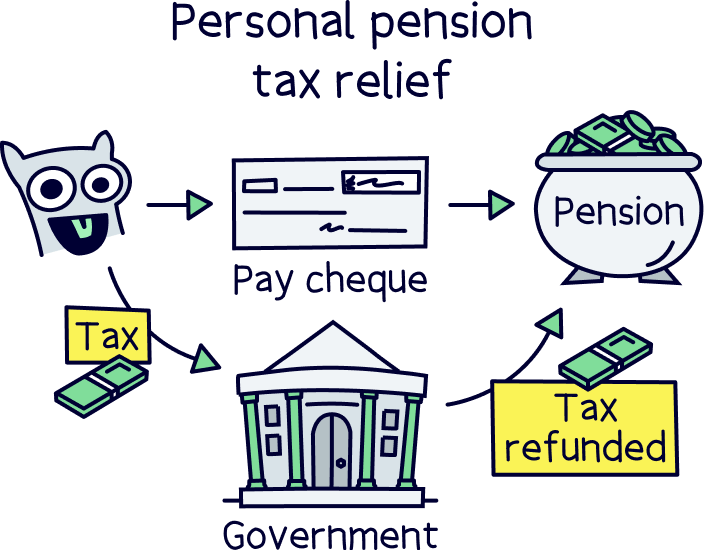

When you add money to a personal pension (a pension you set up yourself), you’ll get 25% from the government too – automatically added directly into your pension pot.

This government bonus, technically called tax relief, is a refund of the tax you’ve already paid, or will pay in your income, at 20% tax (it sounds odd but the maths works out).

This is because saving into a pension is intended to be tax-free, so the government gives you the tax back.

20% tax is applied to earnings between £12,570 and £50,270 (the first £12,570 is your Personal Allowance where no tax is paid).

If you pay higher rate tax (earning over £50,270 and paying 40% tax), or additional rate tax (earning over £125,140 and paying 45% tax), you can also claim this back on a Self Assessment tax return (on anything you’ve paid into your personal pension). If you want help, TaxScouts¹ can help you, their service is rated 5 stars.

Note: we’ve included the government bonus in your personalised pension pot projections, but not any additional tax relief for higher rate or additional tax (40%/45%). This is separate.

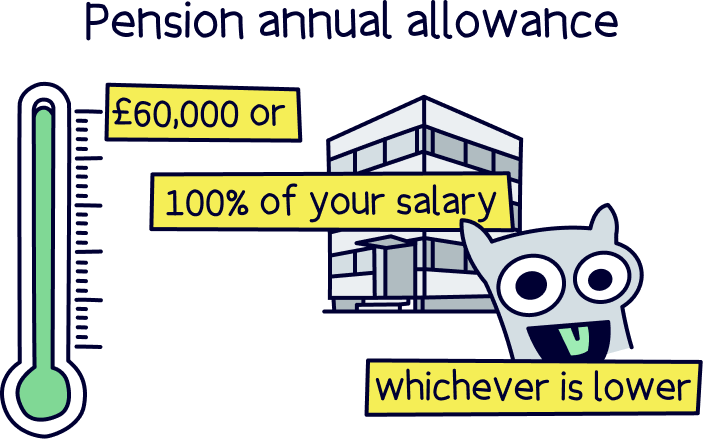

However, there is a limit on how much you can save per year, which is either 100% of your annual income, or £60,000, whichever is lower.

You can use the last 3 year’s annual allowance if you haven’t used it all previously, which can be great if you’ve got something like a bonus from work – but you can only add as much as your total income this year.

For example, if you’ve earned £100,000 this year, you can save £100,000 into your pension this year too, using any unused allowance from the previous 3 years. Also, you need to have had a pension open in those years. This is called the pension carry forward rule.

If you are lucky enough to earn over £260,000 there's a bit of bad news, your annual allowance will reduce by £1 for every £2 you earn above it (so every £20,000 you earn above £260,000 will reduce your allowance by £10,000), until your allowance reduces to £10,000, which will happen if you earn £360,000.

We’ll use your current age to work out your total pension pot by the time you retire – and to work out your State Pension age (the age you can get the government pension).

Your current pension pot is how much you have in your pension already – which includes the total of your pension from work, any old pensions you might have (e.g. from old jobs), and a personal pension (if you have one).

If you’re not sure, an estimate is absolutely fine. Or, you could even put zero for now (although doing this will mean the amount you need to save (shown above) will be more than you actually need (which isn’t necessarily a bad thing!).

This is the age at which you expect to retire.

We’ve set the default as your State Pension age, which is the age at which you’ll likely get the State Pension (the government pension).

If you plan to retire below your State Pension age, we won’t include any State Pension income in the years before your State Pension age. But it will automatically be included when you reach the State Pension age.

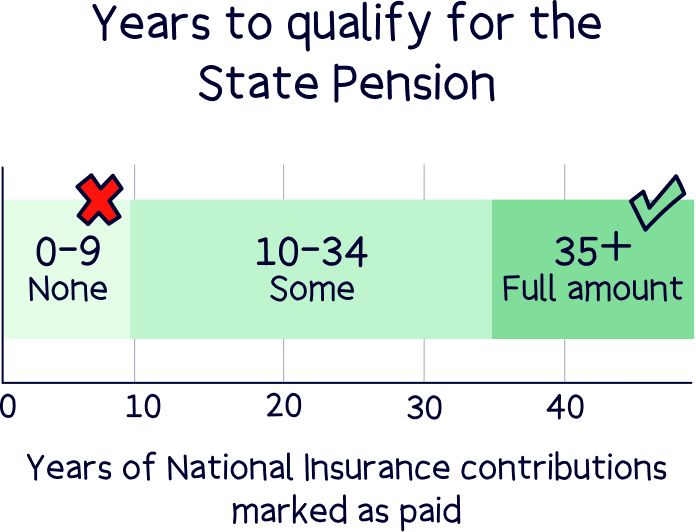

The State Pension is the government pension, and you’ll get this if you’ve made enough National Insurance contributions over your working career. You’ll need to have made at least 10 years worth of contributions to get some money, and 35 years for the full amount.

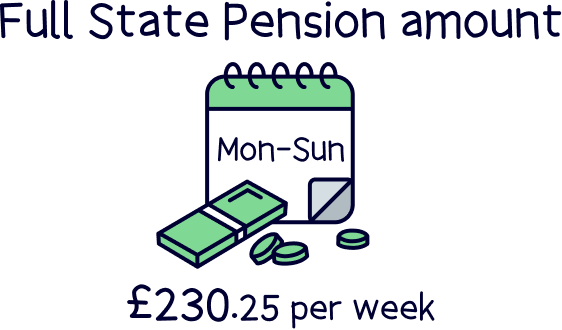

The full amount is currently £230.25 per week (£11,973 per year), which these days isn’t a lot. It’s likely not enough by itself to cover everything you need in retirement – in fact, it’s lower than the minimum recommended (£13,400 per year).

That's why private pensions are so important. They help you boost your retirement income so you can live a bit more comfortably, and not worry about money constantly. If you’re not saving into a private pension yet, we highly recommend it – set one up through your work, or start a personal pension.

We’ve increased what you’ll receive from the State Pension by 2.5% each year, starting at today’s State Pension income of £11,973 per year (which is £230.25 per week).

This is because the State Pension should always increase every year as it’s written in law. It will rise based on whichever is highest of these 3 things:

Together this is called the ‘triple lock’.

So, as a minimum, unless the law is changed, the State Pension will rise by a minimum of 2.5% each year.

If you’re self-employed (i.e. working for yourself), which could be as a sole trader or through a limited company, your pension is different to someone who is employed – mostly because you don’t get any free cash from your employer, and your pension isn’t typically taken out of your pay automatically.

For people who do have a job and are employed, their employer typically has to contribute 3% of their salary if they contribute 5% (by law). And that’s how we’ve got to the default 8% contributions for a work pension.

So, if you tick you’re self-employed, we’ll remove any work pension contributions, and we’ll just count your personal contributions (if you add them).

You’ll still be able to save tax-free into a pension – read above about the 25% government bonus!

Nuts About Money tip: we've got a great guide to self-employed pensions if you’re keen to learn more.

We’ll use your current income to work out how much you’re currently paying into your work pension if you have an employer (with the default as 8%).

We’ll also then plan your income increasing every year by 3.75% until you’re 50. This is the recommended figure provided by the Financial Conduct Authority (FCA).

You might not get a 3.75% pay rise every year, or you might get a bigger one, or you might not get one for a while, and then a huge one if you switch to a better job, but in theory, it should roughly average out.

As an average, salaries should keep up with or be slightly higher than inflation over time (around 2.5%), so it’s a good figure to assume your salary will increase by (and fingers crossed for a bigger pay rise).

After 50, on average, salaries tend to reduce over time, and we’ve planned for your salary to reduce by 2% per year. This is often because people in their 50s and above tend to reduce their hours, enjoy life more, work less overall, move to an easier job, and well, a whole range of things really!

If you’re employed, this is the pension your employer will set up for you when you join (unless you opt out), which is part of the pension auto-enrolment process.

Your contributions are taken directly out of your salary (before tax), and if you contribute at least 5% of your salary, your employer has to contribute at least 3% too by law. That’s how we’ve got to the default 8% figure – but you can change this if you’ve got a nicer employer who is contributing more themselves, or if you are too.

Nuts About Money tip: if you are contributing more into your work pension, but your employer isn’t (and just adding the 3%), it can be a good idea to save any extra you’re planning to save into a personal pension instead. This gives you more control and choice – you get to pick the pension provider (so can pick a great one), and decide where your pension is invested (e.g. no fossil fuel companies, or even making your own investments). Learn more with our guide to a personal pension vs workplace pension, and compare all the best personal pensions.

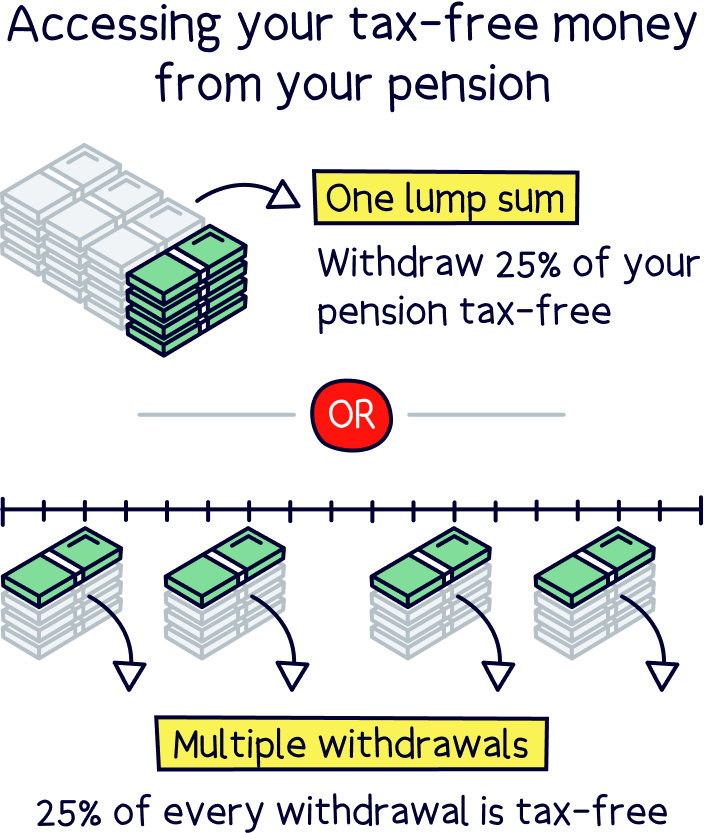

You can typically take 25% of your pension tax-free, and if you want to, you can take this as a tax-free lump sum (all in one go) when you currently reach 55 years old, or any age afterwards, but this is rising to 57 in 2028 (so we’ve used 57 for our calculator).

You don’t have to though, and it’s a big chunk to take if you don’t need the money – a slight warning, your future retirement income will be significantly reduced.

You don’t lose the opportunity for getting tax-free cash – alternatively, you can leave your pension growing, and when you later withdraw from it, 25% of your withdrawals will be tax-free.

Note: there is a limit to how much is tax-free overall, which is currently £268,275. So even if you have a very large pension pot, you’ll only get this much tax-free.

This is how much your pension is estimated to grow while it’s in your pension pot – it grows by being invested sensibly by experts.

As an average over the years until your retirement, we’ve used a figure of 5% as the default. This is around the middle-of-the-road figure, which isn’t too optimistic, but not too low either.

A typical retirement plan would look at 2% for the worst case, 5% for the average, and 8% for a good performing plan.

Remember, this is the average over time, and not for a specific year – where you could see your pension grow much higher than 8%, but you’ll also likely have years where it’s under too.

Using 7% is a popular figure – we haven’t used this because we’ve left some room for the fees involved with a pension. These can be around 0.50% to 2%+ of your pension pot per year, depending on who your pension provider is and where your pension is invested.

After retirement, we’ve estimated your pension will grow at 3% per year on average. This is because your pension typically changes to be similar to a savings plan, to preserve your pension pot and provide a steady income, rather than aiming to grow larger.

We’ve set the default life expectancy to 100 years old (how long you’ll live to). It’s typically best to make financial plans to live around this long due to average life expectancies rising, and more of us living longer, healthier lives.

For example, if you are 18 years old today, there’s a 1 in 4 chance you’ll live until 96 years old, and a 1 in 10 chance you’ll live until 100 (ONS, 2024).

If you estimate to live less than this (within your financial plans), you may end up running out of money when you need it most (and likely not able to work).

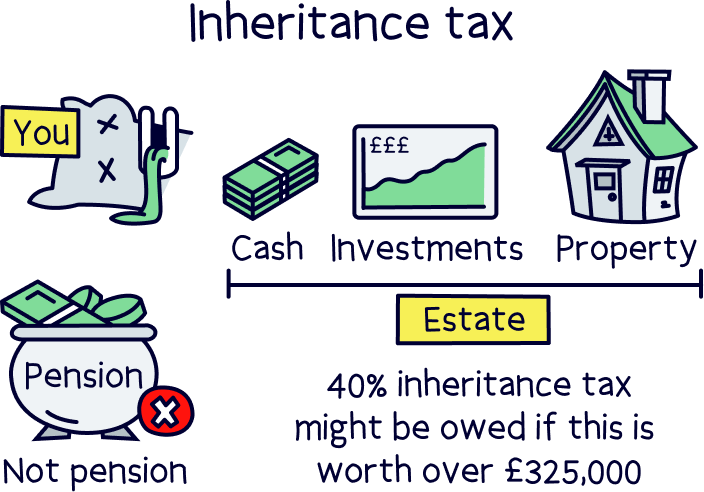

And if you do sadly pass away younger than planned, the money isn’t lost, your pension pot will be passed to your family, or anyone you choose (and free of any Inheritance Tax. They might pay Income Tax on what they withdraw if you pass away over 75, otherwise it’s tax-free).

Your retirement income is pretty much all in your hands these days – there is a pension from the government, but it’s not enough to provide a comfortable retirement. In fact, it’s not enough to even cover the minimum needed.

The State Pension is a good boost to your retirement income, but it shouldn’t be relied on as your sole retirement income, or you’ll likely struggle to get by.

A private pension is not only essential, but it will need to be very large in the future to provide a comfortable retirement – and the more you can save into yours, the bigger your pension pot will grow over time.

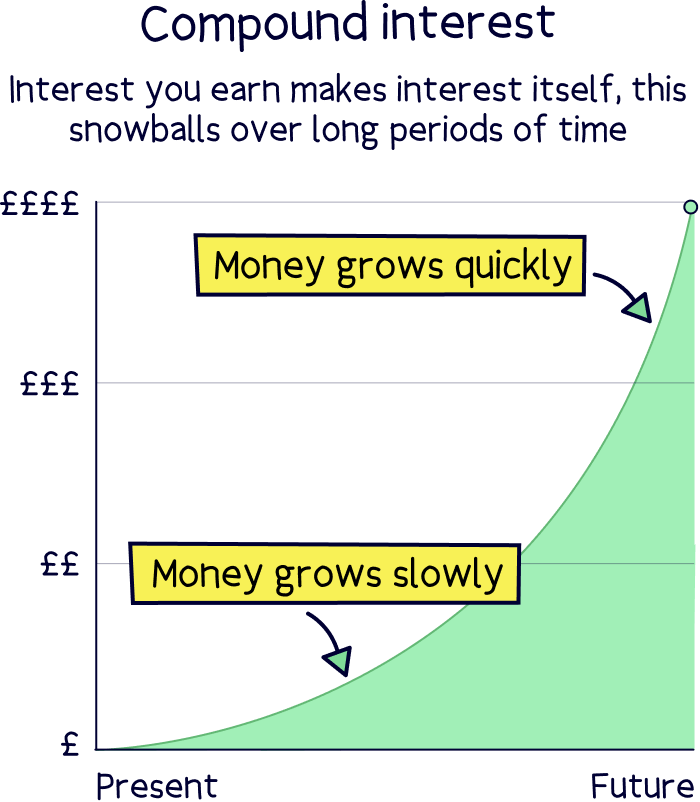

We’re sure you’ve heard that 1,000 times, but it really is true – your money grows a lot over time (much more than you actually save into it), and this snowballs over and over, and given enough time, will hit those figures you see above. Promise!

One of the most popular ways of saving for retirement is to make the most of your workplace pension, by saving 5% of your salary, so your employer has to save 3% too. And if they’ll add more if you do, add more!

However, you'll probably need to save more than that overall though, so if you’re happy with your workplace pension, you could save more into that. Or, you could opt for a personal pension, which is one you set up yourself – doing this means you can decide which pension provider to use (so you can pick a great one), decide where and how your money is invested (e.g. ethically, or in a pension plan you like), and could potentially benefit from it growing quicker and lower fees.

Using a personal pension gives you much more control over your pension pot overall, and you can transfer to a new provider whenever you like (which you can’t do with your current work pension until you change jobs) – so you can always be with a top provider.

You can also transfer over old work pensions from old jobs, so you can keep all your pension in one place – so you won’t forget about it when the time comes to retire (which happens more than you think).

To learn more, here’s our guide to personal pensions, and our picks of the top pension providers.

All the best saving for retirement!

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

PensionBee will contribute £50 to your pension when you open a PensionBee account.