Article contents

Our Nuts About Money survey from 2025 found the average pension pot for 18-24 year olds is £10,500. For 25-29 it’s £25,000. For 30-39 it’s £82,500. For 40-49 it’s £120,000. For 50-59 it’s £300,000, and for 60-66 it's £310,000.

Concerned that you aren’t saving enough cash in your pension savings? Or maybe, like most of us, not sure how much you should actually have in your pension?

Don’t worry, we’ll run through how much you need to have in your pension to get the retirement income you want. We’ll break it down by age too. And, we're using the latest data possible from 2025.

We know that most people aren’t saving enough, and that could be you. The good news is there’s an easy solution – you can open a pension right now, and start saving today, and every time you add money, you’ll get a massive 25% bonus from the Government, all for free.

These are called personal pensions, and are a great way to boost your pension pot in addition to a pension with your work (if you have one), and pretty essential if you’re self-employed. All you need to do is add money, and the experts will handle everything else.

We’ll cover this in much more detail below, but as a spoiler, here’s our top picks for personal pensions.

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

Let’s dive straight into the numbers, here's the average of what people in the UK currently have in their pension savings (their pension pot).

We used three data sources: our own (Nuts About Money) survey data from 2025, government data via the Office for National Statistics (ONS), and data from PensionBee, a large pension provider.

This is based on our survey of our readers. These are the latest results from 2025. This shows the pension pot for the middle of each age group (so half have less and half have more) – it's also called the median and is a popular way of showing averages for things like pension pots.

Data: Nuts About Money (2025)

This is data collected by the Office for National Statistics (ONS), from the latest data available (published January 2025).

Data: ONS (Pension wealth: wealth in Great Britain) - Data released 24th January 2025 for reporting period 2020 to 2022.

This is data on customers from a pension provider.

Note: this is based on a male rather than a female, which is the higher of the two genders on average.

Data: The UK Pension Landscape

Was it what you were expecting?

To clarify, it's important to remember that this is the average pension size, so what the average person in the UK has in their pension, and not the recommended pension size to have a comfortable retirement.

The scary thing is the recommended pension size is much bigger! But don’t panic, if you follow our advice you can increase your pension by a significant amount. We'll cover all this below.

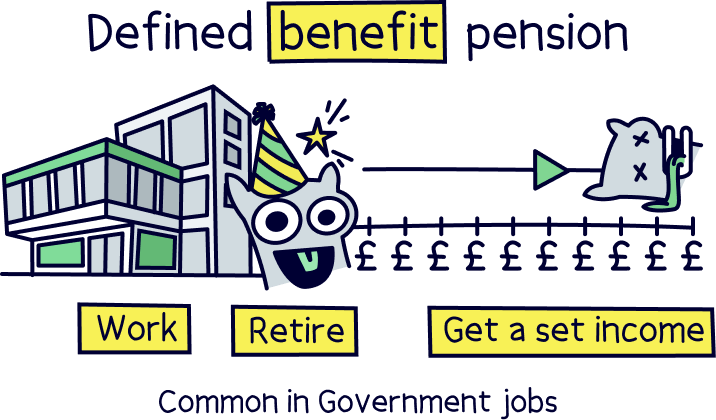

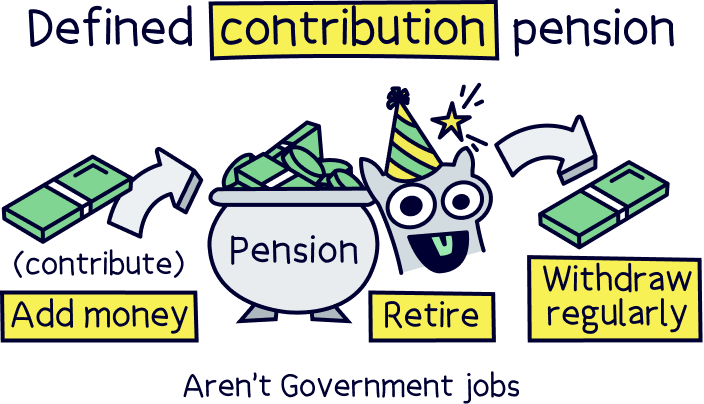

These amounts include the average of all pensions and includes defined benefit pension schemes and defined contribution pension schemes…

Defined benefit pension schemes are more common in government jobs, such as the NHS, and are where your pension is determined by how long you’ve worked there and what your salary is.

A defined contribution pension scheme (with your workplace) is what you’ll most likely have if you don’t work for the government. It's where you pay in a set amount each month automatically from your salary, and your employer adds cash too (3% when you pay in 5%).

The actual average retirement pension income in the UK is £387 per week, which works out as £20,124 per year, or £1,677 per month. (GOV.UK, 2024).

Alarmingly, this hasn’t increased much since 2010, where the average pension income was £371. But the cost of things have risen dramatically, making pensioners much poorer. We’re really not doing a great job of saving for our future in the UK.

That £387 per week number includes both single pensioners and couples. If we split it out, a couple receives £561 per week (so £281 per week each). And a single pensioner receives £267 per week on average.

There is also a difference between gender too, with single male pensioners receiving an average of £286 per week, and single female pensioners receiving £259 per week.

That’s enough to get by (just), but not enough for a comfortable retirement. We’ve covered this in detail below.

Check out our pension calculator to see how much you’ll likely need in retirement, your estimated pension pot size, how much your pension pot might provide (including how much you’ll get from the State Pension), and how much you might want to save each month to provide the retirement you'd like.

It takes less than a minute, and it's pretty awesome (even if we do say so ourselves).

If you’re self-employed, here’s our self-employed pension calculator.

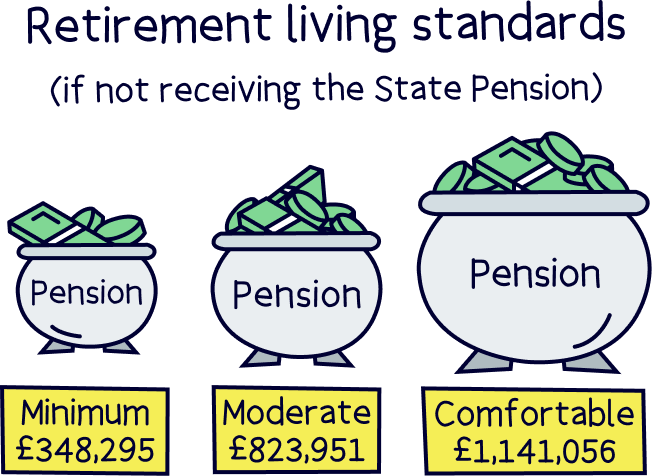

Here's where reality hits home! Retirement income (your pension) can be placed into 3 retirement living standards – minimum, moderate and comfortable:

These are the official Retirement Living Standards set out by the Pensions and Lifetime Savings Association.

And here’s how much you’ll likely spend each year in retirement:

Probably a lot more than you were expecting?

There’s one major thing to point out here. These figures assume that you won’t have any housing costs (it assumes you had a mortgage and it’s been paid off). If you think you’ll be renting or paying off your mortgage later in life, you’ll need to add these costs on top – and they can be a lot.

Plus, if you want those little extras in life, perhaps some expensive hobbies like golf, or multiple holidays, you’ll need to add those costs on top too. Retirement can be pretty expensive!

However, there's help at hand. You could be entitled to the State Pension, which is what you could get from the government when you retire…

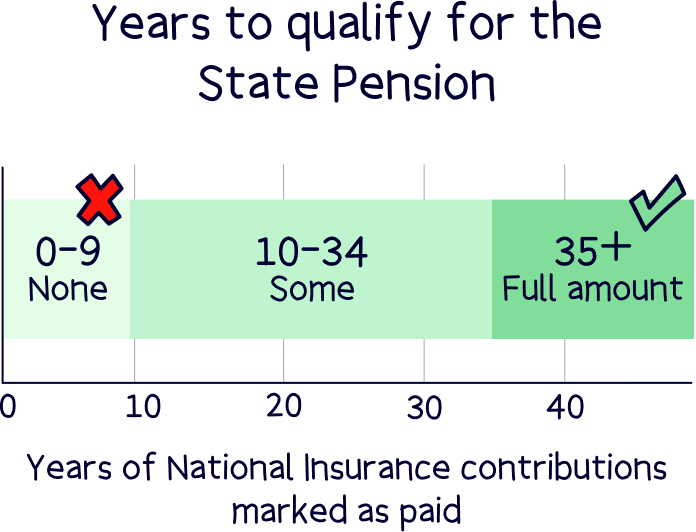

Before we get ahead of ourselves, you’ll need to know what the State Pension is, as it plays a vital role in how much you’ll need to save for retirement.

The State Pension is what you’ll get from the government when you reach the official State Pension age, which is currently 66, but rising to 68 over time. To qualify, you’ll need to have paid National Insurance contributions for at least 10 years, but to get the full amount, 35 years.

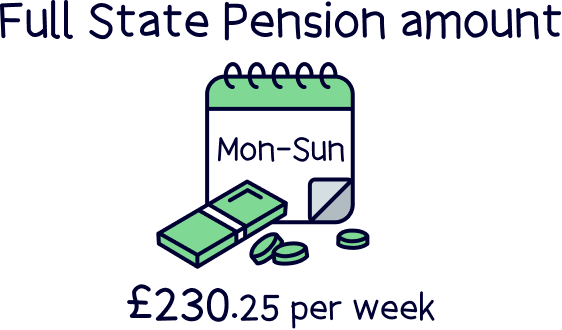

The full amount is £230.25 per week, which is £11,973 per year. It’s not a lot, and ideally you wouldn’t plan to live on just this, you would likely struggle. This supports your private pension, which we’ll cover below.

Let’s run through how you’ll need it in your pension pot to achieve those retirement standards.

And here’s what you’ll need in your pension with the State Pension removed (so, the amount you’ll need separate from the State Pension).

Pretty scary isn’t it? But don’t worry, pension pots can grow very large over time. We’ll run through how to increase yours later on.

You can also learn lots more about this with our guide: how much do I need in my pension pot?

And, check out our pension calculator to get a more personalised estimate.

To put it another way, to get an income to spend £13,400 per year in retirement, you’ll need to qualify for the State Pension (the government pension), and have an extra £88,958 saved in your own private pension (a pension in your own name, we’ll cover what private pensions are just below).

And if you won’t qualify for the State Pension, you’ll need a pension pot of £348,295.

To put it into perspective, this pension income is a lot less than the minimum wage, which is currently £23,836. You’ll likely struggle to maintain the same lifestyle you do if you’re currently working with just the minimum retirement standard.

We recommend aiming for a bigger pension pot if you can – and plan to make the full 35 years of National Insurance contributions if possible.

With a moderate retirement standard, so an annual spend of £31,700, which covers the essentials and a few of life’s small luxuries, but still not many, you’ll need to have saved a total of £564,615 in addition to the State Pension.

And if you’re not expecting to get the State Pension, you’ll need to have saved £823,951 in your pension pot.

Again, we’ll cover how to build up your pension pot below – these big numbers are from a lifetime of saving and your savings can really grow when saving into the right type of pension. We’ll run through how easy it is below.

A comfortable retirement works out as spending £43,900 per year. That covers all the basics and then some, with more luxuries such as a longer holiday each year. However, it doesn’t mean your lifestyle isn’t going to be like the rich and famous, you’ll mostly likely be similar to your lifestyle when you’re working.

With the State Pension, you’ll need to save £881,719 alongside it. And if you’re not expecting to get the State Pension, you’ll need to have saved £1,141,056 in your pension pot. Yikes!

This might seem out of reach, but it can be possible for you – trust us. As a reminder, PensionBee¹ is a great pension provider to use.

You’ve most likely worked out that the average UK pension pot is quite a bit lower than the recommended pension pot. And by quite a bit!

As a quick recap, the average pension pot from government data is:

Let’s take the average UK pension pot for someone aged 64, which is £107,300.

If they qualify for the State Pension, which most people who have worked for most of their lives will have. Then, they would be just below the ‘minimum’ retirement standards bracket. They’d roughly have an income to spend £14,000 per year from their pension.

If they didn’t qualify for the State Pension, their income would be a lot less, around £4,000 per year. And would likely have to continue to work into retirement. As a reminder, minimum wage is currently £23,836 – so your retirement income would be a lot less.

To get a moderate retirement, an income to spend £31,700, you’d need to save a total of £564,615, and that’s if you were also getting the State Pension. That’s around 5x more than the average pension pot at 64 years old (£107,300).

And for a comfortable retirement, you’d need over 8x the average UK pension pot (you'll need £881,719, plus the full State Pension).

So, instead of asking 'What is the average pension pot?' You should be asking 'How much do I need to save to have the retirement I want?'

We’ll cover how to increase your pension pot and contributions below, and you can use our pension calculator to get a personalised estimate.

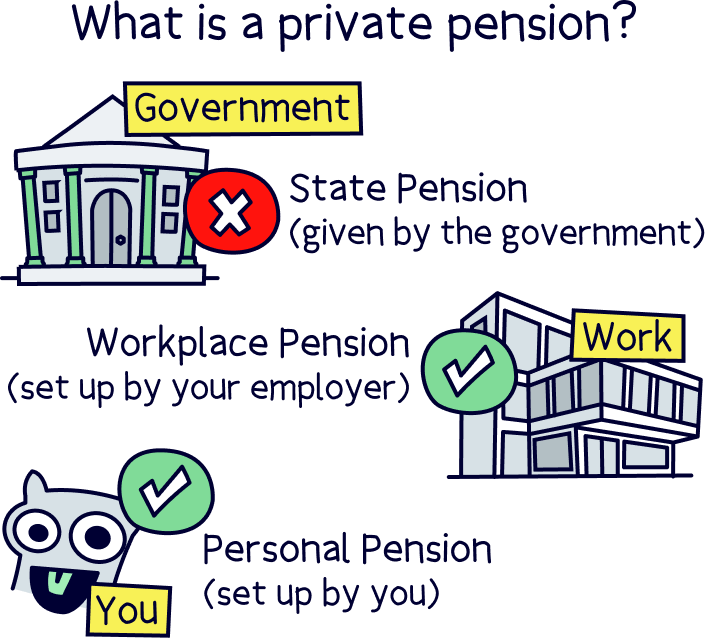

We’ve mentioned a few different types of pensions (and the State Pension above), but if you’re not sure what all the different types of pensions are, don’t worry! That’s why Nuts About Money is here. Lets run through them:

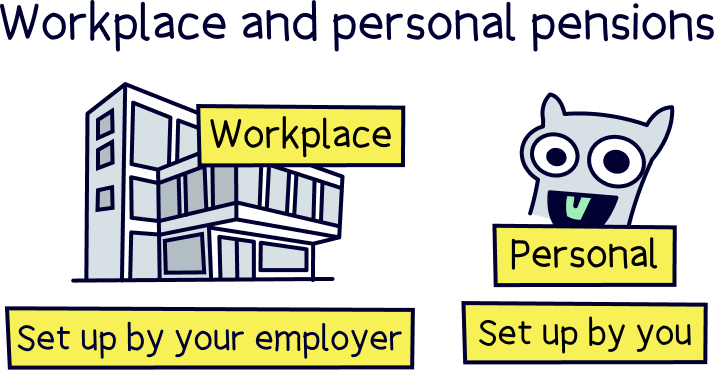

A private pension is a pension in your name and private to you (so not the government pension). You get to decide how much you pay into them, and you get to decide when you’d like to start taking your cash – as long as you’re over 55 (57 from 2028).

Here’s where it gets a bit more confusing, there’s different types of private pensions. You can have a workplace pension, and a personal pension. We’ll cover both below.

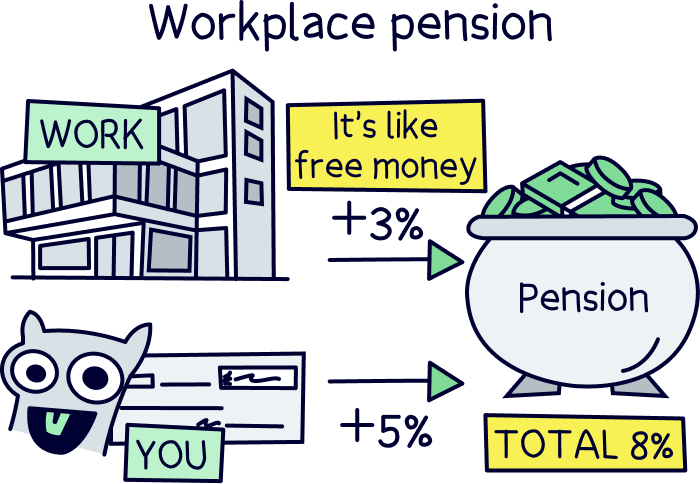

A workplace pension is a pension you’ll probably have if you are employed. Every employer has to set you up with a pension through the auto-enrolment scheme, and they have to contribute to your pension too!

If you contribute at least 5% of your salary to your pension, your employer will add 3% (by law). Pretty great right? It’s basically free money. This extra money can make a big difference to your overall retirement amount.

Some kind employers might even increase this too, and match your contributions if you pay more in. Speak to your HR team (human resources) to find out more.

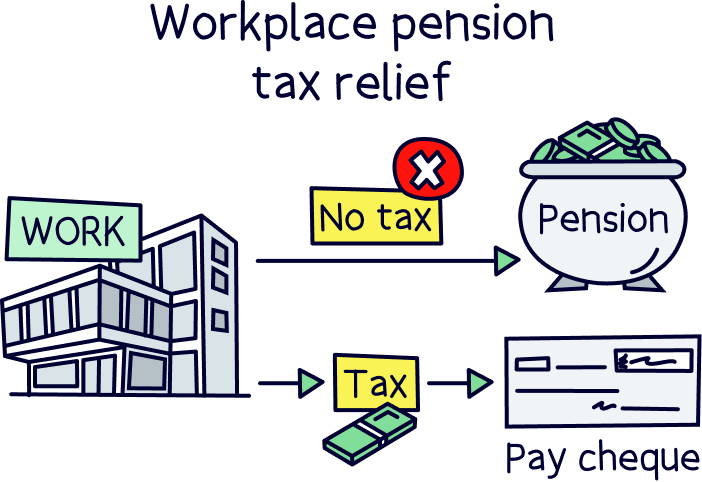

But not only that, with a workplace pension, your pension contributions are taken out of your salary before you pay any tax at all! Meaning your pension contributions are completely tax-free.

The downside is it’s up to your employer which pension provider they want to use, you don’t get to choose – and often they’re not the best pensions out there, with high fees and a poor performance of growing your money.

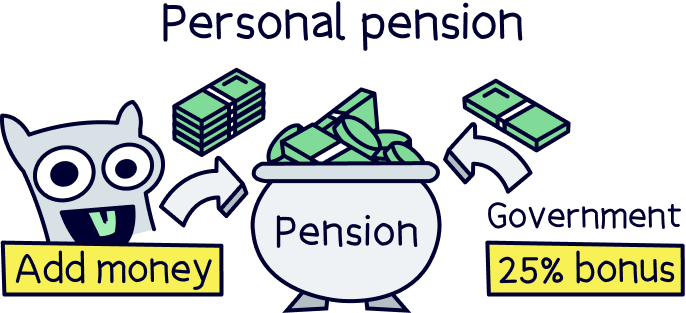

And that brings us onto personal pensions, where you do get to choose!

A personal pension is one that you set up yourself (don’t worry, it’s easy, we cover it below). It’s often used in addition to a workplace pension, or if you’re self-employed, it’s your only option to save for retirement (it’s a great option though). If you are self-employed, we’ve got a useful guide to the best private pensions for the self-employed.

With a personal pension, you get to choose which pension provider to use, so you can pick one of the best – one with low fees and a good record of growing money over time.

Not sure where to look? Check out PensionBee¹, they're 5* rated, easy to use, have low fees and a great track record of growing pensions over time. Here’s our PensionBee review to learn more. Alternatively, you can compare the best pension providers.

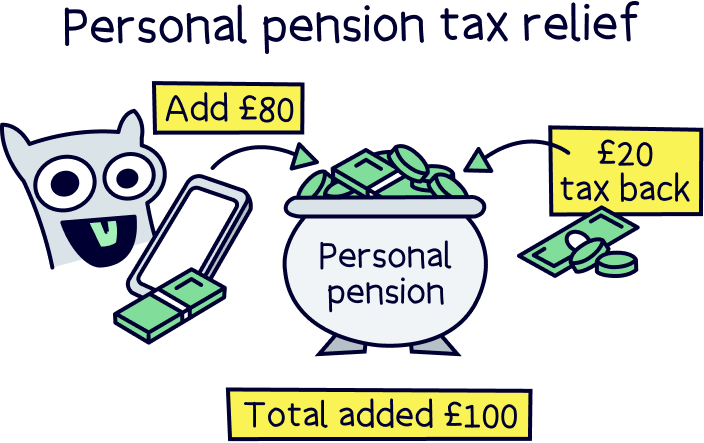

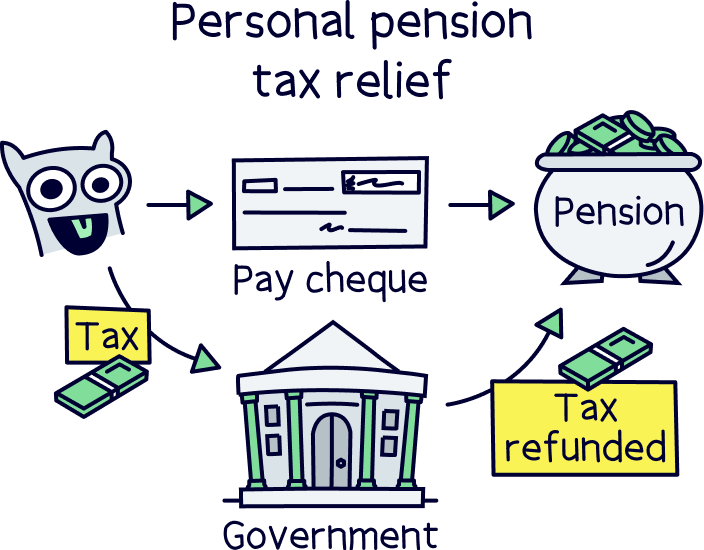

There's more good news, with a personal pension, you’ll get an automatic bonus of 25% of everything you pay into your pension from the government. Yep, we’re not joking!

As saving into a pension is supposed to be tax-free, the government refunds the tax you’ve already paid on your income straight into your pension pot. If you pay higher-rate tax (40%) or additional rate tax (45%), you can also claim this back too (on your Self-Assessment tax return).

A personal pension can really boost your pension savings – and we highly recommend it. We’ll cover how to get started and set up your own below.

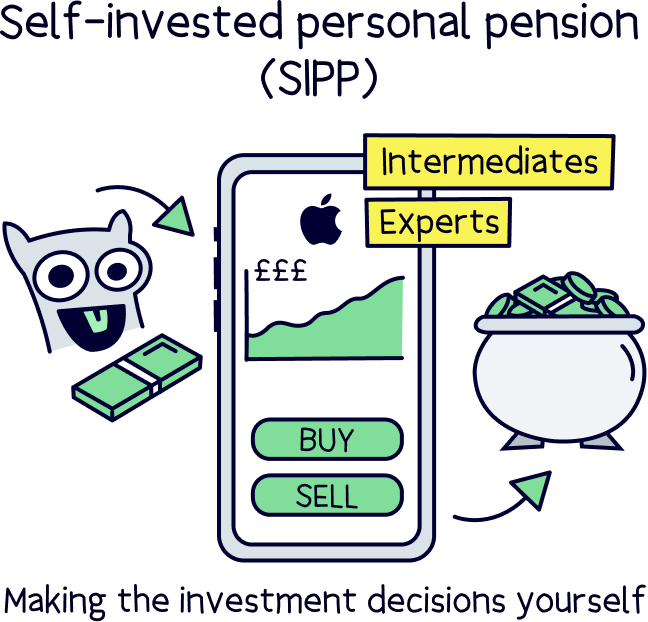

There’s also a self-invested personal pension, which is where you manage your own investments. Instead of the experts looking after your pension, you’ll be the one deciding which investments to make and when to buy and sell. These can often have lower fees as you aren't relying on experts.

We don’t recommend these for most people, but if this sounds like something you’d like to do, here’s where to learn more about self-invested personal pensions, and the best SIPP providers.

A bit worried you won’t have enough to retire with the lifestyle you want? You’re not alone. It's sensible to increase your pension savings if you can, and here’s how.

The answer is pretty simple – time!

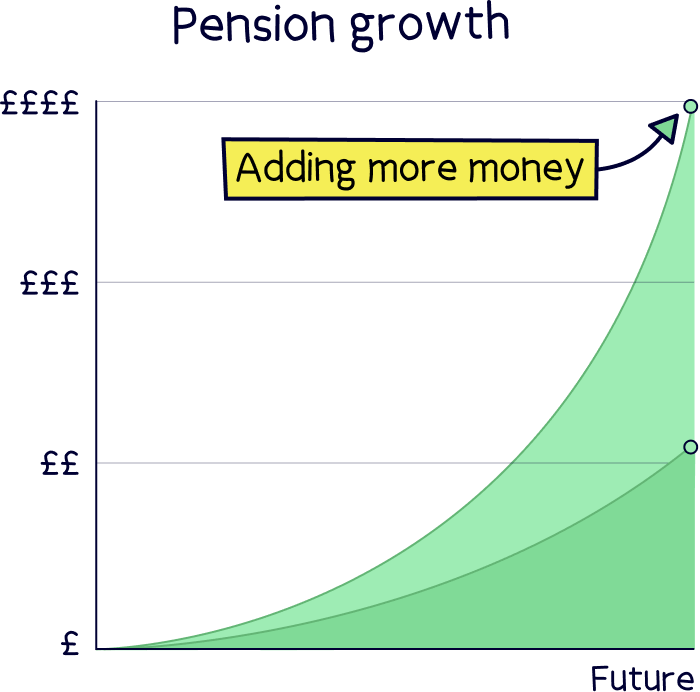

Over time your pension pot grows bigger and bigger. But in order to really benefit, you need to increase your pension contributions each month, and by doing this, over time your money will compound, meaning it will grow much more than the actual total of your contributions.

How? Well, your pension earns money itself (from it being invested), and the money it makes, begins to make money too, and this snowballs over and over.

Your money is pooled together with other pension savers into a pension fund. And this money is then invested in things such as:

The experts managing your pension (the pension fund), will use investment strategies to grow your pension in a safe and sensible way over time, all while being constantly monitored and the investments adjusted when needed.

And by doing this, small sums can become large over time, thanks to compound interest.

Let’s look at a quick example. Let’s say you have £500 to start with and after one year it has increased to £550, so 10%, you’ve made £50. The next year it also increases by 10%, but this time you are making 10% on £550, and so you’ve now made £60.50, and the next year you earn money on the £60.50, and this carries on over and over. It’s so powerful, Einstein called it the 8th wonder of the world, and he knows a thing or two about maths!

Given long enough, your monthly pension contributions can grow into a very large pension by the time you retire.

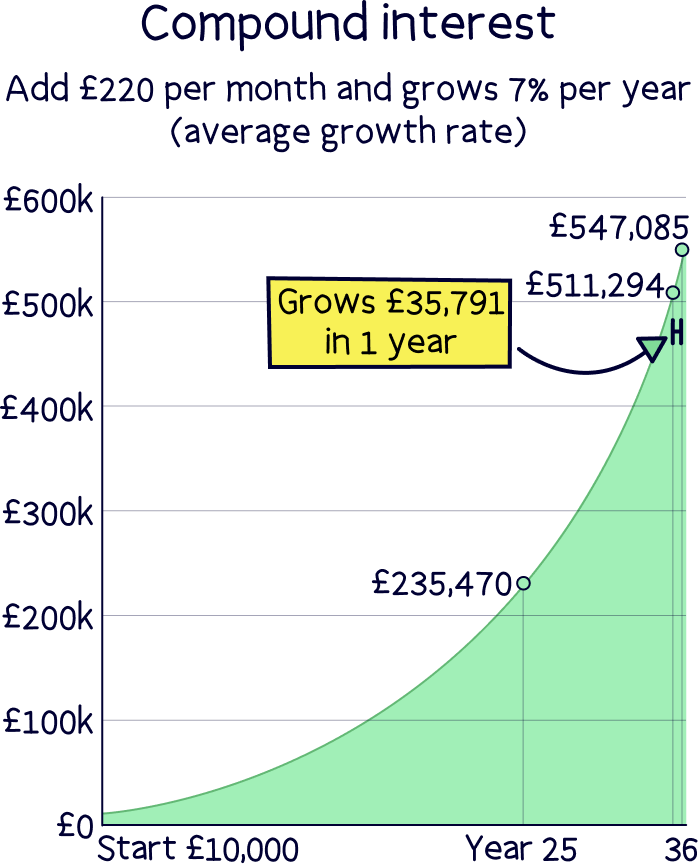

To use a real life example, if you earned the average salary of £33,000 per year, and have already managed to save a pension of £10,000, with a workplace pension, you’ll be adding 8% to your pension each year (5% from you, and 3% from your employer), which is £220 per month.

If your pension pot grew 7% per year on average, after 25 years, you’d have saved £235,470. Not bad right? And if you saved for another 10 years, you’d have £511,294. Wow!

After that, you’d actually be making more money from your pension, £35,791 per year, than your salary (£33,000). Pretty great right?

Now let’s run through how you can benefit from this yourself by how best to increase your pension contributions.

One of the key ingredients to pension wealth is increasing your monthly pension contributions and letting compound interest work its magic over time.

You’ve got 2 options when it comes to increasing your pension contributions, either increase your workplace pension contributions if you are employed, or use a personal pension.

We strongly recommend only adding more money to your workplace pension if your employer is willing to match your increased contributions (e.g. more free money from your employer). If they’re not willing to add more, you’re normally better off with a personal pension…

By opening a personal pension, and making contributions directly yourself (which are still tax-free just like a workplace pension), you’ll be in control of your pension destiny.

You get to pick which pension provider you want to use, so you can pick one of the best ones out there, with low fees and a great track record of growing money over time – plus features like a mobile phone app with up-to-date information on your pension. They’re super easy to use and set up too.

And, you get to decide where your money is invested, for instance, you could pick a pension plan that only invests in socially responsible investments (e.g. no fossil fuels) – we're big fans of these here at Nuts About Money.

If you’re not sure where to find the best personal pensions, we’re here for you. We’ve reviewed the best pension providers, and here are the top ones:

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

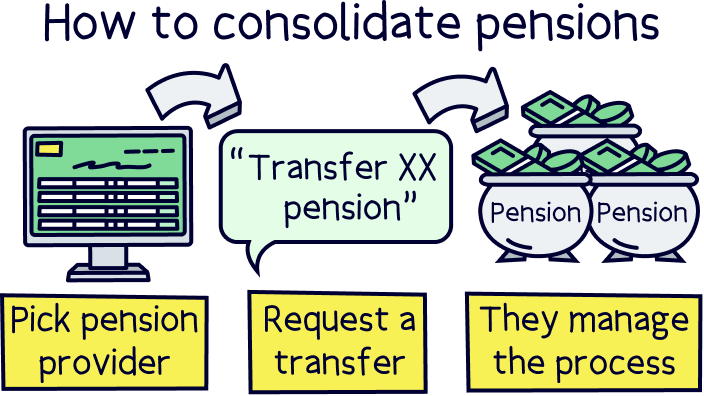

With a personal pension, you can also combine all of your old pension pots into your new one, which is called consolidating your pension.

This is often a good idea to do, as:

Consolidating your pension is easy to do too – if you move to a good pension provider, they’ll actually handle everything for you. All you need to do is let them know who your pension providers are. If you’re not sure, ask your old employer, they’ll let you know. It’s as simple as that!

If you think you might have one, or a few pension pots that you’ve forgotten all about, it’s a good idea to try and find these as soon as you can – don’t wait until you reach retirement age (your memory might not be what it is now!).

They could be better off with a pension provider with lower fees and possibly better pension growth to help boost your pension pot over time, and help you get towards the retirement lifestyle you’d like.

You can use the Government’s pension tracing service to find a lost or forgotten pension, or try Gretel.co.uk, a free service to help find lost pensions (and other investments).

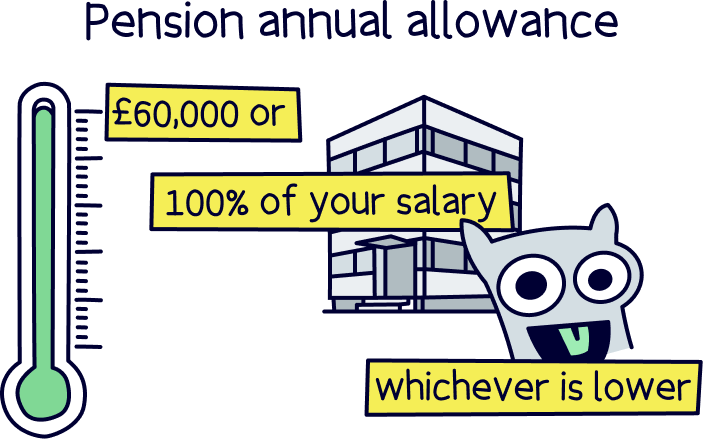

You might now be thinking about paying as much as possible into your pension, which is a good thought, and highly recommended! But there are some limits to be aware of – although they’re pretty high.

There’s a limit on how much you can pay into your pension each year, which is the total of your income (e.g. salary), or £60,000, whichever is lower.

If you think you might hit these limits, it’s often a good idea to save the extra within a Stocks & Shares ISA, where your money can still grow tax-free. Learn more with our guide to Stocks and Shares ISAs.

When it comes to retirement, you’ve got a few options to start taking your pension, and hopefully enjoy your retirement with a nice big pension pot.

At age 66 (rising to 68), you’ll be able to claim the State Pension. Although if you want to defer your State Pension, you can, and you’ll get bigger monthly payments when you do start taking it.

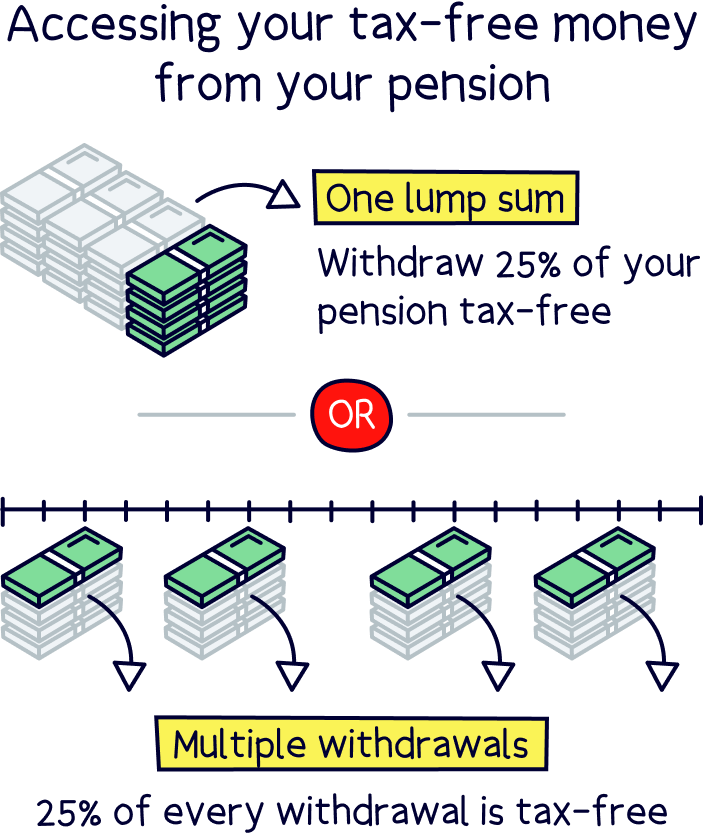

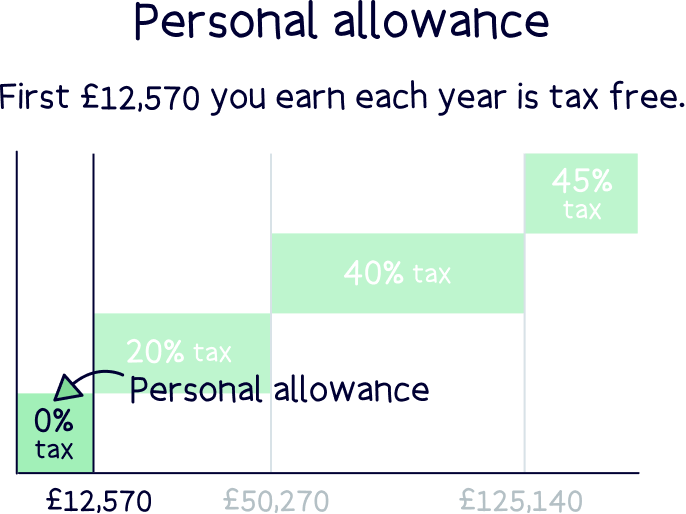

When it comes to your private pension, such as a workplace pension or personal pension, you’ll be able to start taking this from age 55 if you like (57 from 2028). And the first 25% of your pension is completely tax-free – so no tax to pay at all, and you can take this as a tax-free lump sum if you like (so all in go).

With the remaining 75%, you may have to pay Income Tax on it – but it will depend on what your income is at the time, as you’ll still get your tax-free Personal Allowance, which is currently £12,570. Meaning you don't have to pay tax on the first £12,570 you make each tax year.

However, when you start withdrawing your pension, the amount you can contribute to your pension will typically reduce to £10,000 per year (from the current limit of either your salary or £60,000, whichever is lower), so it’s often a good idea to keep building up your pension as much as possible until you’re truly ready to start taking your pension.

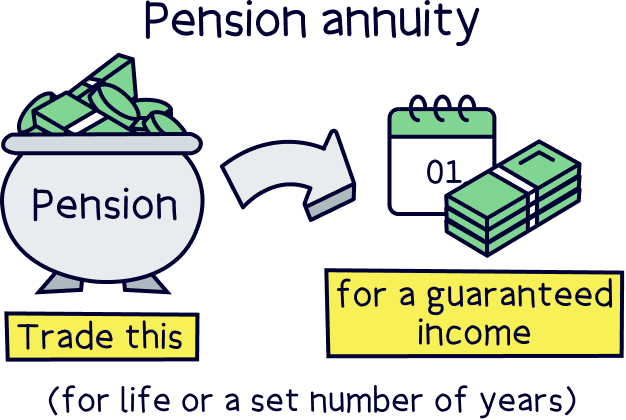

And finally, when you do retire, you can either use your pension pot to buy an annuity, which is a guaranteed monthly income for the rest of your life (or a set number of years), or simply keep your pension pot where it is and withdraw cash from it each month. Your pension provider will often run through your options at the time, and you can also get advice from a financial advisor.

We hope that wasn’t too complicated, or too depressing! To have a comfortable living in retirement, your pension pot is going to need to be pretty big – as much as £1,141,056 (not including the State Pension) to have a retirement income of £43,900 per year.

The good news is that it can grow very big over time, thanks to government help, experts growing your money and compound interest (the money you make, making more money) – but it does mean you need to be contributing to your pension regularly if you can. If you are close to retirement try and add as much as you can afford.

The main issue here is that the average UK pension pot is much smaller than the recommended pension that you’ll need – the UK is actually in a crisis when it comes to pensions. It’s best to ignore what other people are doing, and focus on the recommended pension pot figures.

The State Pension can go some way to help, especially contributing to the minimum retirement standard of living, but it’s up to you to build up the rest of your pension pot!

We recommend opening a personal pension. With this, you’re in control of your pension, you get to pick the best provider – one that’s easy to use, has low fees and a great track record of growing pensions over time.

If you’re not sure where to find the best pension provider for you, check out our best private pensions.

All the best with saving, your future self will really thank you!

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.