Article contents

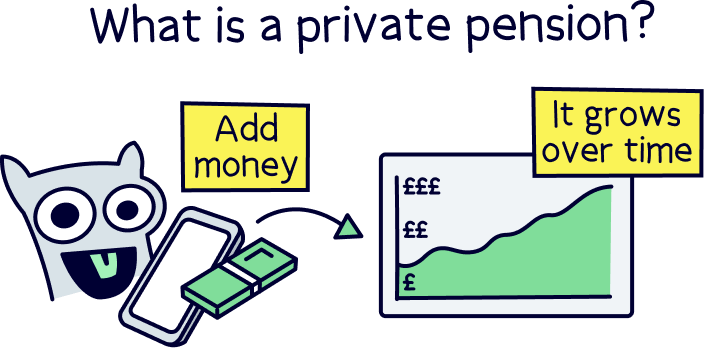

A private pension is a bit like a piggy bank – you pay money in while you’re working, and then you can access your savings when you retire (currently when you’re at least 55). If you have an employer, they’ll normally set one up for you, but you can set one up yourself too.

Whether you’re miles off from retirement or you’re counting down the years, one thing’s sure. A private pension is a great way to make sure you have enough money to tide you over later on in life.

But you might be wondering… what exactly is a private pension? Don’t worry, they’re a lot more straightforward than you might think! Here, we’ll break it all down for you.

A private pension is a special kind of savings account that helps you to squirrel money away ready for retirement. It works a bit like a piggy bank – you pay in money throughout your working life and then when you hit the grand (not-so-old!) age of 55 (57 from 2028), you can normally start taking your money back out.

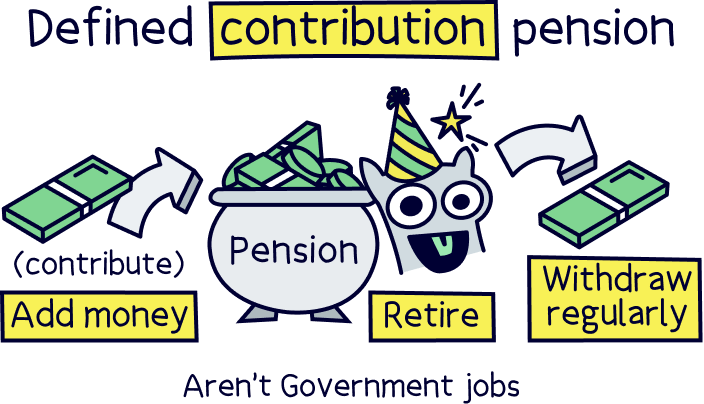

Private pensions that work this way are also known as defined contribution pensions. If you have an employer, the chances are that they’ll set one up for you. But you can also set a private pension up yourself, called a personal pension.

We know what you’re thinking: they sound like any other kind of savings account – what makes them so special?

Well, the savings in your private pension pot will grow over time, without you having to do a thing! That’s thanks to the fact your private pension provider (the company that looks after your pension) will invest your money, which is when they use your money to buy things like stocks and shares (ownership stakes in companies). The idea is that when these increase in value, your savings will too – your money will be handled by experts who know what they’re doing!

On top of this, the government wants to encourage you to save up for retirement so they’re not left propping you up when you’re old and grey. So, you won’t have to pay any tax on the money you put into your pension pot. Kerching!

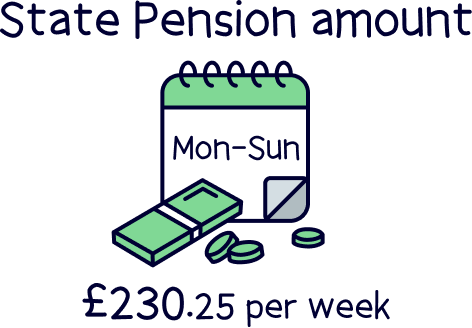

When you reach retirement age (66 now but 67 from 2028), technically called the State Pension age, the government will give you a pension too (the State Pension). However this is likely to be pretty low. Currently it’s just £230.25 per week. Which is why a private pension is strongly encouraged!

We’ll tell you more about why private pensions are so great a bit later. But for now, let's run through how they work.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Find the best personal pension for you – you could be £1,000s better off.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Good question (if we do say so ourselves!). There are two main types of private pensions, and they work a bit differently depending on what kind you have (not that you have to choose between them, as you can have as many pensions as you want!).

Here’s the lowdown.

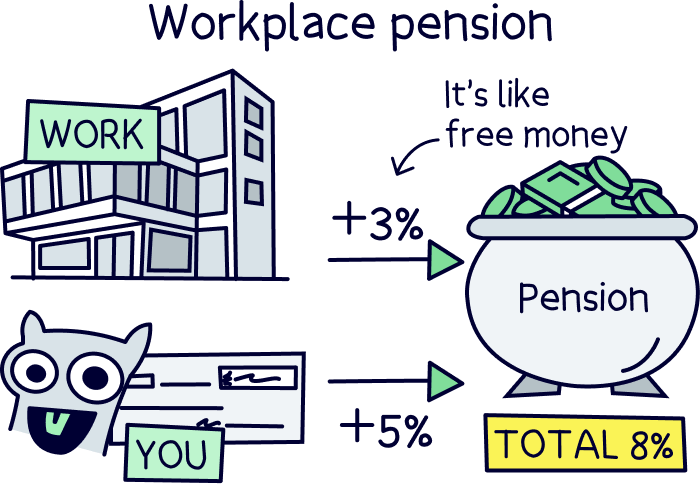

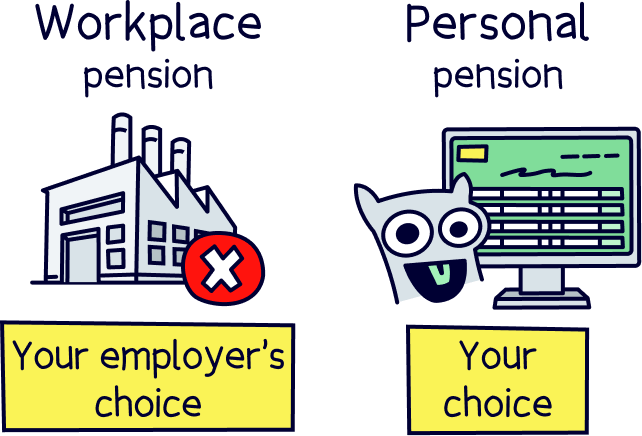

A workplace pension is a pension your employer sets up for you. Yep, that’s right, the chances are your employer will legally have to set you up a pension (called auto-enrolment). Nice!

Technically, there are a couple of different types of pensions they could give you. But in reality, they’ll almost definitely set you up a private pension (defined contribution pension). So, if you’re not sure what kind of pension you have, you can be 99.99999% sure it’s one of these (okay, we made that stat up but you get the idea!).

If you have a workplace pension scheme, you’ll have to put a percentage of your salary into your pension pot each month – at least 5%. But guess what? Your employer will have to contribute to your pension too!

They have to add at least 3% of your earnings themselves, out of their own pocket. This means that workplace pensions are an amazing way to unlock free money from your employer. It’s like a free pay rise – get in!

An alternative type of pension scheme is defined benefit pensions. And these are common in large public organisations such as the NHS. They pay a set amount when you retire depending on how long you have worked there, and how much you earn. (A final salary pension is an example of this).

A personal pension is a pension that you set up yourself. Pensions you set up yourself are always private pensions and anyone can get them. That means they’re especially useful if you’re after a self-employed pension, although they’re great if you’re an employee too!

Sometimes, people use the term ‘private pension’ to mean ‘personal pension’ so it can be a bit confusing! However, personal pensions couldn’t be any more straightforward if they tried. If you choose the company, like PensionBee, they’re quick to set up, easy to understand and really helpful when it comes to building your savings up for retirement.

With a personal pension, you can choose how much money you want to pay in throughout your working life. You might want to set up regular monthly payments. Or, if you prefer, you can just add money into your pension pot when you have some cash to spare.

Perhaps the best thing about personal pensions though is that you get to choose your pension provider (remember, that’s the company that looks after your pension) – unlike with a workplace pension, where your employer will choose your pension provider for you. That means you’ll usually be able to get cheaper fees and a provider who’s got a great track record for growing money quickly. Like when you choose a mobile phone contract, a personal pension means you can shop around for the best deal!

There’s also another type of personal pension, which is a self-invested personal pension (SIPP). This is where you decide which investments to make within your pension, rather than the experts handling everything for you. You still get the lovely tax relief benefits (more on those later).

We only recommend this if you know what you’re doing. If you’re interested, here’s the best self-invested personal pensions.

A private pension isn’t the only way you can save up to tide yourself over in retirement. You could use another kind of savings account (like an ISA), you could sell a property, or you could rent a house out. Or a combination of lots of different things!

But starting a private pension is a really good shout if you’re looking to make sure you can live out your golden years in style. They’re specially designed to make it extra easy for you to save for retirement, which means they have some pretty unique benefits. Here are the main ones.

Remember how we said that you don’t have to pay tax on the money you pay into your pension? Well, this is known as tax relief. And it’s pretty awesome.

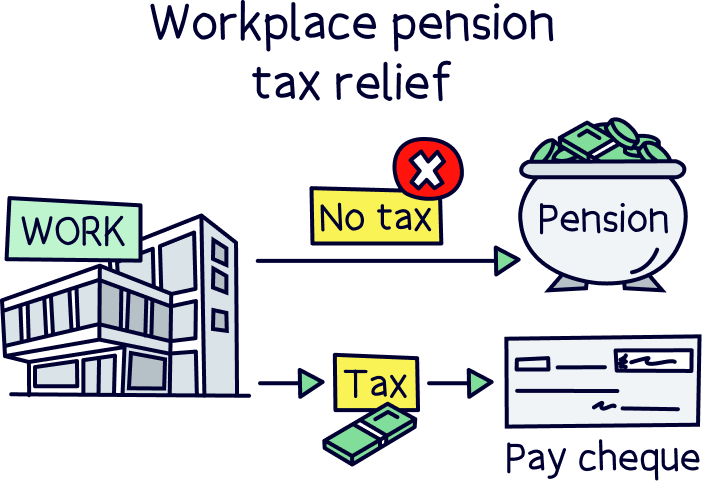

How it works will vary a little bit depending on whether you have a workplace pension scheme or a personal pension scheme. If you have a workplace pension, your pension contributions will get deducted from your payslip before it’s taxed, which means you’ll never pay tax on that money in the first place. So, it’s a great way to get more cash in your own pocket and less going to the taxman (or taxwoman!).

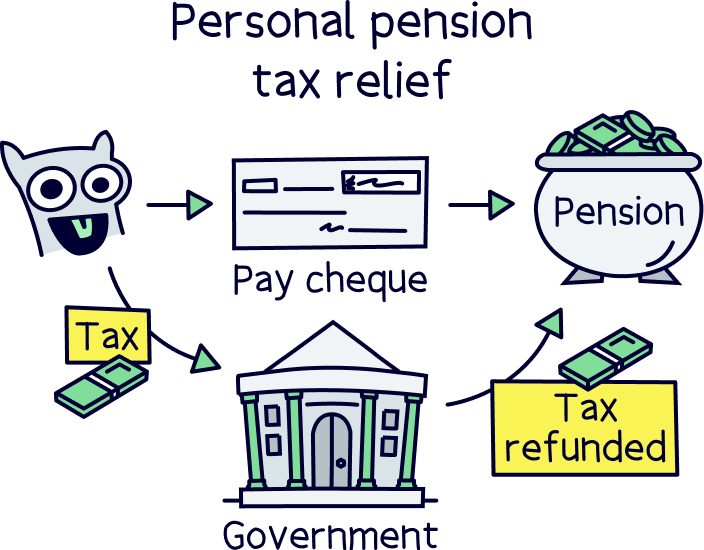

On the other hand, if you have a personal pension, you’ll pay tax on your income like normal. But then, the tax you’ve paid on the earnings that have gone into your pension will be refunded straight into your pension pot – normally automatically. Kerching!

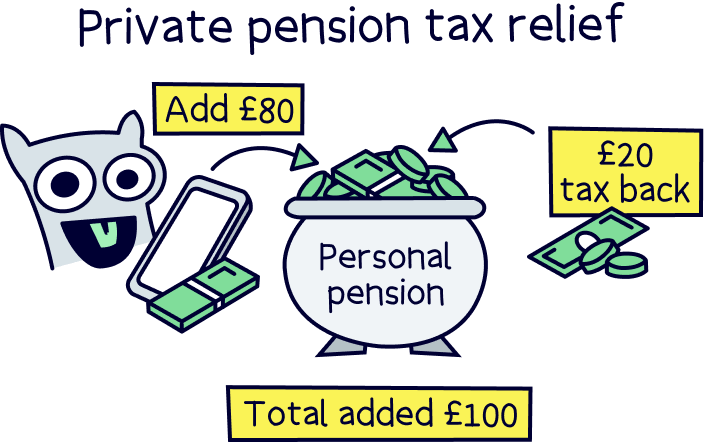

That means each time you add money into your pension, it’ll be topped up by a tasty bonus from the government. If you’re a basic-rate taxpayer (meaning you earn less than £50,270 per year), you’ll get 20% tax relief. In other words, if you pay £80 into your pension pot, the government will add a £20 bonus to turn it into £100 (£20 is 20% of £100).

If you pay more tax, however, you can get an even bigger bonus to make up for it. Higher-rate taxpayers can get 40% tax relief on any income they’ve paid 40% tax on. And additional rate taxpayers can even get some tax relief at 45%. So, if you’ve got some cash to spare, chucking some into a personal pension could be a seeeeriously good move. (You’ll need to claim this yourself on a Self Assessment tax return).

Here’s another wonderful thing about private pensions: your money can grow while it’s sat in your pension pot without you having to do a thing! That means you can expect to get a lot more money out of your private pension than what you put in.

This is all because your pension provider will spend time trying to grow it for you, by investing it (together with other people's money within a pension fund or investment fund). Investing is when your money is used to buy things like stocks and shares, which are essentially small ownership stakes of companies. As those investments increase in value over time, your savings do too!

Now, it’s true that investments don’t just go up in value – they can also go down. But before you panic, it’s important to remember that pensions are about growing your money in the long term. Pension providers are experts who’ll put your money in a range of different investments meaning that, over a long period of time, they’ll go up overall.

So, start getting excited as you’ll have way more money to enjoy in your golden years than what you put into your pension pot in the first place. Cruise, anyone?!

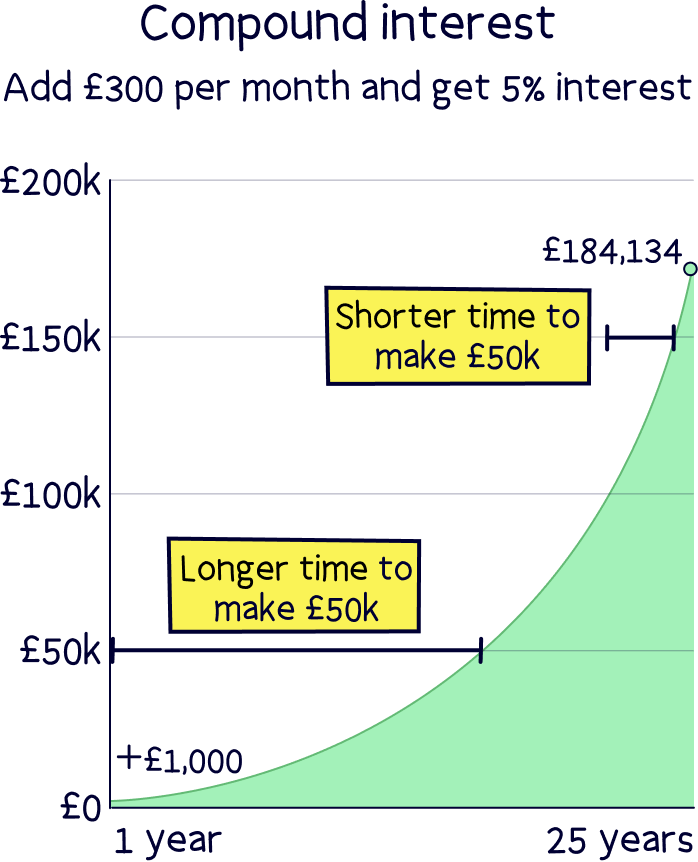

Want to know another reason why your money grows so quickly when it’s sat in your private pension pot? A little clue: it’s to do with something called compound interest.

Compound interest (also known as compounding interest) refers to the fact that when your savings grow, the extra money you’ve made (known as your return), will then grow too. This creates a snowball effect where the more your money grows, the faster it can continue to grow in future.

Mind boggled? Don’t worry, it’s not as complicated as it sounds. Let’s look at an example.

Imagine you squirrel £1,000 into your private pension pot this year. And imagine you make a 5% return (that means profit, remember). Your savings will have increased by £50 and you now have £1,050 in your pension (all without you having to lift a finger!).

Now let’s say you also make a 5% return the next year. 5% of £1,050 is £52,50, so now you’ve got £1,102.50 in your account. All without you adding another penny or doing a thing!

Your money will keep growing like this every year, which means even the tiniest amounts you add to your private pension can turn into fairly large amounts after a long period of time. If you continue paying into your pension over the years as well, it’ll get even larger – going back to our previous example, if your money kept growing like this for 25 years and you also added £300 into your pension every month, you’d end up with £184,134.20! Another 10 years and you’d have a whopping £346,561.45 – almost double!

Finally, let’s end on one that’s a little bit more obvious but still just as great! You can’t withdraw your pension before 55. Well… you technically can, but you really shouldn’t because it would mean getting hit with the most massive tax bill (as much as 55% on the money you take out!) as well as other hefty fees. Gulp!

Now, we know what you’re thinking: ‘how is that a good thing?!’

Well, it means you won’t get tempted to spend the money you’ve carefully stashed away for retirement!

With regular savings accounts, it would be easy to dip into your savings from time to time. So, you could very easily end up depleting your funds before retirement – putting all your hard work to waste!

On the other hand, with a private pension, your money is locked away in an account that’s specially designed to tide you over later on in life. You won’t be able to dip into it each time you’re short on cash, so assuming you struggle to avoid temptation like most of us, that means you’ll probably have more money to live on in your golden years. Which is really what a pension is all about!

So, you’re sold on the idea of a private pension. Go you! But should you be getting a workplace one or a personal one?

Well, if you have an employer then you’ll probably already have a workplace pension – unless you earn very little. That’s because as long as you earn over a certain amount each year (currently £10,000), they’ll normally be required to set one up for you automatically by law.

If your employer offers you a workplace pension, we have one thing to say to you: you should definitely take it. That’s because they’ll have to contribute to it alongside you, from their own pocket – so really, it’s free money!

However, if you have some cash to spare (or you don’t qualify for a workplace pension for whatever reason) it’s super sensible to get a personal pension as well.

Why? Well, personal pensions are ones you set up yourself, which means you’ll get to choose a pension provider that works for you. In other words, you can choose a pension provider that has super cheap fees. And you can also choose one that has a great track record for growing money quickly – so that you’ve got even more savings to enjoy later on in life!

Not only that, but personal pension providers tend to be more flexible – most will let you pay as much or as little into your pension as you want, whenever you want. Oh, and some more modern pension providers like PensionBee and Beach¹ even have handy apps that make it super easy for you to track your savings and watch them grow (over the long term!) ready for retirement. More on them later!

Like we said, you probably won’t need to worry about getting a workplace pension as, if you qualify, your employer will normally sort this out for you automatically. However, if you want a personal pension as well (hint hint, it’s a super sensible idea!) then you’ll need to start one yourself.

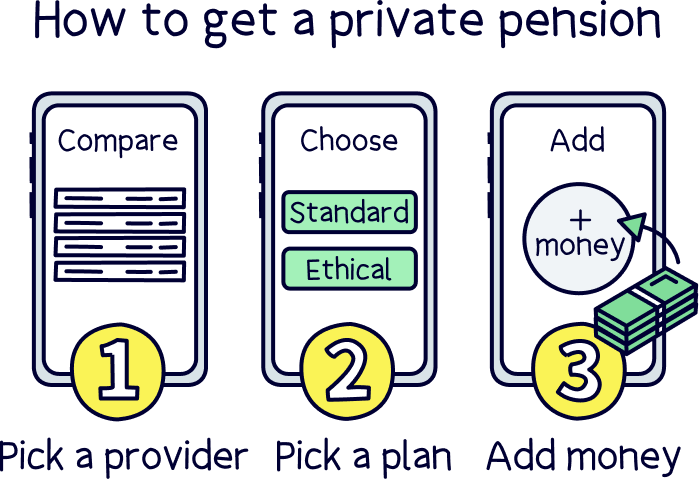

Don’t worry, it’s really quick and easy. Especially nowadays! Just follow these simple steps.

First things first, you just have to choose a company to look after your pension for you. That means now’s the time to go on the hunt for one of those amazing companies we were talking about that have an excellent track record for growing your savings, and lovely low fees.

Not sure where to start? Don’t worry, we’ve done the hard work for you – just check out our selection of the best personal pensions.

A couple that deserve a special mention are PensionBee and Beach¹.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Find the best personal pension for you – you could be £1,000s better off.

Now you’ve signed up with a pension provider, you can pick a plan. That basically just outlines how your money will be looked after, what fees you’ll pay for the benefit, and what funds your money will be invested in (a fund is when lots of people’s money is pooled together in a collection of investments to help your money grow).

Don’t panic if that all sounds hard. It’s not! Your pension provider will help you pick the right plan for you – normally by asking you a few questions about your age and when you think you might want to retire.

There’s just one thing left to do – start adding money into your pension pot so you can start paving the way for a glorious retirement!

Some pension providers will want you to add a certain amount of money into your pension to start with, while some will want you to set up regular monthly payments. However, most of the more modern pension providers are much more flexible and will let you add as much or as little as you want!

Of course, the more you add to your pension pot, the more financially secure you’ll be later on in life – so it’s always sensible to set up a regular monthly payment if you can. However, it’s important not to overstretch yourself either. Remember, you won’t be able to withdraw your pension before 55 so it’s all about finding the right balance between enjoying yourself now and enjoying yourself later!

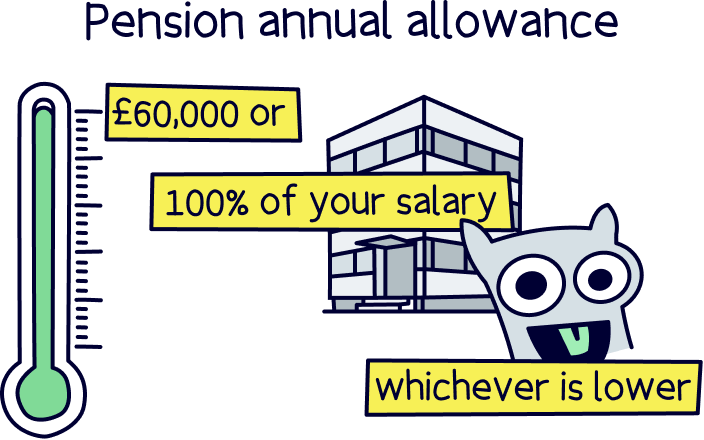

We know private pensions are great right?! And you want to pay in as much as possible as you can? Good idea!

However, there are a few rules. The first is that you can’t save more than your total income within a tax year (April 6th to April 5th), or more than £60,000, whichever is lower. Which is called your annual allowance.

At the end of the day, a private pension is a really sensible thing to get – it’s designed to make it easy for you to save for later on in life, while also reducing the money you end up having to pay to the government through taxes. What’s not to like?!

If you’re an employee, you’ve probably already got a workplace pension (or a few if you’ve changed jobs a few times). But either way, getting a personal pension too is a great way to boost your savings in retirement.

If you’re not sure where to start, just check out our selection of the best personal pensions. Or, you can read our PensionBee review. PensionBee is for you if you want a quick and easy way to start saving for retirement, with cheap fees and a handy mobile app to boot. And you’ll love Beach¹ if you’re keen to save within a pension and an ISA (for general savings) at the same time.

Whichever provider you choose, one thing’s sure: by getting yourself a pension, you’re giving yourself the best possible chance of living life to the full in your golden years.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.