Article contents

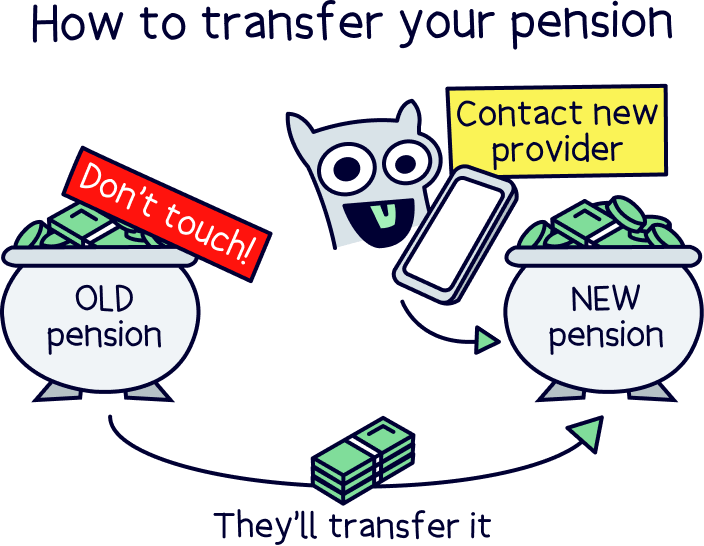

Transferring your pension is easy! Just give your new pension provider the name of your old pension provider and they’ll sort everything out for you. Then, sit back, relax and wait for the funds to land in your new pension pot in around 2 to 4 weeks.

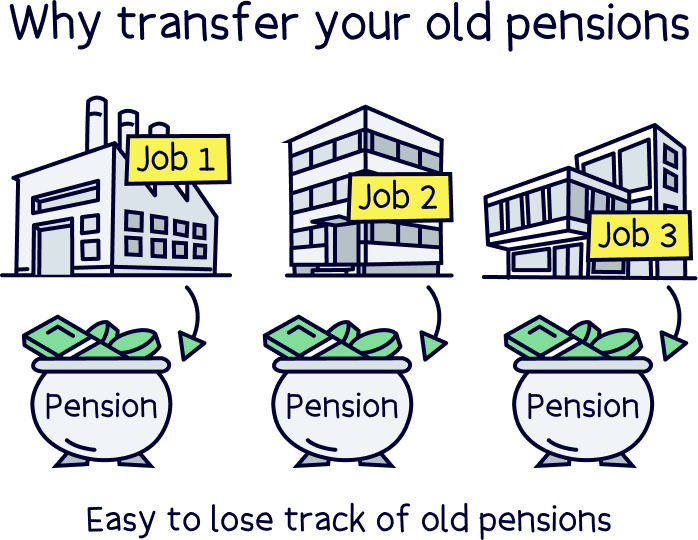

If you’ve had lots of different jobs, it can be easy to lose track of your old pensions. In fact, The Association of British Insurers found that there are around 3.3 million lost pension pots in the UK. Altogether, they’re worth around £31.1 billion! Gulp.

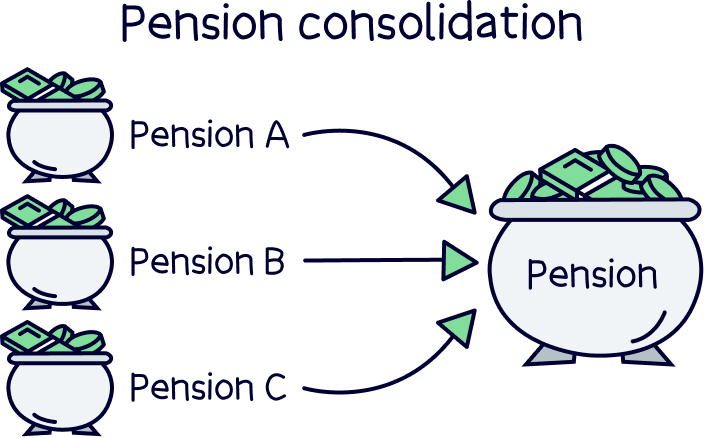

But don’t worry! By transferring your old pensions to a new one, you can keep them all together in one easy-to-manage place, so you know exactly where they are when you come to retire. Phew! Here’s everything you need to know about transferring your pension.

Let’s start with the basics! A pension transfer is when you transfer your existing pension funds from one pension provider to another (your pension provider is the company that looks after your pension for you). Simple!

A lot of the time, people choose to do a pension transfer because they’ve changed employers. Let us explain.

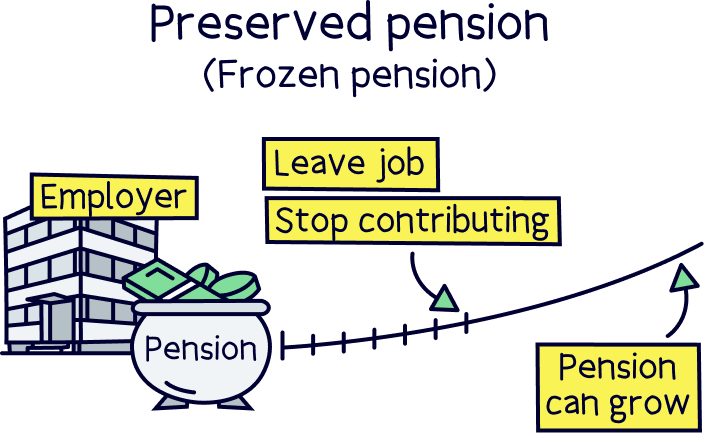

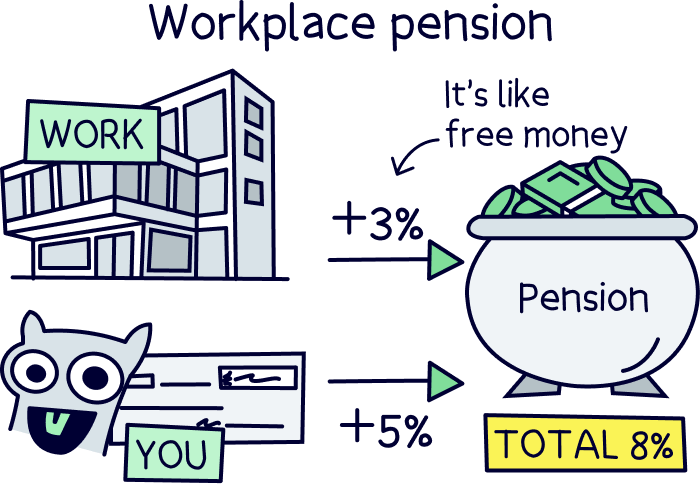

If you’re an employee, the chances are you have a workplace pension – that’s a pension your employer sets up for you. You’ll be contributing a percentage of your earnings to it every month (at least 5%). And your employer has to contribute to it too, from their own pocket (at least 3%). Kerching!

However, if you change employers, you’ll stop contributing to that pension and it will become ‘frozen.’ Meanwhile, your new employer will usually set you up a different workplace pension, with a provider of their choice.

You can just leave your old pension where it is with your existing pension provider until you’re ready to withdraw your pension – the money in it is still yours and it’s not going anywhere! However, it can be easy to lose track of where your old pensions are as you won’t be able to cash in a pension from an old employer until you’re at least 55! Plus, you’re probably not getting the best deal and there’ll be other pension providers who are likely to be able to grow your money quicker.

That’s where a pension transfer comes in. By transferring all your old existing pensions over to just one, you’ll be able to make your savings easier to manage, find cheaper fees and get better performing investments. Which brings us onto…

As you’ve probably already gathered, there are loads of positives to transferring your pension. Here are the main ones.

Find the best personal pension for you – you could be £1,000s better off.

Yes! It’s your pension, so you’re the only one that needs to do anything – your old employer doesn’t have to get involved at all. That said, depending on where you want to transfer your pension, you may or may not be able to choose your pension provider. Let us explain.

If you want to transfer your pension, you have two options. You can either…

We've written a whole guide on it too: can I transfer my pension myself?

Here’s the lowdown:

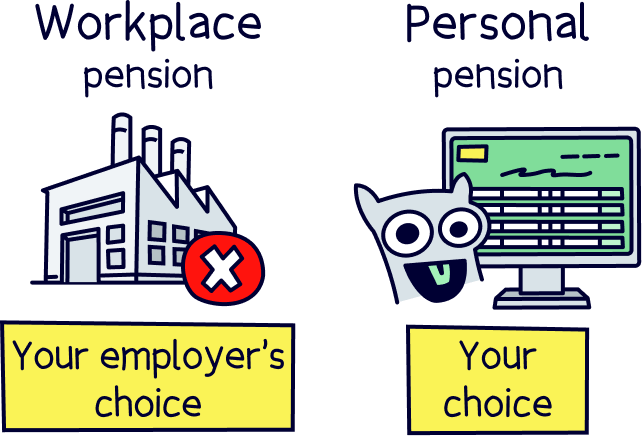

Now, we can’t tell you what to do. But if we can give you one little word of advice, it’s this: transferring your pension to a personal pension (one that you set up yourself) is a really good idea.

That’s because when you start a pension yourself, you get to choose your own pension provider, and so can generally pick a better pension scheme.

In other words, you can choose a pension provider with lovely low fees. And you can choose a pension provider that has a proven track record for growing money quickly. So, you’ll be in the best possible position to end up with even more savings to enjoy in retirement!

You might think that starting your own pension sounds like a lot of work. But guess what? It’s not!

Setting a pension up is quick and easy. In fact, it can take as little as 5 minutes – especially if you use one of the more modern pension providers that we love, as they let you do it all online.

You can check out our selection of the best personal pensions to see what we mean. But two that deserve a particular shoutout are PensionBee and Beach¹.

PensionBee is a super simple option that specialises in pensions, with low fees and a handy app that lets you track your money and watch it grow. Meanwhile, Beach¹ is also super simple but has an easy access pot alongside a pension, for everyday savings.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Find the best personal pension for you – you could be £1,000s better off.

Now, to be clear, we’re not suggesting you should turn down the workplace pension your new employer offers you, as your employer will have to contribute to it from their own pocket. You should take all you can get! Instead, we’re saying you should start a personal pension alongside it, and transfer any old pensions to this one instead. Then, you get the best of both worlds!

If you have a new employer, the chances are they’ll be setting up a new workplace pension for you – normally, they’ll have to by law! (This is part of the auto-enrolment process.)

Just like with your old employer pension, you’ll need to pay into it every month (at least 5% of your earnings). And, just like your old one, your employer will have to contribute to it too (at least 3% of your earnings from their own pocket!). Get in!

If you want, you can choose to transfer your old workplace pension to your new one. Some people choose to do this so that they only have one pension going at a time.

You’ll still get some of the benefits you would from transferring your pension to a personal pension. For instance, it’ll be easier to keep track of your savings if you gather all your old pensions in one place. And it’ll cut down the number of providers you’ll need to pay fees to as well.

However, there’s one big downside: you won’t get to choose your own pension provider.

Instead, you’ll end up transferring your old pensions to whatever pension provider your new employer has picked out for you. And, we hate to break it to you, but this is unlikely to offer you the cheapest fees or the highest growth. In other words, you’ll probably end up paying more than you need to, and your money probably won’t grow as quickly as it could.

So, workplace pensions are wonderful things and you should definitely get one if you’re offered one. But when it comes to transferring your old pensions? Personal pensions win every time if you’re looking to boost your savings in retirement!

Luckily, transferring your pension from a previous employer can be oh-so-easy. And we mean it! Just follow these 3 simple steps.

First things first, you’ll need to choose where you want to transfer your old pension to.

We’d recommend starting a personal pension if you haven’t already, as that way, you’ll get to pick the best pension provider for you. That means you’ll be able to access lower fees, and you’ll also be able to choose a provider who has a good track record for growing pensions quickly!

Not sure where to start? We love PensionBee as it has a great track record for growing your money, an amazing customer service team and an easy-to-use mobile app. That’s right, you can check in on your pension and watch your money grow (over the long-term!) whenever you want, wherever you want!

You also have the option of opening a Self-Invested Personal Pension and do a pension transfer to there. This is where you decide which investments to make, rather than the experts with the pension provider. It’s not recommended unless you know what you’re doing when it comes to investing. These are your retirement savings after all.

Alternatively, with Beach¹ you get a great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too). Plus the customer service is excellent.

PensionBee and Beach both have pretty cheap fees too! But before you decide for sure, check out our selection of the best personal pensions for more great options.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Next, you’ll just need to get the name of your old pension provider. If you’ve only recently changed jobs, the chances are you already know which pension provider is looking after your old pension. But if you’re not sure, don’t worry!

The government has a handy find a pension service – just go to GOV.UK to give it a try.

Alternatively, your new pension provider will often be able to help. Some of them have their own tools that can help you to find your old pension – often, you just need to enter the name of your old employer and voila! You’ll be able to see the details right there.

You just need to give your new pension provider the name of your old one and then…

Yep, that’s right, all that’s left now is to sit back, relax and let your new pension provider do the hard work for you.

They’ll get in contact with your old pension provider to arrange the pension transfer. Normally, the funds will then show up in your new pension within 2 to 4 weeks (although it could take longer).

Sometimes, your old provider will get in contact with you to confirm that you want to go ahead. But other than that, you can just twiddle your thumbs while your pension providers get to work!

You might be able to transfer your pension for free. Get in! However, it all depends on your pension providers.

Sometimes, your old provider will charge you a fee for leaving early, known as an early exit charge. Urgh! However, if you’re under the age of 55, they won’t be able to charge you more than 1% of the balance in your pension. That means even if your old provider charges a fee for leaving, it’ll probably still be worth doing – assuming your new provider has cheaper fees, it’ll probably balance itself out before too long!

Occasionally, your new provider might also try to charge you a set-up charge to start a new pension. However, most won’t do this so we’d recommend choosing a personal pension provider that will let you set up a new pension for free. Most will!

As you can see, there are lots of reasons why you should transfer your pension. But are there any reasons why you shouldn’t?

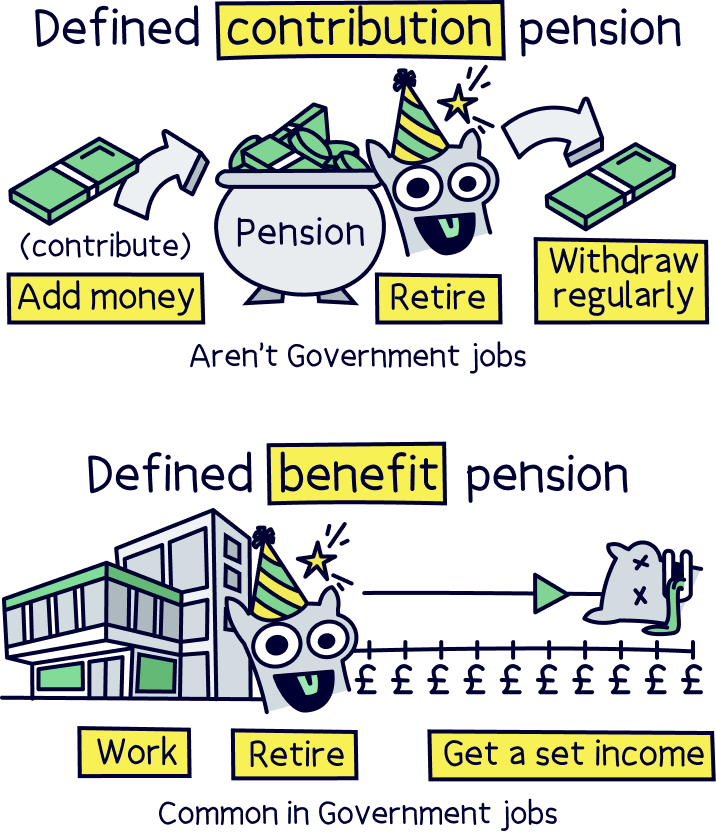

Well, there is one big one – and that’s if you have something called a defined benefit pension (as opposed to a defined contribution pension).

‘Huh?’ We hear you ask, ‘what’s that?’

A defined benefit pension is a workplace pension where your employer pays you an income in retirement based on your salary and the number of years you worked for them. This is different from a defined contribution pension which works a bit like a piggybank – you pay into it every month and the income you get when you retire is based on how much you’ve contributed over your working life (as well as how much your investments grow, of course!).

If you have a defined benefit pension, you’ll probably be better off leaving your pension where it is, instead of transferring it. Why? Well, if you move it elsewhere, you could lose some of the lovely benefits it comes with, like a guaranteed income throughout retirement!

For this reason, if you’re considering transferring one of these pensions, you’ll legally have to get advice from an independent financial advisor first. You can use Unbiased¹, which specialises in matching you with expert advisors, to find the right one for you.

Not sure what kind of pension you have? Then the likelihood is that you have a defined contribution pension (the ones that work a bit like piggybanks). This is because all personal pensions are this kind, and nearly all workplace pensions are too. It’s only a few older ones that aren’t, so fingers crossed, you shouldn’t have to worry about transferring your pension at all!

Got old pensions lying around? Then there’s no excuse – just follow our simple steps above to transfer them over to a personal pension. Then, enjoy cheaper fees, faster growth and more visibility and control over your savings for retirement!

If you don’t yet have a personal pension and you’re not sure where to start, we’ve made things super easy for you. Just check out our guide to personal pensions, where you can compare your options and find the best pension provider for you. You’ll be enjoying cruises around the Caribbean before you know it!

If you’re self-employed, we highly recommend opening a personal pension as soon as you can. Your future self will thank you for it, and you'll have a nice big retirement fund by the time you retire.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.