Article contents

If you move abroad, we have some good news for you. You can take an income from your pension wherever you live. Hooray! Just be aware that not every pension provider will be happy to pay your pension into an overseas bank account.

Keen to trade in the wet and grey of the UK for somewhere a bit sunnier (or simply more exciting)?! Go you! But what does it mean for your pension?

Don’t worry, you can still get paid your pension if you move abroad. Hooray! However, exactly how that works will depend on what kind of pension you have.

Here, we’ll look at what happens to your personal pension, workplace pension and State pension if you move abroad (and don’t worry, we’ll explain what each of those are here too!). Here’s the lowdown.

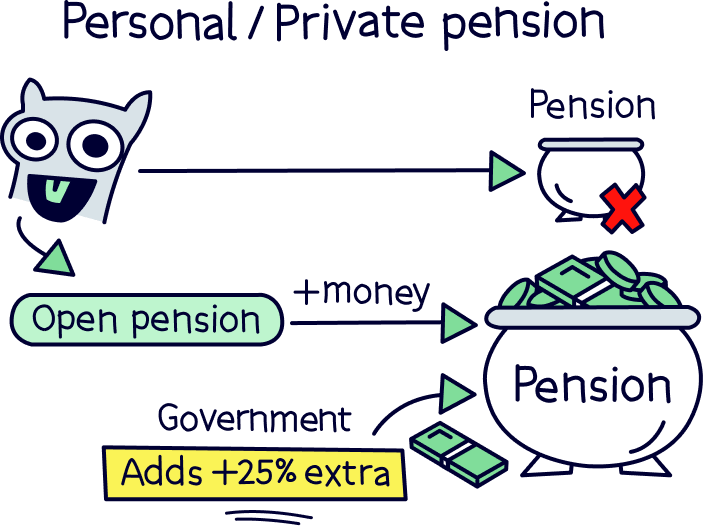

A personal pension is a pension that you set up and pay into yourself, rather than one that’s set up by your employer. Popular personal pension providers include PensionBee¹ and Beach¹.

The good news is that you can still access your personal pension funds if you live abroad and you’ve reached the age where you’re allowed to start taking money out of your pension (at the moment, that age is 55 but it’s rising to 57 in 2028).

The bad news is that not all pension providers will be happy to pay your pension funds into an overseas bank account (your pension provider is the company you got your pension from). And those that do will often ask you to pay extra fees. Doh!

This means you have 3 options:

PensionBee¹ is great, it’s easy to use, has low fees, and great customer service. Also check out Beach¹, where you can save within a pension and an ISA for general savings at the same time.

Find the best personal pension for you – you could be £1,000s better off.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Find the best personal pension for you – you could be £1,000s better off.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

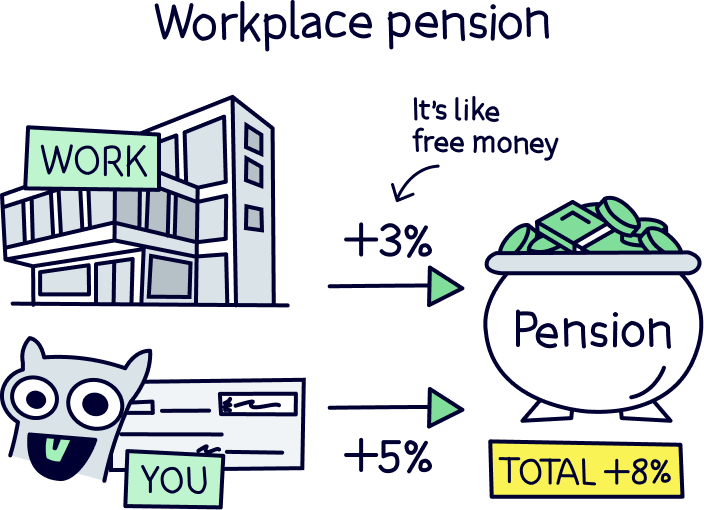

A workplace pension is one that your employer sets up for you. Not only do you contribute a percentage of your earnings each month (at least 5%), but your employer also contributes to it from their own pocket (they have to add at least 3%). Kerching!

Just like with a personal pension, your workplace pension can be paid to you wherever you live, if you’re old enough. Nice!

Similarly to personal pensions, some workplace pension schemes will only be willing to pay into a UK bank account. However, some will be willing to pay into an overseas bank account (normally for an additional charge). Either way, remember that your pension will be paid in pounds sterling. So, if you change it into your local currency, the value will vary depending on the exchange rate at the time.

You may also be able to transfer your pension to a scheme in your new country. Just remember to use one of those Recognised Overseas Pension Schemes (ROPS) we mentioned earlier. If you don’t, you could be treated as having made an unauthorised payment from your pension, which could mean a tax charge of 55% (and maybe even extra penalties on top!). And nobody wants that!

If you transfer your pension to a ROPS that’s within the EEA (European Economic Area) or Gibraltar, you’ll usually be able to avoid paying tax when you make the switch. However, transferring to a ROPS outside of these countries could result in paying tax. Hence why speaking to a financial advisor is so important! If you’re not sure where to find one, just use Unbiased¹ to search for the right financial advisor for you.

That depends! Every country will have different tax laws.

In the UK, you can get paid the first 25% of your pension without having to pay any income tax on it (income tax is a tax you’re charged in the UK on your earnings). Get in! After this, any income you take from your pension will be taxed in the same way as other earnings.

However, it’s important to check the rules of the country you’ve moved to. Some countries will have a similar rule to the UK, but others may not let you take anything out of your pension tax-free at all!

Not only this, but even if you’re classed as a non-UK resident, you might still have to pay UK tax on your pension income. The worst-case scenario is that you end up having to pay tax in both countries on any income you take from your pension.

But don’t panic! Some countries have something called a double-taxation agreement with the UK. This means you can claim tax relief in the UK to avoid being taxed twice (tax relief is when you either get a tax refund or just legally avoid paying tax in the first place). To check whether your country has a double-taxation agreement with the UK, you can check the GOV.UK website.

So, we’ve covered what happens if you’ve moved abroad and you’re ready to take an income from your pension. But what happens to your pension if you move abroad before you start taking money from it?

Well, you have 2 main options:

Having said that, it’s important to understand that just because you can continue paying into your UK pension when you live abroad, that doesn’t mean it’s necessarily going to be the best decision for you. Paying into a pension when you live in the UK comes with certain tax benefits, which we’ll explain in a second. That may not be the case where you’ve moved to, so make sure to do some digging first. Which brings us onto…

In the UK, income that you put into your pension – whether a personal pension or a workplace pension – isn’t taxed. This is because the government wants to reward you for saving to tide yourself over later on in life! It’s known as ‘tax relief’ and can work in a couple of ways depending on whether you’re employed or self-employed.

As well as helping you to save for later on in life, tax relief makes paying into a pension a super sensible financial decision, as it means you keep more of your hard-earned cash to yourself and away from the taxman!

However, you may not be able to get the same benefits if you live abroad, if any at all! To qualify for tax relief on the money you put in your pension, you have to be what’s called a ‘relevant UK individual’ for that tax year (a tax year is like a calendar year, but instead of going from the 1st of January to the 31st of December, it goes from the 6th April to the 5th April).

To be classed as a UK relevant individual, you’ll need to have earnings that the government can charge you income tax on that tax year (remember, income tax is a tax that’s charged on your earnings).

Plus, if you don’t live in the UK currently, you’ll need to have lived in the UK in at least 1 of the last 5 tax years. You’ll also need to have signed up to your UK registered pension scheme during that time. If not, you’ll need to be a Crown Servant (or the spouse or civil partner of one!) – that means someone who works for the government, such as in the army, in the police force or as a civil servant.

As you can tell, that’s quite specific! So, if you’ve moved abroad permanently, the chances are that lovely tax relief might just be a thing of the past.

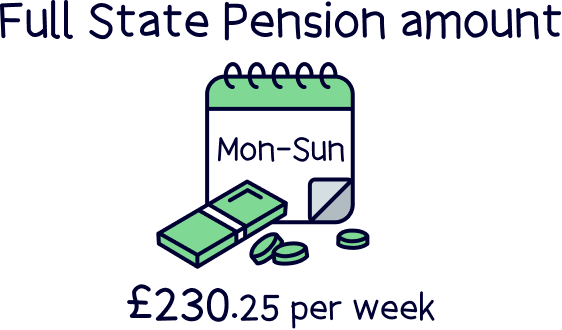

The State Pension is a weekly payment you can receive from the UK government when you reach a certain age, known as State Pension age (currently 66). At the moment, the full State Pension is £230.25 Pension amount per week. Yep, it’s not a lot at all! However, if you have a workplace pension or personal pension, you can still get the State Pension on top, so it’s a really nice extra!

Anyway, if you’re moving abroad, it’s good news for your UK State Pension. You’ll still be able to claim it as long as you’ve made enough National Insurance contributions over the course of your working life (National Insurance is a payment you make to the government alongside your taxes, to pay for things like healthcare).

In order to get at least some of your State Pension, you have to make National Insurance contributions for 10 years. But in order to get the full State Pension, you have to make contributions for 35 years.

You’ll automatically be recorded as making National Insurance contributions if you pay tax in the UK and you earn more than £120 per week (or if you make more than £6,515 a year in profit if you’re self-employed). But if you earn less than £120 per week, you’ll need to make voluntary contributions if you want to qualify for the State Pension (making voluntary contributions means paying National Insurance even though you don’t have to – it sounds rubbish but you’ll thank yourself once you’re old and grey, we promise!).

There’s just one thing that you can’t get if you move abroad permanently, and that’s Pension Credit. Pension Credit is a government scheme for people on a very low income. It tops your household income up to £177.10 if you’re single, or £270.30 if you live with a partner.

Even though you can still get your UK State Pension if you move abroad, you may not get quite the same amount that you would if you were in the UK. Let us explain.

If you’re receiving the State Pension in the UK, you can normally expect your weekly payment to get a little bit higher each year. This is to take into account things like inflation, which refers to the fact that products and services get more expensive in an economy over time.

However, depending on what country you move to, you may not be able to benefit from those yearly increases. Your weekly payment will only increase each year if you live in one of these countries:

If you live anywhere else and you claim the State Pension, you’ll just receive one flat rate for the rest of your life – except if you move back to the UK, in which case your pension will go up to the current rate.

When you move abroad, you have to tell the International Pension Centre (if you live in England, Scotland or Wales) or the Northern Ireland Pension Centre (if you live in Northern Ireland). It’s not hard, you can just fill out an online form or give them a call.

When you hit the State Pension age, you can then contact them again to make a claim (that’s when you ask them to start sending you that lovely weekly payment!).

The great thing about the State Pension if you live abroad is that you can choose whether to have it paid into a UK bank account or a bank account in the country you live in.

If you ask to have it paid into an overseas account, you’ll get paid in the local currency so you don’t have to worry about converting it. Just be aware that the amount you get will still change depending on the exchange rate (the current value of the local currency in comparison to pounds sterling).

You don’t have to take your State Pension as soon as you reach State Pension age. Instead, you can choose to defer it, which is where you delay taking it. We know what you’re thinking: why on earth would you want to delay taking that nice, juicy weekly payment you’re entitled to?

Well, it’s one way of increasing your State Pension. As long as you defer taking your State Pension for at least 9 weeks, your Pension will increase every week you defer it. Exactly how much it increases by will depend on when you reach State Pension age and how long you defer it for.

The extra State Pension you’re entitled to for deferring it can normally be paid as a lump sum, or added onto your weekly payments once you start taking it. Kerching! But what happens to this extra State Pension payment if you defer your State Pension and then sadly die?

Unfortunately, it all depends on when you reach State Pension age. If you turned State Pension age before the 6th April 2016, your spouse or legal partner (if you have one) can inherit your extra State Pension. So, your hard work won’t go to waste!

They can receive the extra State Pension they’ve inherited once they reach State Pension age themselves, as long as they don’t remarry or form a new Civil Partnership before then. This is the case whether they’ve moved abroad or not.

However, if you reached (or are due to reach) State Pension age on or after the 6th April 2016, any extra State Pension you’ve built up by deferring it won’t be able to be inherited. Urgh! That means all that lovely extra cash you’ve built up will go down the drain.

Apparently, it’s to do with the fact that the new State Pension is higher. But let’s be honest, it may make you think again if you’re umming and ahhing about whether to defer your State Pension!

If you fancy moving abroad to start a new adventure in your sunset years, we have some great news for you: you’ll still be able to rely on your pension to fund your new lifestyle, as you can get paid an income from your pension no matter where you choose to live. Yes!

Just remember that every country has its own rules and regulations around pensions. The worst-case scenario is that you end up having to pay tax in both the UK and your new country!

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.