Article contents

The best way to combine your pensions is to choose a great new pension provider. Once you've signed up, simply provide a few details about your existing pensions and they can usually take care of the transfer process for you. If you need help finding one, our top recommendations are PensionBee and Beach, both are easy to use, low cost and have great customer service.

Have you got a pension, or a few pension pots lying around collecting dust? Not sure if they’re growing, what the fees are, or even which pension company they’re with? You're not alone. We'll explain everything you need to know about combining pensions.

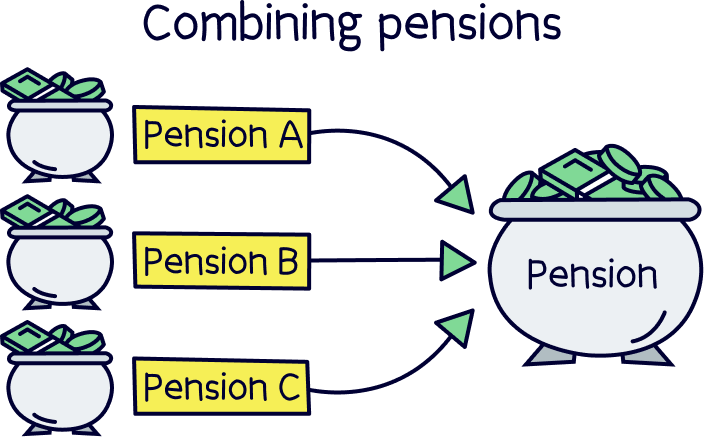

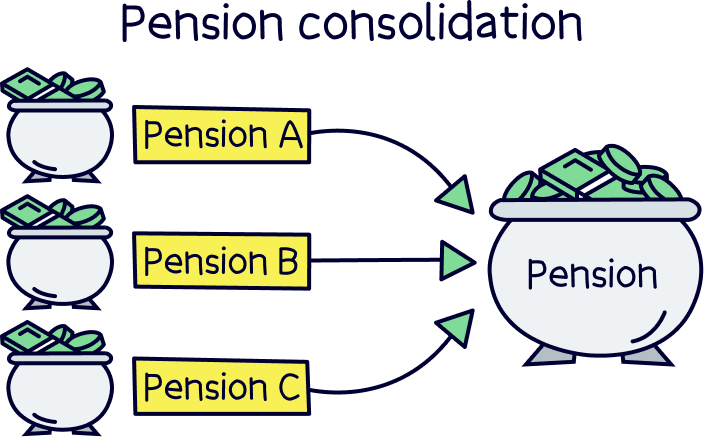

Combining pensions is where you bring multiple pensions together into a single pension pot, making it easier to manage, you won’t be able to forget about a pension pot (which happens a lot), and are able to make sure that it’s with a great pension provider (company) that suits you – such as one that’s easy to use, has low fees and great customer service.

With that in mind, if you’re looking for a new provider, one that can handle everything for you – meaning combine all your pension pots into one, handle all the paperwork that goes with it, and all for free, then here’s the best pension providers for you…

After that, we’ll run through everything you need to know about combining your pensions.

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

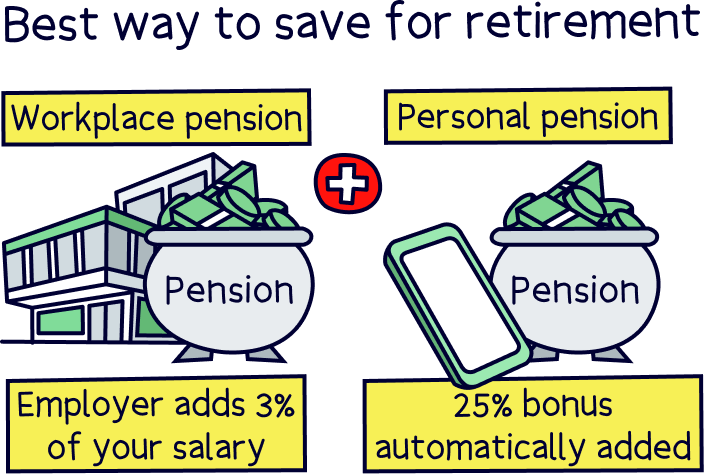

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

Combining pensions can be super easy these days, and is very popular – often the recommended option for most people (we’ll cover all the benefits below).

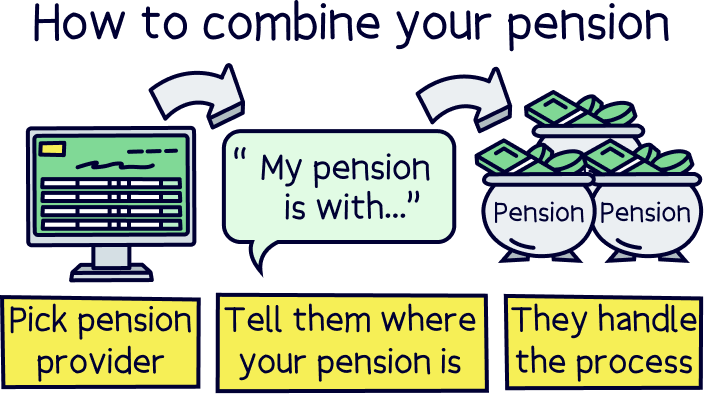

Here’s the easy way to combine pensions in just 3 easy steps:

1. Pick a great new pension provider

2. Tell them where your pension is

3. They’ll handle the whole process, and your money arrives!

That really is it. Once you’ve decided on a great new pension provider, request a pension transfer, and they’ll handle everything for you – that’s getting in contact with your old pension provider, and handling all the paperwork involved with moving your pension across.

After a short while, normally a few weeks, but can be a few months, your money will appear in your new pension account, all ready to keep growing over time!

Plus, there’s normally no extra fees to do this.

As a reminder, check out PensionBee¹, it’s easy to use, low cost and a great track record of growing pensions over time (and you’ll get £50 added to your pension for free if you sign up with Nuts About Money).

There’s also Beach¹, which is great too, and offers a pension and ISA (for everyday savings) at the same time.

For the full range of all the top pension companies, check out the best personal pensions.

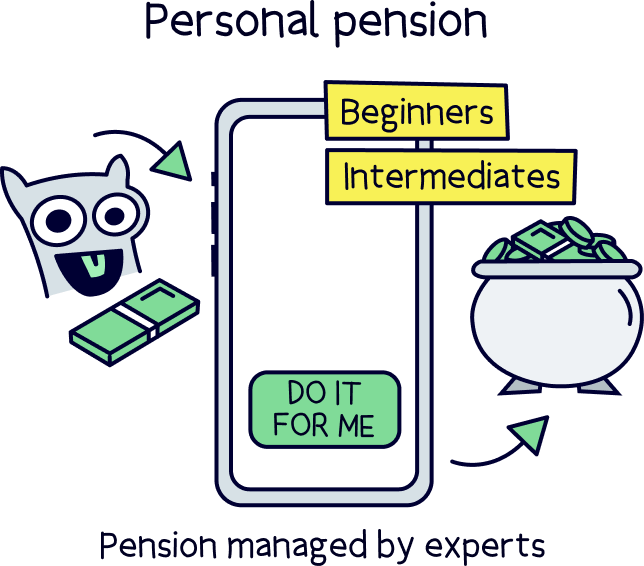

These recommendations are where experts handle growing your money over time (so they sensibly make the investment decisions), it's called an expert-managed personal pension.

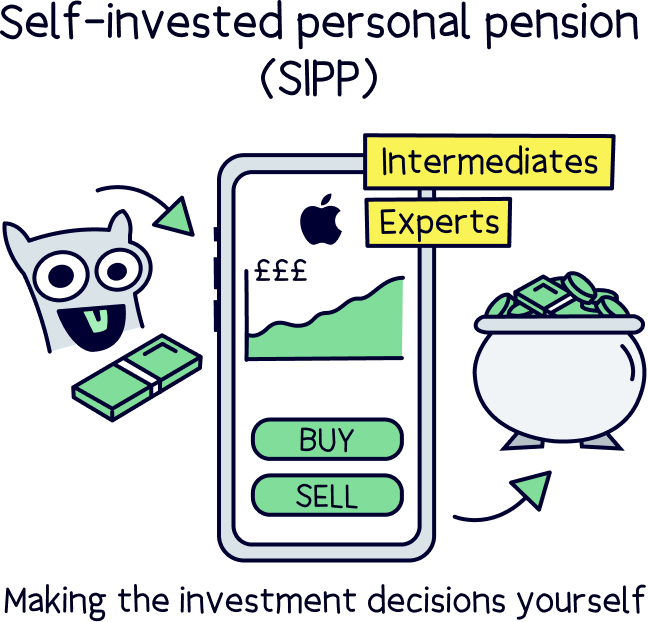

However, you can also make your own investments within a self-invested personal pension, or SIPP. This is only recommended if you know what you’re doing when it comes to investing, but if that sounds like something you’re interested in, check out the best SIPP providers.

Nuts About Money tip: if you’re not sure where your old pensions are, Beach¹ can help you find and combine pensions. It's easy to use!

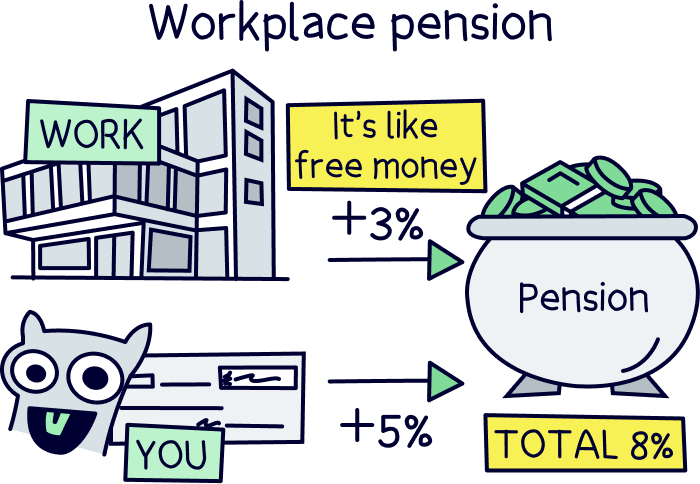

You’ll likely have a pension with your current job, if you’re employed that is. This is called a workplace pension, and is all arranged by your employer, with money taken out of your salary and paid into your pension pot each month.

They’re pretty great because your employer has to pay in 3% of your salary per year, if you pay in 5%, so it’s like a free pay rise!

However, you don’t get to pick which pension provider to use, and often your employer won’t be picking a great one (as there’s not many out there).

You can transfer your old pension pots over to your current workplace pension if you want to, however once you’ve done that, there’s no going back, and you won’t be able to move it again to a new provider until you change jobs.

So, it’s often not a good idea to do this, as you could be stuck with a not so great pension provider, that could have high fees, and doesn't increase your pension in value over time (it's not your choice).

By transferring your pensions to a personal pension, you have full control over which pension provider to use, so you can pick a great one, such as PensionBee¹ or Beach¹, and you’ll be able to transfer your pension again to another provider later if you decide to.

Note: if you’re self-employed, your only option is a personal pension, but it’s a great choice. Learn more with our guide to self-employed pensions.

Now, this is a good question, why should you actually combine your pensions? (Also called pension consolidation.)

Well, there’s a few reasons.

The first, is that you’ll know where all your retirement savings are – they’ll all be in one big (hopefully) pension pot, all ready and waiting for you to retire.

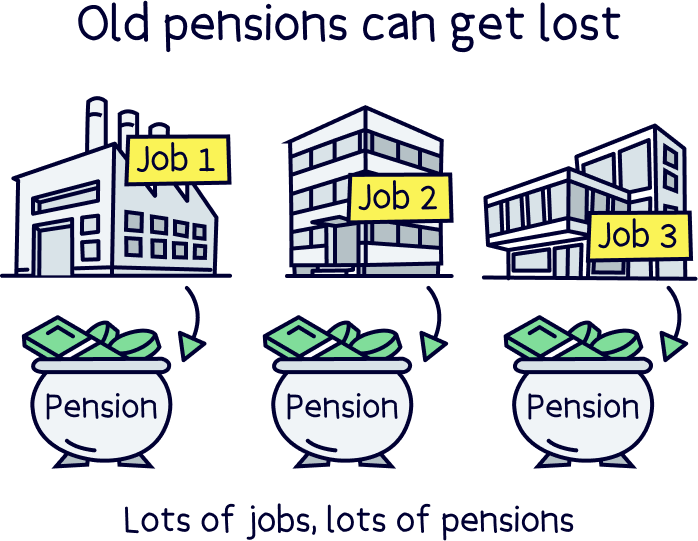

According to The Association of British Insurers, there’s over 3.3 million lost pension pots in the UK. That’s a lot. And, that totals over £31.1 billion. Yikes.

You don’t want your hard earned money to become part of that stat – and your pension provider might not get in touch with you when it comes to retirement (they like to keep hold of them to keep charging their fee).

So, it’s a good idea to move old pensions over into a single pension pot where possible, so you can always remember where it is. Remember, depending on your age, this could be 40 or 50 years from now.

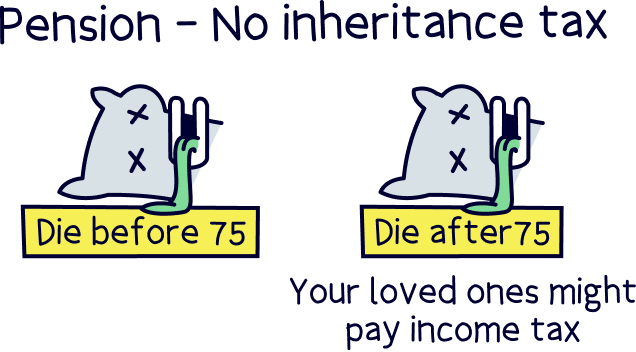

And, if you sadly pass away, your family (or whoever you want to get the pension) will only have to deal with one pension company to access your money.

Note: your pension pot can be passed on completely tax-free if you pass away before 75 years old. It also won't count towards Inheritance Tax.

Do you know how much is in your pension right now? And, how much it’s grown over time? Didn’t think so, not many people do.

If all your pension pots are together, you’ll easily be able to check out how much your total pension pot is worth, and how much it has grown over time. Meaning it will be easier to work out how much you need to save in future to give you the retirement income you’d like.

Nuts About Money tip: to learn more about how much you might need for retirement, check out our guide to how much you’ll need in your pension pot.

You’ll also know if it’s performing well, and know where it’s invested. And, if you don’t like where it is (like oil companies), you can transfer it to a more ethical pension provider like Beach¹, whenever you want to.

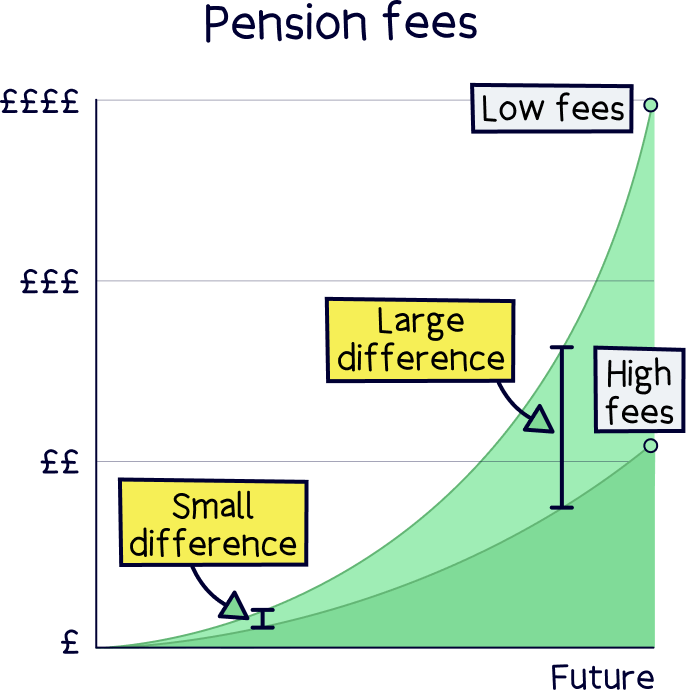

Did you know that you’re still paying fees on all your old pensions? Yep! They’re taken straight out of your pension pot every month – and sometimes these can be quite a lot, it all depends on the pension provider (company).

Some providers have pretty high fees, and others can be pretty low cost. So, combining your pensions can be a great way to make sure all of your pension pots are with a great low cost provider.

But there’s more, some pension providers can also give you a discount if you have more saved with them – sometimes as much as 50% off their fee. Which means consolidating your pensions can mean even bigger savings!

Finally, with a great pension provider, your pension pot might also grow much bigger over time!

When you save into a pension, it’s typically pooled together with other people’s money, into something called a pension fund, also called a pension plan, which is managed by experts who aim to grow it significantly over time.

All pension funds are different, and with some providers, you’ll get to choose which pension plan you want to invest in.

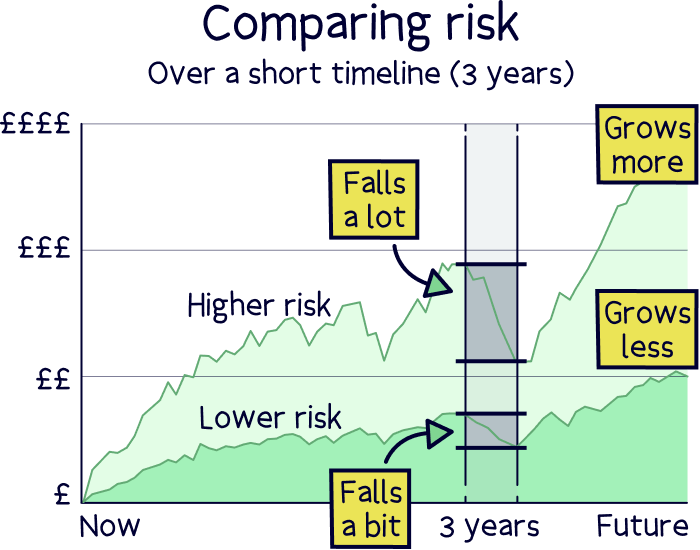

Some pension plans are designed to grow a bit slower, and some are designed to grow faster (but with bigger ups and downs along the way). So, reviewing where your pension pots are and which pension fund your money is in, might give you a few surprises – your money might not be growing at all, or it could be in completely the wrong pension plan for you (which can be based on things like your age).

So, combining all your pensions together means you have full control over where your money is invested, allowing you to pick a provider with a great track record of growing pensions over time, and a pension plan that suits your personal circumstances (e.g. your age).

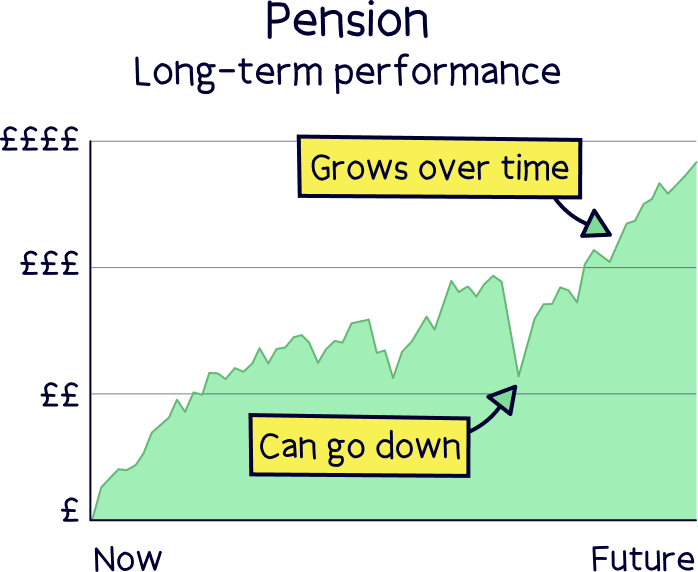

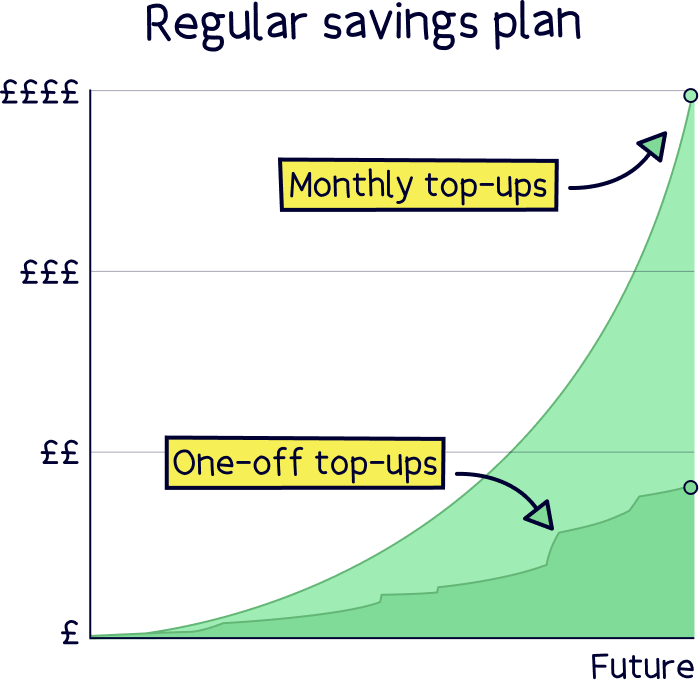

Nuts About Money tip: don’t panic about your money being invested – it’s the best way of growing your money over time, and almost every pension is invested (whether you know it or not). Your pension will go up and down in value, but the experts know what they’re doing, and over time your money should grow very large (also, try and contribute as much as you can afford each month too, it will soon add up and your future self will thank you).

Once you combine your pensions, you can still pay into your new pension – and it’s often a great idea to do this (ideally monthly), so you can keep building up a nice big pension pot, all ready for retirement.

These days, you’ll need a fairly hefty pension pot in order to retire with a comfortable income…

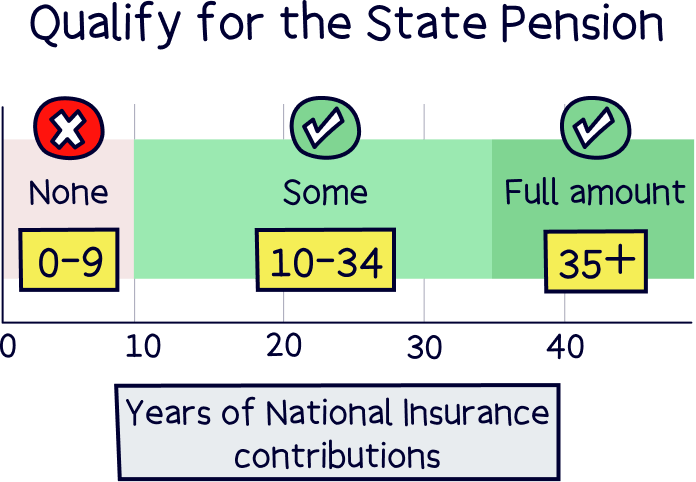

Here’s how much you’ll likely need in your private pensions (e.g. your pension from work and your own pension you set up), and this includes receiving the State Pension:

Note: the State Pension is the pension you’ll get from the Government when you reach State Retirement age (currently 66), and only if you’ve paid at least 10 years worth of National Insurance contributions (but 35 years for the full amount). It’s also not a lot, just £11,973 per year currently, so you’ll likely need a big private pension too.

Nuts About Money tip: learn more with our guide to how much you’ll need in your pension pot.

If you’ve got a pension from your current work, great, often with most workplace pension schemes, if you pay in 5% of your salary per year, your company has to pay in 3% too.

So, a great way to build your pension is to pay 5% into your workplace pension, and then pay into your personal pension if you can after that – that way you get to pick which pension provider you want to use – for instance, the pension you’ll soon set up to combine all of your other pensions.

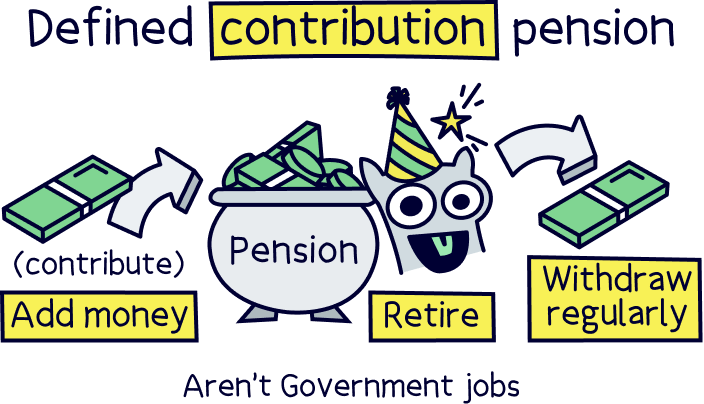

When we’re talking about combining and consolidating your pension(s), we’re talking about ‘defined contribution’ pensions – they’re pensions that you pay into yourself (either from your work, or directly yourself), and it grows into a (hopefully) big pension pot with a financial value (e.g. a £200,000 pension pot).

You can then decide when to take your money out, as long as you’re over 55, and you can decide to transfer them to another provider pretty much whenever you like (as long as it’s not your current workplace pension).

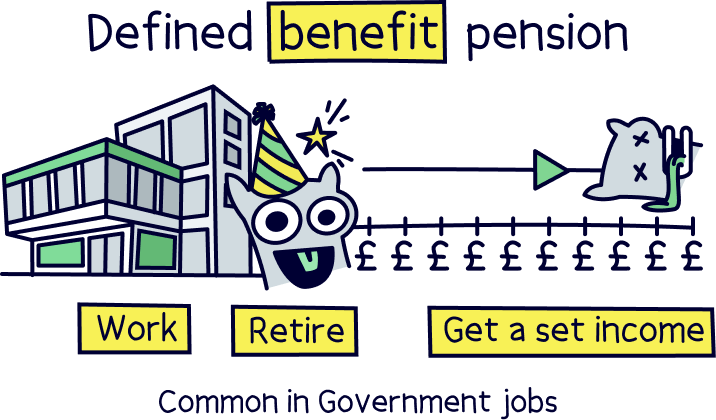

With a ‘defined benefit’ pension scheme, which are more common in government jobs, and the NHS, instead of building up a pension pot, you’ll typically get a retirement income after you retire.

This can be based on things like how long you’ve worked there, and what your salary was. These can also be called a final salary pension (not common these days), or an average salary pension.

They’ve got pretty good benefits (such as a guaranteed income), so it's often not a good idea to combine or transfer these to a defined contribution pension. If you are thinking of doing this, it’s a good idea to speak to a financial advisor first – you can find great ones local to you with Unbiased¹.

Often when combining your pension pots, there won’t be any fees, however if your pension is pretty old, and not with a nice pension provider, there might be some fees for them to transfer it to your new provider, called exit fees.

Your pension provider will let you know if there are any fees as part of the transfer process, and you can decide to either not transfer the pension, or continue with the transfer. It can be a good idea to simply pay the fee so your money is with a great new provider, where it can potentially grow more and with lower fees (and all in one place), but the choice is yours.

Note: the fees aren’t typically too much, and by law they have to be capped at a maximum of 1% if you’re over 55 years old.

Modern pension providers won’t have any fees, so any pension you’ve had in the last 10 years or so (or even longer) likely won’t have any exit fees.

Yep! It’s perfectly safe to consolidate your pension savings.

Your new provider will handle everything for you, and your old provider will send your pension pot directly to them, and it will arrive in your new pension.

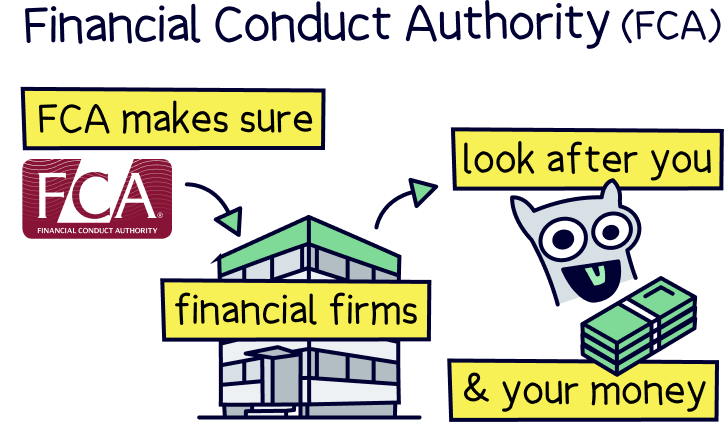

Pensions, and all financial services, are regulated by the Financial Conduct Authority (FCA), that means every pension provider has to be reviewed and approved in order to look after your money.

You can check if a pension provider is authorised by the FCA by checking the FCA register.

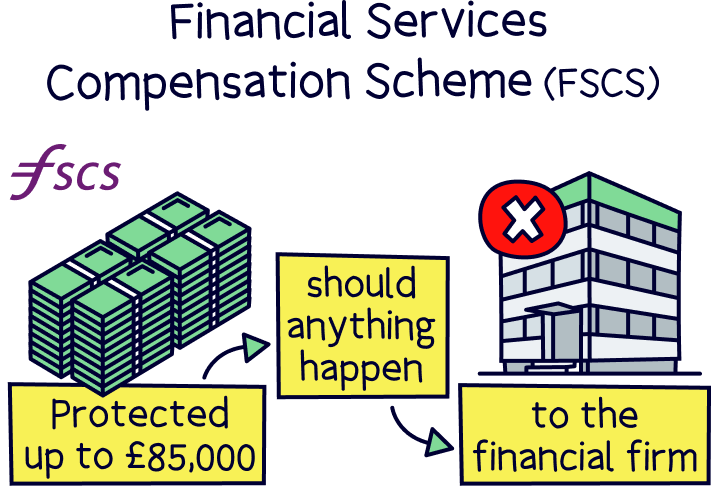

That also means you’re protected by the Financial Services Compensation Scheme (FSCS), which can give you compensation up to £85,000 should anything happen to your pension provider (such as going out of business).

However, your money is actually within the pension fund itself, which is held by very large banks, all in your name, and can only be returned to you. Overall pensions are super safe.

And there we have it. The best way to combine pensions. Pretty simple really isn’t it?

All you need to do is find a great new pension provider, and let them know you want to transfer your old pension(s) across to them. They’ll then get to work and handle everything for you. It’s that simple.

There’s typically no fees to combine your pensions, and after a few weeks (or sometimes months), the money will turn up in your new pension pot, so you’ll never forget where your pensions are, and can keep growing over time, all ready for a nice retirement (fingers crossed).

As a recap, our top recommendation for a great pension provider is PensionBee¹, it’s easy to use, low cost and has a great track record of growing pensions over time – and you’ll get a dedicated account manager to help whenever you need it.

And you’ll love Beach¹ if you’re keen to save within a pension pot and an easy access pot for general savings at the same time.

For the full range of options, check out the best pension providers.

Now all that’s left to do is enjoy retirement!

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).