Article contents

When you consolidate your pensions, you gather your pensions together in one place. It can be a great way of saving money and making it easier to keep track of your savings. Plus, this way, they’re less likely to get lost!

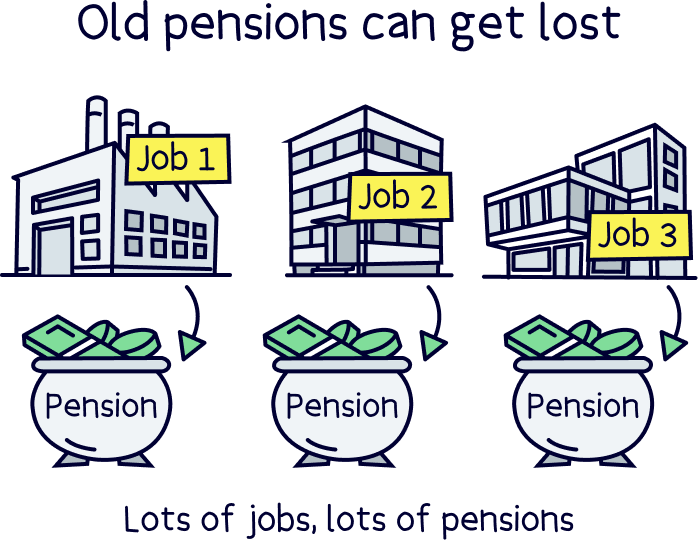

If you’re like most people, you’ll probably have a number of different jobs before you retire. In fact, UK residents are changing jobs on average 5 times in their working lives (according to AAT)! So, the chances are you’ll end up with quite a few pensions knocking around.

Consolidating all your old pensions so they’re in one place can make it easier to track your pension savings. And it can even save you money! But should you do it? We’ll reveal all here (hint: you probably should!).

Pension consolidation is when you gather multiple pension pots together in one place. In other words, you just transfer the money from your old pensions into one new pension, to make your savings easier to keep track of. It’s that simple!

Normally, you’ll do this when you change jobs. Let’s rewind for a second.

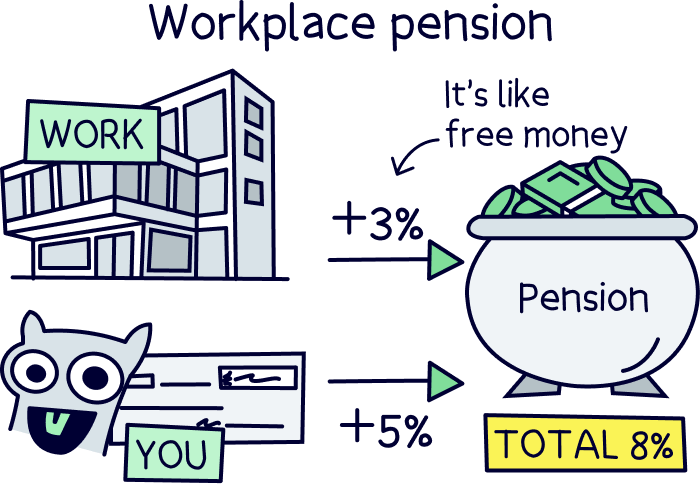

If you’re an employee, your employer will normally be legally obliged to set a pension up for you, known as a workplace pension. You’ll have to contribute to it every month (at least 5% of your pay cheque). But the really great news is that your employer will have to contribute to it too (at least 3% of your pay cheque, from their own pocket). Kerching!

If you change jobs, your new employer will likely set you up a new pension and you’ll stop paying into your old one. The money in your old pension will still be yours. But you can’t cash in a pension from an old employer until you’re at least 55, which means it can be easy to forget all about it – especially if you’ve changed jobs a lot and you have lots of old pensions lying around!

By transferring your pensions from old employers and old pensions, to one new pension, it’ll be much easier to keep track of where your pension savings are and how much you’ve squirrelled away for retirement. Plus, it comes with some other great bonuses. Which brings us onto…

Find the best personal pension for you – you could be £1,000s better off.

Consolidating your pensions can come with a whole host of positives, such as saving you money, growing your pension savings quicker, making them easier to manage… the list goes on! Here’s the lowdown.

We’ve mentioned this one already, but it’s worth mentioning it again because, believe it or not, lots of pensions get lost!

We know that might sound crazy. But The Association of British Insurers found that there are around 3.3 million lost pension pots in the UK. And altogether, these are worth around £31.1 billion. Gulp!

Gathering your old pensions in one place will mean you only have to remember where one pension is, rather than lots. Plus, if you change your address or contact details, you’ll only have one pension provider to notify.

In other words, consolidating your pensions gives you the best possible chance of not losing your old pensions so you can actually enjoy all that hard-earned cash when you’re retired. Nice!

You probably shop around when it comes to mobile phone contracts and energy providers – after all, no one likes paying more than they have to! But the same applies when it comes to pensions – shopping around can save you money.

Let us explain.

When you have a workplace pension (remember, that’s one set up by your employer), your employer will choose your pension provider. Now, as nice as it is to have a pension set up for you, your employer isn’t likely to go hunting for the one with the cheapest fees.

On the other hand, if you start a pension yourself, known as a personal pension, you get to choose the best pension provider for you. That means you can choose one that’s not going to charge you through the roof – like PensionBee, which charges just one low yearly fee. By replacing all your old (probably expensive) workplace pensions with one cheap personal pension, you could save a decent amount of cash!

On top of all that, lots of pension providers will save their best rates for people who have lots of cash in their pension pot. So, by pooling all your savings in one place, you’re more likely to get a better rate on your pension too. Get in!

If you’re self-employed, you won’t have a workplace pension scheme, so we highly recommend opening a personal pension to keep saving as you work.

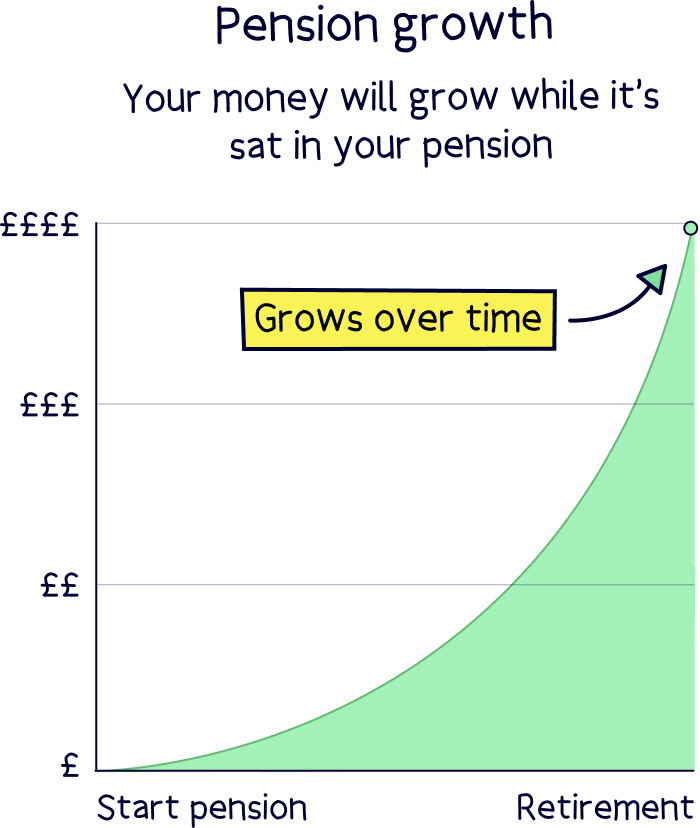

One of the great things about pensions is that your money will usually grow while it’s sat in your pension pot, without you having to do a thing. That’s because your pension provider will spend time investing it – which is when they use your savings to buy things like stocks and shares (small ownership stakes in companies).

The idea is that as your investments increase in value, so do your savings!

Of course, in the short term, these investments can go down in value as well as up. But pensions are all about saving for the long-term, and pension providers are experts at making sure your money will increase in value over a longer period of time.

Now for the really good news. You know how we said that being able to pick your own pension provider means you can choose one with cheaper fees? Well, it also means you can choose one that has a proven track record for growing your money quickly.

In other words, by replacing your old workplace pensions with one personal pension where you get to choose your pension provider, you’ll be more likely to be able to grow your savings quickly. And that should mean you end up with more cash in your pocket by the time you retire. Hooray!

Want to be able to keep an eye on your savings? We don’t blame you! Being able to check how much money you have stashed away in your pensions is important, as that way you know how much cash you have to tide you over in your golden years.

But if you have lots of old pensions, that can be easier said than done.

Let’s say you’ve been in 10 jobs up till now. That means you probably have 10 old pensions! Checking each one regularly to see how it’s doing and how much money is in there is going to be… well… time-consuming!

On the other hand, if you move all your old pensions over to one place, you’ll only have one pension to check in on, which will make it way easier to stay on top of. Not only that, but lots of more modern pension providers like PensionBee¹ and Beach¹ have handy mobile apps that you can use to track your savings on the go. Now doesn’t that sound easy!

At some point, you’re going to want to access all that lovely cash you have stashed away in your pension pots. And guess what? Consolidating your pensions could make it much easier to actually get hold of your money when that time comes!

Once you reach the grand (not-to-old!) age of 55 (57 from 2028), you’ll normally be able to start taking a retirement income from your pensions. If they’re all in one place, that’ll make things that little bit easier. You’ll only need to get in touch with one pension provider to sort out how you’re going to access your money, rather than several.

But even more importantly, consolidating your old pensions could give you more options in terms of how you want to get hold of your money.

Nowadays, there are lots of different ways you can take an income from your pension pot, including something called income drawdown. This allows you take a regular monthly payment straight from your pension – a bit like a salary but better as you can increase or decrease it whenever you want to suit your changing circumstances.

However, before 2015, this wasn’t an option – instead, retirees had to buy an annuity, which basically involves paying a one-off fee for a guaranteed income (either for the remainder of your life, or for a set period of time).

Now, there’s nothing wrong with buying an annuity to tide you over later on in life – in fact, it’s still possible to do this and lots of people want to as it means you’ll get a guaranteed retirement income regardless of what happens. BUT if you have an older pension this might be your only option – if you want to opt for income drawdown instead, you may have to transfer your pension funds to another pension provider.

Enter pension consolidation! By moving all your old, possibly dated, pensions to a new more modern pension pot, you can access much more flexible withdrawal options – making things easy peasy when you retire.

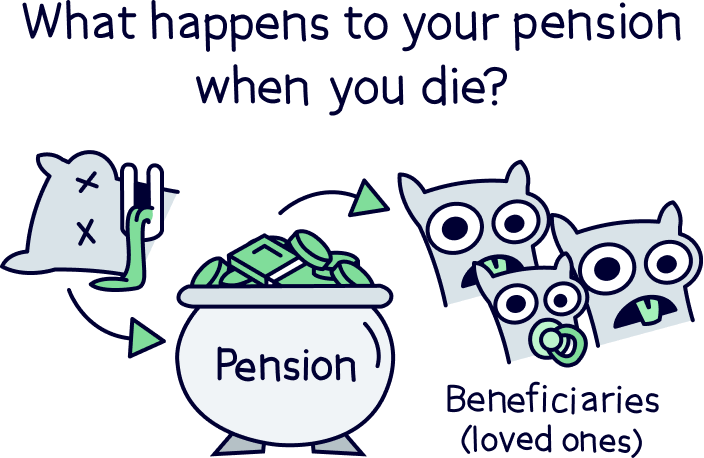

Ever wondered what happens to your pension when you die? (We know, we know, we’ve taken a bit of a turn to the morbid here – sorry about that!)

Well, there’s a silver lining. Workplace pensions and personal pensions (private pensions) can be passed onto your spouse or partner. So, even though you can’t take your money with you after you’ve popped your clogs, you can make sure that your loved ones get to benefit from all your hard work squirrelling those savings away.

Consolidating your pensions will make it much easier for your next of kin to get hold of your savings if the worst happens. Think about it – if you pass away, your loved ones will be going through a difficult enough time as it is. The last thing they’ll want to do is to go on a long treasure hunt to try and track down all your old pensions wherever they may be!

By making sure all the money you’ve stashed away into your pensions is in one place, it’ll be quick and easy for your loved ones to find them so that they can continue with their current way of life (at least financially) now you’re no longer around. Plus, they won’t have to worry about contacting lots of different pension providers to try and get hold of your savings – they’ll just have to deal with one pension provider (the one you chose!) which should take away a lot of the hassle during a really hard time. Sounds worth it, don’t you think?

As you can see, there are lots of reasons why you should consolidate your pensions. But what about the drawbacks? Are there any situations where you might want to think twice about pension consolidation?

Well, there aren’t many! But one little drawback to pension consolidation is that you may have to pay exit fees to leave your old pension provider.

Most of the time, these aren’t worth worrying about. After all, the money you save by consolidating your pensions will normally make up for any exit fees you end up having to pay. In fact, sometimes your new pension provider will even pay the fees for you!

However, if any of your old pension providers charge you huge fees you might want to pause for a second to check if it's worth it – especially if you’re very close to retiring anyway, as you’ll then have less time to make your money back through lower fees with your new pension provider!

Likewise, while most pensions work pretty much the same, on rare occasions employers might give you something a bit more fancy – like one where you can withdraw your pension before 55, or one that comes with critical illness cover built in (that’s an insurance product that pays out if you’re unable to work due to becoming ill). If that’s the case, transferring your pension from one pension provider to another could mean you lose out on those special benefits.

This also applies if you have an older style of pension known as a defined benefit pension. These are pensions where your employer (or ex-employer!) offers you a guaranteed income throughout retirement (for instance a final salary pension, or an NHS pension).

But transferring your pension elsewhere could mean you lose that benefit which you obviously want to avoid! If you have a defined benefit pension scheme, it’s best to get independent financial advice for your personal circumstances. If you’re not sure how to find a financial advisor, use Unbiased¹.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Not sure what kind of pension you have? Then you can be 99.9999% sure that you just have a ‘normal’ one like most people (okay, okay, we made that figure up – but you get the idea!). In which case, you’re all good to go ahead and consolidate, consolidate, consolidate!

Decided that pension consolidation is a goer? Give yourself a pat on the back! But you’re probably also wondering how to go about it.

Luckily, pension consolidation is oh-so-easy. Just follow these simple steps.

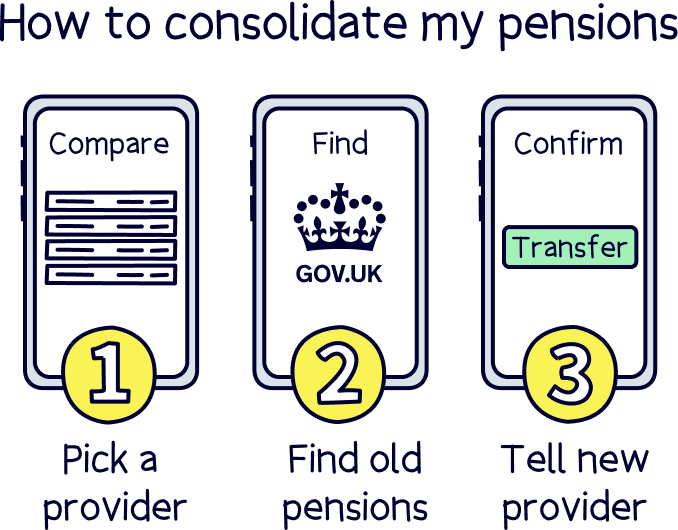

First things first, you just need to choose a new pension provider – you know, the guys who’ll look after all the funds you transfer over from your old pensions.

Although you can transfer your old workplace pensions over to your current workplace pension (if you have one), starting a pension yourself is a much better idea as it’ll mean you can choose your own pension provider. That’s right, now’s the time where you can pick out a company with those lovely low fees we were telling you about earlier – and one that’s got a proven track record for growing pensions quickly!

Don’t worry, we’ve done the hard work for you and have picked out our selection of the best personal pensions. Just choose one of these and you’ll be flying!

A couple that deserve a special mention are PensionBee¹. PensionBee is the perfect choice if you’re after something really easy – their handy mobile app makes it super quick to set up a pension, and they explain everything really well so you don’t have to know anything about pensions beforehand. Oh, and probably worth adding that they have low fees and great customer service too!

On the other hand, Beach¹ is a great shout if you want to save in other kinds of savings accounts alongside a pension (like a tax-free Stocks & Shares ISA managed by a team of experts), meaning you can track all your investment savings in one place. It's also easy to use with a great app.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Now that you’ve chosen your new pension provider, you just need to track down all those old pensions that you want to consolidate. Yep, this is the bit where you start scratching your head and trying to remember where exactly they all are.

Don’t panic if you can’t remember! The government has a really handy tool where you can locate any lost pensions – just head to GOV.UK to get started.

Your new pension provider may also have a similar tool to help you track your old pensions down. Usually, you just have to type in the name of your previous employer and they’ll tell you where your old pension is. Easy!

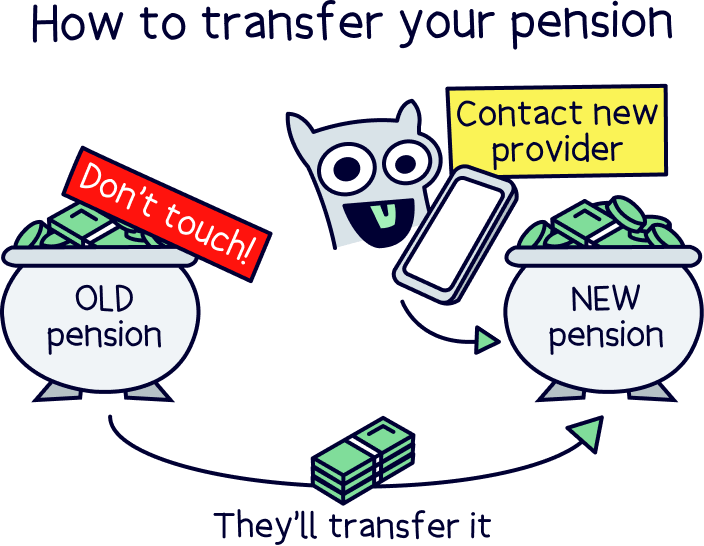

Finally, you just need to tell your new pension provider that you want to go ahead and transfer your old pensions across to your new one. Normally, you can just give them your old pension providers’ names and voila! You just sit back and relax while they do all the hard work for you.

That’s right, they’ll get in touch with your old pension provider to arrange the transfer so you don’t have to do a thing.

Your old pension provider may ask you to confirm that you want to go ahead. But other than that, you can just make your way through Netflix’s whole back catalogue while you wait for the funds to show up in your new pension pot (normally, this will happen within 2 to 4 weeks although it can take longer). Told you it was easy!

Pensions are wonderful things that make it super easy for you to save up for retirement. But too many of them get lost every year!

Consolidating your pensions is a great way to make sure you keep track of every last penny that you’ve saved for your golden years. And it’s also a great way to reduce your fees and grow your pension pot quicker while you’re at it!

Retirement planning is one of the most important things in your life. It’s worth spending some time on so make sure your retirement savings are in the right place and growing nicely. With personal pensions, you can add more to them whenever you like too.

If you’re ready and raring to consolidate your pensions then the first step is to choose a new pension provider. Just check out our selection of the best personal pensions to get started.

If you think you might want professional advice, use Unbiased¹ to find the right financial advisor for you.

After that, you can pretty much just sit back and twiddle your thumbs. Your new pension company will sort everything out so you don’t have to lift a finger. Retirement may seem like a way off now but you’ll be enjoying that cash before you know it (cruise, anyone?!).

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.