Article contents

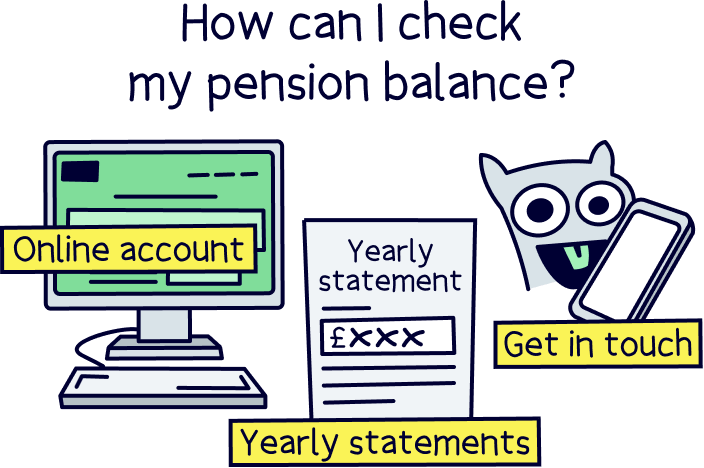

Checking your pension balance is easy! You should receive statements each year letting you know how much money is in your pension. But you can normally also log into your online account to check your balance whenever you want!

Got yourself a pension? Congrats! In fact, if you’ve had a few different jobs over the course of your working life so far, you may even have several pensions floating around.

But how much money do you have saved in them? It’s an important question if you’re planning for retirement – and one that you might be struggling to answer! Don’t worry, luckily checking your pension balance is easy. Here’s the lowdown.

No matter whether you’ve got a workplace pension (one set up for you by your employer) or a personal pension (one you’ve set up yourself), checking your pension balance works exactly the same way. And guess what? It’s super quick and easy! (Wait, what is a personal pension?).

There are a few different ways that you can stay on top of your pension balance, depending on your pension provider (that’s the company looking after your pension for you). Here’s the lowdown.

This is probably THE easiest way to check your pension balance. Basically, your pension provider should send you a yearly statement, letting you know exactly how much money is in your pension pot.

You won’t have to do a thing – the statement should just fly through your letterbox (or into your inbox) every year. As long as your pension provider has the right contact details for you, of course!

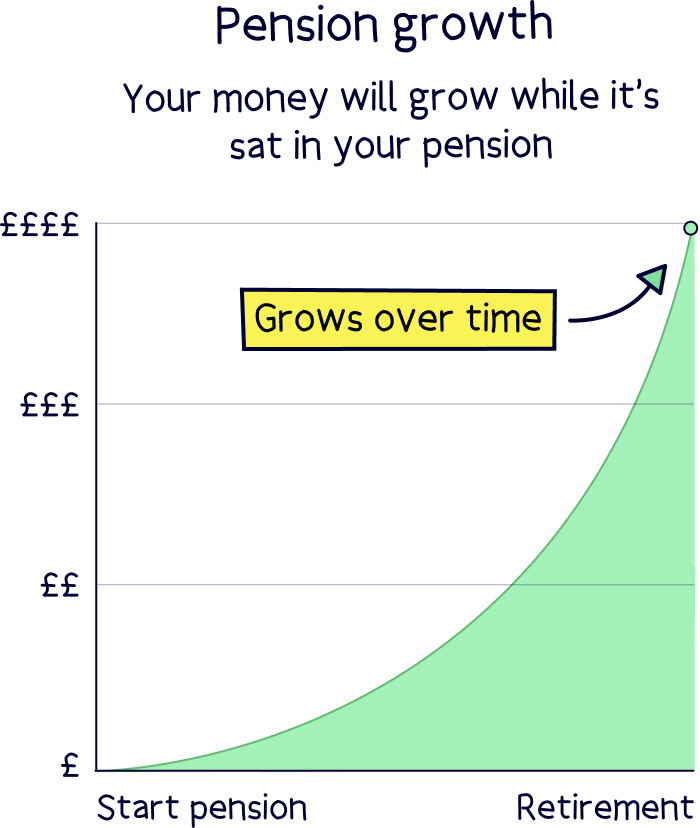

Not only will your pension statement provide your pension balance. It’ll also let you know how your investments are performing.

In case you weren’t sure, your pension provider will use your savings to buy things like stocks and shares (which means you own a tiny portion of a company) and other investments. When these investments increase in value, so does your pension!

That’s how they make sure you have even more to live off when you retire than what you paid into your pension in the first place.

Anyway, the one thing to bear in mind is that this is exactly what it says on the tin – a yearly pension statement. It should show your total pension balance, but also things like the investment returns (how much you’ve made over the years and in the most recent year).

If you want to check your pension balance more frequently, you might need to use other methods too. Which brings us onto…

Most pension providers will also have a way for you to check your pension balance online.

A lot of the time, this will take the form of an online account – you might have to sign up to their online services if you haven’t already, or simply enter your account details (usually your email address and password). You might need your policy number from your paperwork if you need to register. And voila! Once you log in, you’ll be able to see your pension balance.

Even better, lots of more modern pension providers are starting to introduce handy mobile apps, so you can check your balance whenever you want, wherever you want.

A couple of our favourites that offer this are PensionBee and Beach¹. These personal pension providers are fully online and their fab apps make it super quick and easy to check your pension balance – or even add money to your pension on the go! It’s definitely worth checking them out if you fancy starting a personal pension to boost your savings in retirement (always a sensible idea!).

Last (but definitely not least!), don’t forget that behind any pension provider is a team of human beings – just like you! If you want an update on your pension and you’re not sure where to go, you can just get in touch with your pension provider to ask. They’ll normally be able to tell you your balance over the phone, and they’ll almost certainly be able to send you an up-to-date statement.

In fact, they might also be able to point you in the direction of where you can more easily check your pension balance in future – maybe you have an account that you just weren’t aware of, or maybe you’ve moved house or changed your email address so you weren’t getting their updates.

Either way, it won’t be hard to get in touch with your pension provider if you know who they are. On which note…

Find the best personal pension for you – you could be £1,000s better off.

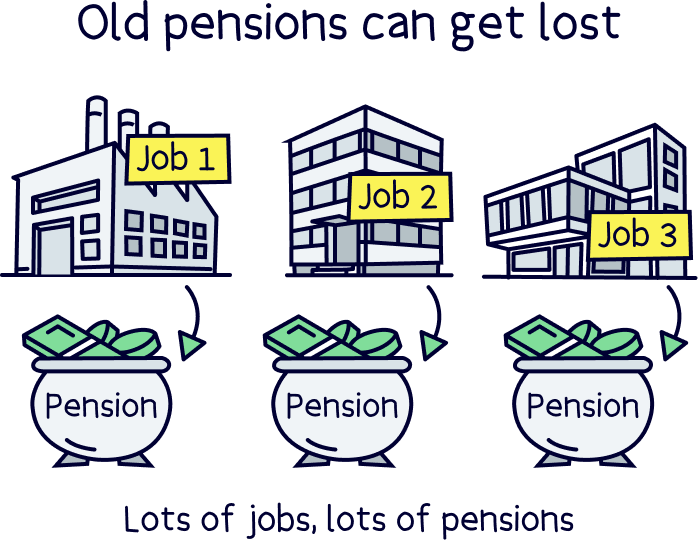

We know what you’re thinking: ‘How could anyone lose a pension?!’

Well, it’s easier than you might think – the Association of British Insurers found that there are around 3.3 million lost pension pots in the UK. And altogether, these are worth around £31.1 billion. Gulp!

The main reason you might lose a pension is if you change jobs – each employer you have will likely set you up a workplace pension. When you get a new job, you’ll stop contributing to your old workplace pension and start contributing to a new one, set up for you by your new employer. According to AAT, the average worker in the UK changes jobs 5 times – so, if you’re like most people, you’ll probably end up with around 6 pensions by the time you retire!

With so many pensions from so many past employments, it’s not surprising that you could forget about one or even a few!

If you think you’ve lost a pension (or you simply want to check whether you have more pensions than you realised!), don’t worry. The government has a handy ‘find a pension’ tool – just head to GOV.UK to track down any old pensions that you may have forgotten about.

Then, once you know about your lost pensions, you can use any of the methods we’ve mentioned above to check your pension balance. Easy!

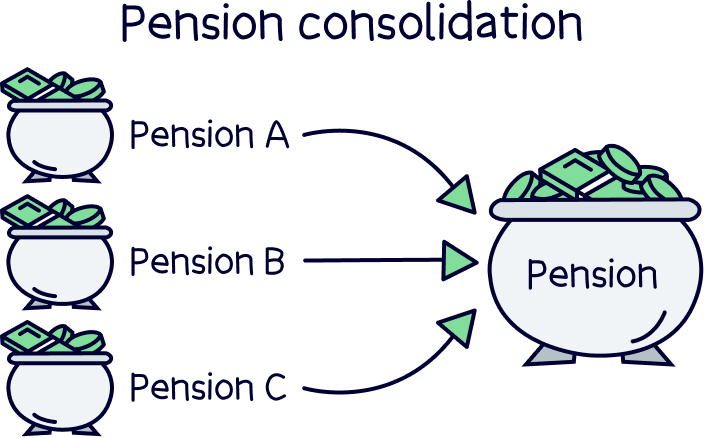

We know, we know, it can be a bit of a pain having to check the balance for so many pensions. And of course, you don’t want to risk any getting lost again! So, you’ll probably be pleased to hear that there is an easier way – you can consolidate your pensions, which is when you transfer all your old pensions over to a new one.

Not only is consolidating your pensions a great way to keep track of them more easily by gathering them all in one place, but depending on which pension provider you choose, it could also reduce your fees and help you to grow your money quicker. Check out our list of the best private pension providers to get started.

You can check how much State Pension you’re on track to receive using the government’s handy State Pension forecast tool, on GOV.UK.

Confused? Let’s rewind for a second.

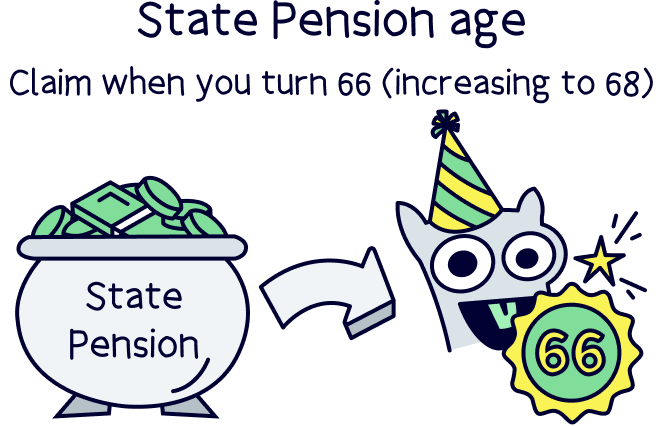

The State Pension is a weekly payment you’ll probably be able to get from the government once you hit State Pension age. That’s currently 66, but it’s gradually climbing to 68.

The State Pension works differently from private pensions (wait, what’s a private pension?). Private pensions (by which we mean most workplace pensions and all personal pensions) work a bit like a piggybank – you contribute to a pot of money that you can then access when you retire.

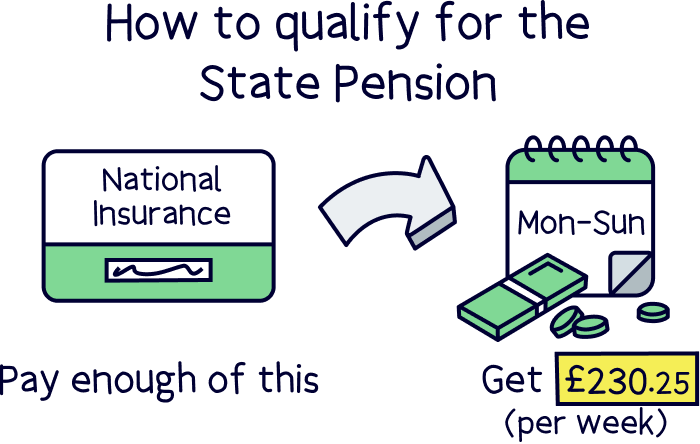

However, with the State Pension, there’s no pot or piggybank. Instead, you qualify for it by making National Insurance contributions (National Insurance is a payment you make to the government alongside your taxes). That’s right, the amount you get when you hit State Pension age will be based on how many years you’ve paid National Insurance for.

You’ll need to make National Insurance contributions for at least 10 years to qualify for the State Pension at all. But to qualify for the full State Pension (£230.25 per week), you’ll need to make National Insurance contributions for at least 35 years.

We know that might sound like a long time. But normally, you’ll qualify for the State Pension automatically because most people have to pay National Insurance.

Having said that, if you get paid very little, you might not have to pay National Insurance – which might sound great until you realise that this can stop you from qualifying for the State Pension!

This is why it’s so important to check your National Insurance record and how much State Pension you’re on track to receive. Not only is it handy to know so you can plan for retirement, but you’ll also get information about what you can do to increase the amount you’re entitled t

If you can afford to, you can normally make voluntary National Insurance contributions for the past 6 years. So, if you nearly qualify for the State Pension but not quite, or you’re close to getting the full State Pension but you’re not quite there yet, you can usually make extra National Insurance contributions to make up for those you’ve missed and maximise your retirement income. Your older self will thank you later!

Forgotten where to go already? Head over to the GOV.UK website to check how much State Pension you could get (you'll need your Government Gateway ID – or need to register for one).

As you can see, checking your pension balance is oh-so-easy. And it’s a great way to make sure you’re saving enough to tide yourself over in your golden years.

Retirement planning is super important, so aim to be aware of how much of a pension you’ll retire on from all of your retirement savings and from the State Pension. Then you’ll know if you need to start increasing your pension savings or if you’re on track to hit your retirement goals.

If you want to boost your retirement income and you haven’t yet got a personal pension, starting one is easy. And it’s a really sensible way to make sure your savings are working as hard for you as they can be. To get started, check out our pick of the best personal pensions.

If you’re self-employed, you probably won’t have a workplace pension. We’d recommend setting up a personal pension as soon as you can – it’s never too early to start planning for retirement.

If you’re after a super simple pension option with low fees, a great track record for growing your money and all online with a handy mobile app, check out PensionBee¹.

Beach¹ is also great, it's an easy to use pension with a great app. Add money or combine old pensions (and find lost pensions). Plus, the customer service is excellent.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.