Article contents

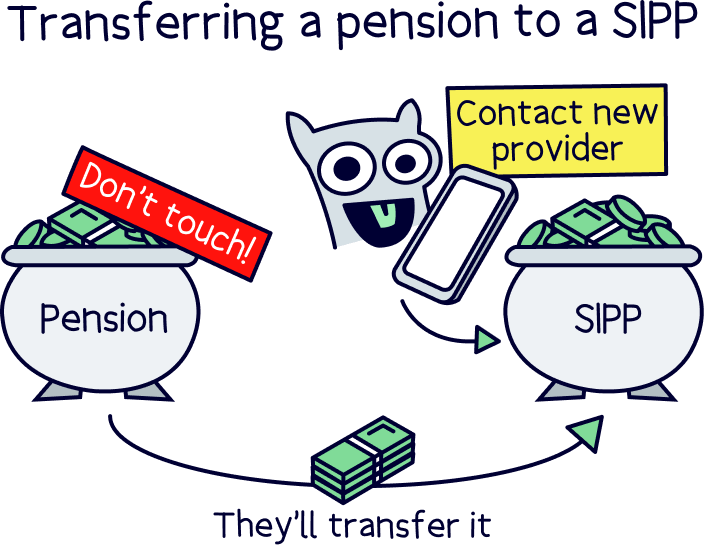

Transferring a pension to a SIPP is oh-so-easy! You just need to choose a new pension provider, open a SIPP and then ask your new pension provider to sort out the transfer for you. Simple!

If you’ve had lots of different jobs, the chances are you have a ton of old pensions lying around. In fact, the average UK resident changes jobs on average 5 times in their working life (according to AAT) – that means 5 pensions on average!

But as great as pensions are, having too many can make them easy to lose. Which is where a pension transfer often comes in! By transferring all your old pensions across to one new pension – like a SIPP – you’ll make them easier to manage. Oh, and you’ll usually be able to access cheaper fees too!

Here’s all you need to know about transferring your pensions to a self-invested personal pension (SIPP). Hint: it’s really easy to do, with companies like AJ Bell¹, here’s our AJ Bell review.

A pension transfer is when you transfer your pension funds from one pension provider to another (your pension provider is the company that looks after your pension for you). Simple!

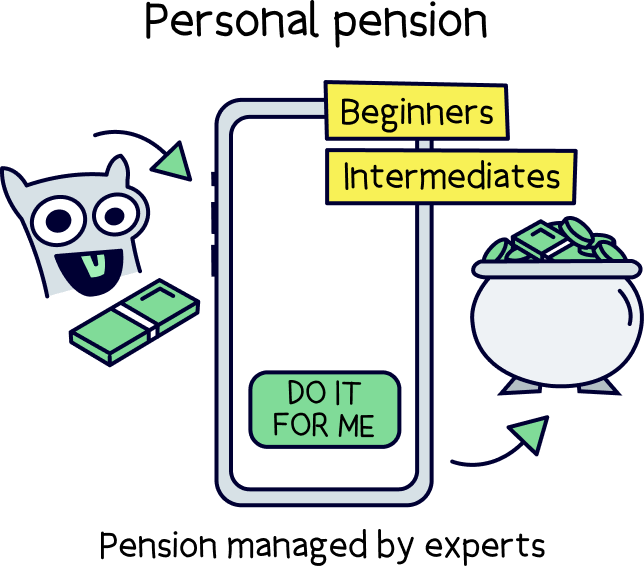

SIPP stands for self-invested personal pension, and is just a type of pension you can choose to transfer your other pensions to. It’s a kind of personal pension – that’s one you set up yourself, as opposed to a workplace pension, which is one your employer sets up for you (although they are both types of private pensions).

With most personal pensions, your pension provider will be pretty hands-on and will spend time trying to grow your savings for you. They do this by investing your pension savings into a pension fund or investment fund, which invests in things like stocks and shares (essentially where you own small parts of companies). As these companies increase in value, the idea is that your money will too and you’ll have more savings to live off than what you paid into your pension in the first place.

Find the best personal pension for you – you could be £1,000s better off.

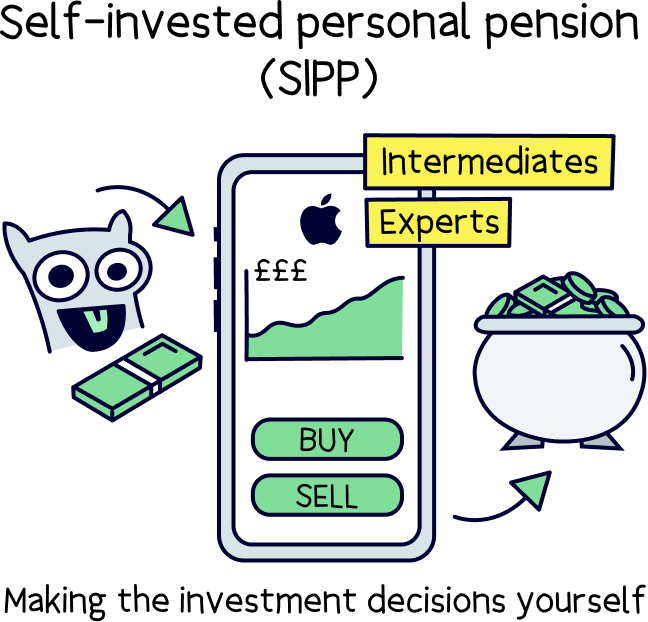

With a SIPP, your savings will also get invested. But instead of your pension provider handling that process for you, you’ll have to invest your savings yourself. That means you’ll choose exactly where your money goes, and will be responsible for your whole investment strategy.

In short, transferring your old and current pensions to a SIPP could be a great shout if you’re a bit of a pro at investing and you know what you’re doing (check out AJ Bell¹ if you are). But if you’re new to investing and you’d rather leave your savings in the hands of experts, you’ll probably be better off opting for a more standard personal pension, where your pension provider will look after your pension’s growth for you. Not sure what one to use? Try PensionBee¹, here's our PensionBee review.

Having said that, there are a few SIPPs that can be effectively managed for you too. You still make the investment decisions, but you decide from a smaller range of options that your provider offers, so it’s less complicated.

Don’t worry, you’ll have lots of options whatever you decide – check out our selection of the best private pension providers if you’re not sure where to start.

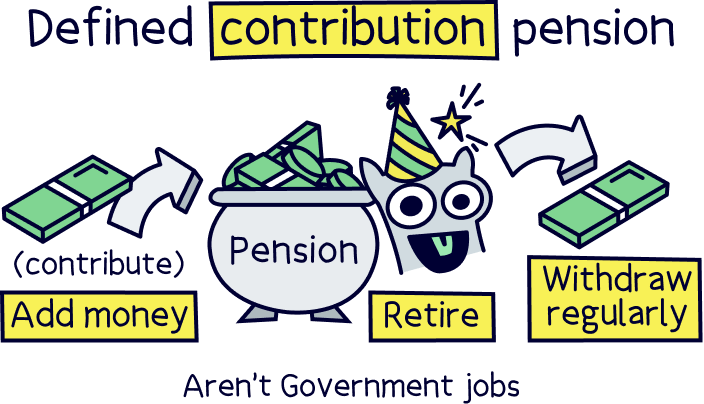

By the way, we’re talking about defined contribution pensions – which are private pensions all in your name, you decide how much to contribute, who manages it, and what to do with the money when you retire.

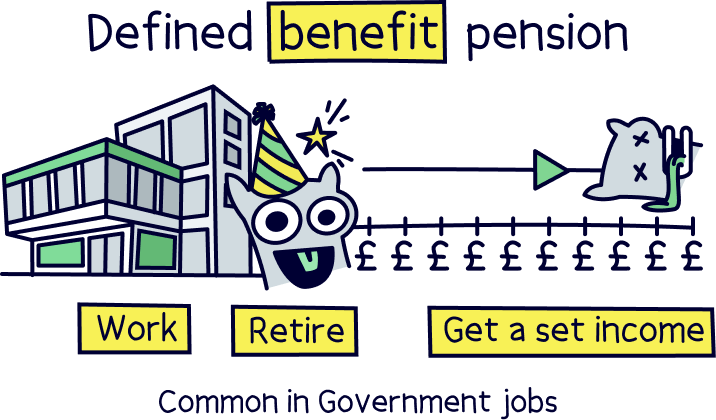

The alternative is a defined benefit pension, and you’ll find these in large public organisations like the NHS, where your retirement income is set per month when you retire, and depends on how long you’ve worked there and what your salary was (final salary pensions are an example of these).

Yes, you can transfer a company pension to a SIPP! In fact, one of the main reasons people choose to do a pension transfer is because they have lots of old workplace pensions lying around.

Let’s rewind for a second.

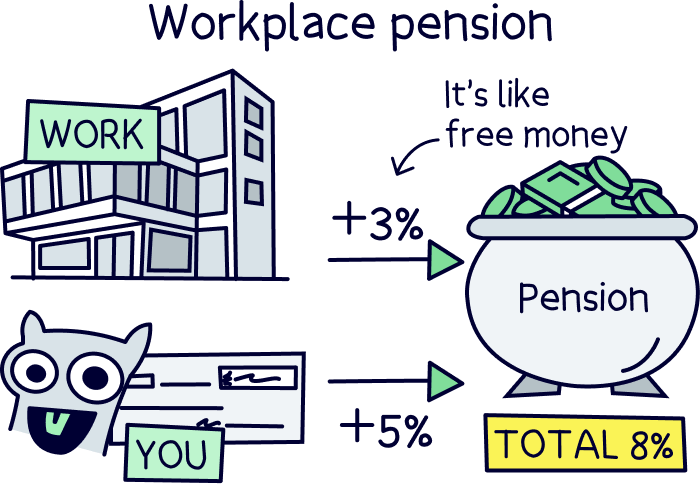

Workplace pensions are pensions that are set up for you by your employer. Normally, your employer will legally have to set one up for you (and they’ll legally have to contribute to it alongside you each month too – at least 3% of your salary from their own pocket, kerching!).

If you move jobs, you’ll stop contributing to your old company pension and it will become ‘frozen.’ Meanwhile, your new employer will likely have to set you up a new workplace pension, and you’ll start contributing to this instead.

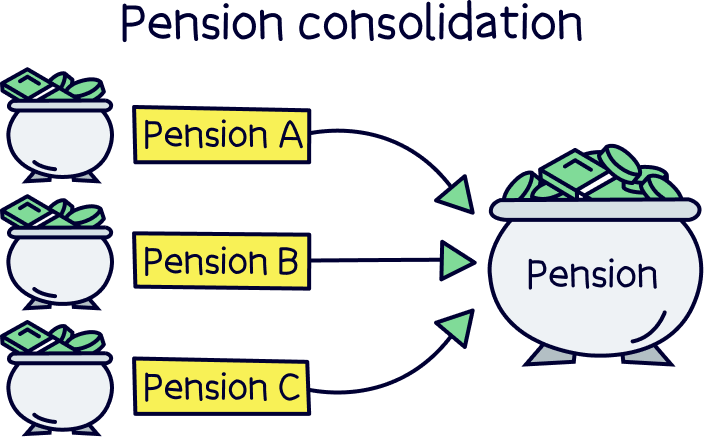

You can just leave your old workplace pensions sat where they are, ready for retirement. But you won’t be able to cash in a pension from an old employer until you’re at least 55! So, if you have a few of them dotted around, they can be pretty easy to lose – in fact, The Association of British Insurers found that there are around 3.3 million lost pension pots in the UK, worth around £31.1 billion altogether!

Instead, to make them easier to keep track of, it can be a good idea to transfer all your old pensions across to a new one, so all your pension funds are in one place. This is known as consolidating your pensions.

If you have an old workplace pension – or several – that you want to transfer to a SIPP, that should be pretty easy. Most pension providers that offer SIPPs will be happy to accept transfers from workplace pensions.

Just bear in mind that your workplace won’t usually be happy to contribute to a SIPP. So, if you want to carry on unlocking free money from your employer through their workplace pension contributions (hint: you definitely should!!), you’ll need to keep your current workplace pension with your current employer going alongside your new SIPP. Makes sense, right?!

If you have a defined benefit pension, which some large workplaces have in place (such as the NHS), which pays a set amount when you retire (rather than having a pension pot that you add to with a defined contribution pension), then it gets a bit complicated.

Often you might be better off keeping it where it is, because the income when you retire can be great (for instance a final salary pension). However, sometimes it is good to transfer it to a personal pension.

There’s no set rules, and it’s different for everyone. We recommend speaking to a financial advisor to give you tailored advice. And if the value of your defined benefit pension is over £30,000, you won’t be able to transfer it without independent financial advice. You can find the right financial advisor for you with Unbiased¹.

Note: the value of your pension is called a ‘cash equivalent transfer value’ (CETV).

Yes! Remember, a personal pension is one that you set up yourself – and a SIPP is just one kind of these.

The other kinds you might come across are stakeholder pensions and simply ‘personal pensions.’ These can both be easily transferred to a SIPP.

There are lots of different reasons why you might want to transfer a personal pension to a SIPP.

Perhaps you’re looking to consolidate multiple personal pensions, in the same way as we’ve described you can do with workplace pensions. Or maybe you’re after cheaper fees – that’s right, even though other kinds of personal pensions often have decent fees, SIPPs tend to be even cheaper! And of course, you might simply want to invest your money yourself, to get more control over your savings.

Ultimately, there’s no one right answer and it’s all about your own personal situation. Which brings us onto…

If you’re umming and ahhing about transferring a pension to a SIPP, you’re probably after a list of all the great reasons you should do it… right? Well, here are the main benefits.

As great as SIPPs can be, they’re not for everyone. Here are some things to think about before taking the leap and transferring your pension to a SIPP.

Convinced you want to transfer a pension to a SIPP? Then you’ll probably want to know how to do it. Luckily, it’s super easy – just follow these simple steps and you’ll have a SIPP in no time.

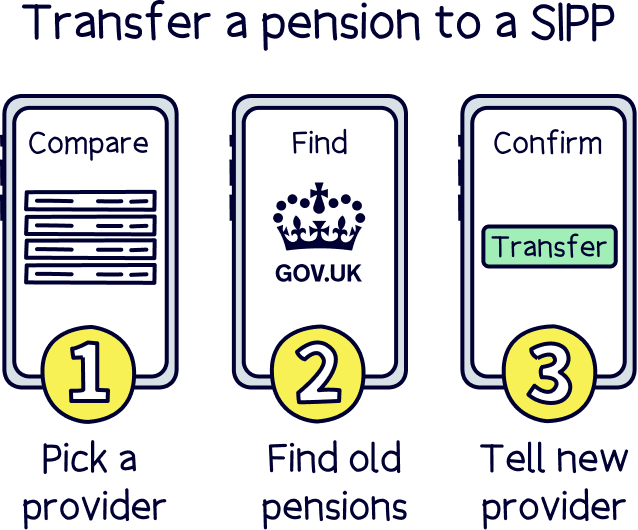

First things first, you’ll need to choose a new pension provider – this is the company you want to transfer your old pension to.

There are lots of different pension providers so you’ll need to spend some time deciding which is the best one for you – they’ll all have different fees and different investment options available to you. Oh, and remember to check that any pension providers you’re considering actually offer SIPPs, as not all of them will!

Don’t worry, we’ve done the hard work for you and have listed our pick of the best personal pensions for you to choose from, including the best SIPPs.

Anyway, once you’ve chosen your new pension provider, you just need to sign up with them and move onto step 2…

Find the best personal pension for you – you could be £1,000s better off.

Want more options? Find the full range with our best self-invested personal pensions.

Next, you’ll need the name of your old pension provider (or pension providers, if you’re transferring more than one pension!).

If you’re not sure which pension provider is looking after your old pension, don’t panic. The government has a handy ‘find a pension’ service which will help you to track it down – just head over to GOV.UK to get started.

Alternatively, your new pension provider (you know, the one you picked in step 1) will often be able to help you track down your old workplace pensions with their own online tools that they’ve developed for this purpose. Usually, you’ll just need to enter the name of your old employer and voila! They’ll give you the name of your old pension provider.

Either way, you just need to give your new pension provider your old pension provider’s name and then…

Now all that’s left is to sit back and relax as your new pension provider will sort the pension transfer out for you.

They’ll get in touch with your old pension provider to get the ball rolling. Sometimes, your old provider will get in contact with you to confirm that you definitely want to go ahead. But other than that, you won’t have to do a thing!

That’s right, you just sit back, relax and wait for those pension funds to show up in your new pension. Normally, this will happen within 2 to 4 weeks, although it could take longer. Told you that transferring a pension to a SIPP was easy!

There’s one important point to consider, and that’s the cost of leaving your current pension provider – some pension scheme providers are fairly greedy when it comes to exit fees!

Most likely there won’t be any fees to transfer your pension (if you have a more modern pension). But if you have an older pension, you might have some. Check your paperwork if you have any. If you have an older style pension and are over 55, the fees are capped at 1%.

However, just having to pay a fee doesn’t mean it’s not the right choice to transfer your pension. The benefits normally outweigh any cost – but you need to weigh up the decision yourself. If you’re unsure it’s best to speak to an independent financial adviser. You can find the best one for you with Unbiased¹.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Self-invested personal pensions are exactly the same as any other private pension. As long as you are 55 (or 57 from 2028), you can ‘retire’ and take the cash whenever and however you like.

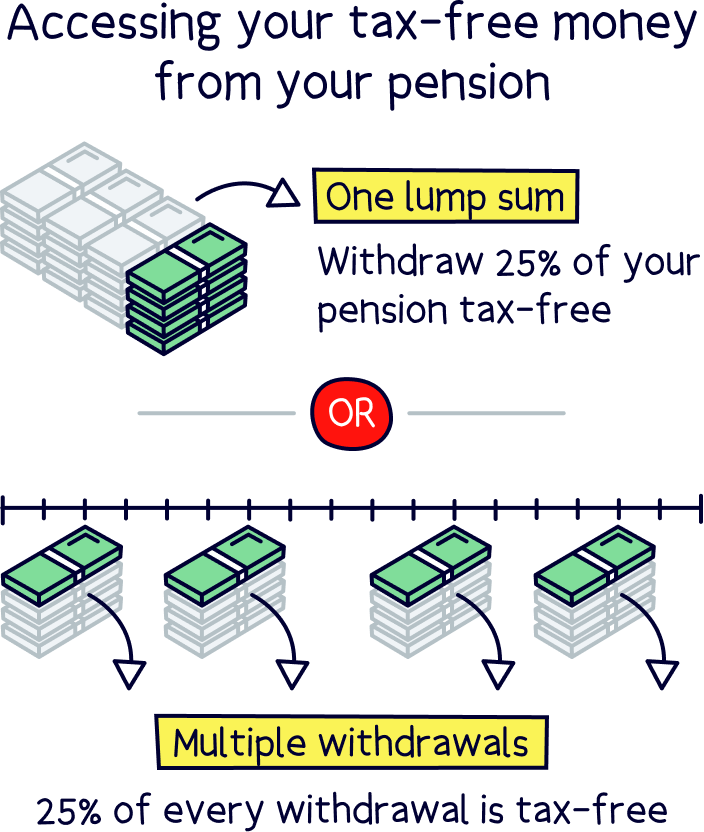

You can take the first 25% of your pension savings tax-free. Whoop! You can do this either as a tax free lump sum, or you can take it as regular income and the first 25% will be tax free, the rest you’ll pay Income Tax on, just as you would with your income now (e.g. your salary).

You can either keep your pension pot invested, and take a regular income, or you can use the funds to buy an annuity – which provides a guaranteed income for life (or sometimes a set number of years).

And when you reach State Pension age (66 but rising to 68), you’ll get the State Pension too. Provided you have made enough National Insurance contributions across your life (minimum 10 years, but you’ll need 35 years to get the full pension payment).

Transferring a pension to a SIPP is insanely easy. Just pick out a new pension provider from our list of the best private pension providers to get started (and make sure you choose a pension that’s managed by you, rather than a team of experts!). Then, you can just twiddle your thumbs while your new pension provider does all the hard work for you!

Just remember that SIPPs aren’t for everyone. If you’re an experienced investor already, they can be a great way of taking control over your savings, accessing more investment options and unlocking cheaper fees.

But if you’re a beginner or you’re fairly new to the world of investing, putting your savings in the hands of experienced professionals will probably be a better shout. After all, we’re talking about your life’s savings here – so you want to make sure they’re being looked after properly!

Ultimately, whether you transfer your pension to a SIPP, or you decide that transferring your pension elsewhere is a better way to go, one thing’s sure: by gathering your old pensions together in one place, you’ll be able to track your savings much more easily so you know exactly where your money is when you come to retire (cruises around the Caribbean, anyone?!).

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.