Article contents

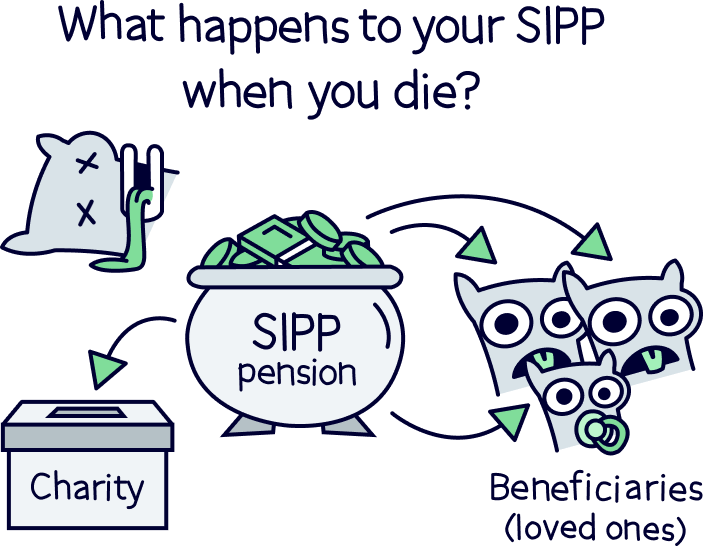

When you die, you can pass your SIPP onto whoever you want. Hooray! If you die before you’re 75 and the funds are transferred into your loved one’s name within 2 years of your death, your loved one will even be able to get the balance tax-free.

A self-invested personal pension (SIPP) is a great way of saving for retirement, and to tide you over later on in life – with massive tax advantages. But what happens to it when you die?

Well, it’s not exactly the cheeriest of topics (sorry!) but it’s not all doom and gloom. You’ll be pleased to know there’s even more tax advantages. You can pass your SIPP on to whoever you want when you die, so all those years of scrimping and saving won’t go to waste. Here’s the lowdown.

SIPP stands for self-invested personal pension. It’s basically a savings account that makes it really easy to grow your money so that you have enough to live on when you retire.

Find the best personal pension for you – you could be £1,000s better off.

With a SIPP, the money you put into your pension pot gets invested, similar to a Stocks & Shares ISA. That means it’s used to buy things like stocks and shares, which are essentially ownership stakes in companies. The idea is that these investments should increase in value over time, and when they do, you’ll make more money. Woohoo!

Just bear in mind that, like any other pension, you won’t be able to take money out of your SIPP until you reach a certain age. At the moment, that age is 55 but it’s rising to 57 in 2028 (and depending on how old you are, it may rise even higher by the time you’re ready to take money from your pension!).

If you’re thinking: ‘SIPPs sound pretty much the same as any other personal pension to me,’ then you’re not wrong! They aren’t very different at all! The main difference is that SIPPs allow you to choose and manage your own investments (or you can pay a financial advisor to help you – you can use Unbiased¹ to find the right one for you).

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

In other words, with a SIPP you’re in complete control and you can make changes to your investments or add new ones whenever you want. Plus, SIPPs often have a greater range of investments available than other pension types do – perfect if you like being able to pick and choose where your money goes!

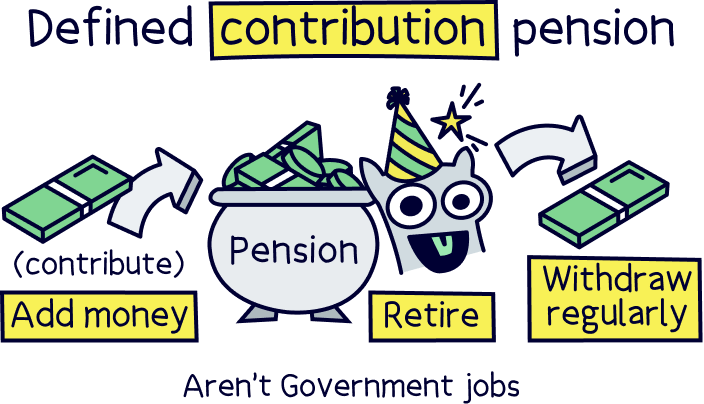

A SIPP is a type of defined contribution pension. Which is where you add money yourself (contributions), and decide how and where the money is managed. All personal pensions and most workplace pensions are defined contribution pensions (together they are called private pensions).

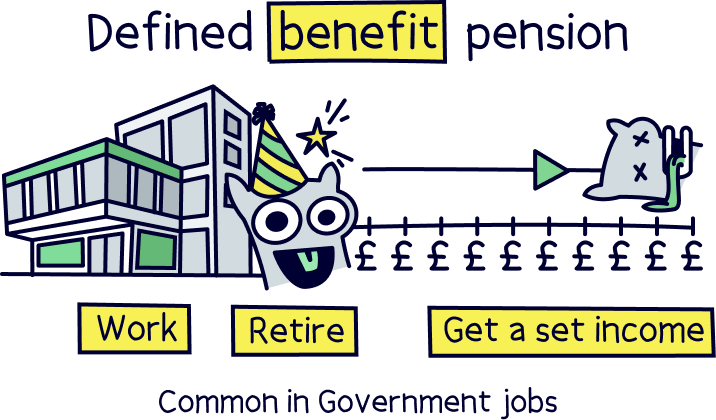

The alternative to this is a defined benefit pension, and these are common in workplaces such as the NHS. It’s where the income you receive from your pension when you retire is set by the rules of the pension scheme. It’s often dictated by how long you have worked, your salary, etc. You might have heard of a final salary pension, which is a defined benefit pension. These are not SIPPs.

We’ve got some good news for you. When you die, you can pass your SIPP onto whoever you want. So, all those years of saving and growing your money won’t go to waste – instead, your pension can go towards supporting your loved ones (or a chosen charity!) financially, even after you’re gone.

Better still, you don’t have to choose just one person to leave your pension to. Instead, you can split the funds between multiple people in whatever proportion you want. For example, you might choose to give 40% to your partner, 20% each to your 2 sprogs, 10% to your best mate and 10% to a charity that’s close to your heart (40% + 20% + 20% + 10% + 10% = 100%). It’s all up to you!

The people you want to leave your pension to are known as your beneficiaries. You can nominate them by letting your pension provider know who you want to leave your SIPP to (your pension provider is the company providing your pension for you). This is super easy and can normally be done by simply logging into your account online.

It’s not the nicest word, but the value of your SIPP is called ‘death benefits’, as it’s a benefit your nominated beneficiaries get when you pass away.

Note: your SIPP provider can also be known as your pension scheme administrator. And they’ll handle everything if you pass away while they still manage your pension.

So, what exactly can your beneficiaries do with your pension? Well, they can choose to take the funds (known as their ‘death benefits’) in 2 ways. They can either:

Whichever option they choose, they’ll be taxed the same. Which brings us onto…

Obviously, we hope you live well past the age of 75. But if you don’t, there’s a silver lining: your beneficiaries won’t have to pay any tax on your pension funds at all! If, on the other hand, you die after you turn 75, your beneficiaries will have to pay Income Tax when they withdraw funds from your pension (Income Tax is a tax that’s charged on their earnings each tax year).

Here’s all you need to know about SIPPs and taxes.

Inheritance Tax is a tax that’s charged on your belongings when you die. If everything you own added together (known as your estate) comes to more than £325,000, an Inheritance Tax of 40% will be charged on anything over that £325,000 threshold. Gulp!

But guess what? Your SIPP isn’t counted as part of your estate! So, your loved ones will be able to inherit the whole thing, without needing to pay a penny of Inheritance Tax on it. Kerching!

By the way, if you’re interested, here’s our guide to Inheritance Tax on ISAs.

Whether or not your beneficiaries have to pay Income Tax when they withdraw funds from your pension depends on when you die.

If you die past the age of 75, the funds your beneficiaries withdraw from your pension will be counted as part of their income.

In the UK, if you earn over a certain amount (currently £12,570, called your Personal Allowance), you have to pay tax on anything over that threshold. That means if your beneficiaries are earning over £12,570 (including the funds they withdraw from your pension) then they’ll need to pay tax on those funds.

The amount of tax they have to pay will depend on how much they’re earning.

The only exception is if you’re not leaving your SIPP to a person (for example, you might choose to leave it to a trust, which is a legal way of storing money for someone else). In this case, the funds have to be withdrawn as one big lump sum and the payment will be taxed at 45% (eek!).

But at the other end of the scale, if you choose to leave your SIPP to a charity, they won’t have to pay any tax on the lump sum as long as you don’t have any surviving dependants (a dependant is someone who relies on your income, such as a child who’s in full-time education).

We have some good news! If you die before you turn 75, the funds your beneficiaries take from your pension won’t count as part of their income. This means they won’t have to pay any tax on them. Get in! (Of course, we hope you live a lot longer, but at least there’s something to celebrate if not!)

There’s just one requirement: the funds must be designated to your beneficiaries within 2 years of your death (designating your pension funds just means transferring them into your beneficiary’s name). If the funds aren’t designated to your beneficiaries in time, your beneficiaries will be charged tax whenever they withdraw money from the SIPP, in the same way as if you died past the age of 75.

Don’t panic though! 2 years is plenty of time to designate the funds to your beneficiaries. So, this usually won’t be a problem although, of course, it’s still something to bear in mind.

Once you get to the age of 55 (or 57 from 2028), you can choose to start dipping into your pension pot. There are a few different ways of accessing the money, but one thing you can do is use some or all of the funds to buy a guaranteed income, known as an annuity.

This could be an income that’s guaranteed for the rest of your life, known as a lifetime annuity, or one that’s only guaranteed for a set period of time, known as a fixed-term annuity. This income is then treated like any other income and is subject to Income Tax.

So, what happens to it if you die?

Well, normally when you die, the payments will stop. However, some providers will let you nominate a beneficiary for your annuity in the same way as you can for your SIPP. In this case, your beneficiary can receive the income in your place. The only problem is that you can normally only nominate someone at the start of your contract, so if things change partway through (for instance, you nominate your spouse and then get divorced), your plans could get foiled!

That said, you often won’t have to use the whole of your SIPP to buy your annuity. If you still have some funds left in your SIPP, this can be passed onto your loved ones as normal (and tax-free if you’re under the age of 75 when you die!).

Okay, so let’s imagine you’ve passed your SIPP onto your beneficiary and they’ve been taking a regular income from it. Now let’s imagine that they sadly pass away too, leaving some funds in the SIPP. What happens now?!

Well, the good news is that the SIPP can be passed down to their beneficiaries in exactly the same way as you passed it down to them. Your loved one will just need to nominate their own beneficiaries. If your loved one dies before the age of 75, their beneficiaries will be able to get the funds tax-free. Or, if your loved one dies after the age of 75, their beneficiary will be able to access the funds subject to tax.

In this way, a SIPP can be passed down again and again until there are no funds left. What a legacy!

A SIPP can be a fantastic way of growing your money ready for retirement. But better still, you’ll know that none of your hard work will go to waste – if you pop your clogs and can’t benefit from your SIPP yourself, your loved ones will still be able to (they’ll claim your SIPP death benefits).

Not only will you save from all that tax from saving within your pension during your life, if you do pass away, your family won’t pay any tax either – a pension doesn’t form part of your estate when you die. It passes to any beneficiary you name with the pension provider (the pension scheme administrators).

That’s if you die before 75, and your beneficiary receives the whole lot tax-free. After 75, they'll have to pay Income Tax (if they withdraw enough to qualify for Income Tax themselves). They can take it as a lump sum or a regular income, just as a regular pension.

Looking to open a SIPP? We’ve put together a table of the best SIPPs if you’re looking to make your own investments. You can also check out the best expert-managed personal pensions too, if you want the experts to handle things for you. You could even do both!

Keep up the retirement saving and you’ll be living it large when you retire – sipping margaritas on cruise liners before you know it!

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.