Article contents

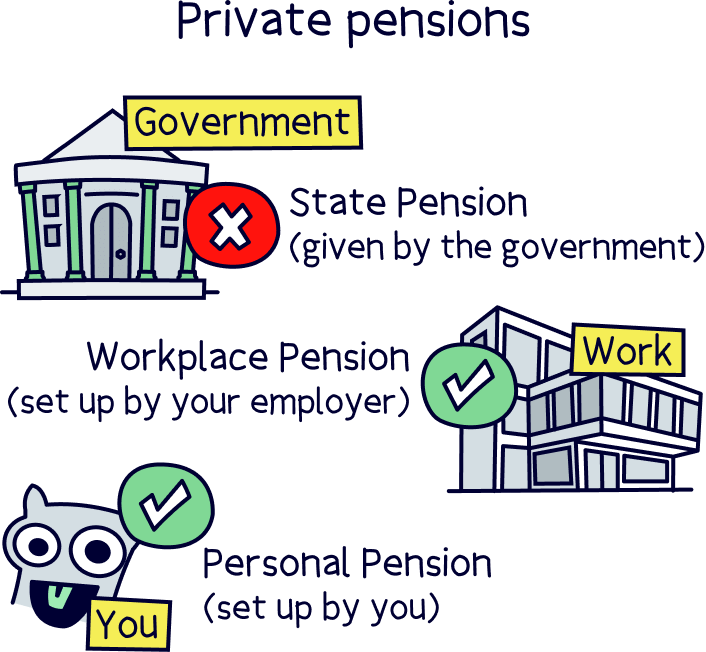

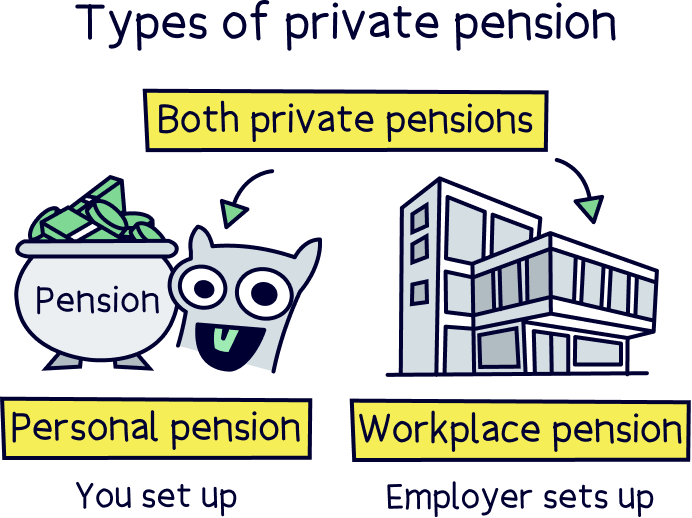

Yep! A workplace pension is a private pension, which simply means a pension private to you, so in your name, and you own it. Rather than a public pension, which is the pension you’ll get from the government, called the State Pension (at State Pension age, currently 66).

Yep! A workplace pension is a private pension, so it’s private to you – in your name, and you normally decide how much to pay into it, and later when to start withdrawing from it (normally when you retire).

It’s different to the public pension, which is the government pension, called the State Pension, and is what you’ll get when you reach State Pension age (currently 66). That’s provided you’ve made enough National Insurance contributions during your lifetime (at least 10 years, but 35 years for the full amount).

You’ll get the State Pension in addition to your private pension (your workplace pension). However, it’s likely not enough to tide you over in retirement by itself, and that’s where private pensions come in (unfortunately it doesn’t even come close to what you’ll need for a comfortable retirement (more on that later)).

Here’s where it gets a bit confusing. There’s a few different types of private pensions, and there’s multiple types of workplace pensions.

Let’s start with workplace pensions.

Depending on where you work will depend on what type of pension you’ll have, and which workplace pension scheme they’ll use.

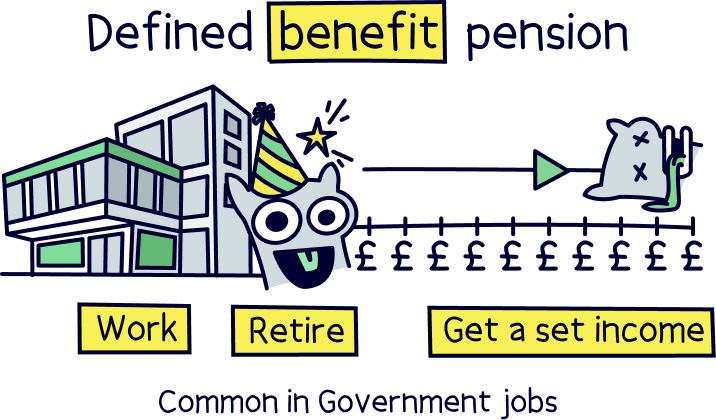

If you’re in a public sector job, such as the NHS, or another government role, you’ll typically have a defined benefit pension, and if you’re working for a regular business (private sector), you’ll normally have a defined contribution pension.

A defined benefit pension is where you’ll get a set retirement income when you retire, often guaranteed for life. The amount you’ll get is based on things such as how long you’ve worked there, and what your salary was.

They can often be called final salary pensions, or average salary pensions. Although you’ll be lucky to get a final salary pension these days (which is where you retire on the same amount you got paid as your final salary).

You’ll pay into it over your career directly from your salary, and the scheme can be operated by the organisation itself, such as the NHS.

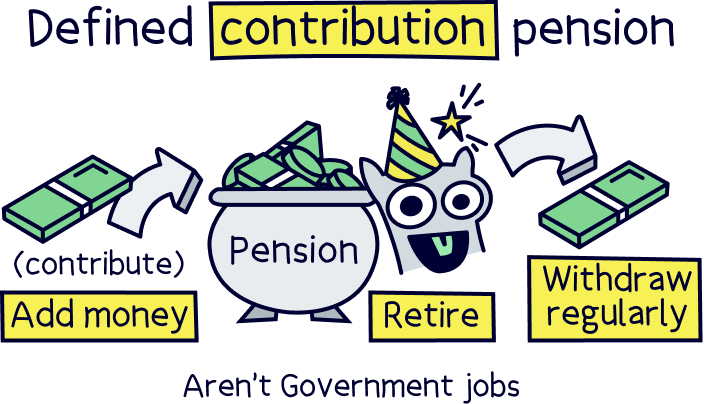

A defined contribution pension is where your pension is more in your control, and you’ll decide how much you want to pay in, often taken directly from your salary before you pay any tax (but you can also set up a personal pension, more on these later).

They typically have a financial value, which grows over time, called a pension pot, such as £100,000.

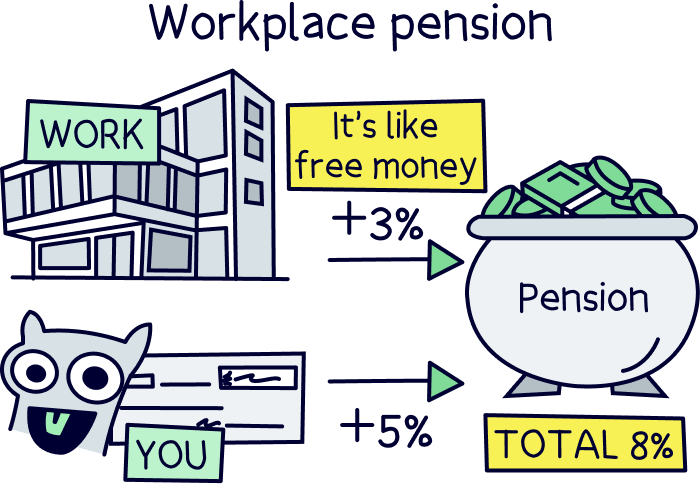

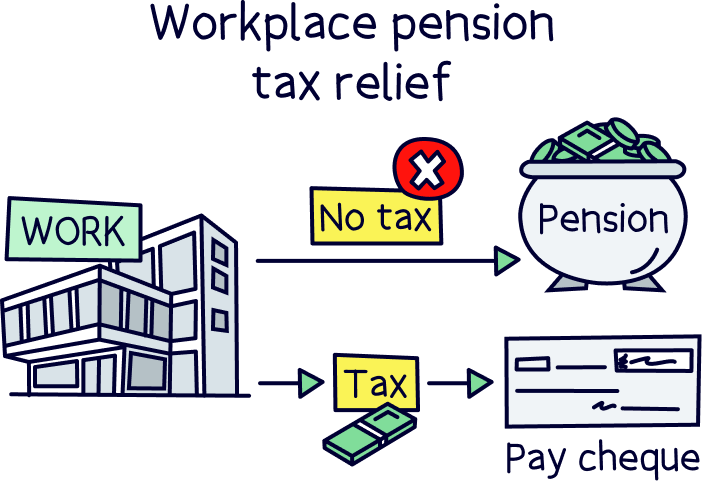

Your employer will typically set it up for you, and register you onto their workplace pension scheme, called auto-enrolment, and they’ll also contribute too (required by law). If you pay in a minimum of 5% of your annual salary, your employer has to contribute 3%.

Some nice employers might pay in a bit more if you pay in more too (it's worth asking).

Your pension will grow tax-free too, so it can grow much faster over time. You might pay tax when you withdraw from it, it depends on your income at the time.

You can start withdrawing from it at age 55 if you want to (57 from 2028), and 25% of it will typically be tax-free, which you can take as a tax-free lump sum if you like. (Although it’s often a good idea to keep it growing over time, until you really need it and retire.)

As mentioned, a workplace pension is set up by your employer, and you’ll typically make pension contributions through your pay each month, before you pay any tax.

These can be either a defined benefit pension, if you’re in a public sector job, such as the NHS. Or, they can be a defined contribution pension, if you’re in a private sector job (regular job) – we’ve run through both above.

Your employer will decide which pension provider (company) to use, but you may get a choice from a few different pension plans (where your money is actually invested).

A personal pension is a pension that you’ll set up yourself, so you decide which pension provider to use, and you’ll pay into it after you’ve been paid (as and when you want to).

You’ve got a lot more control compared to a workplace pension, and can decide how you’d like your pension to be invested so it grows over time (pensions are invested to help them become more valuable over time) – either with experts (recommended for most people), or making your own investments (which is called a self-invested personal pension, or SIPP).

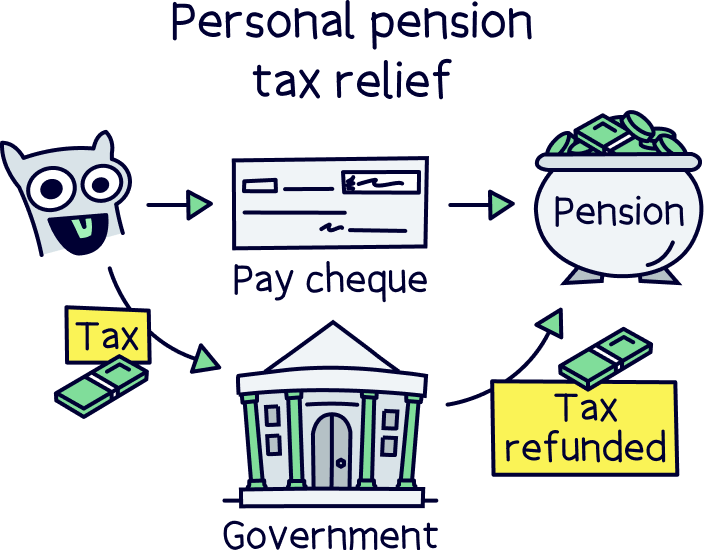

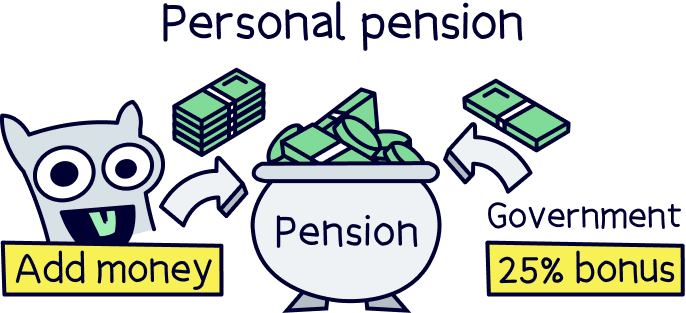

You can save into them tax-free, but as you’ve already paid tax on your income (e.g. your salary), the tax you’ve paid is refunded back into your pension pot when you add money (make contributions).

This works as a 25% bonus from the government when you save, added automatically into your pension pot.

And, if you’re a higher rate taxpayer (paying 40% tax, earning over £50,270), or an additional rate taxpayer (paying 45% tax, earning over £125,140), you can claim back some of the tax paid too (on a Self Assessment tax return). If you need help filling in your Self Assessment tax return, chat to Taxfix¹, their service is low cost, quick and 5* rated.

Personal pensions are pretty great to boost your total pension pot, alongside a workplace pension, as you’ll need a very hefty pension pot to afford a comfortable retirement these days (we’ll cover that just below).

Check out PensionBee, it’s easy to use, has low fees and a great record of growing pensions over time.

Nuts About Money tip: if you’re self-employed, or become self-employed in future, a personal pension is your only option, but a great one. Learn more with our guide to self-employed pensions.

It’s a great idea to plan ahead for your retirement, and take control of your own retirement savings, rather than relying on just your workplace.

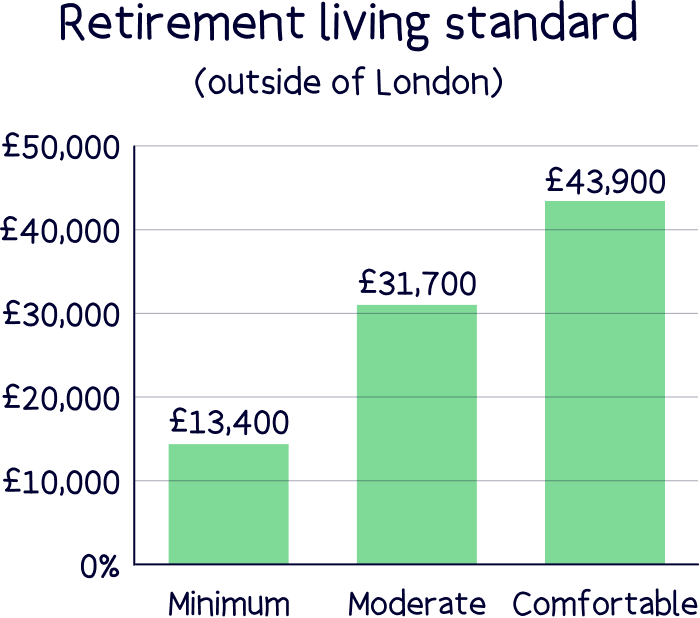

To afford a comfortable retirement, you’ll need a whopping £881,719 in your private pension pot to provide a retirement income of £43,900. Yikes.

This income figure was determined by the Pensions and Lifetime Savings Association, and there’s 3 different income levels: minimum, moderate and comfortable. Together, they’re called the Retirement Living Standards…

Note: it’s assumed you won’t have any housing costs, such as rent or mortgage payments (it’s presumed you have paid off a mortgage).

Here’s what each retirement standard looks like:

Oof. That’s a lot isn’t it? And that’s including receiving the State Pension (the government pension). We’ll cover that in just a bit.

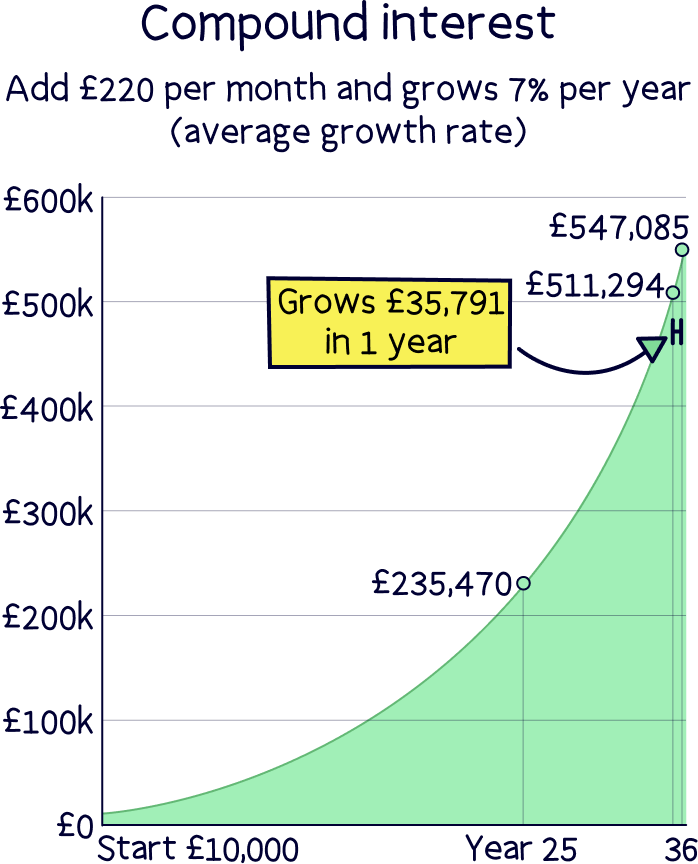

Don’t lose hope though – pensions are really great at building up your retirement savings over time. That’s thanks to something called compound interest, which is where the money you make, begins to make money too, and this snowballs over and over, turning smaller amounts into very large amounts of time.

Let’s use an example. Imagine you have a pension pot currently worth £10,000, and you’re able to save £220 per month. If it grew at an average of 7% per year, after 25 years you’d have a massive £235,470!

Another 10 years and it would grow to £511,294, nearly double! And then just one year after that, you’d earn £35,791. How great is that?

The key is to start saving as soon as you can, and save as much as you reasonably can. That way the compounding effect has longer to work its magic, making your future brighter and brighter every day.

Now you can simply save more into your workplace pension if you want to, and it’s a good idea to make the most of the free cash from your employer, by paying in at least 5% per year, so they’ll pay in 3%.

And if they’ll add more if you add more, then take full advantage and put in as much as needed to get the most free cash (e.g. if they add 7% if you add 7%, then try and add 7%).

After that, it’s often a good idea to switch to a personal pension to continue saving. That’s because you get full control over your pension savings, rather than your employer.

Workplace pensions via your employer aren’t necessarily the best pensions out there, some have high fees, bad customer service, and don’t grow too much over time. Employers often just pick any old one to get the box ticked that they offer a pension, rather than picking the very best pension out there.

Think of a pension a bit like your mobile phone contract, or broadband provider – it pays to shop around and find the best deal and provider for you.

So, taking control of your pension with a personal pension means you can pick the best pension provider for you (such as one that’s easy to use, has low fees and a great record of growing pensions over time, alongside great customer service). More on those just below.

And, you can also decide where or how you’d like your pension invested (either letting the experts handle things, or making your own investments).

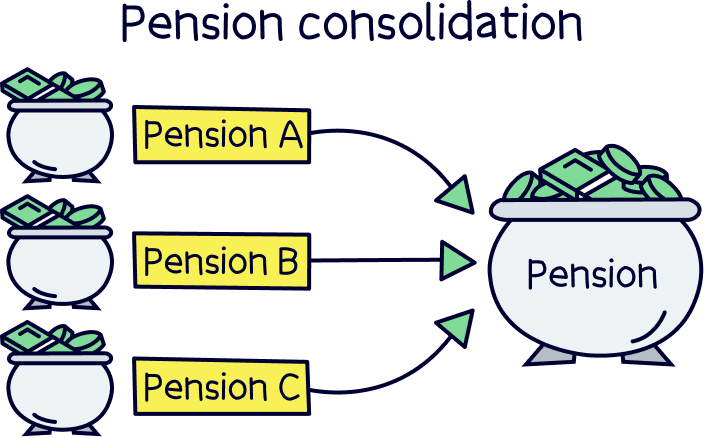

You’ll also be able to transfer your pension to another provider whenever you like in future, so you can always be with a top provider. You can’t transfer your current workplace pension (but you can transfer your old work pensions into a new single personal pension, which is called pension consolidation).

To make things easy for you, we’ve reviewed all the top personal pension providers. And here they are…

Easy to use, and you can leave the investing to the experts.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Check out PensionBee, it’s easy to use, has low fees and a great record of growing pensions over time.

To make your own investment decisions.

0% fees

InvestEngine is a super low cost investment platform allowing you to save and invest within a pension and an ISA, and with a great range of investment options.

There's no fees for an account, and no commission to buy and sell investments. And there’s a wide range of investment options, with over 700 investment fund options (ETFs only).

It's more than just low cost though, it’s pretty easy to use, there’s some great features to help you invest, and the customer service is excellent.

Minimum deposit: £100

Best for: those looking for a low cost platform with a range of fund options

• Easy to use

• Very low cost

• Commission-free

• Great range of ETFs

• Great customer support

• Only ETFs (but a wide range)

• No financial advice

AJ Bell is well established, with a good reputation.

It's one of the cheapest SIPPs out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is excellent too.

Overall, it's one of the best options for a SIPP.

Offers available

Interactive Investor is a well established company, and very popular.

Instead of paying a percentage of the investments in your account (like other investment companies), you’ll instead pay a fixed fee per month – and it’s pretty low, starting at just £5.99 per month for a pension (SIPP).

This makes it one of the cheapest SIPP providers out there, especially if you have a fairly sizeable amount within your pension (e.g. over £30,000).

On top of that, there’s a huge range of investment options (e.g. shares and funds) – one of the largest.

It's easy to use, and the website and app are great. The customer service is excellent too.

A great choice overall.

Check out PensionBee, it’s easy to use, has low fees and a great record of growing pensions over time.

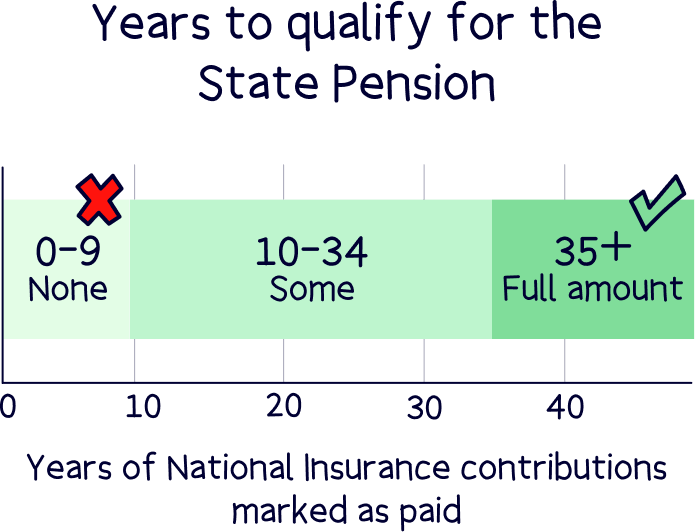

You’ll also likely get the State Pension, which is the pension you’ll get from the government when you reach State Pension age (currently 66).

It’s currently £230.25 per week (£11,973 per year), so not enough to live on for most people – which is why private pensions play a vital role in providing a retirement income later in life.

In order to get the State Pension, you’ll need to have paid at least 10 years worth of National Insurance contributions, and 35 years to get the full amount.

There we have it. A workplace pension is a private pension – which is a pension all private to you. It’s in your name, you decide how much you want to save, and later on, when and how much you want to withdraw from it.

There’s two types of workplace pensions, a defined benefit pension, which are typical in government jobs, such as the NHS, where you’ll get a guaranteed income when you retire (often for life).

And then there’s a defined contribution pension, which is common in private sector jobs, where both you and your employer will pay in (you 5% and your employer 3%), so you get some free cash from your employer.

They’re pretty great overall, and can really boost your retirement income over time – and working together with a personal pension (one you set up yourself) can really improve your financial future, providing that comfortable retirement you deserve.

If you’re looking to start a personal pension, check out PensionBee¹, it’s easy to use, has low fees and a great record of growing pensions over time. Beach¹ is also really great, they don’t just cater for pensions, they have an easy access account too (a tax-free ISA), plus the app is easy to use and the customer service is excellent.

Happy saving!

Check out PensionBee, it’s easy to use, has low fees and a great record of growing pensions over time.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out PensionBee, it’s easy to use, has low fees and a great record of growing pensions over time.