Article contents

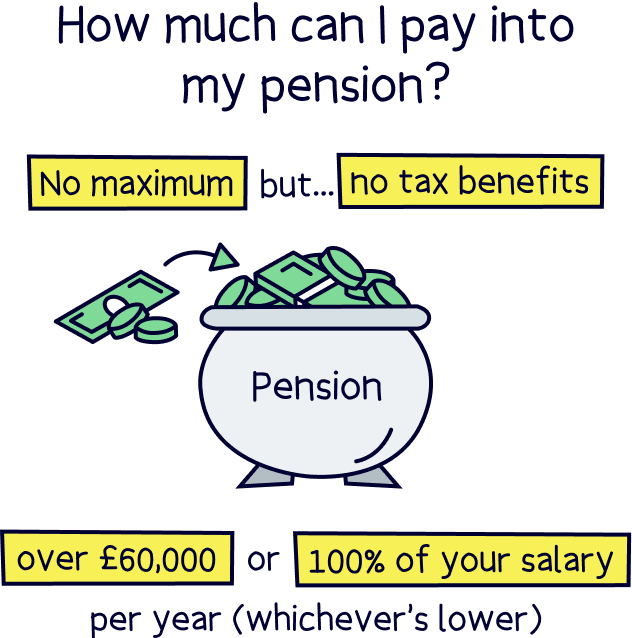

In the UK, you can pay as much as you want into your pensions. But you’ll probably want to avoid contributing more than £60,000 each year or 100% of your salary (whichever’s lower). Otherwise, you won’t get the same tax benefits.

Starting a pension is a great way to make sure you’re going to have enough money to live comfortably later on in life. After all, pensions come with lovely tax benefits and they’re a great way to grow your savings over time. But is there such a thing as saving too much when it comes to pensions?

Well, yes! Even though you can technically pay as much as you want into your pension, the tax benefits just won’t be the same if you save more than a certain amount (although this amount is pretty high, so it won’t really apply to most people!). Here’s the lowdown.

In the UK, there’s no maximum pension contribution. Instead, you can add as much into your pension as you want. And of course, the more money you add into your pension, the more financially secure you’ll be later on in life. Nice!

HOWEVER, even though you can technically put as much money as you want into your pension, there is such a thing as ‘too much.’ If you save over £60,000 each year or 100% of your salary (whichever’s lower), which is your annual allowance, you won’t get all the lovely tax benefits that pensions normally come with.

Let us explain.

The government wants to encourage you to save up for your golden years so they’re not left propping you up in your old age. To incentivise you, they give you this lovely thing called ‘tax relief.’ In other words, you don’t have to pay any tax on the income you earn (such as your salary) that you go onto pay into your pension pot. Kerching!

If you have a workplace pension (one that’s set up for you by your employer), your tax will get worked out before you receive your pay cheque. So, it’ll mean less of your earnings will go to the taxman (or woman!) and more will end up in your own pocket.

On the other hand, if you have a personal pension (one you set up yourself), you’ll just pay your tax like normal. Then, you’ll get a tax refund, with any tax you’ve overpaid going straight into your pension pot. That means you’ll get a lovely bonus from the government every time you contribute to your pension.

Note: a workplace pension and a personal pension are both types of private pension. The State Pension is a public pension.

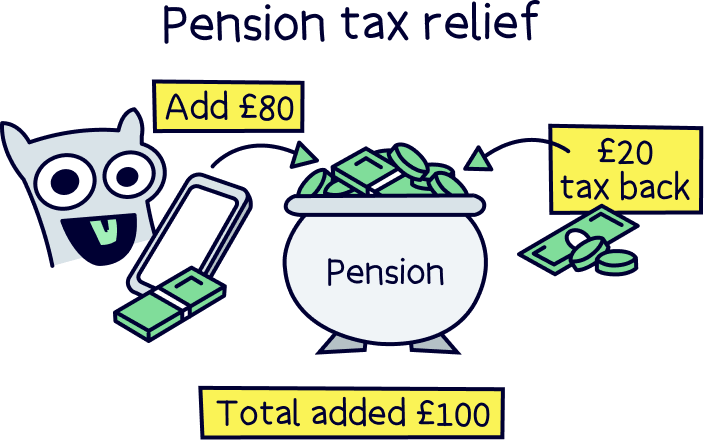

Let’s say you’re a basic-rate taxpayer (someone who earns less than £50,270 per year). In this case, you’ll get 20% tax relief – which means if you pay £80 into your pension pot, the government will add a £20 bonus to turn it into £100 (£20 is 20% of £100). On the other hand, if you’re a higher earner and you pay 40% or even 45% tax on some of your income, you’ll be able to get some tax relief at 40% or 45% too. Get in!

You’ll often hear this called a government bonus, and it actually works out as a 25% bonus on whatever you pay into your pension. Plus, it’s added automatically. Although you’ll have to claim the 40% or 45% portion back on your Self-Assessment tax return (it’s easy to do but if you want help try Taxfix¹, their service is rated 5*).

So, what does this mean in terms of maximum pension contributions?

Well, the government wants to help you save for retirement, but they don’t want you taking the mickey either. So, they’ll only give you that lovely tax relief up to a certain amount, which is £60,000, or your total income (e.g. salary), whichever is lower. We'll explain this in more detail below.

Find the best personal pension for you – you could be £1,000s better off.

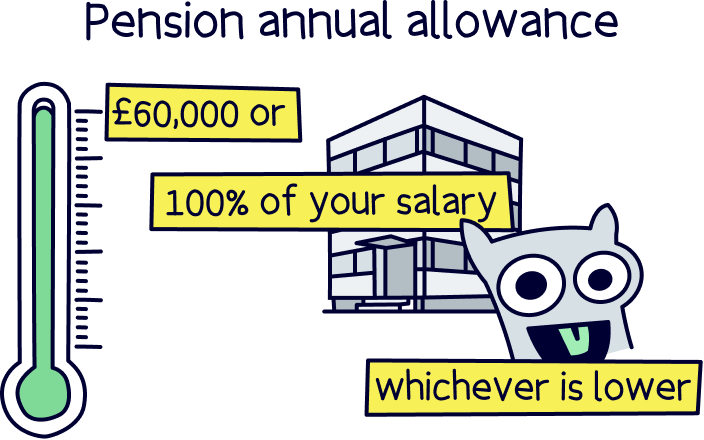

At the moment, the maximum you can pay into your pension each year (while still benefiting fully from that lovely tax relief we told you about!) is £60,000 or 100% of your salary – whichever is lower. This is known as your annual allowance.

Don’t worry if that sounds confusing – let’s look at some examples.

Imagine you earn £30,000. In that case, your annual allowance will also be… wait for it… £30,000. The figures are the same because you’re earning under £60,000 per year.

Now let’s say you earn £100,000. That means your annual allowance will be £60,000 (because you’re earning over £60,000 per year – the same would apply if you earned £60,001 or anything over that).

Makes sense, right? The only exception is if you’re over the age of 55 and you’re already taking an income from your pension. In this case, you can still continue contributing to your pension (and topping up your savings!) if you want to. But your annual allowance will be much smaller – normally £10,000.

Right, now we’ve cleared that up, you’re probably wondering what happens if you go over your annual allowance.

Well, you’ll still be able to claim tax relief on some of the money you add into your pension. But anything on top of the annual allowance will be subject to an annual allowance charge – that’s just the government’s way of trying to claw back any tax relief they’ve given you on that money.

That said, you can carry forward your annual allowance for three tax years (tax years are like calendar years except instead of starting on the 1st of January, they start on the 6th of April). So, if you haven’t maxed out your pension contributions for the last three tax years, you might be able to put more into your pension this year to make up for it. Let’s dive into that a bit more.

If you want to pay more in this year than your annual pension allowance (so £60,000 or your total income, whichever is lower), you might be able to do this if you didn’t use up all of your allowance in the previous 2 years, and this year. (you carry forward your allowance.)

This is called the personal carry forward rule, and effectively any unused allowance you have, you can use in this year! Pretty great right if you get a lump sum like a bonus from work, or some inheritance, or just got lucky on the lottery!

A lot of us will be worrying about the need to save more, not less into our pensions. So, how much should you be contributing?

Well, it depends! One general rule is to take your age and halve it to work out how much of your salary you should be contributing. So, if you’re 30, that would mean paying 15% of your salary into your pension pot (half of 30 is 15).

However, we get that that’s a lot of money – especially if you have a family to feed!

Of course, the more money you pay into your pension, the more financially secure you’ll be later on in life. But at the same time, it’s important not to overstretch yourself either – you won’t usually be able to withdraw your pension before 55, so you’ll need to leave yourself enough money to enjoy life now, as well as later!

At the end of the day, the most important thing is to start saving as soon as you can, and to add to your pension whenever you’re able to. That way, your money has as much time to grow as possible and you can hopefully turn small amounts into something much bigger over a long period of time!

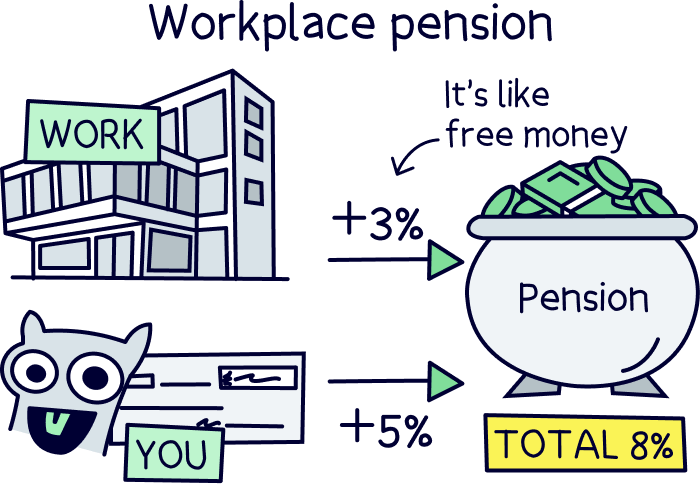

If you’re an employee, the chances are you have a workplace pension (remember, that’s a pension that your employer has set up for you!).

With a workplace pension, you’ll generally have to contribute at least 5% of your earnings each month. Meanwhile, your employer will legally have to contribute to it themselves too – at least 3% of your earnings, from their own pocket (woohoo!).

But what happens if you have some extra cash handy that you want to save for retirement?

Well, you can increase your workplace pension contributions. Sometimes, this can be worth it because a few (very generous!) employers will offer to up their employer contributions if you up yours – so it can be a great way to unlock free money! Chat to your employer to see if they do this.

However, most employers won’t want to give you more than they have to (we know, we know, it’s a shame!). So, most of the time, you’ll be best off starting a personal pension alongside your workplace one (remember, a personal pension is one you set up yourself).

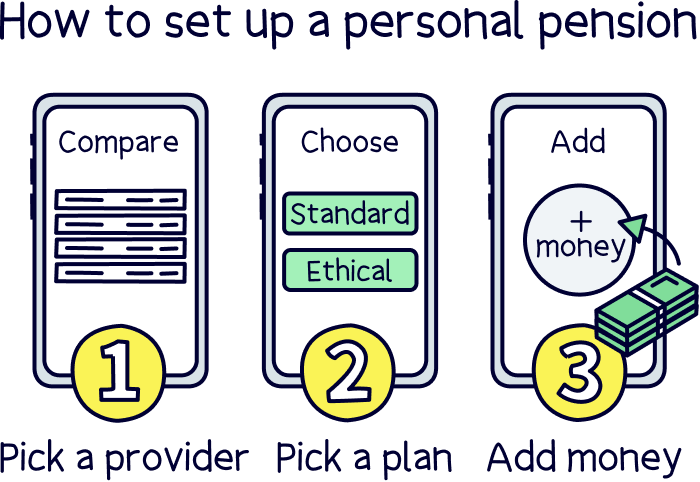

With a personal pension, you get to choose your pension provider yourself (unlike with a workplace pension, where your employer picks your pension provider for you). That means you’ll be able to choose a company with cheap fees. And even more importantly, you can choose one that has a good track record for growing pensions quickly, meaning you’re likely to end up with more money to enjoy during retirement!

Luckily, setting up a personal pension is seriously quick and easy. Especially if you use a modern pension provider, like PensionBee, that does everything online via a handy mobile app!

If you’re not sure where to start, we’ve made things easier for you by putting together a list of the best personal pensions. Alternatively, you can check out a couple of our favourites.

We’ve mentioned PensionBee briefly already, but it’s great for beginners – you don’t need to know anything about pensions beforehand and its handy mobile app makes everything super simple (oh, and they have low fees and great customer service too!).

Beach¹ is also really great, they don’t just cater for pensions, they have an easy access account too (a tax-free ISA), plus the app is easy to use and the customer service is excellent.

Technically, you can pay as much as you want into your pension pots. However, if you want to make the most of that lovely thing called tax relief, you’ll want to avoid paying in more than £60,000 per year or 100% of your yearly salary – whichever one is lower. Yep, we know, it’s unlikely you’ll have that much spare cash lying around, but it’s better to be safe than sorry!

Similarly, unless you want to face hefty tax charges, it’s probably best not to let your pension pots build up to more than £1.073 million. It’s true that might sound like A LOT, but it’s easier to do than you might think – all because pensions can be so great at growing your money!

Anyway, while these allowances are great to bear in mind, most of us will probably be thinking about saving more, not less into our pensions. And if that sounds like you, starting a personal pension is a great way to top up your income in retirement – even if you already have a workplace pension ticking along nicely.

If you’re self-employed and so haven’t got a workplace pension scheme, we highly recommend getting the ball rolling with your retirement planning and opening a personal pension as soon as possible! The sooner you build up your retirement savings, the more you’ll have when you retire.

Luckily, it’s really easy. Just check out our selection of the best personal pensions and you’ll be on your way already. Your older self will thank you for it!

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.