Article contents

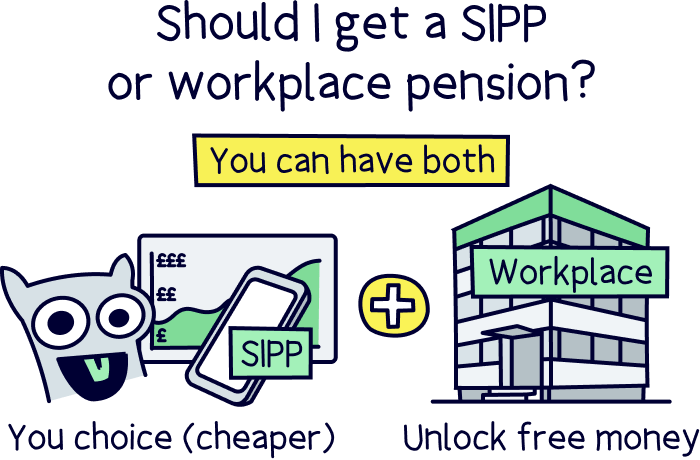

You don’t need to choose between a SIPP and a workplace pension, you can have both. Your workplace pension will allow you to unlock free money from your employer, while a SIPP is a great way to boost your savings for retirement.

Pensions are designed to help you save for retirement, so that you can live your golden years to the full. So, starting a pension is super sensible. But there are a few different kinds of pensions floating around.

If you’re umming and ahhing about whether a SIPP or a workplace pension is best for you, guess what? You don’t actually have to choose between them. In fact, having both is often a really good shout. Here’s the lowdown.

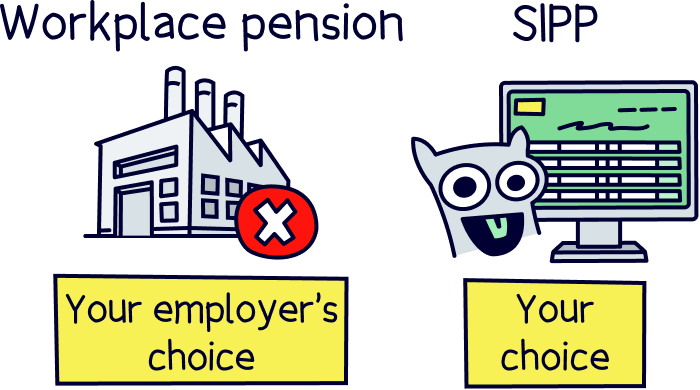

Okay, to start with, you’ll probably want to know the difference between a SIPP (self-invested personal pension) and a workplace pension. They’re both great ways of saving for retirement. But, surprise surprise, they’re great in different ways!

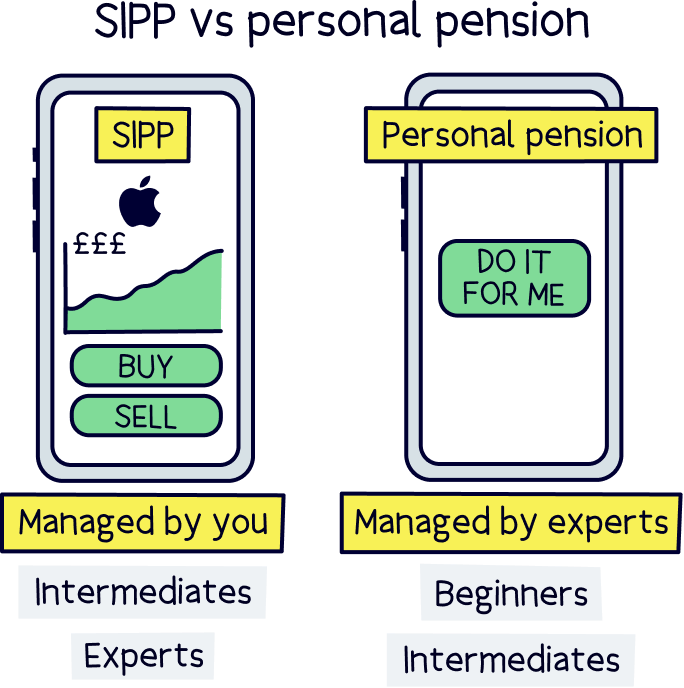

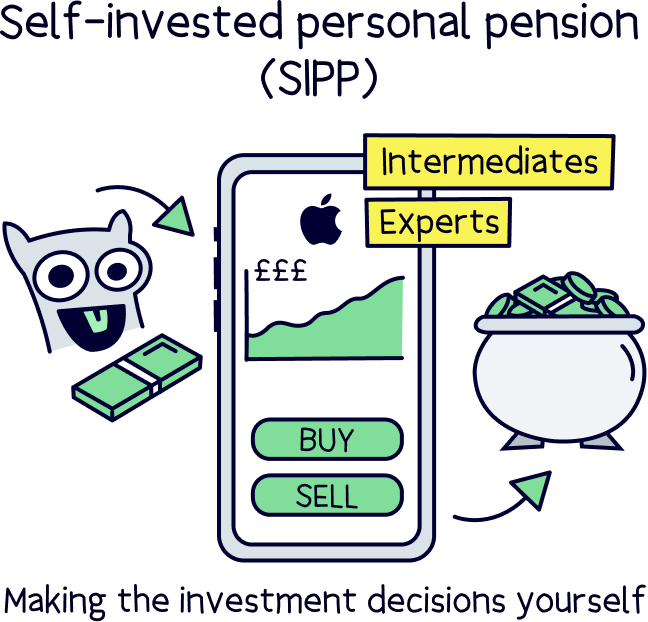

SIPP stands for self-invested personal pension. It’s a type of personal pension, which means it’s one you set up yourself (in contrast to workplace pensions, which are pensions your employer sets up for you).

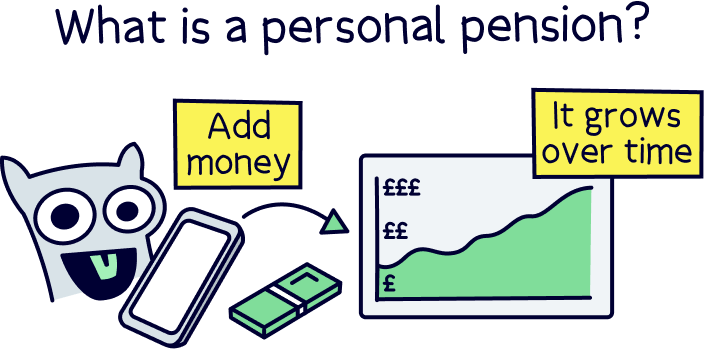

Personal pensions like SIPPs work a bit like piggy banks. You pay money into them throughout your working life. Then, once you reach a certain age – normally 55 (rising to 57 in the future) – you can start withdrawing your money.

Oh, except they’re way better than piggy banks as hopefully, by the time you retire, you’ll have much more money to withdraw from your pension than what you actually paid in, in the first place. Pretty great, huh? This is because of a couple of things.

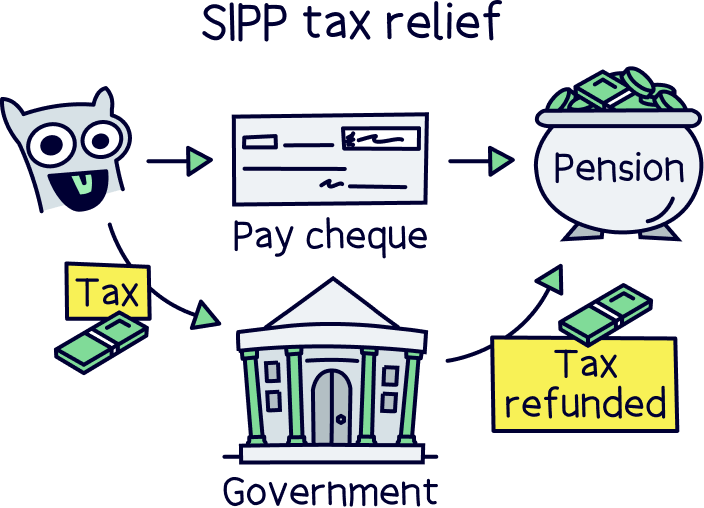

Firstly, you won’t have to pay any tax on the money you add into your pension (as it's usually from your salary), this is known as tax relief. Instead, the tax you’ve paid on that money (through earnings) will get refunded straight into your pension pot by the government, to help boost your savings. Nice!

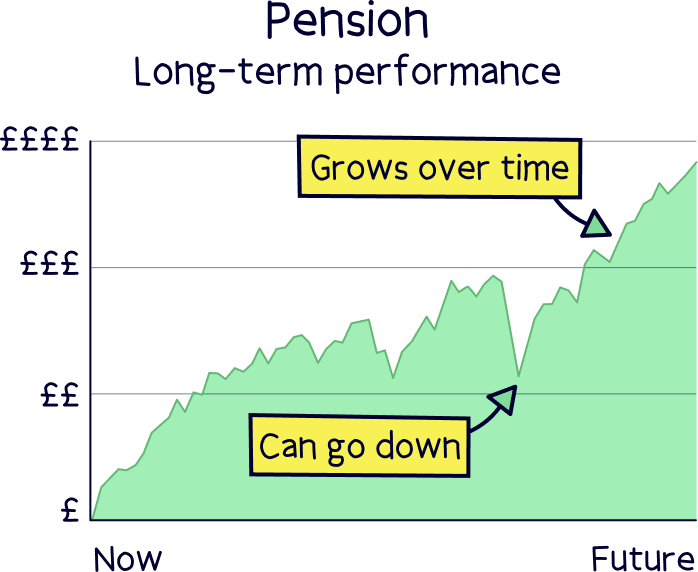

And secondly, if you use experts to invest and manage your savings sensibly over time they will grow in value a lot more – that’s when they’re used to buy things like stocks and shares (which essentially means you own small parts (share) of companies). As your investments increase in value, your savings will too!

With most personal pensions, your money will grow without you having to lift a finger, as your pension provider (the company looking after your pension) will invest your savings for you. However, with a SIPP, you’ll need to spend time investing your savings yourself (there’s a reason it’s called a self-invested personal pension!). That’s right, you get to choose your investments and you’re responsible for managing your investment strategy.

If you’re a bit of a pro when it comes to investing and you want more control over where your money goes, a SIPP could be right up your street. But if you’re a beginner and you’d rather have an expert’s help, a traditional SIPP probably won’t be for you.

Interested in getting a SIPP? Here's our recommended best and cheapest SIPP providers.

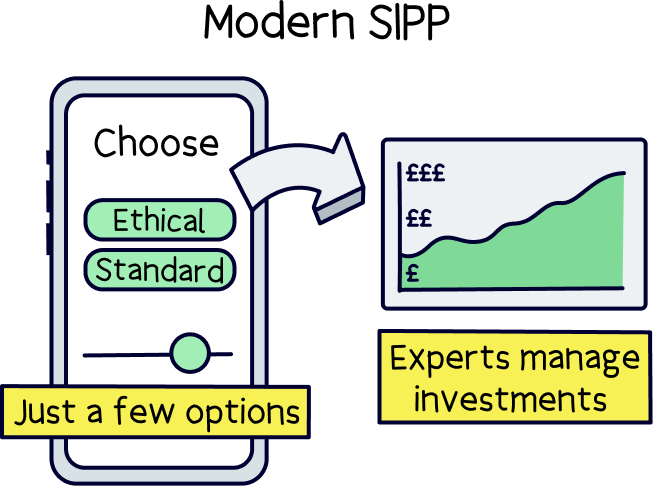

Having said that, there are some newer, partially-managed modern SIPPs that act as a bit of a middleground. With these, you still get to make the investment decisions, but you choose from just a few options that have been carefully picked out by your pension provider – and they manage your investments for you. So, it’s a lot less complicated and more beginner-friendly!

Check out our selection of the best private pension providers UK to get started.

A workplace pension is a pension that your employer sets up for you. If you’re employed, the chances are you already have one of these. Usually, your employer will legally have to provide you with one.

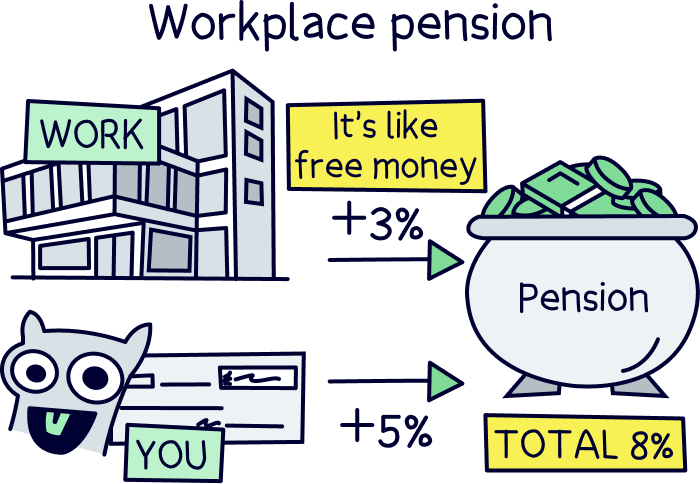

With a workplace pension, you need to pay at least 5% of your earnings into your pension each month. But the great news is that your employer will also have to contribute to it – at least 3%, straight from their own pocket. Yep, it’s basically free money!

Just like a SIPP, most workplace pensions work like piggy banks – you and your employer will contribute to your pension throughout your working life, and then once you reach the age of 55, you’ll be able to start withdrawing your money.

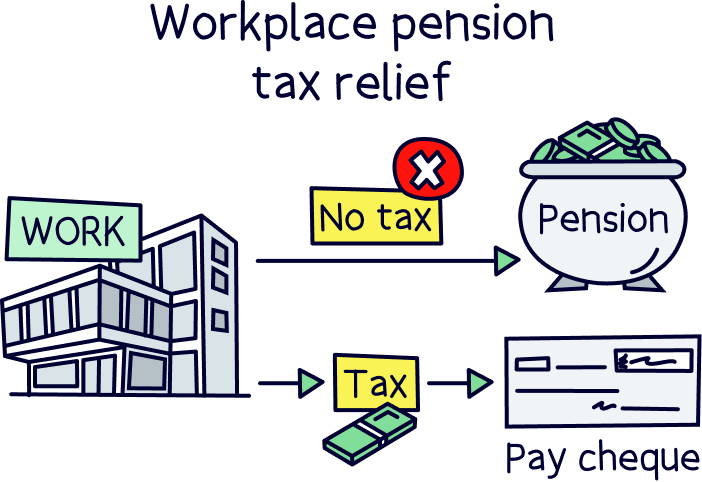

You’ll still benefit from that lovely tax relief we told you about earlier (remember how we said that you won’t have to pay tax on the earnings that you pay into your SIPP?). The only difference is that instead of your tax being refunded into your pension pot, you’ll simply pay less tax in the first place – as your tax will be calculated and deducted from your payslip each month.

Oh, and your savings will still get invested – you’ll just get to rely on your pension provider to do it for you, instead of having to choose your investments yourself. Simple!

Nuts About Money tip: Find out how much money you could save with our pension tax relief calculator.

SIPPs and workplace pensions are both great in different ways. So, it’s REALLY hard to give a straight answer on this. But we’ll do our best to break it all down for you.

First things first, SIPPs tend to have cheaper fees than workplace pensions – and most personal pensions too! That’s because with traditional SIPPs (ones where you buy and sell investments yourself), you won’t be relying on your pension provider to spend time trying to grow your savings for you. Instead, you’ll be putting the hard work in yourself.

Another great thing about SIPPs (and other personal pensions) is that you can choose your own pension provider – unlike workplace pensions, where your employer will pick out a pension provider for you.

Being able to choose your own pension provider is great because it means you can pick one with lovely low fees and great investment records. If you’re after one of those partially-managed SIPPs we told you about, you can also make sure your pension provider has a great track record for growing people’s pensions, meaning your savings will hopefully grow quicker than they would in a workplace pension. Woohoo!

So far, SIPPs are sounding like the winners, right?

Well, they are pretty great. BUT workplace pensions have one majorly awesome thing going for them: your employer has to contribute! Remember how we said they’ll contribute at least 3% of your salary to your pension pot, from their own pocket each month? That could be a lot of free money!

Because of that, even though SIPPs trump workplace pensions in many ways, we’d always recommend getting a workplace pension if you’re offered one. After all, you’d be mad to turn down free money! Which brings us onto…

Find the best pension for you – you could be £1,000s better off.

Let’s be really clear here: if your employer offers you a workplace pension, you should definitely take it. After all, a workplace pension means you can unlock free money from your employer!

However, here’s the important bit… you don’t actually have to choose between the two! Instead, we should really be asking ‘should I get a SIPP as well as a workplace pension?’

And the answer is yes! If you have extra cash that you can set aside for retirement, starting a SIPP (or another kind of personal pension) on top of your workplace pension is usually much more sensible than increasing your workplace pension contributions.

Nuts About Money tip: you can estimate your total pension pot at retirement and your yearly retirement income with our pension calculator.

You know how we said that with a personal pension like a SIPP, you can choose your pension provider yourself? Well, that means you can save money by choosing a pension provider with lovely low fees.

If you opt for a SIPP, you’ll also be able to choose a pension provider that can offer you a wide range of investment options, to suit your preferences. Or, if you go for a managed SIPP, you can make sure your pension provider has a good track record for growing pension savings quickly (check out PensionBee¹, and Beach¹).

There’s just one exception.

A few very lovely employers will offer to match your pension contributions – in other words, if you pay more than the minimum 5% of your salary into your pension, they’ll follow suit and will also pay more into your pension. Get in!

If you’re one of these lucky people, it’ll probably be more sensible for you to put any extra cash into your workplace pension, rather than into a SIPP, as it’ll mean unlocking more free money from your employer. However, most employers will only increase their contributions by so much. So, once you’ve maxed out what you can get from them, then it’s time to start thinking about starting a personal pension, like a SIPP. Makes sense, right?!

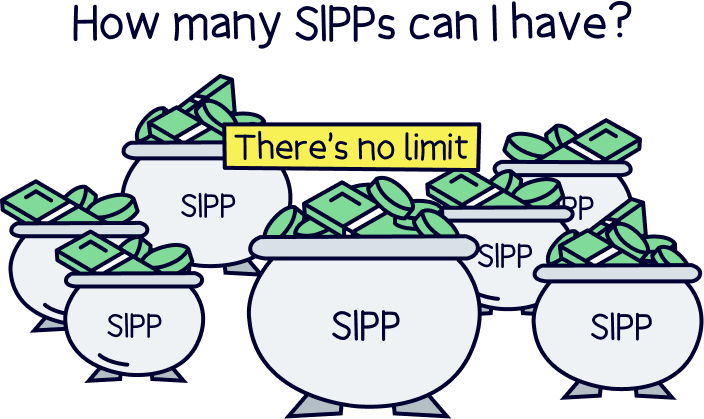

Yes! There’s nothing to stop you from having a SIPP and a workplace pension at the same time. In fact, there’s nothing to stop you from having as many pensions as you want! We mean it: you could have 50 pensions if you wanted (although we definitely wouldn’t recommend that – they’d be way too hard to keep track of!).

However, even though there aren’t any limits to how many pensions you can have, there are a few rules about how much you can pay into them to keep in mind.

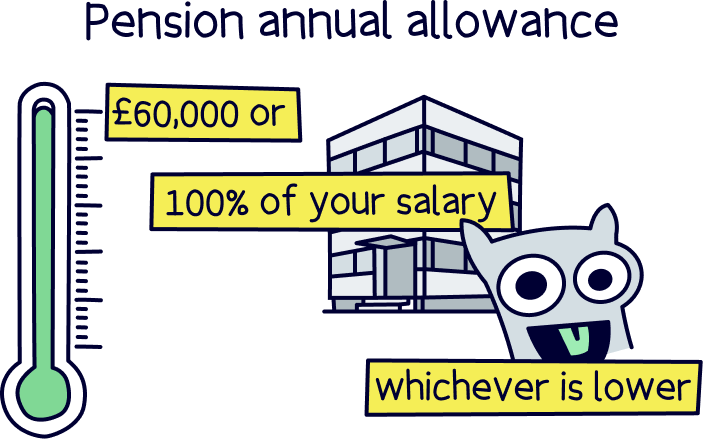

The annual allowance is a limit to how much you can pay into your pensions as a whole, while still getting all the lovely tax benefits that pensions normally come with.

At the moment, the annual allowance is £60,000 or 100% of your salary – whichever is lower.

That means if you earn £30,000 per year, your annual allowance will be £30,000 (it’s the same as your salary because you’re earning under £60,000). But if you earn £100,000 per year, your annual allowance will be £60,000 (because you’re earning more than £60,000). Make sense?!

The only exception is if you’re over the age of 55 and you’re taking an income from your pension already. In this case, your annual allowance will be quite a bit lower – normally £10,000.

So, what happens if you go over your annual allowance? Well, you won’t be able to claim that wonderful thing called tax relief on the extra money – which might mean you’re better off doing something else with it instead (like stashing it away in another type of savings account – for instance, a Stocks & Shares ISA or a Lifetime ISA. Check out our best investment platforms UK to learn more).

Even though you can have as many workplace pensions as you want, you can only pay into workplace pensions that you currently work at.

Let’s rewind for a second.

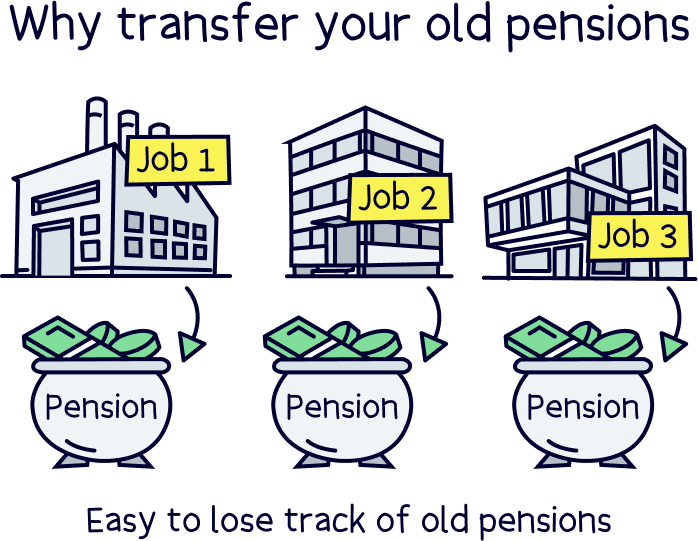

It’s easy to end up with lots of workplace pensions. In fact, if you’ve had a few employers in your working life, the chances are you’ve racked up a few of them already. That’s because each time you change employers, your new employer will usually set you up a new workplace pension!

The average worker in the UK changes jobs 5 times (according to AAT) – so, you’re likely to have had around 5 workplace pensions by the time you retire. This is totally fine. Like we said, you can have lots of workplace pensions – and the money in those pensions will still be ready and waiting for you when you come to retire.

However, you can only have active workplace pensions with companies you currently for – ones your current employer(s) have set up for you. The rest have to be dormant, meaning that you and your employer are no longer paying into them.

Unfortunately, having lots of dormant pensions lying around can make them easy to lose. It’s true! The Association of British Insurers found that there are around 3.3 million lost pension pots in the UK, worth around £31.1 billion altogether!

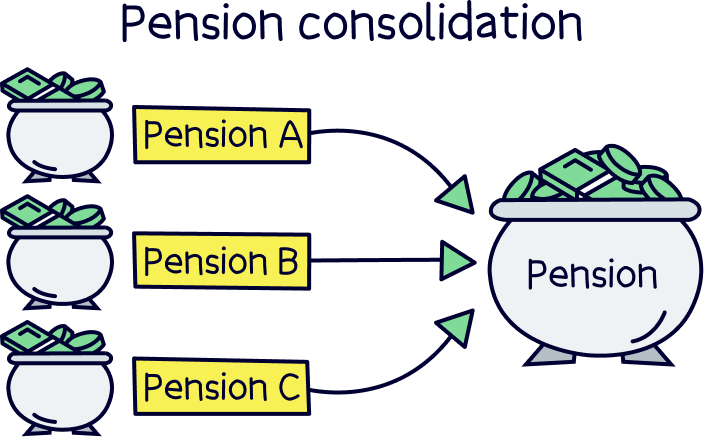

That’s why it’s often more sensible to consolidate your pensions, which is when you start a new personal pension (like a SIPP) and then transfer your old pensions to your new one. By gathering all your old workplace pensions in one place, you’ll make them easier to keep track of and you’ll know exactly where your money is when you come to retire. Phew!

Luckily, transferring a pension to a SIPP is quick and easy – check out our dedicated guide to learn how.

As you can see, there’s no need to choose between a SIPP and a workplace pension. Instead, you can have both!

If your employer offers you a workplace pension, we’d always recommend accepting it – that way, you’ll be able to unlock free money from your employer! However, if you have extra savings left over after your workplace pension contributions, starting a personal pension – like a SIPP – is a great shout. By starting a SIPP alongside your personal pension, you might be able to access lower fees and a greater range of investment options, meaning you might be able to grow your money faster.

Just remember that, traditionally, SIPPs require you to make your own investment decisions, so they’re often not great for beginners. If you’re keen to have your money looked after by experts, another kind of personal pension might be better.

No matter what you choose, boosting your savings for retirement is quick and simple – just browse our selection of the best personal pensions to get started. Then, enjoy watching your savings grow ready to live the high life in your golden years.

Finally, if you want to learn more, visit our pensions home page.

Find the best pension for you – you could be £1,000s better off.

Find the best pension for you – you could be £1,000s better off.

Find the best pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best pension for you – you could be £1,000s better off.