Article contents

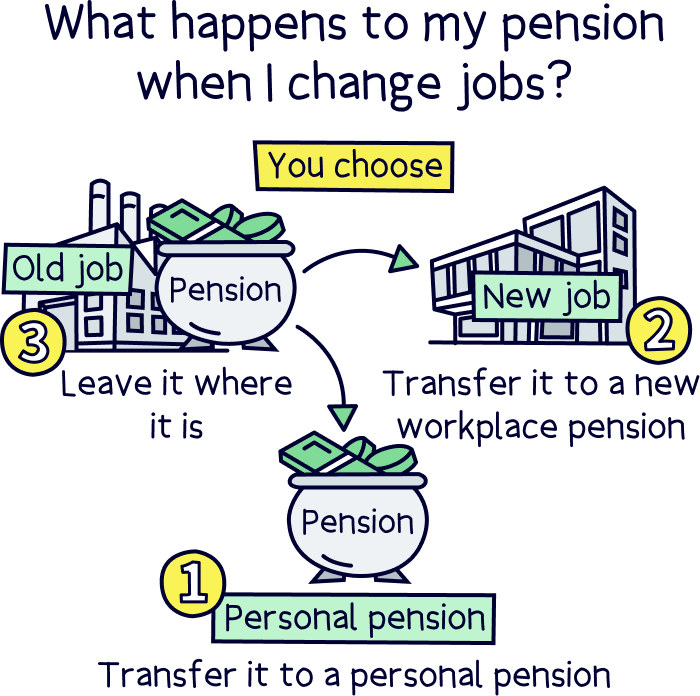

Your pension is your money. You can either move it to a personal pension (recommended), move it to where your new pension is (with your new job) or just leave it where it is.

New job? Congrats! But what happens to your old pension you worked so hard for? The good news, it's all yours and you can do what you want with it (almost).

Let’s run through what happens to your pension when you change jobs. Don’t worry, there’s nothing to worry about.

In fact, you now get to decide what happens to your pension, rather than your old employer. So you could save more money, and have your pension grow more too.

Let’s first start by saying you can’t actually cash in your pension (get the money from your pension). Which is a good thing. Otherwise we’d all be pretty tempted to move jobs and spend the money!

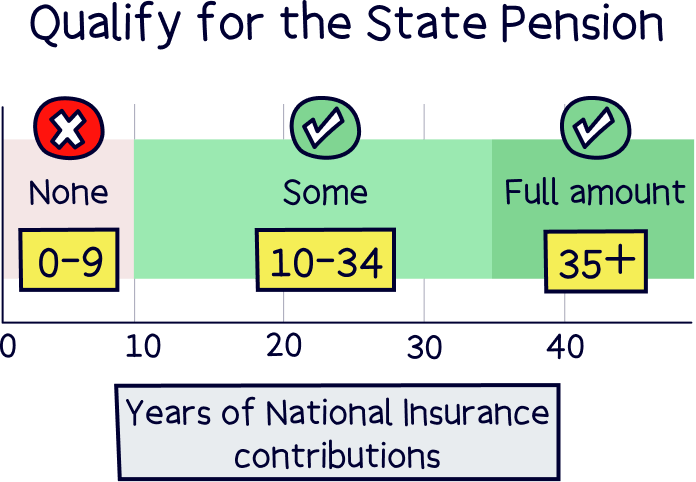

But we definitely don’t want to do that. The pension is there for us to have a comfortable life in retirement. Otherwise you will be on a lot less than minimum wage if you rely solely on the government pension (called the State Pension). Which is what you get if you pay enough National insurance over the course of your life (number of years).

If you’re concerned your pension is quite small, we have a guide on increasing pension contributions in a manageable way.

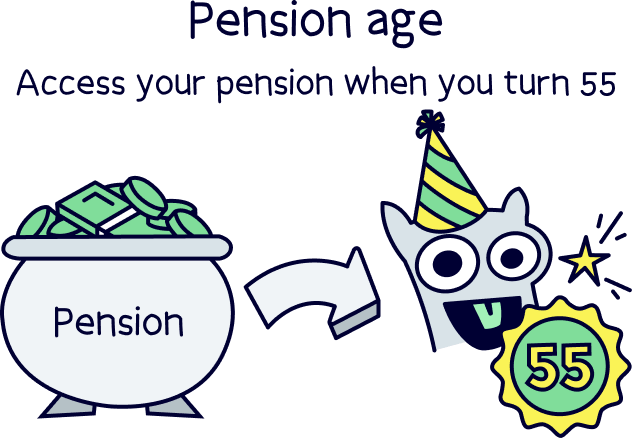

Note: you can’t take money from it until you’re at least 55 (57 from 2028), and ideally you shouldn’t touch it until you actually retire. Let it grow even more! (Well, you can, but the fees to do so are so huge that it’s not worth it).

Learn more about this with: can I cash in a pension from an old employer?

You’ll have control over your money, and potentially lower fees and more money over time.

So what actually happens then? Well not much! Your pension just sits there, hopefully earning money.

Just in case you weren't too sure, your employer doesn’t manage your pension or the money inside it, they use a pension provider to look after your pension. And it’s their job to grow your money safely over time so you have a nice big pot at retirement.

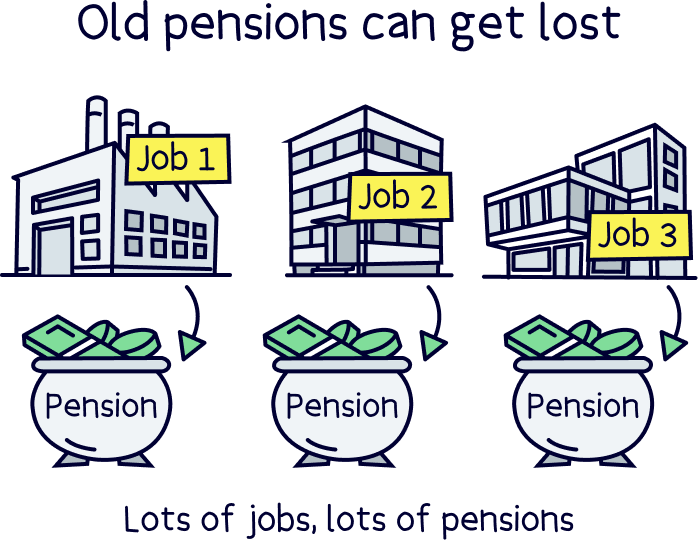

When you leave your job, your pension is simply just left alone by your employer. They will stop adding to it, and forget all about it. They probably won’t even tell you what to do, how to access it, and sometimes they won't even tell you who the pension provider is, unless you ask.

And then there’s the pension provider. They have your money, and are charging you fees to manage it (taken from your pension), so they hope that you just forget about it, and keep you in the dark. Unfortunately a lot of people do forget about their pension(s)!

With a workplace pension (setup by your employer that you pay into through your salary), they’re often not the best pension providers. They’re normally with large companies who have high fees and historically don’t grow your money very much (for instance Aviva).

So the good news is that when you change jobs, you can do something about it!

Let’s run through your options.

As it's your pension and not your old employers, you can do something about where your pension is, and potentially avoid the high fees you might be paying.

You can:

Let’s run through each option.

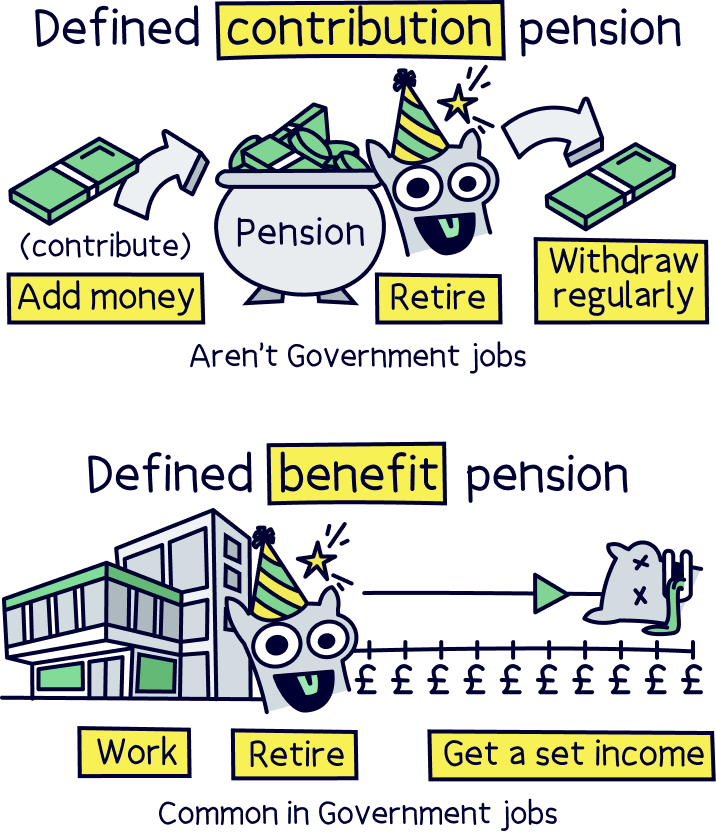

By the way, we’re talking about defined contribution pensions, rather than defined benefit pensions. Defined contribution pensions are the most common type of workplace pensions, and you'll most likely have one of these.

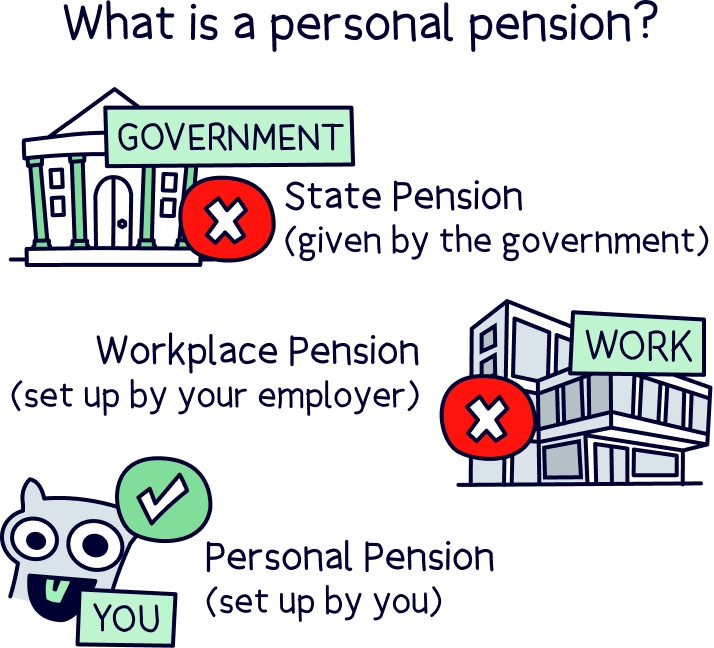

It’s where money is taken from your salary each month, and added to a pension scheme in your name, that you ultimately control (called a private pension). You decide how much to contribute, how the money is invested and when to take the money out (after 55).

A defined benefit pension is where you get a set monthly income when you retire based on things like how long you’ve worked and what your salary was. These are more common in large public organisations such as the NHS.

You may have a stakeholder pension as your workplace pension scheme, but they’re pretty rare these days. These are just the same as any other workplace pension (private pension). You can transfer them just the same.

This is by far your best option, that’s why we’ve put it first!

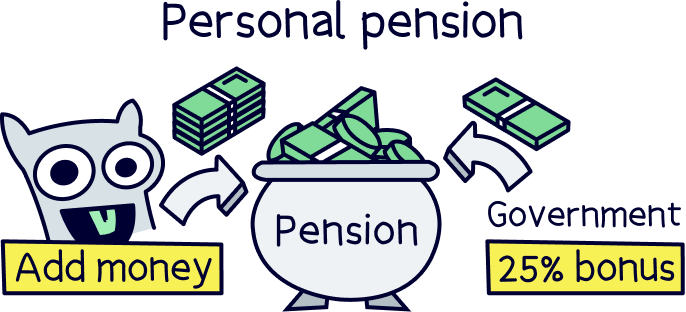

A personal pension is a pension that you set up, is in your name and has nothing to do with any of your employers. It’s all yours.

You decide who you want to use as your pension provider. And you can even add more money to it yourself too if you’re feeling flush, or want to save more regularly, which is always a good idea.

If you do add money, you’ll get a 25% bonus from the government on what you put in, every time. Pretty great right? Learn more about that with our guide: What is a personal pension?

A personal pension is super easy to set up too. We’ll run through everything below.

By the way, a personal pension is a type of private pension. That just means, it’s in your name, rather than the State Pension, which is what most people get from the government when they retire. A workplace pension is also a private pension. Confusing right?

The benefits of having control of your pension is that you can pick a pension provider that has low fees (so you save money), and can choose one that could grow your money a bit more (for instance, one that has a great track record of growing your money).

With a workplace pension, they’re normally pretty expensive, and have pretty poor records for growing your money.

Better still, you can even choose one that aligns with your values, such as only investing your money in an ethical and sustainable way (so no investments in fossil fuel companies for instance). Your pension money can literally help save the planet! Pretty cool right?

Plus, if you decide you want to change your personal pension provider in the future, it’s easy to do.

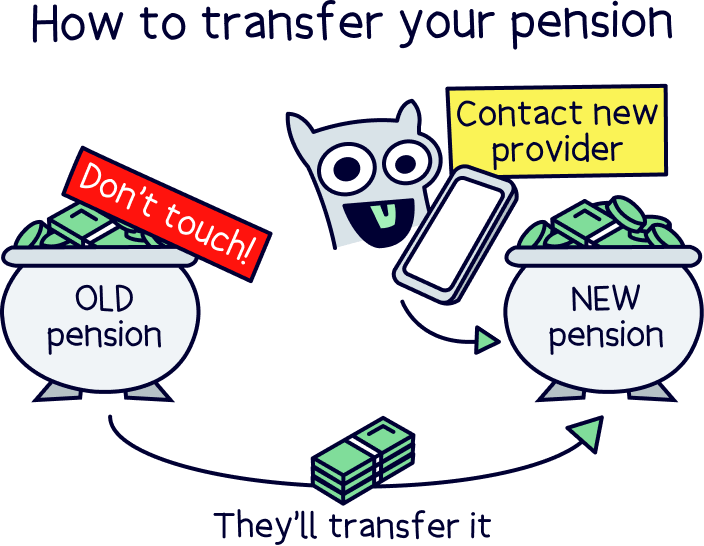

What about your current workplace pension then? Well, now you’ve left your job, you can transfer all of your money into your new personal pension, just like that. You don't have to do much at all.

By law, your workplace pension must transfer your money as soon as possible to your new provider.

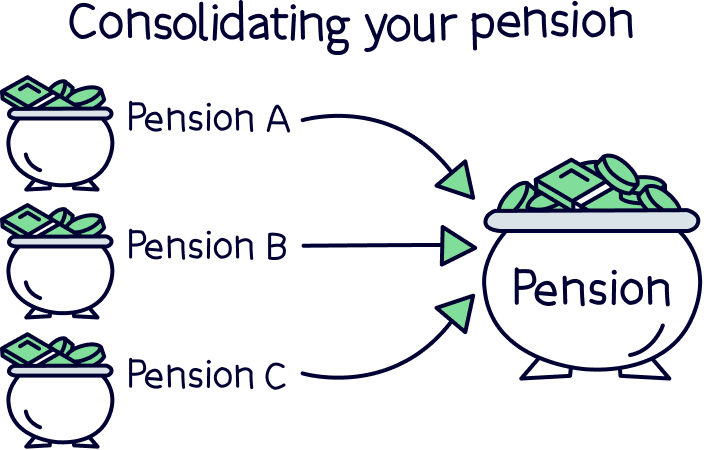

To us, it’s a no-brainer. You get control of your pension, and you can even move all of your old pensions into one pension (called consolidating), to keep them all together.

Firstly, this means you won’t lose them in future. According to The Association of British Insurers, there’s 3.3 million lost pensions in the UK, that totals £31.1 billion!

And second, by consolidating your pensions, you can potentially benefit from even lower fees (the more cash in a pension, the lower the fees).

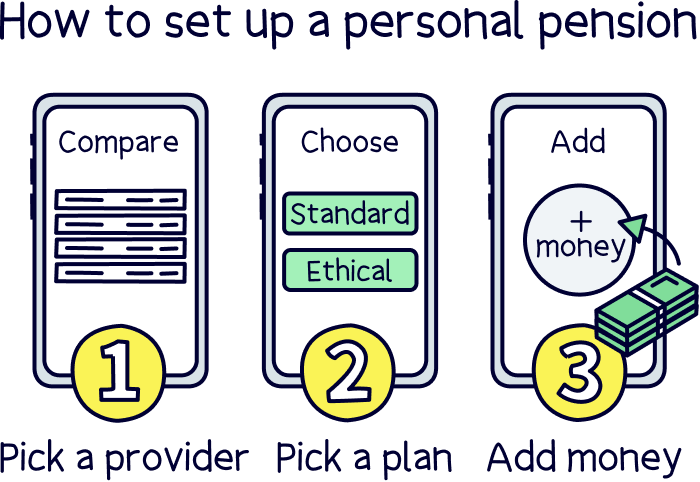

Setting up a personal pension is super easy! First, decide on which provider you want to use.

If you’re not sure where to look, we’ve put together the best private pensions. All you need to do is pick one you like, choose a plan, and add money. As easy as that.

Not got much time? Our favourite is PensionBee¹ – they have a great, easy to use mobile app to track your pension whenever you want to, have low fees, plus the customer service is great. Here’s our PensionBee review to learn more.

If you’ve started a new job, you’ll probably have a new workplace pension set up for you by your new employer.

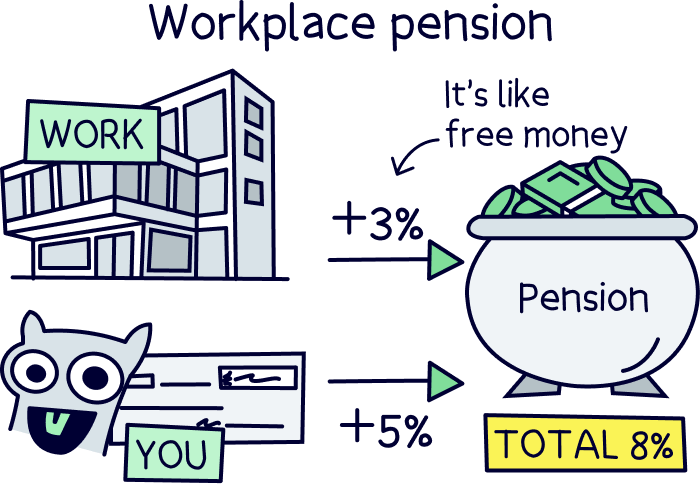

A workplace pension scheme is where you have to add a certain amount from your salary (normally 5%), and your employer has to contribute too (3% as a minimum contribution). So you’re getting a bit of free cash from your employer! (this scheme is called auto-enrolment.)

Note: we’re talking about ‘defined contribution pensions’, which simply means you and your employer are contributing to your pension pot. Another type is a ‘defined benefit pension’, which is where your employer will pay you an income when you retire (not very common).

It’s always good to have a workplace pension because of the free cash, but it’s only when you pay from your salary, not when you transfer a pension across.

And so, you can transfer your old workplace pension to your new workplace pension if you want to. This means you don’t have to worry about forgetting about your old pension anymore.

However, you might find your new workplace pension is expensive, and doesn’t have a great record for growing your money. And you often won’t be able to decide if you want to save your money with an ethical or sustainable fund (a fund is a type of investment). That’s why we recommend a personal pension that you have full control over.

It’s a big decision, as once you do this, you can’t move it again until you leave your job.

To move your old workplace pension to your new workplace pension, all you need to do is speak to your new pension provider, and they’ll be able to sort this for you. (You will need to ask your new employer who the new pension provider is.)

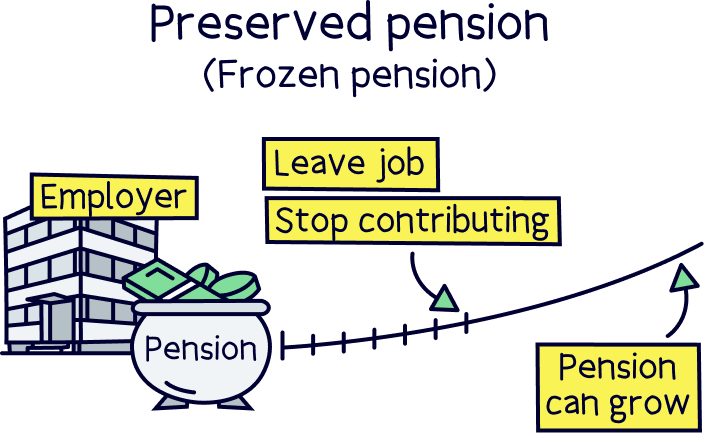

Finally, you could just leave it where it is! This is called a preserved pension or a frozen pension. It’s the lazy option, you will probably be paying high fees but they will try and grow your money (fingers crossed!).

If you opt for this option, make a note of who the provider is and ideally keep all the paperwork safe where you and your loved ones can find it.

When you retire, you’ll need to request the money! Pension providers aren’t the most forthcoming when it comes to letting you know you have a pension with them (they want to keep getting the fees).

Note: you can’t add any more money into it from your new job, they’ll set up a new pension for you. You might be able to add money to it yourself, depending on who the provider is.

If you’re now self-employed, or become self-employed in the future. A personal pension is the best option to save for retirement – as you need to manage your own pension, and choose a pension scheme. (As you won’t have an employer to do it for you!).

It’s super easy to set up one and manage (well, you just let the experts handle everything for you). You can then transfer in your pension from your old job. As easy as that.

Then set up regular payments if you can, and collect that nice government bonus (25%) everytime you make a payment. Pretty great right?

Here’s where to find the best personal pensions.

Changing jobs gives you a great opportunity to move your pension over to another pension provider, where you could benefit a lot more.

You’re now able to have full control over your money, you can move it from your current pension provider (the one your employer set up), to one that you do want to save with.

You could move it to a personal pension, one that you choose, with lower fees and better records for growing your money over time. Plus, if you want to save ethically and sustainably (for instance not have your money invested in fossil fuels), you can do this too.

Or, you can move it to your new workplace pension, one that your new employer will set up, and keep your money together. However, you’ll often have the same issues, where you don’t have any control, the fees can be higher and often not great growth over time. Once you do this, you can’t transfer it again until you move jobs.

And finally, you can leave your pension where it is. It’s all safe, and should grow over time ready for your retirement. You won’t have any control over it though, and you may be paying much higher fees than you need to be.

It’s also important to keep a note of who the provider is, so you don’t forget about it when the time comes to retire. Your family might need to track them down if you pass away too.

But the best option is to open a personal pension and transfer your workplace pension into that. Well, why not transfer all your old workplace pensions over.

That way it will be easier to remember where your pension is, just one place. You’ll have full control over which pension provider you want to save with, and potentially benefit from lower fees and better growth over time (that’s a big deal!).

It’s easy to do and set up, you actually don’t need to do much, your new personal pension provider will handle everything for you.

Not sure where to look? Check out the best private pension providers to find the best one for you, or check our PensionBee¹, one of our favourites.

You’ll have control over your money, and potentially lower fees and more money over time.

You’ll have control over your money, and potentially lower fees and more money over time.

You’ll have control over your money, and potentially lower fees and more money over time.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

You’ll have control over your money, and potentially lower fees and more money over time.