Article contents

When you die, your ISA can be passed onto your loved ones. You just need to state who you want it to go to in your will. If it’s a stocks and shares ISA, your loved ones can choose whether to sell the investments for cash or keep the investments.

ISAs can be a great, tax-efficient way to save. But what happens to them when you die?

We know, we know, it’s not the cheeriest of topics, but it’s an important one. And we think you’ll be pretty pleased with the answer. Your loved ones will be able to reap all the benefits of your ISA once you’ve gone, even though you won’t be around to enjoy it yourself! Here’s the lowdown.

ISA stands for Individual Savings Account. It’s basically a savings account that makes it really easy to grow your money without having to pay tax on it. Kerching!

There are 2 main types of ISAs: Cash ISAs and Stocks & Shares ISAs.

A Cash ISA is a savings account where you don’t have to pay tax on the interest you earn.

If that sounds like gobbledygook to you, don’t worry. Interest is a kind of charge that you either pay when you borrow money, or receive when you lend money. It’ll be a percentage of what you either borrow or lend.

With a Cash ISA, you can earn interest on the money you put in there. And, better still, you won’t have to pay tax on any of the interest you receive!

You can get fixed-rate Cash ISAs, which last for a set period of time and guarantee you a certain amount of interest. However, these will charge you a hefty fee if you need to take your money out during that time. Or, you can get instant-access ones, where you can put in and take out money whenever you want – but the interest rates will be a bit lower to make up for it!

A Stocks & Shares ISA is also known as an investment ISA. It’s basically a tax-efficient investment account, which means it’s much better at making money for you than a Cash ISA.

Any money you put into a Stocks & Shares ISA will get invested in stocks and shares for you (those are basically ownership stakes in companies). The idea is that these companies should grow and become more valuable – and when they do, you’ll make money. Woohoo!

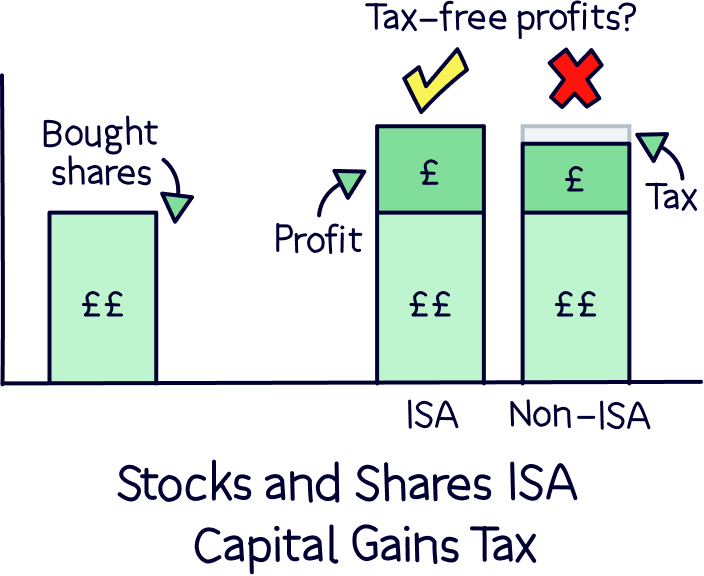

As if that wasn’t enough, the really good thing about investing through a Stocks & Shares ISA is that you won’t have to pay any tax on the returns you make. That includes no Capital Gains Tax (a tax that’s charged when you sell something that’s increased in value, including stocks), and no dividend tax (a tax on payments you might get from certain companies who give cash to people who have shares). Not bad, eh?

Of course, it’s not guaranteed that you’ll make money. But it’s very likely that you will. Ultimately, it’s a great way of investing tax-free so that you can save for your future (and let’s be honest, saving is something we should all be doing more of!).

Learn more about Cash ISAs vs Stocks & Shares ISAs.

We've put together the best investment platforms to help you find the best ISA for you.

The 2 we’ve mentioned above are the main kinds of ISAs. However, there are a few more niche types that you may also come across. These are:

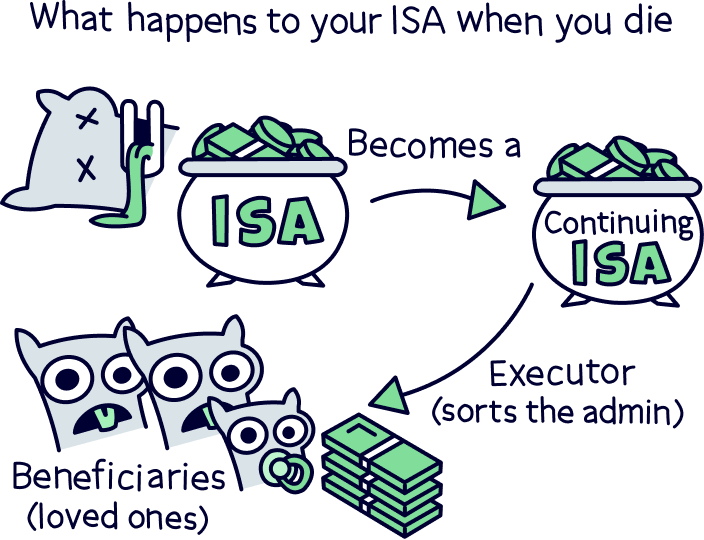

When you die, your ISA will become something called a ‘continuing ISA’ for a limited period of time. During this time, your ISA can continue to grow and keep its tax benefits, although now that you’ve gone, no more money can be added.

Your ISA will be kept open as a ‘continuing ISA’ until either:

If neither of these things has happened after 3 years and 1 day, your ISA provider will close your ISA.

However, what you’re probably wondering is… well… who gets to benefit from your ISA?! Which brings us onto...

Your loved ones can inherit your ISA once you’ve passed away. In fact, you can leave your ISA to whoever you want in your will (hence why it’s super important to get your will sorted out sooner rather than later!).

If you’re leaving your ISA to your spouse or partner, they’ll probably be able to inherit your ISA savings through something called an ‘inherited ISA allowance,’ also known as an ‘additional permitted subscription’ (APS).

If you’re thinking ‘Huh? What the hell’s that?!’ then don’t worry. Let’s rewind a little.

When you get an ISA, you’ll be limited to how much you can put into it each year, known as your ‘allowance.’ This is the government’s way of controlling how much tax-free growth your money can make. Exactly how much the allowance is can change, but at the moment it’s £20,000 per year.

However, the ‘inherited ISA allowance’ means that your spouse or partner can add the value of your ISA to their normal allowance, in order to be able to inherit it – only your spouse or partner though, and not anyone else.

Imagine your ISA is worth £40,000 when you pass away. Assuming you’ve left your ISA to your spouse, they’ll get the normal £20,000 allowance for the year just like everyone else, PLUS an extra £40,000 allowance so that they can inherit your ISA. Altogether, their allowance for the year would be £60,000.

Now, we bet we know what you’re thinking. What happens if you don’t want to leave your ISA to your spouse or partner?

Well, that’s totally fine, you can leave it to whoever you want. But they won’t get the additional allowance. Instead, the value they inherit will count towards their standard yearly £20,000 allowance.

Meanwhile, your partner can still claim the extra allowance even if they don’t get your ISA. But this won’t be too useful for them unless they have more than £20,000 of their own cash to add to their ISA in the first place!

Your loved ones can choose what they want to do with the value of your ISA. However, exactly how that works will depend on what kind of ISA you have.

If you have a Cash ISA, they can choose between:

If you have a Stocks & Shares ISA, they can choose between:

Normally, you can only open 1 Cash ISA and 1 Stocks & Shares ISA each year. However, if your loved one is opening up a new ISA purely because they’re transferring inherited savings, it’s okay to open up a second one in the same year.

That said, you can only use your inherited ISA allowance once. So, your loved one won’t be able to keep moving the inherited money around without it counting towards their yearly allowance of £20,000.

Before your ISA is closed (while it’s still a ‘continuing ISA’), it can continue to grow and keep its tax benefits. In other words, even though nobody can add more money to it, it can still increase in value without being subject to income tax or Capital Gains Tax.

However, it will be subject to inheritance tax – unless you leave it to your spouse or partner.

Inheritance tax is a kind of tax that gets charged on the property and belongings of someone who dies. If everything you own (known as your ‘estate’) adds up to more than £325,000, a tax of 40% will be charged on anything over that £325,000 threshold.

Your ISA will form part of your estate, which means its value will be added to everything else you own. And, if everything you own (including the value of your ISA) adds up to more than £325,000, the government will charge income tax on it.

BUT there’s one big exception. Anything you leave to your spouse or civil partner won’t be subject to inheritance tax. That means if you leave your ISA to your partner, they can inherit it for free.

It’s really important to save for the future, and an ISA can be a great way to do that – especially a Stocks & Shares ISA, which will typically get you some great returns if you leave your money in there for long enough and all without you having to pay tax on it! Even better, your hard efforts won’t go to waste if you pop your clogs, as your loved ones will be able to inherit your ISA and benefit from all the savings you’ve managed to squirrel away and grow during your lifetime.

If you don’t yet have an ISA, you can fin the best one for you with our comparison table of the best investment platforms UK.

We've put together the best investment platforms to help you find the best ISA for you.

We've put together the best investment platforms to help you find the best ISA for you.

We've put together the best investment platforms to help you find the best ISA for you.

This article was written by the team at Nuts About Money, and fact-checked by 2 independent reviewers. You’re in safe hands.

We've put together the best investment platforms to help you find the best ISA for you.