Article contents

Some pensions, like personal or workplace pensions, are passed to your spouse or partner when you die, so they can continue with their current way of life, at least financially.

Get £50 added to your pension.

Visit PensionBee¹Capital at risk.

Pensions are boring and talking about them isn’t fun, but they're important, especially talking about what happens to your pension when you die.

You can’t take your money with you when you die, but wouldn’t it be good to know that the money you worked so hard for is going to your loved ones? Well here’s some news for you – there are ways to make sure the cash you’ve worked hard to save through your pension gets passed onto your loved ones when you die.

In this guide we’ll explore the main pension types and what you should think about to make sure your family is looked after financially when you pass away.

Find the best personal pension for you – you could be £1,000s better off.

Picture the scene: you’ve worked really hard throughout your adult life; at some point you started paying into a private pension, perhaps one that your employer pays into straight from your payslip or one you set up yourself; you know that when you retire, you won’t need to worry about paying your living costs and can enjoy your well-earned retirement.

Touch wood nothing bad will happen to you, but since this guide is all about what happens to your pension when you die, at some point we have to consider what’ll happen then and how you can financially plan for the worst.

What’ll happen to all that money you paid into your private pension? Let’s find out.

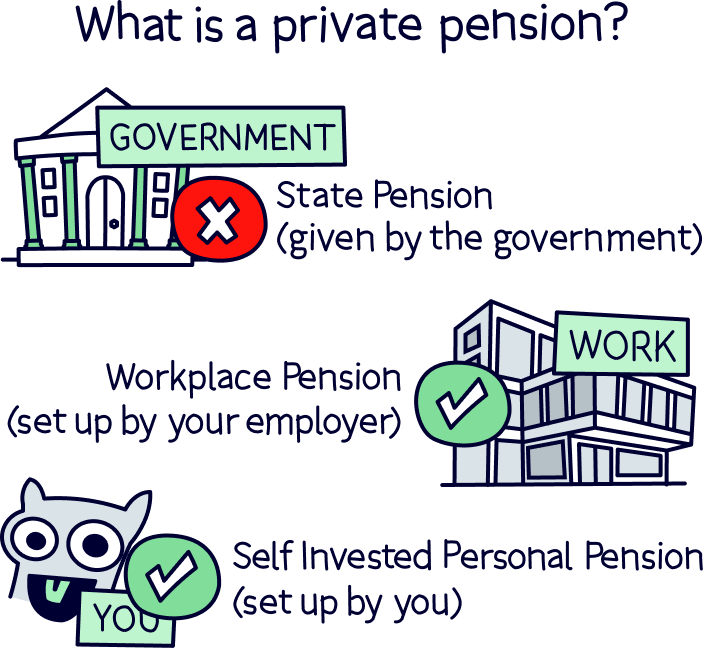

Private pensions are any pensions that aren’t the State Pension (the State Pension is the one paid to all people by the government once they reach retirement age). This includes things like workplace pensions (those are the ones your employer sets up and pays into on your behalf) and personal pensions, including SIPPs (that stands for 'self invested personal pensions' – this is a personal pension that you set up and manage yourself).

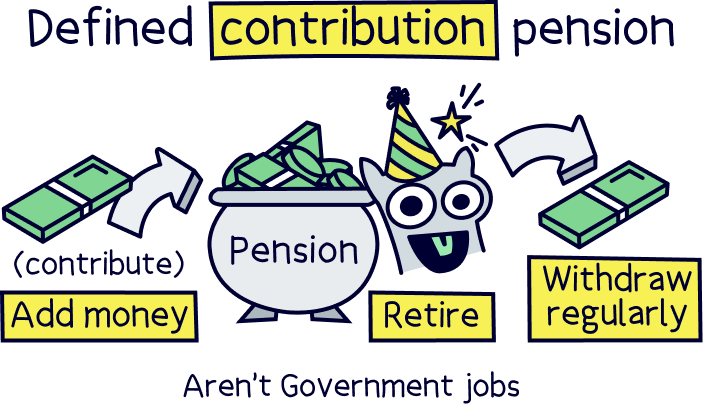

There are two main types of private pension: defined benefit and defined contribution pensions.

This is the most common type of pension. For this type, the value of the pension pot is made up of the amount you and your employer pay in (the ‘contribution’) – it ‘defines’ how much you’ll receive when you retire. The value of the pension pot can also be affected by where the pension is invested, such as investments in large, successful companies that increase in value over time.

And what’ll happen to your defined contribution pension after you die? This will depend on how old you are when you die and whether you’ve already started receiving payments from that pension pot. Here’s how it works:

Your loved ones can receive your defined contribution pension tax-free if you die before you turn 75 and haven’t started receiving income from this pension. The money can be given to your loved ones as a lump sum, invested in things like shares or to purchase an annuity (a regular income).

What happens then will be decided by how you originally chose to access your cash:

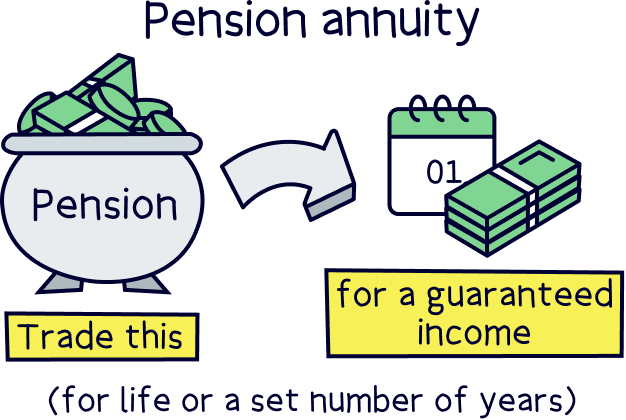

And what happens if you have an annuity? Normally, if you already start receiving payments from your annuity before you die, your family can’t inherit that cash, although some annuities do allow this. Check with your specific annuity plan to find out where you and your family stand.

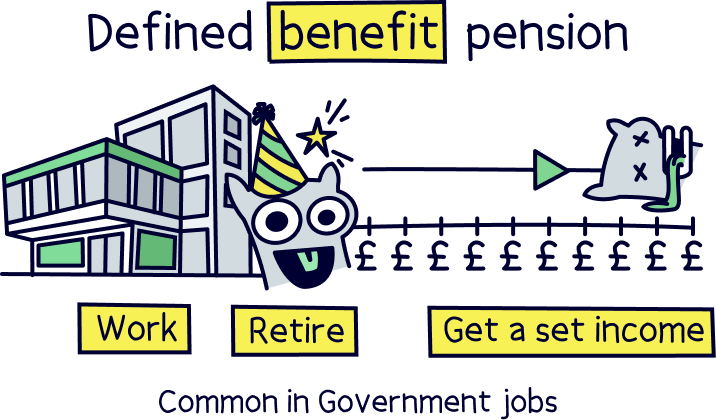

You might have heard of a defined benefit pension called a final salary pension. This is when the money you receive when you retire is based on the amount you earned at your job, how long you worked there and your age. You’ll be guaranteed a certain amount, and that’s what you’ll receive.

The value of your defined benefit pension is based on your salary and how many years you worked for your employer(s). How much of your defined benefit pension is passed on when you die depends on whether you retire before you die.

If you die before you reach retirement age, your defined benefit pension will pay a lump sum to your family. This lump sum tends to be around 2-4 times the salary you were earning when you died – different employers use different pensions, so your amount will depend on that. This payment will be tax-free for your family if you die before you reach 75.

And if you’ve already retired when you die, your loved ones can inherit that pension.

When you die your family may need to pay inheritance tax if the value of everything you own is more than £325,000. But you’ll be pleased to hear that they won’t need to pay inheritance tax on money they receive through your pension.

They might need to pay income tax though, but this depends on how old you are when you die:

Luckily there’s not much more to say about workplace pensions (phew!). This is because workplace pensions are essentially another type of private pension. These are pensions that your employer sets up, then you pay into it and your employer tops it up with additional cash – they have to provide you with a pension scheme if:

Nowadays most workplace pensions are defined contribution and follow the same rules described above.

The standard State Pension – that’s the weekly income, paid by the government and received by all pension-age people who worked in the UK and made National Insurance payments for at least 10 years – can’t generally be passed onto your loved ones when you’re no longer around.

However there is the possibility for some people to pass on their State Pension. If you reached state pension age before 6 April 2016, your spouse or civil partner can claim your state pension through something called the Additional State Pension.

As part of the new State Pension rules, you might be able to inherit an extra payment on top of your State Pension if your spouse passes away.

Something to remember: if you remarry or form a new civil partnership before you reach State Pension age, you won’t be entitled to inherit anything from your late spouse’s State Pension.

If you work for the NHS, you’re entitled to an NHS pension when you retire. The amount you’ll receive through your NHS pension will depend on how much of your earnings you paid into your pension pot while you worked there and how long you were employed there.

Your NHS pension is then topped up by your employer at a rate of 20.68%. Compared to most workplace pensions, this employer contribution rate is at the higher end of the UK’s overall average employer pension contributions.

When you die, you could be able to pass on some of your NHS pension benefits to your loved ones. Here are what the NHS calls ‘eligible dependants’ – the people you could pass your NHS pension to:

This would be your legal spouse, registered civil partner or qualifying scheme partner.

Your child or children can receive your NHS pension after you die. This can also be a child who isn’t your own but is dependent on you.

You can nominate a specific person to receive your NHS pension after you die.

You can nominate anybody to receive your NHS pension pot when you die. This can be as a lump sum or as a more typical regular payment. Here’s how each of those works:

Even though the retirement age for many people in the UK is 65, that age doesn’t factor into many pension schemes.

We mentioned it earlier in this guide, but 75 is actually the age things change for your pension. For example, the tax rules change:

This largely depends on the type of private or workplace pension you have. The two main types – defined benefit and defined contribution pensions – have slightly different rules but are still very similar, and they hinge on whether you die before or after you turn 75.

It’s possible for some people to be able to pass on their State Pension to their loved ones if you reached State Pension age before 6 April 2016.

You can nominate someone to receive your NHS pension after you die, and they can either receive a lump sum or a regular amount for life.

Not much changes at 65. You might retire then but the important age when it comes to pensions is 75.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

Find the best personal pension for you – you could be £1,000s better off.