Article contents

The best time to start a pension is right now, no matter what age you are. If you’re 40, you should put aside a bit more than someone who starts a pension younger, but it’s never too late to start saving for your retirement.

Get £50 added to your pension.

Visit PensionBee¹Capital at risk.

Looking to start a pension? Congrats! That’s the first step to making sure you’re comfortable in your old age.

If you’re aged 40, you may already have some money saved up in a pension. But if not, don’t worry! If you started working aged 18, that means you’re less than halfway through your working life (scary, right?!). So, even though we’d always recommend starting a pension as early as possible, you still have loads of time to save for retirement.

You might just need to add more to your pension each month than someone in their 20s, in order to get enough saved up to tide you over in retirement. It’ll soon add up though, and your future self will thank you for it!

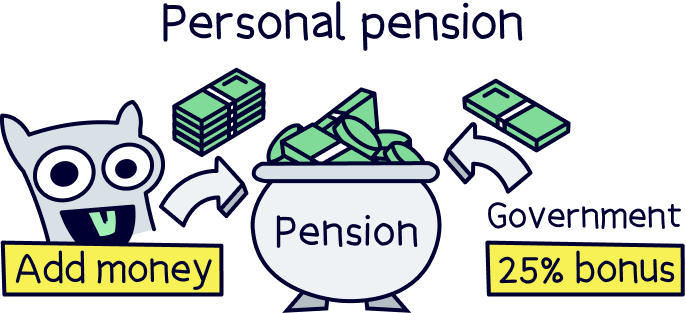

Nuts About Money tip: to help save for your future, open a personal pension. You'll get a 25% bonus every time you save. Our recommend provider is PensionBee¹.

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

No! It’s never too late to start a personal pension. And we mean it – there is actually no minimum amount of time that you have to pay into a pension before you start taking an income from it.

That means you can start a pension whenever you want – even aged 50, 60 or 70! However, we’d avoid waiting that long before starting a pension if we were you.

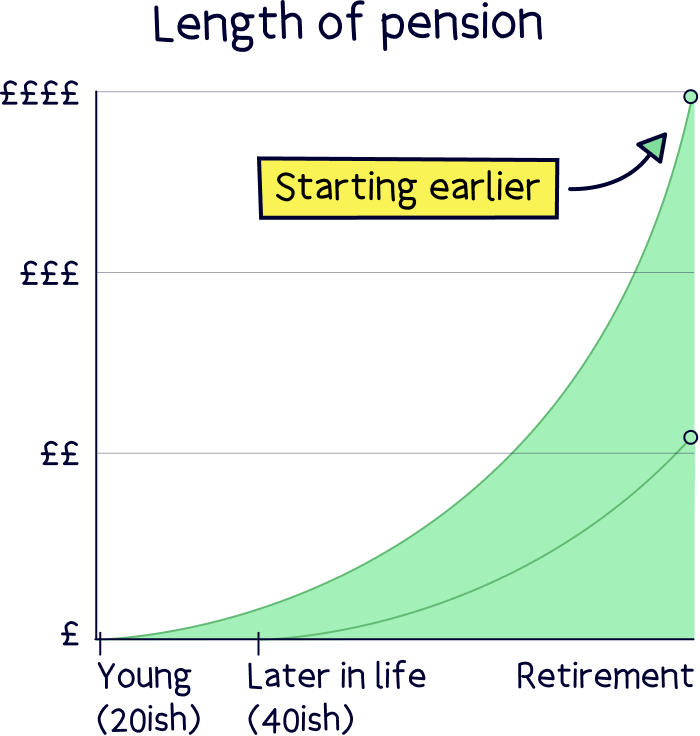

Why? Well, the earlier you start a pension, the easier it is to save up enough to live comfortably when you retire as you’ll have longer to build up your savings.

At the age of 40, if you contribute to your new pension regularly, you’ll still have time to save up a decent pot of money that can tide you over in your sunset years. It just means you might have to pay bigger chunks of your income into your pension pot than you would if you were younger, in order to squirrel away enough money before retirement.

We’ll look at how much you’ll need to pay into your pension in a moment. But for now, let’s just say that the best possible time to start a pension is right now. And even if you can’t afford to pay much into it (or even to make regular payments) anything is better than nothing – it all adds up.

Starting a pension as soon as you can – whether you’re 40 or not – comes with a whole host of benefits. So, trust us. You don’t want to wait a moment longer than you need to. Here’s why.

First things first, a pension is a great way to make sure you have enough money to live on when you’re older. You might plan on working forever, but you never know what the future might hold. So, it’s wise to set some money aside for later on in life. That way, you know you’re prepared for every eventuality.

The other great thing about a pension is that you don’t actually have to retire in order to start taking an income from it. You just need to hit a certain age (normally 55 for a personal pension, which is one you can set up yourself). That means if nothing else, you can just view it as treating yourself in your older years!

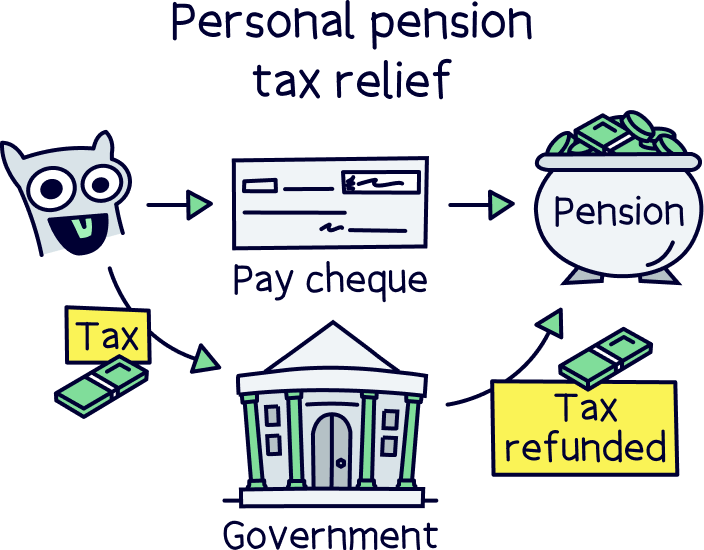

Perhaps our favourite thing about pensions is this lovely thing called tax relief.

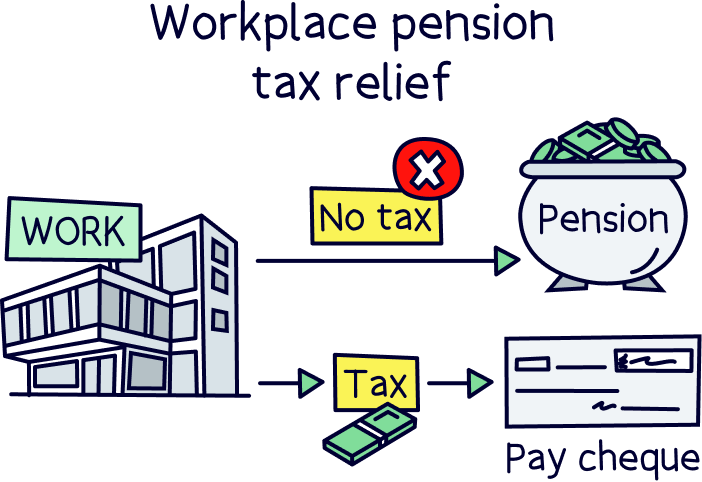

Tax relief means that you don’t have to pay tax on any income you put into your pension pot. Why? Well, the government wants to encourage you to save up for retirement so they don’t have to financially prop you up when you’re old and grey!

If you have a workplace pension (one that’s set up for you through your employer) then you simply won’t have to pay any tax on the money you put into your pension.

But if you have a personal pension (one that you set up yourself, whether you’re self-employed or you just want to set up a pension outside work to boost your income in retirement – very sensible!) then things work a little differently.

Your income will be taxed as normal through your pay cheque. But the government will then refund the tax straight into your pension pot. Kerching!

If you use one of our recommended pension providers like PensionBee, this is done automatically whenever you add money (pension providers are companies that give out pensions).

If you’re a basic-rate taxpayer (meaning you earn less than £50,270 per year), you’ll get 20% tax relief. That means if you pay £80 into your pension pot, the government will add in a £20 bonus to turn it into £100. Nice!

If you’re a higher-rate taxpayer, it’s better still. You can get 40% tax relief for any income you’ve paid 40% tax on. And if you’re an additional rate taxpayer (someone who pays 45% tax on some of their income) then you’ll even get some tax relief at 45%!

This means that starting a pension is a great way of reducing your tax bill right now, as well as saving up for later in life.

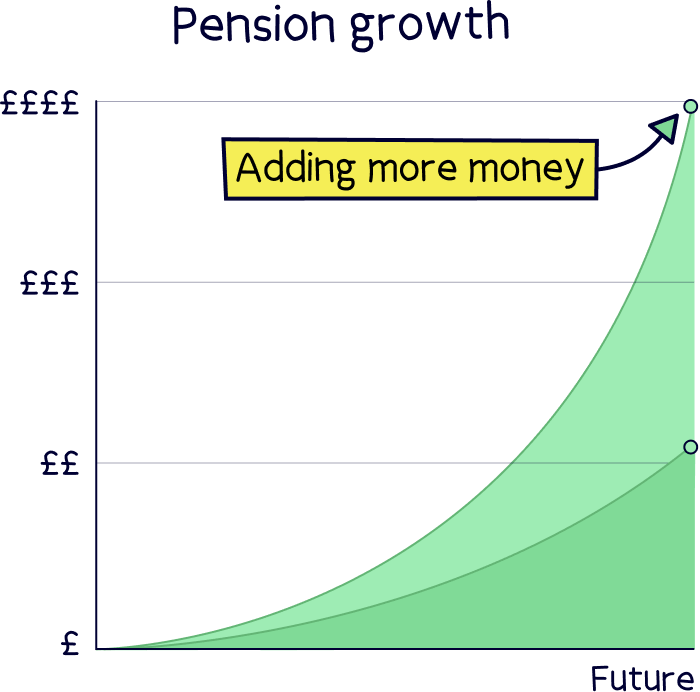

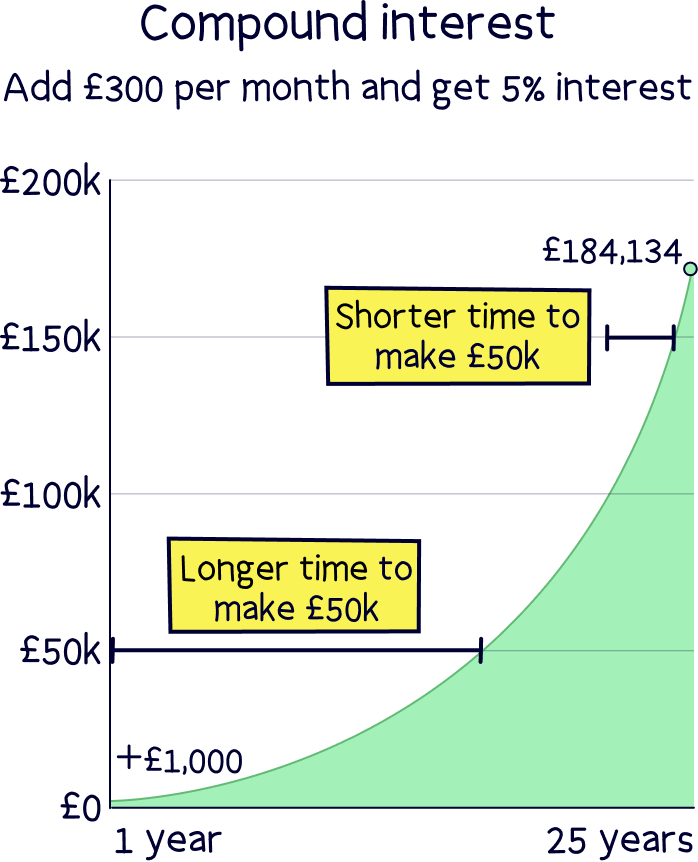

You know how we keep telling you that small contributions to your pension pot can add up over time? Well, there’s an actual reason behind it, and that’s something called compound interest.

Compound interest basically refers to the fact that when you leave your money sitting in a savings account like a pension, it will grow as the investments increase in value, or as you earn interest. Then, the extra money that you’re making will also grow too. And the extra money that this generates will grow too, and so on and so forth. This carries on and on meaning that the more money your pension makes, the quicker it will grow.

Confused? Don’t worry, let’s look at an example.

Let’s say you start a pension right now and you invest £1,000 this year. Now let’s say you make a 5% return, which is £50. That means in just one year, that £1,000 has turned into £1,050.

Imagine you now make a 5% return in year 2 as well. Suddenly, your £1,050 will become £1,102.50 (it’s now made £52.50 instead of £50 the previous year). And it will carry on growing like this every year, on top of the money you add to it yourself.

If your money keeps growing like this for 25 years and you add £300 per month too, you’ll end up with £184,134.20. Pass the champagne!

Okay, so the general rule is to take your age and halve it to work out how much of your salary you should pay into your pension. If you’re 40, that would mean putting aside 20% of your salary. But we get it, if you’re like most people, that probably sounds pretty unrealistic – especially if you have a family to feed!

Our best advice is to save as much as possible while still having a bit left over to enjoy life. You can’t take money out of a pension once you’ve added it, so you have to be sensible. But saving anything is better than nothing! If you’re got kids and you find money a bit tight right now, you can hopefully add more later on. The most important thing is to start adding money as early and often as possible – it all adds up!

Here are some other things that it can be useful to take into account when you’re working out how much you need to save.

A great way to work out how much money you need to put into your pension is to start with how much money you’ll need to live off when you’re older. You can then work backwards from there.

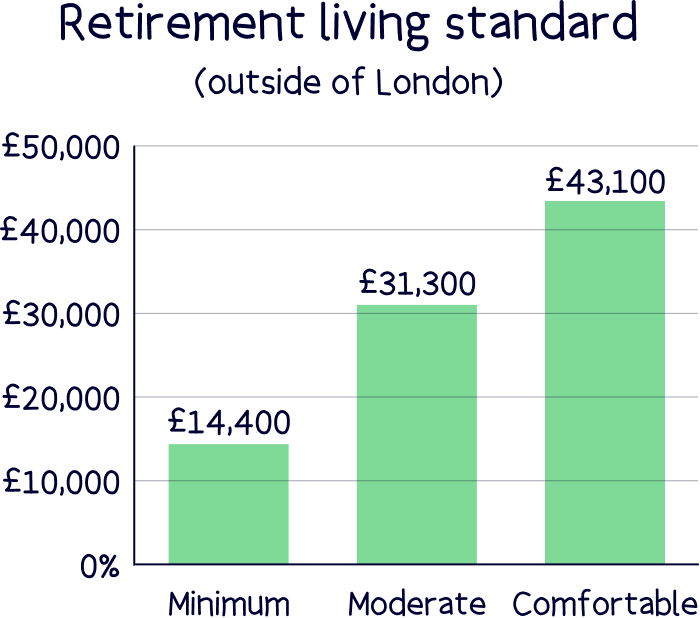

According to the Pension and Lifetime Savings Association, a single person in retirement will currently need around £14,400 a year to achieve a minimum living standard. However, they also say that to achieve a moderate living standard, it’s more like £31,300 a year, or £43,100 a year for a comfortable one. So, how do you know how much you’ll need?

Well, everyone’s different so it’s completely up to you. But if you’re stuck, we’d recommend a figure of 50% to 66% of your current salary to live on in retirement. So, if you earn £30,000 per year, that would mean saving enough to pay yourself between £15,000 and £20,000 per year in retirement.

Don’t worry if that sounds like a really big number! You don’t have to save all this from scratch. You might be able to move to a smaller property when you retire to free up some cash, or you may have old pensions lying around that you’ve forgotten about. All this can help to tide you over later on in life. We’ll come to these properly in a sec!

Another factor will be when you want to retire. If you want to retire at the age of 55, you’ll need to put aside more of your salary than if you’re planning on retiring at the age of 70. That’s because you’ll have fewer years left to save before retirement!

Think about it. If you’re 40 now and you plan to retire at 55, you only have 15 more years to save. On the other hand, if you wait until you’re 70, you’ll have a whopping 30 years left to save!

Ultimately, if you haven’t started saving for your retirement yet then don’t panic. It just means that you probably won’t be able to retire early if you want to carry on living your current lifestyle.

Just remember to be realistic. You might love your job and want to work until you’re well into your 70s but you never know what the future will hold. If something happens that forces you to retire early, you could end up in a sticky position if you haven’t planned for it.

At the end of the day, it’s all about finding the right balance for you. So, make sure to take into account your own unique circumstances – like how physical your work is – when you’re considering your retirement age. The average retirement age in the UK is 64.7 years old for men and 63.6 for women, according to The National Archives.

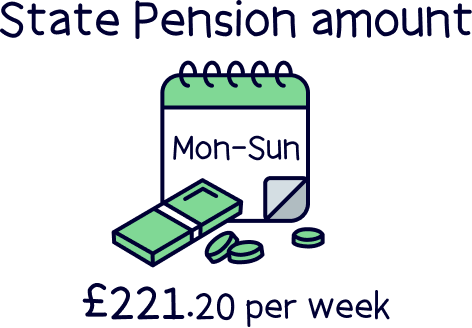

The State Pension is a weekly payment you can get from the government once you reach State Pension age. That’s currently 66 but it’s slowly getting higher – for people born in April 1960 or after, it’ll be 67 and then it’s going to gradually climb to 68.

The full State Pension is currently £221.20 per week. So, it’s not much at all! However, it’s a nice extra that you can take on top of any workplace pensions and personal pensions you have.

If you qualify for the State Pension (and most people do), this may mean you don’t have to put aside quite as much money for retirement, as the State Pension will boost the income you can take from your workplace or personal pension. Not by much, but every little helps, right?!

Anyway, you can access this weekly payment as long as you’ve made enough National Insurance contributions throughout your working life (National Insurance is a payment you make alongside your taxes to cover things like healthcare).

For most people, National Insurance is compulsory. So, you should be well-placed to qualify for the State Pension. However, if you earn very little you may not need to pay it. That might sound great but unfortunately, it means missing out on that lovely State Pension – unless you make voluntary contributions.

We know, we know, voluntarily paying for something you don’t have to doesn’t sound like fun and it’s important that you don’t overstretch yourself. But if you can afford to then we’d strongly recommend voluntarily paying National Insurance so you can unlock that nice weekly payment in your old age. You’ll thank yourself when you’re old and grey, we promise!

If you want to save using a pension check out our recommended pension providers.

Of course, your pension isn’t the only thing you can use to live off when you retire. You may have other financial reserves you can dip into in your sunset years, which means you could afford to put a little bit less into your pension pot.

Do you have a house you plan to sell? Lots of people move to a cheaper home when they hit retirement age, which means they get a hefty chunk of cash in their pocket perfect for tiding themselves over in their old age.

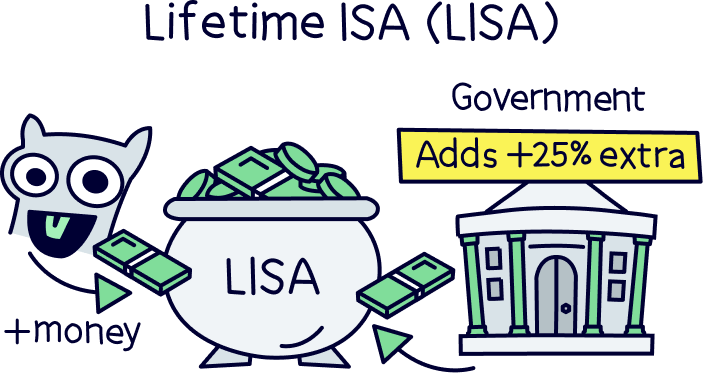

Do you have money stashed away elsewhere? You might have other savings accounts that could support you later on in life – like a tax-free ISA or a Lifetime ISA (a special type of savings account designed to help you save for your first home or for later on in life. Note: you can find out more by visiting our friends at Tembo¹).

Don’t get us wrong, if you’re looking to save for retirement, we’d recommend a pension over an ISA any day. That way, you get that lovely government bonus we told you about! But if you have other savings accounts alongside it, there’s no reason why you can’t take them into account when you’re working out how much you need to put aside in your pension. Just be sure that you don’t dip into them early so you don’t become unstuck when you’re old and grey.

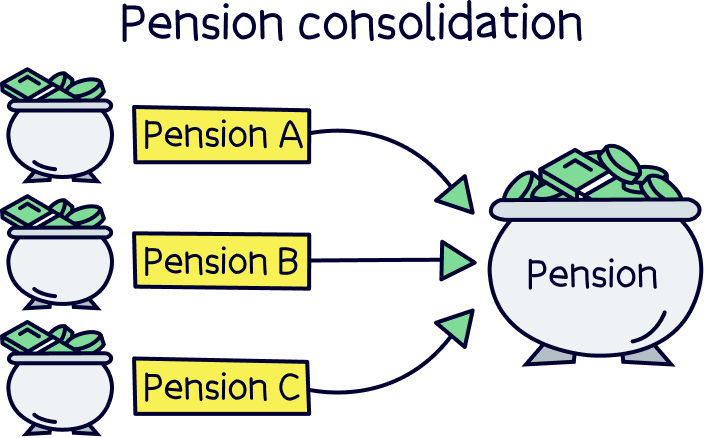

If you’re 40, you may well have had workplace pensions set up for you by previous employers. After all, employers will normally have to set up a pension for you by law!

Remember that crappy job you had in your gap year? You might have a pension from it. What about that job you quit 10 years ago? You probably have a pension from that too.

See if you can track any old pensions down. You might have already saved up more for retirement than you realise. And if some of those pensions are quite old, they’ve probably grown quite a bit since you last saw them! You can find your old pensions using the government’s Pension Tracing Service.

Once you’ve tracked down those old pensions, it might be a good idea to transfer them all into your new pension, which is called pension consolidation. This will make them easier to manage and reduce the risk of them getting lost again! Plus, you’ll sometimes be able to benefit from a cheaper fee when your money is all together in one pension.

Transferring your old pensions to your new one can be super easy. You just have to ask your new pension provider and they’ll sort the whole thing for you. In fact, our favourite pension provider, PensionBee, will literally just ask for the name of your old pension provider before doing all the work and transferring it for you. So, you won’t have to lift a finger!

Hit 40? Don’t have a pension? Or simply want to start a new pension to boost your savings once you retire?

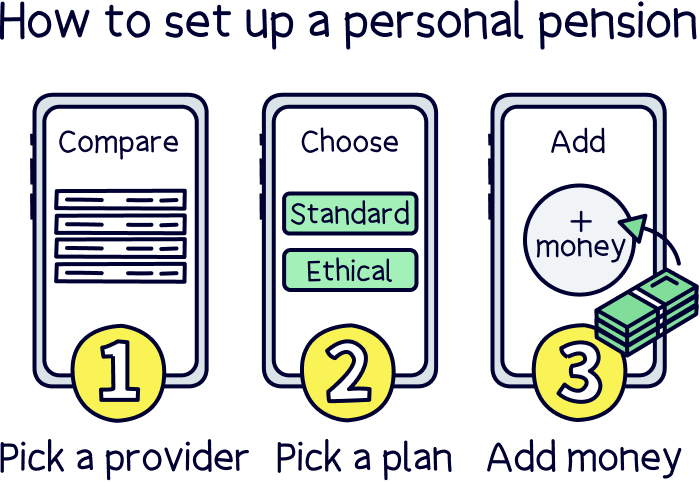

Luckily for you, starting a pension has never been easier! Here’s how to do it in 3 simple steps.

First things first, you’ll need to choose a pension provider. These are the people who give out pensions and who’ll look after your money for you.

Different pension providers will offer slightly different services. Some will spend more time trying to help your money to grow than others will. And some will charge you higher fees than others. So, it’s important to find a provider that works for you.

That said, our favourites are the modern pension providers that make it super easy to save and manage your money with online apps, and they’re normally cheaper too! We’ve listed them below.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

Now you have a pension provider, they’ll help you to pick a plan. This is a couple of questions that lays out how your money will be looked after and how much you’ll pay for the pleasure.

Often, this is to do with how old you are and when you think you might retire – at 40, you’re still young(ish), so you could pick a plan that aims to grow your money a lot!

If you pick a modern pension provider, you’ll often also be able to choose to have your money invested only in ethical and socially responsible companies. So, you’ll know that when your money grows, it hasn’t come at a cost to the environment or local communities.

We’re obviously a big fan of these – why not help the world at the same time as helping your savings?! If you’re a fan too, PensionBee and Moneyfarm are all providers that you can do this with.

Once you’ve signed up, all that’s left to do is to start paying money into your new pension. It’s as easy as that!

Some pension providers will ask you to pay in a minimum contribution each month. But most will let you pay in as much or as little as you want. You don’t even have to make regular payments if you don’t want to!

That’s right, if you’re strapped for cash, you could just add some money to your pension whenever you have some spare. Or, if you’re serious about saving, you could go the other way and set up a direct debit to put in a regular amount each month.

Remember, if you’ve waited until you’re 40 to start a pension, it’s wise to put aside as much as you can so you can save enough to tide yourself over when you retire. But equally, it’s important not to overstretch yourself either – you can’t take the money back out if you need it. It’s all about finding the right balance for you.

Now, as far as we’re concerned, there’s nothing bad about pension providers that use apps and websites to make saving up for retirement easy. In fact, we think they’re the future! But we get that not everyone’s the same.

If you’re a bit more old-school, you can start a pension by speaking to a financial advisor. These are professionals who can help you to find the right pension provider for your needs, and set up a pension for you either over the phone or in person.

The downside is that this can be expensive. Financial advisors will normally add their own fees on top and the plans they offer you will often have more expensive fees too. That said, if you’re still keen, Unbiased¹ is a great way to find the right financial advisor for you.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

If you take anything away from this article, we hope it’s this: start a pension as soon as possible and pay as much into it as you can without stretching yourself too thin (you won’t be able to take this money out for many years). The sooner you can start squirrelling money away into a pension, the easier it will be to save for your sunset years. And if you pay into it as often as possible, it will soon add up.

It’s easier than you might think to start a pension these days, as you can get started right away with our recommended pension providers, PensionBee¹ and Moneyfarm¹. Their modern apps and low fees make saving for retirement and growing your money a breeze. In fact, we’d go so far as to say it can even be fun!

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.

This article was written by the team at Nuts About Money, and fact-checked by 2 independent reviewers. You’re in safe hands.

Check out PensionBee – it’s easy to use, low cost and has a great track record of growing pensions.