Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more.

Article contents

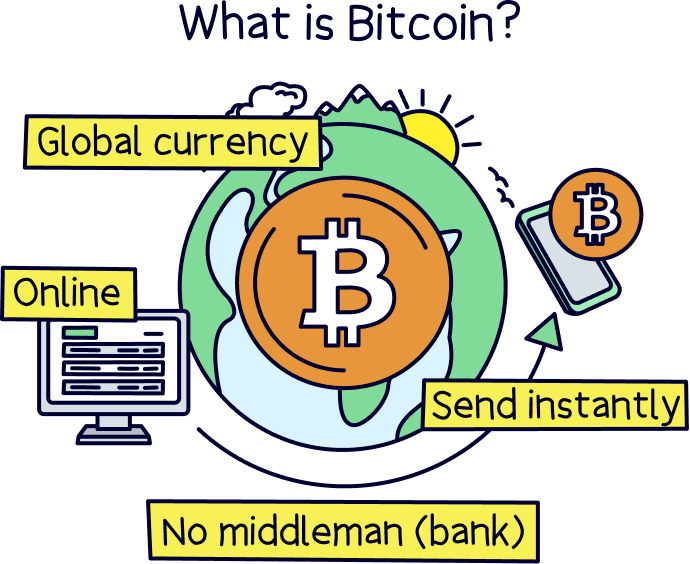

Bitcoin is digital money (a currency) which you are able to send directly across the world from person-to-person without a bank involved, in seconds and for very low cost. It’s also inflation resistant, and not controlled by any central authority – meaning you can't just print more of it like governments do with money.

Heard about Bitcoin and digital currencies (digital money) and haven’t got any idea what they’re talking about? Don’t worry! It can be complicated, but we’ll explain everything you need to know clearly.

Bitcoin is a pretty new currency that only exists in digital form, so there’s no bank notes or coins, everything happens across the internet using your phone or computer. However, it’s particularly unique, and an evolution of traditional currencies that currently exist (such as Pounds or Dollars – also called fiat currencies).

It has 3 core elements, which we’ll cover in more detail later:

Bitcoin was the first cryptocurrency and currently the world’s largest. It was created in 2008 by an anonymous person, or team or people, who called themselves ‘Satoshi Nakamoto’, and largely inspired by the mismanagement of money by governments and central banks (banks of a certain country, such as the Bank of England) – particularly around the global financial crisis that occurred during that time, when governments bailed out large banks who themselves were mismanaging money. And unfortunately, it’s all got a lot worse since then, particularly during the coronavirus pandemic.

We won’t go into the details too much, but governments and central banks have the ability to create more money whenever they like (and also adjust the interest rate of their borrowing), and as a result, causes the value of money to reduce (called inflation), which means things get more expensive over time, like food and bills. Effectively, creating new money makes the poor, poorer and the rich, richer (as the things rich people own, such as property and businesses, often grow in value too).

Almost every government in the world, and so the country itself, is in fact in huge amounts of debt, and most are potentially bankrupt. Many people out there believe that governments have too much power when it comes to public finances and money creation – and Bitcoin is seen as the perfect solution.

Bitcoin has a fixed supply of money (coins), new bitcoin can never be created, and so there can never be any mismanagement, now or in the future – in terms of money in circulation.

The supply is 21,000,000 (or will be in the year 2140 when all the bitcoin are created – called mined. More on that later).

As we mentioned above, this means inflation (reducing the value of your money) is near impossible (although currently the price changes often). And, people have full control over their own money, rather than a government. In fact, it’s possible the value of their money will actually naturally increase in value similar to a savings account.

It’s also seen as a ‘store of value’, which means it’s a safe place to leave your cash as it won’t decline in value (like cash does), similar to gold. However, the price fluctuates (goes up and down) too much for most investors to do this currently.

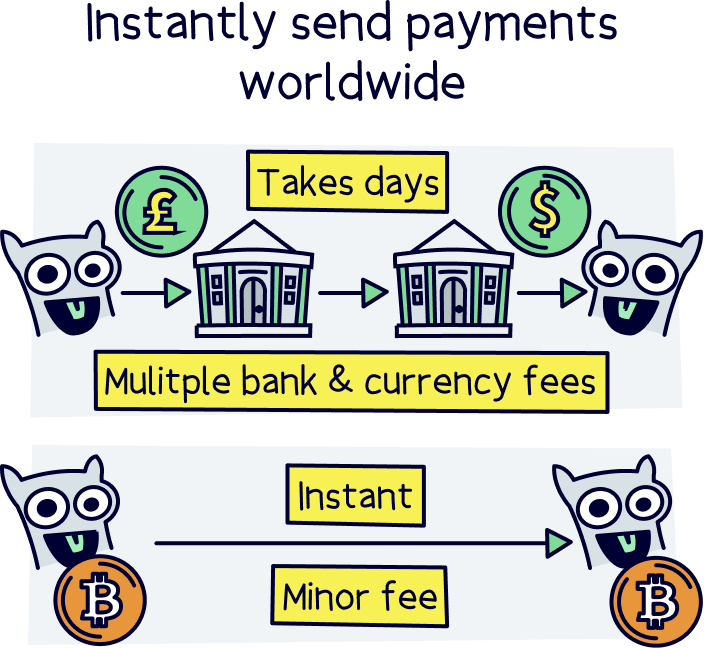

Did you know that when you send money via your bank account to someone else, it actually goes through loads of different banking systems and then finally ends up in their bank account? And if you’re sending internationally, there’s even more systems. It can take days – not to mention the hefty fees you pay for sending money abroad! Plus hidden fees like currency exchange fees.

With Bitcoin, you can send it directly to someone else, in seconds, without a bank(s) as a middleman. And for almost zero fees. It sounds so simple, but it’s never existed before. There’s no need for a bank to confirm the transaction, it all happens on the Bitcoin network, effectively run by software and computers. It’s the modern version of money transfer.

But it gets much better than that, as you can send bitcoin near-immediately, for free, and directly to someone else, businesses that take payments (e.g. a shop) can actually receive bitcoin as payment rather than a card payment – which saves them a huge amount of money, as much as 3% per transaction. That’s a seriously good saving, this saving can be passed on to the customer making things and services cheaper. They'll also get the cash immediately, rather than waiting days for transactions to settle (complete).

While creating Bitcoin, ‘Satoshi Nakamoto’ also created a new technology called ‘blockchain’, and it’s this technology that Bitcoin runs on, and is also the technology that has created an entire new industry called cryptocurrencies (we’ll cover that a bit more later).

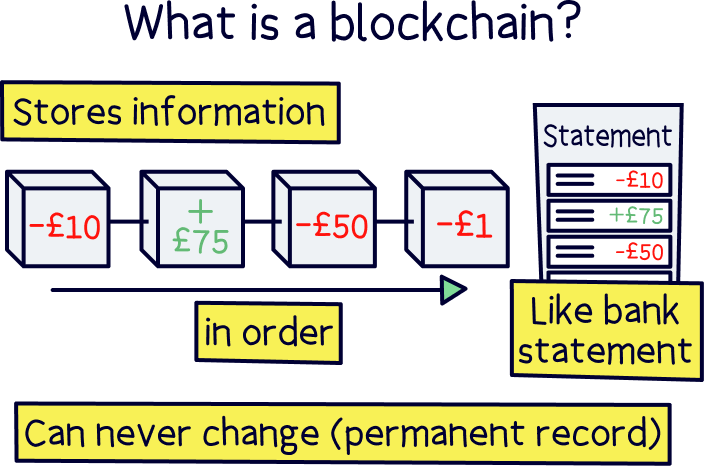

Without getting too technical, a blockchain is very similar to a database, but it can never be changed or altered, only new information can be added to it, and this information is contained in a ‘block’ that is added to the ‘chain’. In a long, permanent, never changing line of blocks. This is also called the Bitcoin ledger.

So imagine making a bitcoin transaction, and sending money to a friend, your bitcoin transaction would be added to the latest block, then the block is added to the chain. And, then this is permanently stored in the ‘database’ (the Bitcoin ledger). The technical term for this is the Bitcoin network, or simply Bitcoin blockchain, and the way this all happens and bitcoin transactions are recorded is called the bitcoin protocol (set of software rules).

As no one controls the Bitcoin network, these transactions can never be changed (or hacked), it is a permanent record (and so your bitcoin is very safe).

The Bitcoin blockchain is completely public to see, and so everyone (and most importantly software), now knows that you sent your friend some money, and their balance has gone up by that amount and your balance reduced by the same amount.

You could think of it like a bank statement, with money coming in, and going out, in a fixed order, and once it happens, it can never change. It’s still very private for individuals however. No one knows who owns which bitcoin address (unless it’s public, such as a charity’s address).

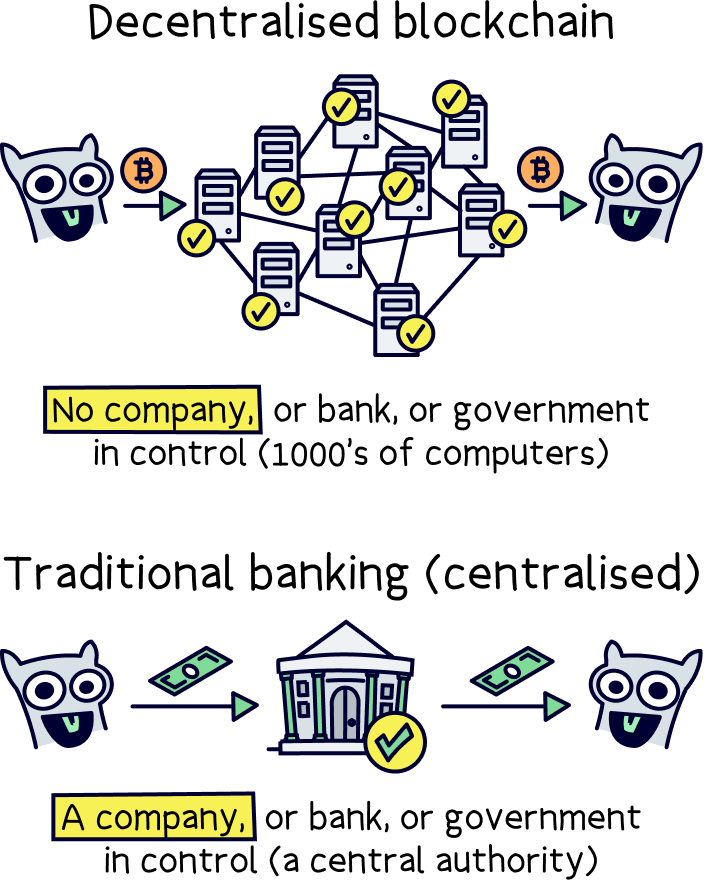

Now you might be thinking that doesn’t sound very complicated or clever at all. Well, it’s actually never been done before, and the genius behind the technology is that it is distributed across the world, so there’s no one central company (such as a bank) deciding which transactions are right or wrong, and the right time order of transactions.

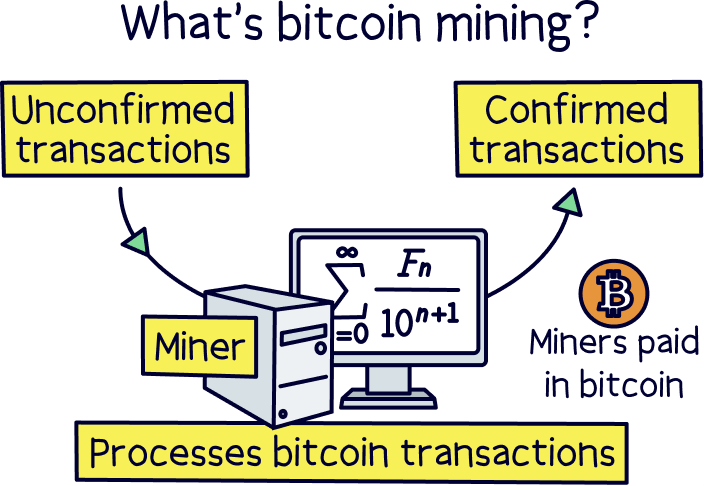

There’s a huge network of computers, called bitcoin miners, all over the world, who process the transactions and confirm that the order of transactions within each block is correct, and then add it to the blockchain to make it permanent. (More on that below.)

When you make a transaction on the bitcoin network, you’ll pay a small transaction fee (when you send bitcoin), which goes to the miners as a reward for including your transaction in the block.

Although making bitcoin transactions in shops and other places is completely free, as they use the bitcoin ‘lightning’ network. We won’t go into that now, but it makes transactions super fast, effectively free, and more private. Learn more on the lightning network website.

Bitpanda is a hugely popular crypto broker, with a wide range of coins, top grade security and great features.

The core concept behind Bitcoin is the network of computers spread across the world, called bitcoin miners. This makes Bitcoin completely decentralised, meaning it is spread out in thousands of different places, rather than centralised where it runs from a single place – such as Google or Amazon, who run their own services. There’s actually over 1,000,000 bitcoin miners across the world!

Again, we won’t get too technical here, but every miner runs bitcoin software that processes transactions and confirms them to be true and the right order, and then broadcasts this back to the network in the form of a block, where all the other computers mining bitcoin accept and add to the chain, and then a new block is created and so on and so on.

This happens every 10 minutes, and if a miner is the one to propose a new block, they’ll be rewarded with a ‘block reward’ of new bitcoins, which is currently 6.25 bitcoin, but will reduce over time until 21,000,000 bitcoin have been ‘mined’. In 2024, it will be 3.125 bitcoin.

A bitcoin miner has to solve a complex maths problem first in order to be the one who proposes the block, which can use lots of energy, and it's this difficulty and the energy use that protects the network from being hacked and overrun. The energy use guarantees that the blockchain will always remain true. It is therefore arguably a great use of energy.

It is worth highlighting that the current way of sending money across multiple financial companies, banking systems and networks uses far more energy than Bitcoin does.

Note: mining like this is called ‘proof of work’, which is where computers have carried out ‘work’ (the mining process), as opposed to ‘proof of stake’, which is where you are willing to stake (use as a deposit) your own money to propose transactions as genuine, such as Ethereum (more on that below).

You might have noticed we’ve used Bitcoin (with a capital B), and bitcoin (with a lowercase b), a lot. There is actually a difference. The network, or blockchain is called Bitcoin, and the coins, or tokens that you own and transfer across the network are called bitcoin. Simple!

When you use the Bitcoin blockchain, instead of having a bank account like you would with traditional money (fiat money), you have a bitcoin wallet instead. And this is where you store your bitcoin, and use it to make transactions to send and receive bitcoin too, or make bitcoin payments with somewhere like a shop (if they accept bitcoin).

Your wallet has a unique bitcoin address (similar to your unique email address), which can be read on the blockchain, and is public for everyone to see. However that doesn’t necessarily mean anyone knows who owns the address. There is still privacy when using bitcoin.

And, you can have as many wallets as you like, new ones can be created in seconds, with no cost, and effectively there’s an unlimited number of wallets that can be created.

Bitcoin wallets are unique to anything that existed before, there’s no username or password (although there can be depending on which wallet you use). Instead, a private key is created for you (which is effectively a password).

This private key is what is used to access your wallet and make (sign) bitcoin transactions. It means that only the person with the private keys can access and use a wallet and the money inside. This makes it very secure. Your bitcoin can never be lost or stolen without the key. Just don’t lose it, or share it with anyone!

With the creation of blockchain technology, a new industry has emerged, crypto, or cryptocurrency. This is networks, or blockchains, using the blockchain technology to do other innovative things, rather than simply sending, or storing money.

The most innovative and popular development is Ethereum. Which allows for software programs to run on the blockchain too, and effectively use the computing power of all the computers across the world supporting the network to run. It’s similar to the internet, where most of your phone apps and computer software run, without you needing to do anything.

So, a software engineer could create their own software, or business, and use the blockchain and the transaction-based concept to run their program. These programs are called ‘smart contracts’.

This has the potential to disrupt pretty much everything that happens in the world currently. For instance, traditional finance, supply chains, shopping, you name it, it could be improved with blockchain technology.

It makes things far more efficient, accurate, cheaper, and decentralised (so no central authority) – so potentially large megacorporations such as Amazon, Google, Facebook, who have far too much power and control could never exist again. It’s very early stages, but it’s a very interesting space, we're geeking out now!

Yep, it’s perfectly legal to use the Bitcoin network, send bitcoin, use bitcoin to pay for things. Do anything you want with it! And it’s perfectly legal to buy and sell bitcoin. In fact, if you’re interested, here’s how to buy bitcoin in the UK.

And the same goes for any cryptocurrencies, including Ethereum. We’ve also got a guide on how to buy ethereum in the UK too.

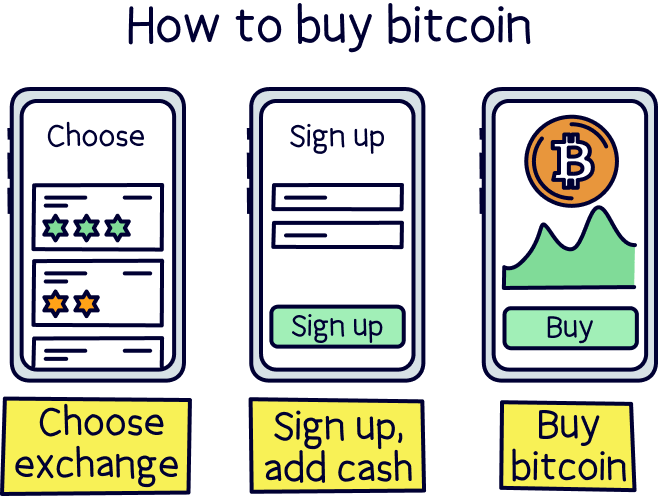

If you want to buy bitcoin (or sell), all you need to do is head over to a cryptocurrency exchange (a place where you can specifically buy cryptocurrencies). There’s websites (and phone apps) dedicated to crypto, and you can simply buy bitcoin with your local currency (Pounds).

After that, you can either keep it on the bitcoin exchange, or withdraw it to your own wallet (recommended), where it’s more secure and all under your control. Here’s where to find a bitcoin wallet.

On an exchange, bitcoin is often represented as BTC – which is bitcoin’s ‘ticker’. It’s a short code for trading and investing, similar to how the company Apple is AAPL on a stock exchange.

The price of bitcoin changes all the time, so be prepared to have fairly large changes in price if you want to invest. However, historically it’s increased in price quite substantially.

To buy bitcoin, check out the best crypto exchanges.

Bitpanda is a hugely popular crypto broker, particularly in Europe, where it’s one of the largest crypto platforms, and still growing - it has more than 7,000,000 customers worldwide. In the UK, it offers access to over 600 cryptocurrencies, with no deposit or withdrawal fees. Bitpanda was founded in 2014 in Europe (Austria), which is old for crypto!

You might have heard of them as they’ve sponsored PSG, AC Milan and Bayern Munich football teams, alongside the Davis Cup tennis tournament and the World Padel Tour.

Bitpanda is suited to pretty much every type of crypto investor, from those just getting started and looking to buy and hold assets such as bitcoin, all the way to advanced traders looking for a secure and reliable platform.

Trading is available 24/7, and there’s industry leading security to ensure your account and crypto are secure.

For beginners, it’s accessible, and there’s a wide range of help articles to get started and learn about investing and the platform itself. And you can get started with just £10.

Fees wise, it’s reasonable. There’s no fees to deposit or withdraw money, or to hold crypto within your account. You’ll pay a fee when you buy or sell crypto, and this ranges from 0.99% to 2.49% depending on which crypto you are buying (lower for the more popular coins such as bitcoin).

You can earn rewards on your crypto too (called staking), all within the Bitpanda platform.

The customer support is good, with a large help centre that covers most common questions and a support ticket system where you can email in for specific issues, with great service and feedback.

Overall, it’s a great platform, and well worth checking out.

Account fee: free

Dealing fee: from 0.99% to 2.49% per trade

Currency conversion fee: n/a

Deposit or withdrawal fees: n/a

Uphold is super easy to buy and store crypto. It's one of the easiest places out there, and the mobile app is great.

It's very popular in the UK, Europe, USA and across the world, with over 10 million customers. And, it’s also one of the safest platforms out there.

The range of coins is good (over 250), and you can store local currencies too (e.g. Pounds, Euros, Dollars).

You can also open a business account (if you have a company).

Popularity: popular

Mobile app: Yes (Apple and Android)

Crypto wallet: yes

Fees: high

Minimum deposit: £1

eToro is one of the most popular places to buy assets like crypto (including bitcoin), stocks and shares, and more.

Their website and app is easy to use.

Plus, it’s easy to view your performance, buy/sell and trade other cryptocurrencies.

A great feature exclusive to eToro, is allowing you to follow other investors, learn from them and even copy their trades.

Popularity: extremely popular

Mobile app: yes (Apple and Android)

Bitcoin wallet: yes

Fees: medium-high

Minimum deposit: $50

Bitpanda is a hugely popular crypto broker, with a wide range of coins, top grade security and great features.

We hope that made Bitcoin a bit easier for you to understand. It’s an incredibly complicated topic, but also incredibly exciting, and the technology is constantly evolving and constantly being developed – it is software afterall!

There’s a lot more to it, but the best way to learn more about Bitcoin is to simply try it out. Buy some on an exchange, make a wallet (optional), buy some bitcoin and start using it. The easiest way to get started is by using one of our best crypto exchanges (UK).

You can also learn lots more on the official Bitcoin website.

Bitpanda is a hugely popular crypto broker, with a wide range of coins, top grade security and great features.

Bitpanda is a hugely popular crypto broker, with a wide range of coins, top grade security and great features.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things crypto, with several years of combined experience writing and talking about crypto, blockchain and investing. We’ve lived the ups and downs of the bull and bear markets, and know our bitcoin from our blockchains, and are keen to see how the industry grows.

More than 8 years of combined experience researching and writing about crypto

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of crypto exchanges and companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Bitpanda is a hugely popular crypto broker, with a wide range of coins, top grade security and great features.