Review contents

Yonder is a modern credit card that allows you to earn some great rewards (think dining out, shows, holidays and small things like a glass of wine), while also being a great card to spend abroad. There’s no currency conversion fees so it’s cheap to use abroad, you can use it pretty much anywhere. As a full member you can get travel insurance too. As it’s a credit card, you’ll get more protection when you spend money and can build your credit rating.

It’s not often a new credit card company emerges, so it's getting some well deserved attention! Yonder are taking on the likes of American Express in the UK with their new credit card that rewards spending with points that you can redeem for experiences local to your city, that change every month. Think restaurants, drinks, theatre shows, that kind of thing.

If you like to explore your city, trying new places, doing new things, keep reading, Yonder might be right up your street.

It’s great for travel too, with worldwide travel insurance for the family (with the full membership), and more importantly, no foreign exchange fees when spending abroad. Plus, you can earn points if you book your flight with Yonder, and use points to buy flights too.

And, of course, you can borrow money like all other credit cards. So, you can build your credit rating, get more protection on your spending (more on that below), and pay back what you borrow as and when you like (but please be careful, there's fees involved when not paying back in full each month, see below).

If you’ve heard enough already and are keen to get started, get one month free and up to 10,000 bonus points when you sign up for the full membership and spend £200–£1,000 in your first 30 days. Head over to the Yonder website¹ to get started.

Right, let's dive into the details.

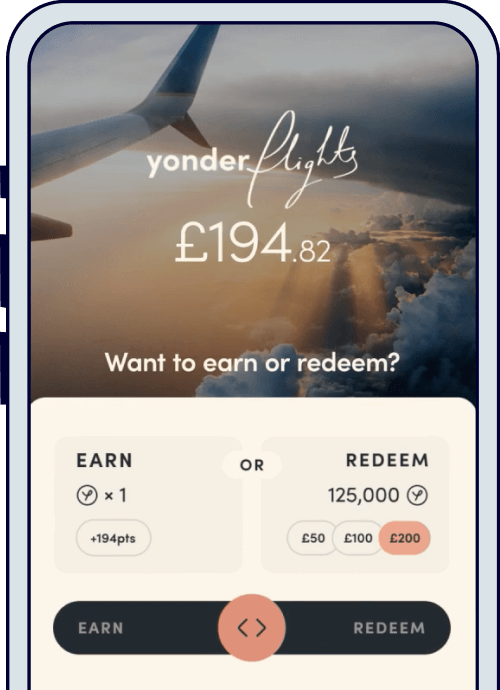

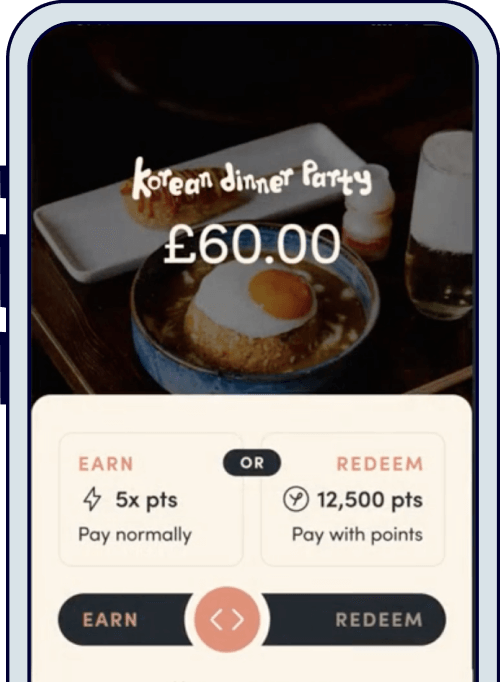

Yonder is a rewards credit card, and that means when you spend on your card, such as in shops, restaurants, pubs, anywhere, you get a certain amount of points based on the amount you spend. Normally, it’s 1 point for each £1 spent.

With Yonder, you’ll get 5 points for each £1 if you are on the full membership, or 1 point for each £1 if you are on the free membership.

With these points you can then choose rewards, based on the number of points you have and want to use. Simple right? Not all credit cards are like this, most just allow you to borrow some money and pay it back. So this one's a bit special.

We’ll run through the rewards below.

Aside from the points and rewards, it’s great for holidays too. And with the full membership you can use your points for flights with any airline!

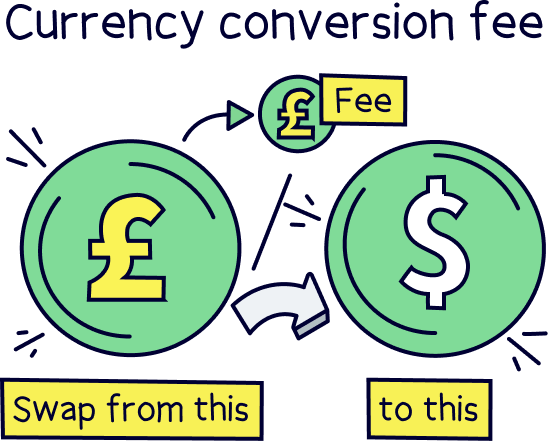

You can also use your card abroad in a foreign currency and not have to worry about expensive currency conversion fees. Yonder doesn't charge a fee, and as the card is a Mastercard, it uses Mastercard’s exchange rate, which is one of the best you can get (although it still has a tiny Mastercard fee that most currency cards have).

That also means you don’t have to worry about actually getting any foreign currency before you go abroad, or setting up an app to hold foreign currency (unless you want to). Simply use your Yonder card abroad in shops and when you are out and about.

There’s also travel insurance included in Yonder’s paid membership, which is worldwide insurance for the whole family. We’ll cover the insurance details in more detail below.

Try Yonder for a month, and get up to 10,000 bonus points to spend too.

Yonder says ‘rewards you’ll actually use’, which sounds promising, but lets take a look at what you can get…

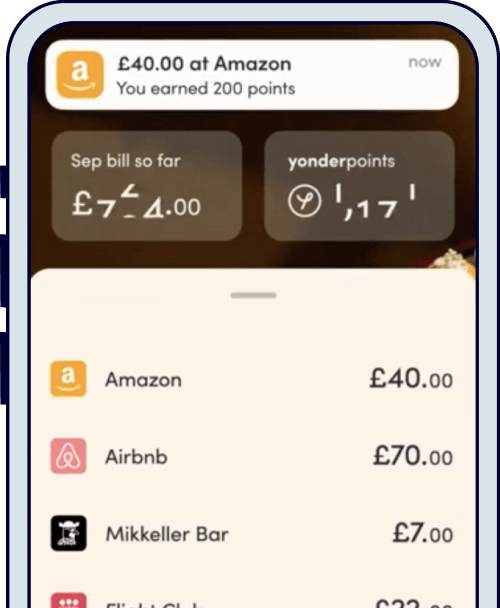

These are pretty good, and they’re things like hotel stays abroad and in the UK and live events, such as gigs, outdoor cinemas, art exhibitions and shows (big ones like the Lion King). There’s loads more, and suited to all types of people (even things like renting a car). If you don’t like going out, there’s things for home too, like fresh flowers from top florists.

They also include eating out in restaurants in your local city (London, Manchester, Birmingham, Bristol and Bath), and these change each month. Some previous restaurants have been places like Gunpowder and Bao (semi-famous restaurants in London).

And there’s small things, like a glass of wine or beer, or snacks. Essentially, it’s any business that would like to promote their business to Yonder customers. You get a good deal, and the business gets a nice bit of promotion with the hope you might come back in future.

The great thing about this is businesses aren't allowed to give you a crappy deal, such as only during certain times (like only in the mornings), or only choosing certain food dishes. We know the score don’t we? But with Yonder, there’s no limits, everything that the restaurant offers is on the table.

And finally, the experiences are available for everyone, but the ones Yonder thinks will suit you are put into a ‘for you’ page, so you can find them easily. So, what you get should be useful and local to you, and as a reminder, they are updated every month.

Simply use your Yonder card when you buy things. There’s no coupon or discount code to add. Pretty handy actually. And then in the Yonder app just tap the transaction that matches the offer after you spend and select use points instead of cash.

There is a ‘fair use’ policy, which simply means sometimes there might be a limit on what you can actually get for free on the deal. For instance, it might be up to £100 per meal. At which point, your points would be able to claim the £100, but anything over that you’d still pay cash. This all depends on the actual deal itself.

Travel and credit cards go hand in hand, and with the full membership with Yonder, you can use your points for flights with any airline (rather than just British Airways, which is the deal with American Express). That means your annual trip to Spain just got a bit cheaper.

This works in the same way as using other offers. Just buy the flight using the card first, and then within the app select use points. There is a limit of £200 per booking though, so you might not get the whole flight covered.

It’s a pretty great travel card, and you can spend abroad in basically any country and any currency (except places where there are restrictions like Iran and North Korea). You spend with your card as per normal, such as at a restaurant or shop, and it will be converted into the local currency when you pay.

Nuts About Money tip: select pay in the local currency if asked, such as in a shop, rather than paying in pounds, otherwise you’ll face conversion fees from the shop itself (their payment provider).

As the card is a Mastercard, it means you can use it pretty much worldwide, and in pretty much every restaurant, shop, bar, wherever you want to. It works with most currencies too. Super handy for travelling.

And when it comes to fees, it's pretty minimal. Yonder don’t add any currency conversion fees on themselves, and you’ll use the Mastercard rate to exchange money, which happens when you spend, which is one of the best exchange rates you can get.

This is a bigger deal than you might be thinking. Normally spending on a credit card abroad is super expensive, and a big no-no. Credit card companies can add up to 3% as a fee, and don’t use a good exchange rate (meaning hidden fees). That can really add up when you’re spending. And definitely don’t use your normal debit card if it’s from a high street bank, as they often have high fees too. Use a card designed for travel, or if you’re a Yonder customer, use that.

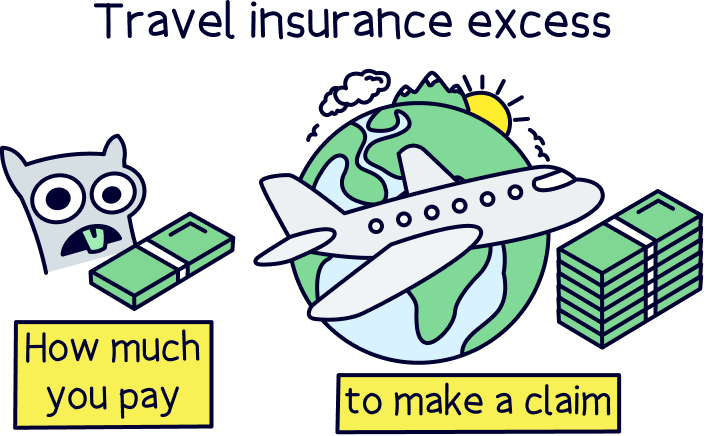

As a Yonder full member, you also get travel insurance too. It’s pretty comprehensive, and likely suited to most people for a typical holiday.

It covers the whole family (if you have one), which means your partner (in the same house) and any children under 25, as long as they are travelling with you.

The main key points of the coverage are:

There’s a few other things too, such as your baggage not turning up after landing, and costs while your flight is delayed (such as an overnight stay).

In terms of the excess, which is how much you pay yourself if you make a claim, it’s zero for most things and £50 for a few things, such as lost baggage and missed flights.

The cover can last up to 60 consecutive days on a single trip, and each trip needs to be from and back to the UK. You can travel for a maximum of 180 days per year.

An important thing here is to use your Yonder card to get the coverage, so you need to put the flight deposit (or full cost) on your card to get your flight covered (e.g. cancellations), and your hotel to have your hotel covered (e.g. again cancellations), otherwise you probably won’t be able to claim for everything. Yonder uses this information to check things. You’ll get the points too of course.

Right then, can everyone get a card? How does it work?

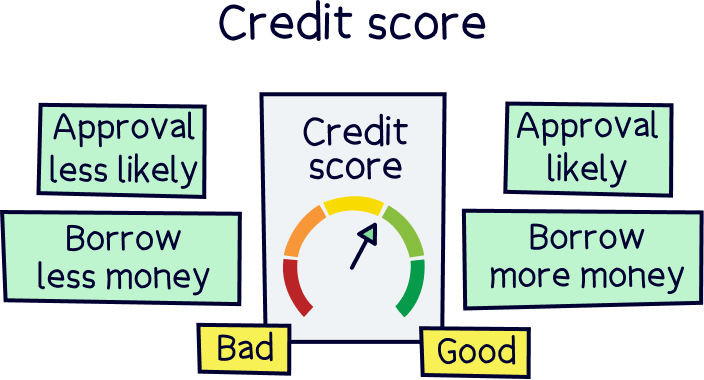

First things first, unfortunately if you’ve got quite a bad credit rating, you won’t be able to apply. That’s things like if you have a CCJ in the last two years, have missed payments on things like a loan or are currently on a debt management plan.

You’ll also need to be 18 and a UK resident, and have a UK bank account, and you’ll need to connect your bank account to Yonder, who will look at your spending data for a review to determine your credit limit on your card.

There’s a minimum salary of £25,000 if you are employed in a job, and if you are self-employed you’ll normally need an annual income of £35,000.

There’s a two step process, you can check your eligibility quickly on the Yonder website¹. Simply add a few details and it will review your circumstances in a couple of minutes. There’s no impact on your credit score, but it will run a ‘soft’ credit check, which checks basic details.

If that’s all good you can download the Yonder app and set up a proper account, which requires filling in some more details and linking your bank account. It took me around 15 minutes.

Your credit limit (how much you can spend on your card) is personal to you, and based on your spending data from your bank account and the Yonder card. You’ll get a set one initially, but within your app you can request to increase or decrease this if you like, and you’ll be reviewed again.

You can also increase your credit limit temporarily by adding money to your Yonder account, and however much you add will increase your limit. For instance, if you want to purchase something for £5,000, but only have a credit limit of £2,500, you can add £2,500 to your Yonder account to increase your credit limit to £5,000 for the purchase.

That's a bit complicated, but it makes sense for large purchases if you don’t quite have a big enough credit limit.

When you spend on your card, you are technically borrowing money from Yonder. This is fine if you pay back what you spend in full each month (highly recommended for credit cards), but if you don’t want to do that, you don’t have to, and instead you will be charged interest on the amount you borrow.

The interest rate can vary, but on the paid plan, it’s 29.32%, excluding the monthly fee (£15 per month). And on the free plan it's 32.26%. That’s how much you’ll pay if you were to borrow the money for a whole year (not accounting for interest to be paid on the interest).

That’s pretty normal compared to most credit cards, for instance American Express Gold (which also has a monthly fee) is currently 30%.

There’s two plans with Yonder, a free plan and a paid plan, which they call a membership. To get all of the perks you’ll need to be a member. Let’s run through both.

Cost: £15 per month (£160 per year)

You can cancel whenever you like too, there’s no fixed period that you must sign up for.

If you want to try the paid membership for a month first, get one month free and 10,000 bonus points when you sign up on the Yonder website¹.

With Yonder, as it’s a credit card, you’ll have Section 75 protection on purchases over £100. This means the credit card provider also gives you protection should something go wrong with your purchase (alongside the retailer), such as you don’t receive any item when buying online.

That means you can claim directly from the credit card provider to get your money back, increasing your chances of success, rather than only the retailer (e.g. a shop) if you were just using your bank debit card.

The customer support is good. It’s all within the app itself and on their website over live chat, or you can email in. Unfortunately there’s no phone support.

The response times are pretty good and it runs 24/7.

There’s a decent help center on the Yonder website¹ with pretty much everything covered too.

Yes, it’s safe to use Yonder.

Yonder is authorised and regulated in the UK by the Financial Conduct Authority (FCA), which means they have been reviewed and approved to provide you with a credit card.

Customers really like Yonder, particularly for the rewards and the travel perks, such as no currency conversion fees.

Customers mention the rewards are actually things you would use and love the variety. And there’s lots of mentions of using it for travel.

On Trustpilot it’s rated 4.6 out of 5, from over 1,450 ratings, which is very high (it’s officially excellent).

Here’s a quick recap and the pros and cons of Yonder:

We like Yonder a lot. It’s a great modern credit card company, perfect for those who regularly spend and like to enjoy life, such as holidays, eating out, going to shows etc.

Why not start earning rewards if you are going to spend anyway? And with the extra addition of having a card that has no fees abroad, and travel insurance too.

If you use the rewards regularly, you’ll earn more than the monthly fee, so in theory it pays for itself. And if you don’t think you’ll use the rewards, you can still get a free card for the extra benefits (like travel).

Plus, extra protection on your spending as it’s a credit card, and it builds your credit rating too. Lots of people use a credit card to pay for pretty much everything and then pay it off at the end of the month automatically.

If you like the rewards, it’s probably one of the best cards for travelling too, with no hidden conversion fees and can be used pretty much everywhere.

The customer support is good if anything should go wrong (24/7), and the app is nice to use and feels smooth, allowing you to browse all the rewards and offers.

Overall, we’re giving it a solid 5 stars for a credit card. It’s definitely worth checking out and at least trialling for a month to check out the rewards, and maybe take it on holiday too.

You can get a month free and up to 10,000 bonus points if you sign up on the Yonder website¹.

You'll need to be over 18 & a UK resident to apply and your approval will be based on some financial info you share with us. If you're approved, a £15 membership fee applies to the full membership. Use points towards experiences, fair use limits apply. Travel cover subject to booking with your Yonder card, eligibility and exclusions. Please only spend what you can afford to pay back. The representative rate is 66.0% APR variable for the full membership and 32.3% for the free membership. Travel insurance cover subject to booking with your Yonder card, eligibility and exclusions. For more information, plus other T&Cs, check out yonder.com

Try Yonder for a month, and get up to 10,000 bonus points to spend too.

Try Yonder for a month, and get up to 10,000 bonus points to spend too.

Try Yonder for a month, and get up to 10,000 bonus points to spend too.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Try Yonder for a month, and get up to 10,000 bonus points to spend too.